Green Composites Market Outlook:

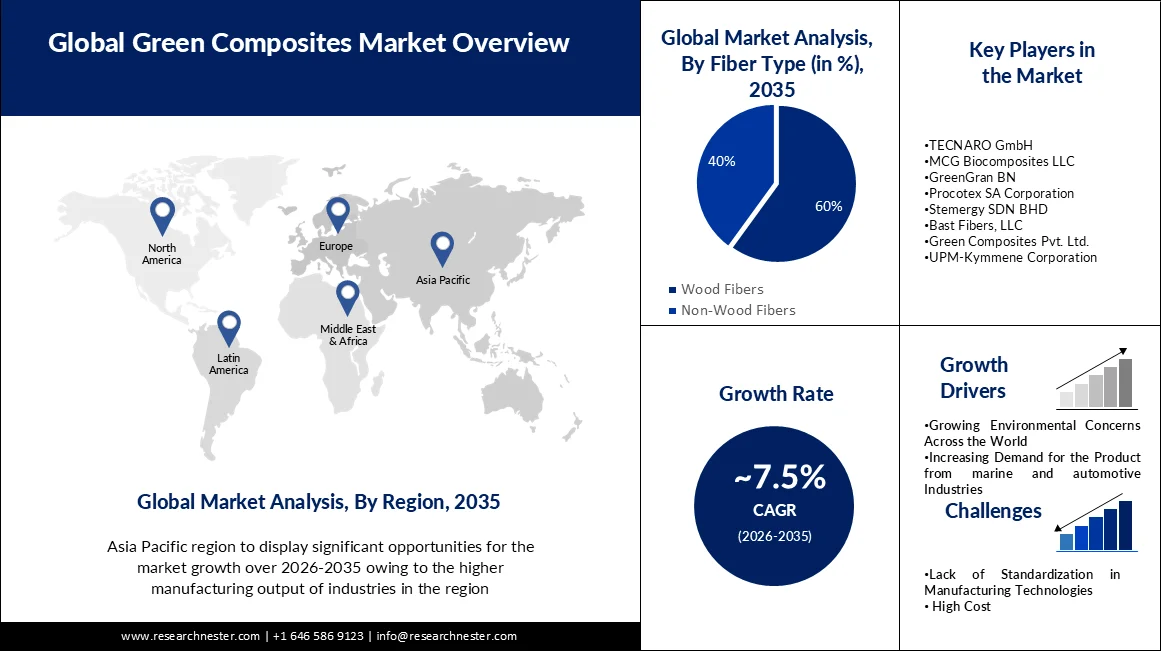

Green Composites Market size was valued at USD 34.27 billion in 2025 and is set to exceed USD 70.63 billion by 2035, registering over 7.5% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of green composites is evaluated at USD 36.58 billion.

Governments around the world are introducing regulations to reduce carbon emissions and encourage the use of environmentally friendly materials. These regulations and initiatives consist of tax benefits, subsidies, and incentives for industry players to adopt eco-friendly sustainable solutions such as green composites. For instance, the European Union has set a goal of reducing greenhouse gas emissions by 55% by 2030, and using eco-friendly composite materials can help achieve these goals.

Consumers are becoming increasingly aware of the environmental impact of the products they use. Therefore, nowadays consumers are highly watchful of what they are purchasing and consuming. As a result, there is a growing demand for sustainable and environmentally friendly products, including eco-friendly composite materials. Also, manufacturers and producers are responding to this demand of customers and as a result, they implementing green composites in their products as per customer preference. Research shows that 60% of consumers worldwide consider sustainability when making purchasing decisions.

Key Green Composites Market Insights Summary:

Regional Highlights:

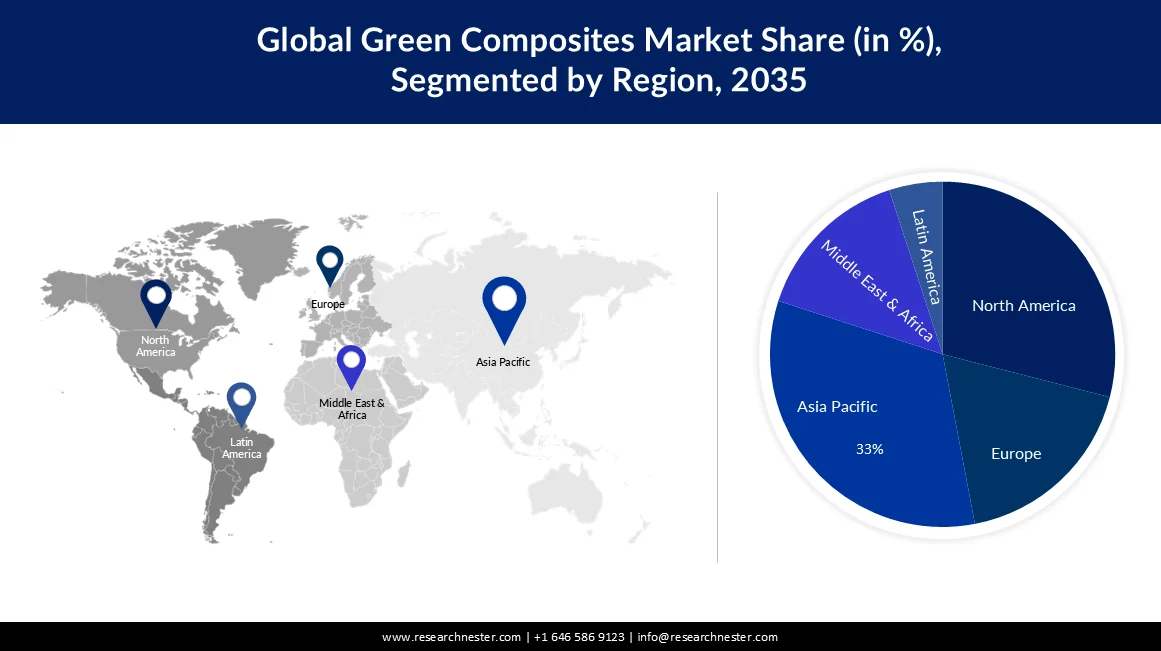

- Asia Pacific green composites market is projected to account for the largest revenue share of 33% by 2035, driven by high manufacturing output across construction, automotive, and defense industries alongside rising urbanization and population growth

- North America is anticipated to witness substantial expansion by 2035, attributed to stringent government regulations on low-emission products and increasing demand from the growing aerospace industry

Segment Insights:

- In the green composites market, the construction segment is projected to expand at nearly 30% growth rate during 2026–2035, propelled by stricter environmental regulations and rising demand for energy-efficient buildings

- The wood fiber segment is expected to register the highest CAGR of 60% by 2035, fueled by increasing utilization across packaging and construction industries

Key Growth Trends:

- Growing Environmental Concerns Across the World

- Increasing Product Demand from Marine, and Automotive Industries

Major Challenges:

- High in Cost

- Lack of Standardization in Manufacturing Technologies

Key Players: of Fassisi GmbH, Bionote USA Inc., Swissavans AG., MEGACOR Veterinary Diagnostics, Woodley Equipment Company Ltd..

Global Green Composites Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 34.27 billion

- 2026 Market Size: USD 36.58 billion

- Projected Market Size: USD 70.63 billion by 2035

- Growth Forecasts: 7.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (33% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: China, United States, Germany, Japan, France

- Emerging Countries: China, India, Japan, South Korea, Germany

Last updated on : 25 February, 2026

Green Composites Market - Growth Drivers and Challenges

Growth Drivers

-

Growing Environmental Concerns Across the World - Growing environmental concerns around the world are driving the green composites market as consumers and industry seek sustainable and environmentally friendly alternatives to traditional materials. The United Nations Environment Program (UNEP) has identified green composites as a promising solution to environmental problems. UNEP recognizes the potential of green composites to reduce greenhouse gas emissions, reduce waste and improve resource efficiency.

-

Increasing Product Demand from Marine, and Automotive Industries – Demand for environmentally friendly composite materials from various industries such as marine, and automotive industries due to their benefits in terms of sustainability, weight reduction, and performance enhancement is growing rapidly. Reportedly, with the help of lightweight materials such as green composites a 10% reduction in vehicle weight has the potential to improve fuel efficiency by 6% to 8%.

- Growing Focus on Green Composites by Market Players – A large number of market players are substituting fossil feedstock with bio-based food ingredients materials. Therefore, manufacturers are focusing on incorporating biodegradable substitutes in their products as a result of the demand for green and sustainable products by consumers.

Challenges

-

High in Cost - Green composites can be more expensive than traditional materials, making them less competitive in price-sensitive markets. Manufacturers need to find ways to reduce production costs and enhance economies of scale to make green composites more cost-effective.

-

Lack of Standardization in Manufacturing Technologies

- Technical Limitations

Green Composites Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.5% |

|

Base Year Market Size (2025) |

USD 34.27 billion |

|

Forecast Year Market Size (2035) |

USD 70.63 billion |

|

Regional Scope |

|

Green Composites Market Segmentation:

End Use Industry Segment Analysis

Green composites market from the construction segment is predicted to observe nearly 30% growth rate between 2026-2035. Green composites can be used in a variety of architectural applications such as walls, roofs, and floors. In addition, the demand for green composite materials in the construction industry is expected to grow in the coming years due to factors such as stricter environmental regulations, growing awareness of sustainability, and the need for energy-efficient buildings. Environmentally friendly composite materials are also used to retrofit and refurbish existing buildings as they help improve energy efficiency and reduce carbon footprint. For instance, a project in the Netherlands refurbished a historic building with green composite insulation panels, saving up to 70% of energy.

Fiber Type Segment Analysis

The wood fiber segment in the green composites market is poised to hold the largest CAGR of 60% by the end of 2035. The use of wood fiber composites in various industries such as packaging, construction is estimated to boost the segment’s growth in the market. The use of wood fiber composites in the construction industry is increasing due to their advantages such as high strength, durability, and lightweight. Reducing vehicle weight with wood fiber composites can improve fuel efficiency and reduce carbon emissions.

Our in-depth analysis of the global green composites market includes the following segments:

|

Fiber Type |

|

|

End User Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Green Composites Market - Regional Analysis

APAC Market Insights

Asia Pacific industry is likely to account for largest revenue share of 33% by 2035. The market is expanding with the high manufacturing output of industries in the region, mainly construction, automotive, and defense. Population growth and urbanization in the region are increasing the demand for eco-friendly materials in these industries, creating opportunities for eco-friendly composites.

North American Market Insights

The green composites market in the North America region is expected to grow significantly in the near future. This can be credited to stringent government initiatives to regulate the use of low-emission products in the region. In addition, the strong footprint of market players is also forecasted to propel market growth in the region in the future. In addition, the increasing demand for high-performance composite materials, followed by the growing aerospace industry in the region, is projected to elevate the growth of the market in the North America region. As per the International Trade Administration U.S. Department of Commerce, the aero trade balance increased to USD 77,590 million in 2019 from USD 54,937 million in 2010.

Green Composites Market Players:

- ALPAS Srl

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- TECNARO GmbH

- MCG Biocomposites LLC

- GreenGran BN

- Procotex SA Corporation

- Stemergy SDN BHD

- Bast Fibers, LLC

- Green Composites Pvt. Ltd.

- UPM-Kymmene Corporation

- Wienerberger AG

Recent Developments

- November 2021- Weinerberger declared that it decided to spend about USD 70 million in 2021 to boost efficiency at its plants in Europe and North America. The company is already almost halfway toward its 2023 goal of cutting carbon dioxide emissions by 15% compared to levels last year.

- June 2021- Procotex announced that it will acquire the short Carbon fiber business of ELG UK. The acquisition is part of the company’s continuous innovative efforts toward a sustainable future.

- Report ID: 3888

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.