Humic-based Biostimulants Market Outlook:

Humic-based Biostimulants Market size was valued at USD 645.6 million in 2025 and is projected to reach USD 1.51 billion by the end of 2035, rising at a CAGR of 8.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of humic-based biostimulants is evaluated at USD 703.1 million.

The humic-based biostimulants market is positioned within the broader expansion of sustainable agricultural inputs supported by the soil degradation trends and fertilizer efficiency mandates documented by the multilateral and national agencies. According to the Food and Agriculture Organization, May 2024 data, nearly 33% of the global soils are moderately to highly degraded, directly affecting crop productivity and nutrient uptake. Moreover, the World Bank Group 2026 data has reported that the global consumption of fertilizers reached 134.2 kilograms per hectare in 2022, reflecting the sustained dependence on nutrient inputs. On the other hand, the increasing regulatory and agronomic pressure to improve nutrient use efficiency and reduce environmental losses is accelerating institutional adoption of soil-enhancing amendments across regulated agricultural markets globally.

In the emerging agricultural economies, the humic-based biostimulants market demand is closely linked to the soil health programs and balanced fertilization initiatives. In India, the Department of Fertilizers, 2023 to 2024, indicated that the total consumption of fertilizers was around 60 lakh metric tons, alongside the Soil Health Card scheme, which covers a million soil samples analyzed to promote site-specific nutrient management. Further, the USDA October 2023 data shows that the U.S. farm sector cash receipts exceeded USD 555 billion, reflecting sustained purchasing capacity for crop input technologies. These institutional frameworks, combined with rising scrutiny on nutrient runoff under the U.S. EPA’s water quality programs, are influencing distributors and agronomic service providers to incorporate humic-based formulations into integrated crop management portfolios.

Key Humic-based Biostimulants Market Insights Summary:

Regional Highlights:

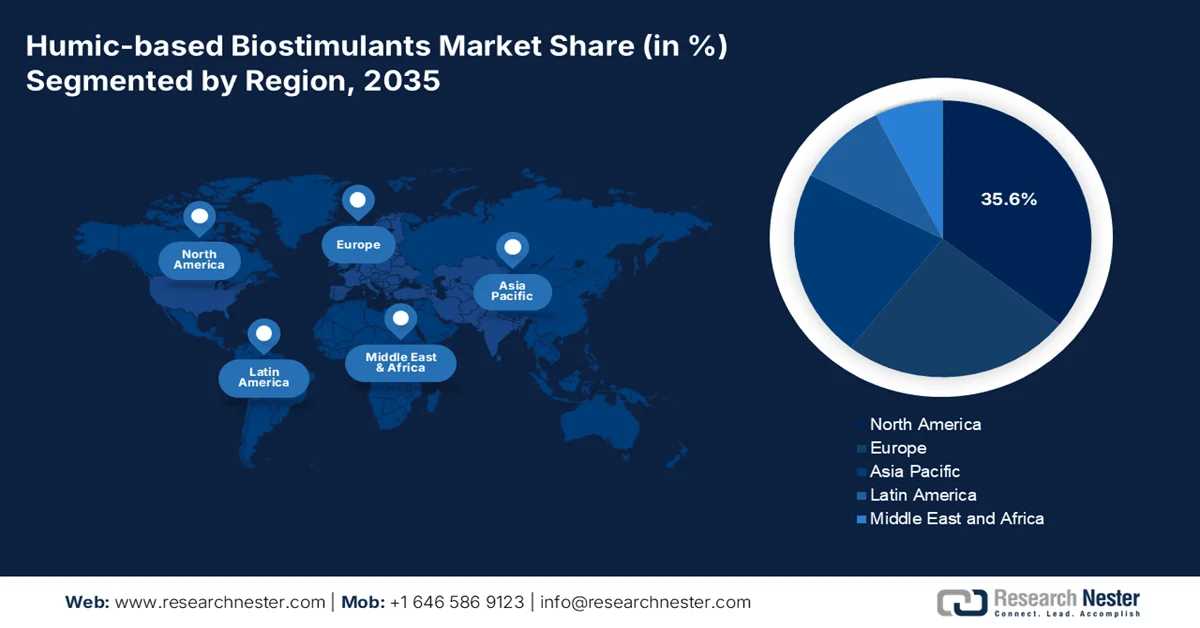

- North America in the humic-based biostimulants market is anticipated to command a 35.6% revenue share by 2035, attributed to large-scale row crop adoption and conservation program funding

- Asia Pacific is forecasted to grow at a CAGR of 14.8% during 2026–2035, fueled by government fertilizer reduction mandates and large-scale smallholder adoption

Segment Insights:

- The Indirect Sales segment of the humic-based biostimulants market is projected to account for a dominant 70.4% share by 2035, propelled by the entrenched purchasing habits of the global farmer base

- The Leonardite segment is anticipated to retain the largest share in the market by 2035, owing to its superior chemical and economic properties

Key Growth Trends:

- Growth in organic farming

- Rising investment in agriculture productivity

Major Challenges:

- Raw material sourcing and quality consistency

- High R&D and efficacy validation costs

Key Players: BASF SE, UPL Limited, FMC Corporation, Haifa Group, Valagro, Tradecorp, Biolchim S.p.A., Grownics, Humintech GmbH, Helios Group, Lallemand Inc., Omex Agrifluids.

Global Humic-based Biostimulants Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 645.6 million

- 2026 Market Size: USD 703.1 million

- Projected Market Size: USD 1.51 billion by 2035

- Growth Forecasts: 8.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, India, Germany, Brazil

- Emerging Countries: Japan, Canada, Australia, South Korea, Malaysia

Last updated on : 24 March, 2026

Humic-based Biostimulants Market - Growth Drivers and Challenges

Growth Drivers

- Growth in organic farming: Expansion of certified farmland increases the demand for non-synthetic soil inputs, driving the growth of the humic-based biostimulants market. According to the CABI August 2025 data, the global organic farmland exceeded 77 million hectares. The European Commission reports continued growth in the organic area under the CAP support measures. In the U.S., the USDA-certified organic sales surpassed USD 60 billion in 2022. Further, the policy-backed organic transition payments are encouraging the farmers to adopt soil-enhancing inputs compatible with the organic standards. Moreover, the certification alignment and compliance documentation are critical for accessing procurement channels in regulated organic supply chains. Additionally, national organic action plans across EU member states are accelerating input standardization and traceability requirements.

- Rising investment in agriculture productivity: National agricultural budgets are expanding to secure food supply resilience. According to the PRS India February 2025 data, India’s Union Budget 2025 to 2026 allocated over USD 14.9 million to the Ministry of Agriculture and Farmers Welfare. Further, the FAO highlights that increasing public investment is needed to close productivity gaps. Government-backed extension services are promoting the integrated nutrient management, indirectly expanding the demand for soil-enhancing amendments. Additionally, the Indian Council of Agricultural Research continues to strengthen field-level demonstrations and soil-based advisory services to improve nutrient use efficiency across major cropping systems. Such public expenditure frameworks are reinforcing structured procurement channels for agronomic inputs aligned with national productivity and sustainability targets.

- Food security and yield stabilization initiatives: The global food demand pressures are driving the investment in yield resilience. The FAO projects that global food production must rise significantly to meet the future population's needs. The World Bank finances agricultural resilience projects across developing economies. Further, the global humic-based biostimulants market is expected to grow steadily, supported by expanding public spending on soil restoration and climate-smart agriculture in Asia and Europe. Yield stabilization under drought and nutrient stress conditions is increasingly prioritized within government-backed agronomy programs. National food security missions are integrating the soil health interventions to reduce the climate induced production volatility.

Challenges

- Raw material sourcing and quality consistency: Securing consistent high-quality raw material, mainly leonardite, with optimal oxidation levels, presents a significant entry barrier in the humic based biostimulates market. New players struggle to secure long-term supply agreements with the mining operators. Further variations in the raw material quality directly impact the product efficacy, leading to inconsistent field results that damage brand reputation. Top companies address this challenge by partnership strengthening its capabilities.

- High R&D and efficacy validation costs: Demonstrating the product efficacy via scientific validation requires a substantial investment that challenges new market entrants in the humic-based biostimulants market. Researchers must now use metabolomics or genomics to pinpoint the substances that target specific metabolic pathways, moving beyond broad claims to precise demonstrations of stress tolerance or nutrient uptake improvement. This requires expensive laboratory equipment and extended field trial periods.

Humic-based Biostimulants Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.9% |

|

Base Year Market Size (2025) |

USD 645.6 million |

|

Forecast Year Market Size (2035) |

USD 1.51 billion |

|

Regional Scope |

|

Humic-based Biostimulants Market Segmentation:

Distribution Channel Segment Analysis

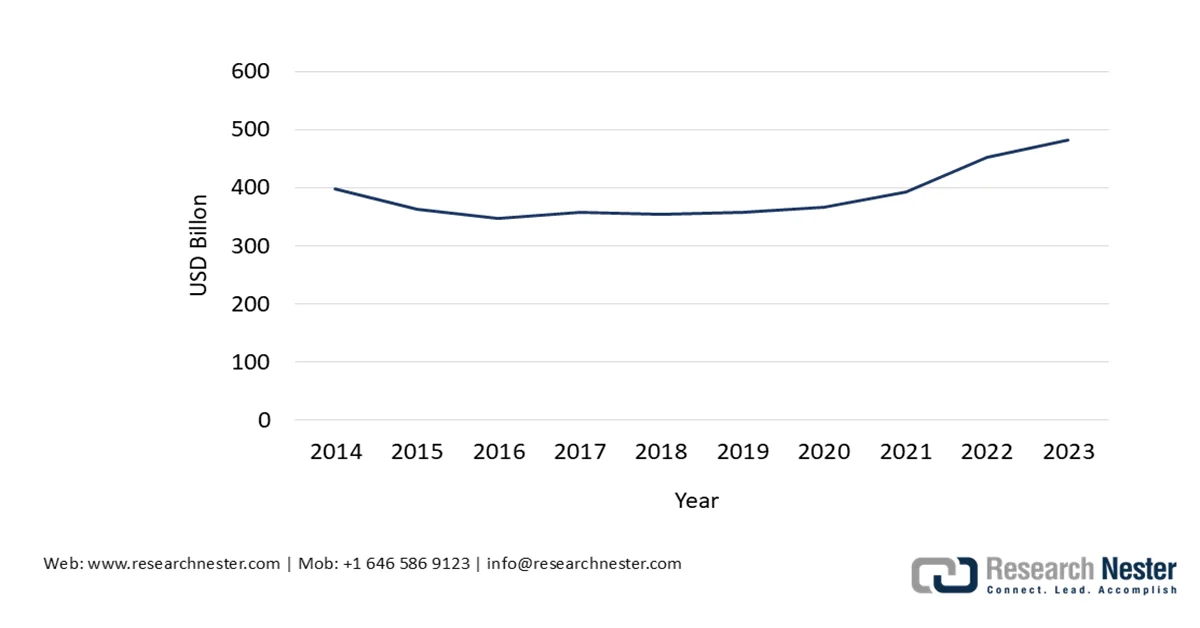

Under the distribution channel segment, the indirect sales are projected to capture the dominant 70.4% share value in the humic-based biostimulants market by the end of 2035. The segment is driven by the entrenched purchasing habits of the global farmer base. The majority of agricultural producers, mainly small to medium-scale farmers, rely on localized agricultural retailers, cooperatives, and distributors for their input purchases. These intermediaries provide crucial agronomic advice, product education, and the convenience of consolidating multiple farm inputs in a single trusted transaction. Further, the physical nature of the humic products, often heavy bags or large liquid containers, makes e-commerce a challenging option, reinforcing the preference for local suppliers. According to the USDA July 2024 data, the total farm expenditure reached USD 481.9 billion, reinforcing the demand for the local cooperatives and retailers, underscoring the resilience of this traditional channel despite the growth of digital platforms.

U.S. Farm Expenditure, through 2023

Source: USDA July 2024

Source Segment Analysis

Within the source segment, the leonardite is expected to maintain the largest share value in the humic-based biostimulants market by the end of 2035. The segment is driven by its superior chemical and economic properties. The leonardite is a highly oxidized form of lignite coal that is naturally rich in humic acids when compared to the softer sources such as peat or younger lignite. This high concentration translates directly into lower processing costs and higher efficacy for manufacturers, making it the preferred feedstock for commercial-grade biostimulant production. Its consistent molecular structure also allows for the creation of standardized, predictable products, a key requirement for large-scale agricultural buyers. The strategic importance of this resource is indicated by the production strengthening its role as a critical mineral for the agricultural biologicals industry.

Form Segment Analysis

The liquid form segment is projected to garner a significant revenue share humic-based biostimulants market during the assessed timeline and is driven by the global agricultural shift toward precision farming and mechanized irrigation. Liquid humic acids offer unparalleled versatility as they can be easily mixed with the liquid fertilizers and applied via drip irrigation systems or as foliar sprays. This allows for targeted application directly to the root zone or leaf surface, maximizing plant uptake and minimizing waste. Farmers prefer liquids because they eliminate the dust and handling difficulties associated with dry powders, ensuring safer and more efficient field operations. The growing adoption of center pivot irrigation in water-stressed regions further accelerates this trend.

Our in-depth analysis of the humic-based biostimulants market includes the following segments:

|

Segment |

Subsegments |

|

Form |

|

|

Source |

|

|

Mode of Application |

|

|

Crop Type |

|

|

Function |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Humic-based Biostimulants Market - Regional Analysis

North America Market Insights

North America is projected to hold the largest share and is poised to hold the regional revenue share of 35.6% by the end of 2035. The humic-based biostimulants market in North America is driven by the large-scale row crop adoption and conservation program funding. The U.S. dominates the regional consumption due to its extensive corn, soybean, and wheat acreage, while Canada contributes via organic production expansion in the Prairie provinces. The primary drivers include USDA conservation incentive programs, state-level fertilizer reduction mandates, and increasing distributor adoption in the Midwest. The market is shifting toward liquid formulations compatible with the precision application equipment. Government cost-share programs under the Inflation Reduction Act are accelerating adoption among contract growers supplying major food processors.

The expanding public expenditure on soil health, conservation compliance, and climate-resilient agriculture is driving the humic-based biostimulants market in the U.S. As per the USDA February 2023 data, the Inflation Reduction Act funding allocated USD 19.5 billion to climate-smart agriculture programs, including soil carbon and nutrient management initiatives that directly influence demand for soil-enhancing inputs. Moreover, the USDA February 2026 data shows that the U.S. net farm income increased by 18.2% in 2025, reflecting sustained farm-level liquidity and input purchasing capacity. Furthermore, the Environmental Protection Agency (EPA) continues implementation of nutrient reduction strategies under the Clean Water Act, noting that agriculture remains a leading contributor to nutrient pollution in U.S. water bodies. These regulatory and funding frameworks are strengthening the adoption of integrated nutrient management practices across row and specialty crops and providing positive market growth.

The federal investments in sustainable agriculture, soil conservation, and climate adaptation are influencing the humic-based biostimulants market in Canada. According to the Government of Canada, July 20023 data, the Sustainable Canadian Agricultural Partnership (2023–2028) commits approximately USD 3.5 billion in federal-provincial funding to strengthen the environmental performance, including soil health and nutrient management initiatives. In addition, Statistics Canada's March 2023 data recorded total farm operating revenues of USD 117,163,851,064 in 2024, indicating stable producer spending capacity for crop inputs. Environment and Climate Change Canada continues to advance national targets for greenhouse gas reduction from agriculture, with programs supporting improved nutrient stewardship and soil carbon practices, enabling a stable market growth.

APAC Market Insights

The Asia Pacific is the fastest-growing region and is poised to expand at a CAGR of 14.8% during the assessed period, 2026 to 2035. The humic-based biostimulants market in APAC is driven by the government fertilizer reduction mandates and large-scale smallholder adoption. The region’s dominance stems from the concentrated agricultural economies in China and India, where national programs actively promote soil health restoration. Moreover, the Asian Productivity Organization, via its member governments, has reported that there is an increase in biostimulant field trials across the region, indicating accelerating institutional acceptance. Agricultural cooperatives and state marketing federations are emerging as primary procurement channels. Japan and South Korea lead in precision application technologies, while Malaysia's palm oil sector represents concentrated plantation demand.

The national policy measures targeting fertilizer efficiency, soil restoration, and agricultural modernization are propelling the humic-based biostimulants market in China. According to the People's Republic of China, December 2023 data, the country’s total grain output reached 695.41 million tons in 2023, reflecting sustained production intensity across major cropping regions. Further, the Ministry of Agriculture and Rural Affairs has continued implementation of the Zero Growth in Chemical Fertilizer Use initiative, promoting improved nutrient management and soil quality enhancement. On the other hand, China’s central government allocated a certain amount toward agriculture, forestry, and water affairs expenditure, reinforcing funding for sustainable land management and rural revitalization. These regulatory and fiscal frameworks are promoting the integration of soil conditioning inputs, particularly as regional authorities emphasize the reduction of nutrient losses and the restoration of soil organic matter to stabilize yields under climate variability.

The humic-based biostimulants market in Japan is driven by the national policies focused on sustainable agriculture, soil conservation, and productivity optimization. According to the Statistical Handbook of Japan 2025 data, Japan’s total agricultural output was valued at USD 60.4 billion in 2023, reflecting continued investment capacity within high-value horticulture and rice segments. Moreover, the Government of Japan allocated a budget to the agriculture, forestry, and fisheries budget supporting smart agriculture, soil improvement, and environmentally friendly farming practices. These structural priorities are encouraging adoption of soil-conditioning inputs that enhance nutrient uptake efficiency and crop quality across rice, vegetables, and specialty crop systems under sustainability-linked subsidy programs.

Total Agriculture Output

|

Category |

2019 |

2020 |

2021 |

2022 |

2023 |

|

Total |

8,894 |

8,937 |

8,838 |

8,998 |

9,495 |

|

Crops |

5,630 |

5,656 |

5,378 |

5,477 |

5,723 |

|

Rice |

1,743 |

1,643 |

1,370 |

1,395 |

1,519 |

|

Vegetables |

2,152 |

2,252 |

2,146 |

2,229 |

2,324 |

|

Fruits and Nuts |

840 |

874 |

916 |

923 |

959 |

|

Livestock and Its Products |

3,211 |

3,237 |

3,405 |

3,465 |

3,721 |

|

Beef Cattle |

788 |

739 |

823 |

826 |

770 |

|

Dairy Cattle |

919 |

925 |

922 |

901 |

925 |

|

Pigs |

606 |

662 |

636 |

671 |

719 |

|

Chickens |

823 |

833 |

936 |

969 |

1,203 |

Source: Statistical Handbook of Japan 2025

Europe Market Insights

Europe represents a mature and regulated humic-based biostimulants market and is driven by the European Green Deal’s target of reducing fertilizer use. The European Commission’s Farm to Fork Strategy creates procurement demand for inputs that enhance nutrient use efficiency, with humic substances positioned as compliant solutions. The market growth is concentrated in Mediterranean horticulture regions and Western Europe arable farming areas. Government-funded advisory programs, including the European Innovation Partnership for Agricultural Productivity and Sustainability, provide matching grants for farmer-led trials. The European Commission's Joint Research Centre published extensive guidance on the biostimulant efficacy evaluation, creating verification frameworks for institutional buyers.

The structured public funding for sustainable agriculture and soil protection is shaping the humic-based biostimulants market in Germany. According to the BMLEH December 2024 data, approximately USD 7.18 billion annually is allocated to agricultural support measures, including eco schemes linked to soil conservation and nutrient efficiency. Further agricultural production is indicating a stable farm-level input expenditure capacity. Moreover, the BMLEH February 2024 data highlights that agriculture accounts for around 8% of Germany’s total greenhouse gas emissions, reinforcing policy emphasis on soil carbon management and improved nutrient stewardship. These regulatory and funding structures are supporting demand for soil-enhancing inputs within cereals, oilseeds, and specialty crop systems, particularly as compliance with nitrate reduction and climate mitigation targets becomes increasingly integrated into farm-level subsidy frameworks.

The humic-based biostimulants market in UK is influenced by agricultural policy reforms prioritizing soil health and environmental land management. According to the UK Parliament's January 2022 data, the Environmental Land Management schemes have allocated USD 3.20 billion annually to support sustainable farming practices, including soil improvement and nutrient management measures. Moreover, the UK Government’s Agricultural Transition Plan outlines progressive replacement of direct payments with sustainability-linked incentives, reinforcing demand for soil-enhancing agronomic inputs. The Office for National Statistics reported that UK agriculture contributed approximately USD 18.6 billion in gross value added, reflecting continued operational investment capacity within the sector. These funding mechanisms and regulatory frameworks are driving the adoption of integrated soil management strategies across cereals, oilseeds, and horticulture segments, particularly as compliance with nutrient stewardship and soil carbon targets becomes embedded within farm support payments and procurement structures.

Key Humic-based Biostimulants Market Players:

- BASF SE (Germany)

- UPL Limited (India)

- FMC Corporation (U.S.)

- Haifa Group (Israel)

- Valagro (Italy)

- Tradecorp (Spain)

- Biolchim S.p.A. (Italy)

- Grownics (South Korea)

- Humintech GmbH (Germany)

- Helios Group (Australia)

- Lallemand Inc. (Canada)

- Omex Agrifluids (UK)

- BioAg Pty Ltd (Australia)

- Black Earth Humic (U.S.)

- Humic Growth Solutions (Canada)

- Agriculture Solutions Inc. (U.S.)

- MaxGrowth LLP (India)

- Sumitomo Chemical Co., Ltd. (Japan)

- BioPrime AgriSolutions (India)

- HGS BioScience (USA)

- ProdOz (Australia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BASF SE, a Germany chemical giant, leverages its massive agricultural division to maintain a leading position in the humic-based biostimulants market. The company has strategically integrated humic substances into its broader portfolio of crop protection and seed solutions, emphasizing the concept of agricultural solutions. By investing in R&D, the company focuses on standardized, highly effective humic formulations to improve the nutrient uptake efficiency.

- UPL Limited has captured a significant share in the humic-based biostimulants market via its aggressive local-to-global strategy. The company utilizes its vast manufacturing base to produce cost-effective humic acid products derived from the leonardite, making them accessible to price-sensitive markets. UPL’s strategic focus is on sustainability and circularity, often positioning its natural humic extracts as an essential tool for soil health restoration.

- FMCC Corporation has strengthened its position in the humic based biostimulats market by focusing on innovation and proprietary formulation technologies. Recognizing the shift toward integrated pest and crop management, FMC has incorporated humic acid-based products into its biologicals portfolio to complement its strong chemical synthesis heritage.

- Haifa Group is renowned in the humic-based biostimulants market for its specialized high-quality products that often combine humic acids with controlled-release fertilizers. The company’s strategy revolves around precision nutrition, where humic-based biostimulants are used to enhance the efficiency of its primary potassium nitrate and speciality fertilizers lines. In 2024, the company has reduced 28% of the carbon footprint.

- Valagro, now a part of the Corteva Agriscience group, is a pure play leader in the biologicals sector with a strong emphasis on the humic-based biostimulants market. Renowned for its high-tech formulations, the company uses raw materials to create products under its brand that are known for purity and consistent molecular weight. In 2024, the company made a total sales of USD 16,981 million.

Here is a list of key players operating in the global humic-based biostimulants market:

The global humic-based biostimulants market is highly fragmented and is defined by a mix of large multinational agricultural corporations and specialized regional players. The competitive landscape is driven by intensive research and development focused on efficacy and formulation technologies such as micronutrient enrichment and compatibility with synthetic fertilizers. The key strategic initiatives include mergers and acquisitions to expand geographic footprints and product portfolios, as well as partnerships with distribution networks to penetrate new markets such as the Asia Pacific. In March 2022, Valagro launched its innovative biostimulant Talete in the Indian market. Companies are increasingly investing in clinical trials and scientific validation to differentiate their products in a crowded market, responding to the rising global demand for sustainable agriculture and higher crop yields.

Corporate Landscape of the Humic-based Biostimulants Market:

Recent Developments

- In February 2026, BioPrime AgriSolutions secures regulatory approval for its Biostimulants portfolio. This regulatory clearance encompasses the full spectrum of biostimulants categories, including Humic Fulvic Acid, Seaweeds, Botanicals, Amino Acids and various other combinations for proprietary foliar and granular applications.

- In October 2025, HGS BioScience, a leading provider in humic and fulvic products has announced the acquisition of NutriAg Ltd., a Toronto-based innovator in bionutritional technologies.

- In February 2025, ProdOz announced the launch of a new enhanced efficiency fertilizer after promising trials. ProdOz crop science technologist Zenon Kynigos said Fertica H+ was developed specifically to improve Australian soil health and support sustainable farming practices.

- Report ID: 8464

- Published Date: Mar 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Humic-based Biostimulants Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.