Graphite Electrodes Market Outlook:

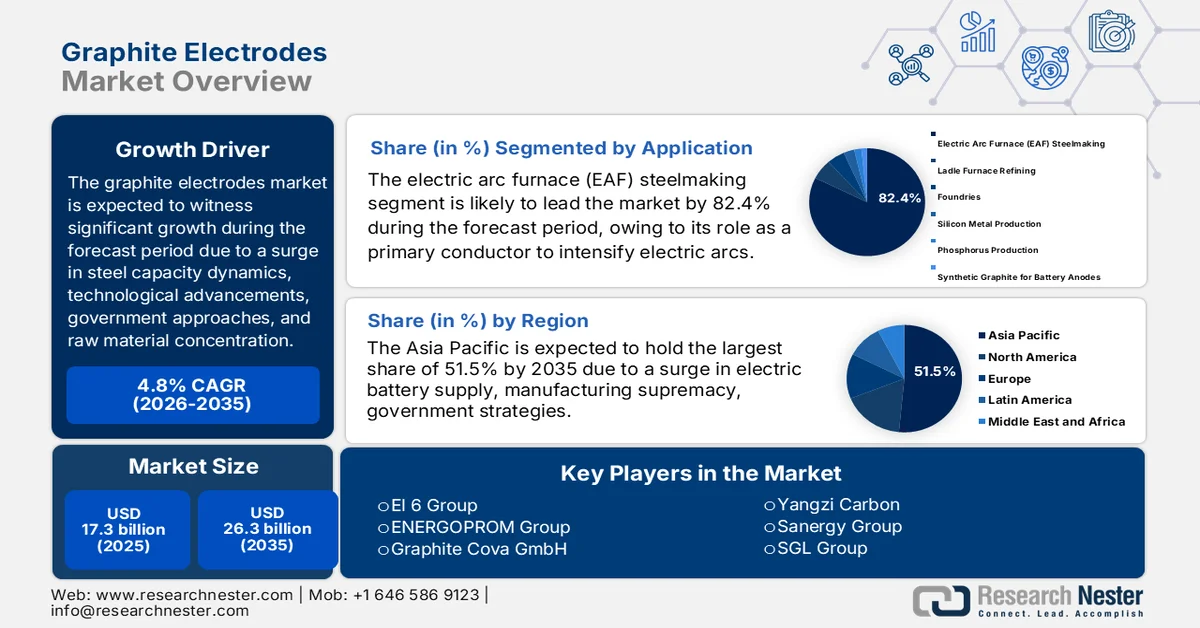

Graphite Electrodes Market size was valued at over USD 17.3 billion in 2025 and is expected to reach USD 26.3 billion by the end of 2035, growing at a CAGR of 4.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of graphite electrodes is evaluated at USD 18.1 billion.

The worldwide graphite electrodes market is being significantly reshaped by suitable factors expanding beyond conventional steel industrial dynamics. These factors include shifting geopolitical imperatives, technological discontinuities, emerging applications, trade protectionism, regional government initiatives, and raw material concentration. According to official statistics published by the IEA Organization in 2025, there has been a rise in the demand for lithium minerals by almost 30%, which has significantly exceeded the 10% yearly growth rate. Likewise, the demand for rare earths, graphite, cobalt, and nickel also increased by 6% to 8% as of 2024. Moreover, for battery-based metals, such as graphite, cobalt, and nickel, the energy industry accounted for 85% of the overall demand growth. Besides, the continuous investment in critical minerals mining is also responsible for boosting the graphite electrodes market across different countries.

Investment Analysis in Critical Minerals Mining (2021-2024)

|

Mineral Type |

2021 (USD Billion) |

2022 (USD Billion) |

2023 (USD Billion) |

2024 (USD Billion) |

|

Diversified Major |

18.9 |

22.7 |

25.2 |

28.8 |

|

Copper, Nickel, and Cobalt Specialist |

13.4 |

18.5 |

19.6 |

16.7 |

|

Lithium Specialist |

2.9 |

4.4 |

7.1 |

9.1 |

Source: IEA Organization

Furthermore, the artificial intelligence integration in electrode manufacturing, diversification into lithium-ion battery applications, focus on low-emission and energy-efficient electrode production, aerospace and defense applications as an emerging demand source, along with expansion in ferroalloy and silicon production, are trends that are driving the graphite electrodes market globally. As stated in an article published by NLM in March 2025, to ensure electrode manufacturing, industries and nations have initiated projects, such as Japan’s NEDO RISING II, China’s Made in China 2025, and the U.S. Department of Energy’s Battery 500, jointly targeting energy densities surpassing 500 W h kg−1 by the end of 2030. Besides, advances, including high-voltage electrolytes, silicon-based anode materials, and high-nickel cathode materials, have enabled lithium-ion batteries to gain energy densities of an estimated 300 W h kg−1 for commercial applications and almost 350 W h kg−1 in the laboratory scale, thus making it suitable for uplifting the market.

Key Graphite Electrodes Market Insights Summary:

Regional Highlights:

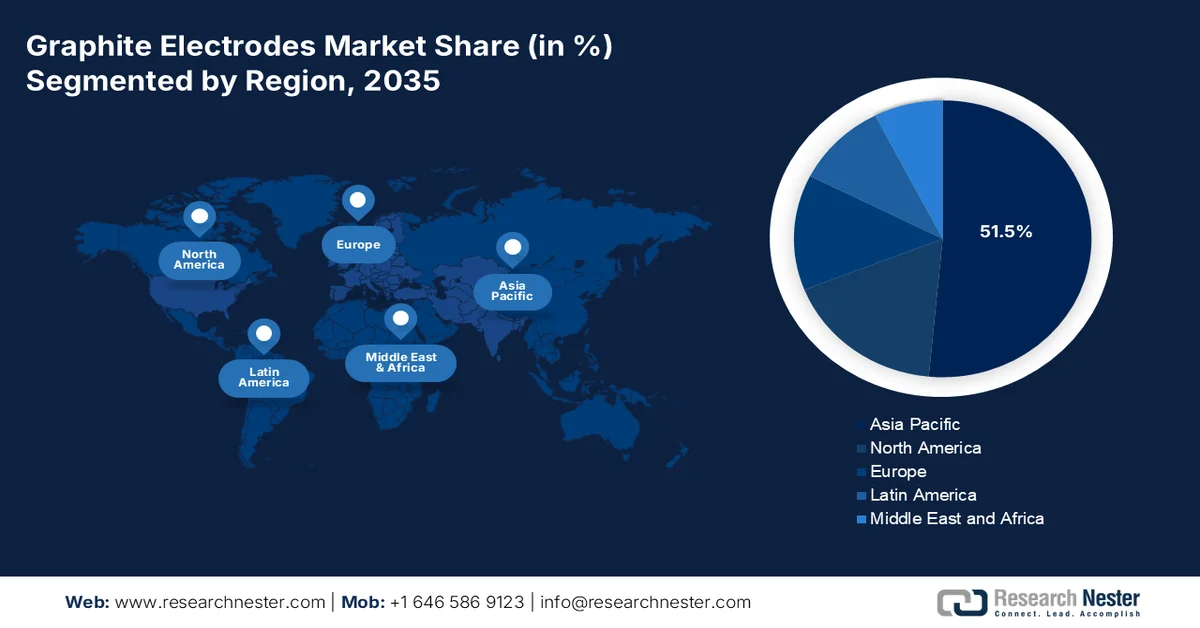

- The Asia Pacific graphite electrodes market is projected to secure a 51.5% share by 2035, strengthened by the region’s extensive manufacturing dominance and mineral production ecosystem supporting industrial supply chains.

- Europe is anticipated to witness the fastest expansion during 2026–2035, accelerated by the carbon border adjustment mechanism and the region’s accelerating transition toward green steel production.

Segment Insights:

- The Electric Arc Furnace (EAF) Steelmaking segment in the graphite electrodes market is expected to capture 82.4% share by 2035, attributed to its fundamental function as the primary conductor enabling the generation of high-intensity electric arcs for scrap steel melting.

- The Steel Industry segment is likely to hold the second-largest share during 2026–2035, stimulated by its reliance on graphite electrodes as essential conductors of high-voltage electricity for melting scrap metal in EAF processes.

Key Growth Trends:

- Increase in high-quality steel demand

- Surge in non-ferrous metals production

Major Challenges:

- Raw material supply concentration and geopolitical vulnerability

- Structural oversupply and irrational pricing pressure

Key Players: Resonac (Japan), GrafTech International (U.S.), Tokai Carbon (Japan), Showa Denko K.K (Japan), Nippon Carbon Co., Ltd (Japan), SEC Carbon, Ltd (Japan), Fangda Carbon New Materials Technology Co., Ltd. (China), Graphite India Limited (GIL) (India), HEG Limited (India), Jilin Carbon Group Ltd (China), Kaifeng Carbon Co., Ltd (China), Kaifeng Pingmei (China), Nantong Yangzi Carbon Co., Ltd. (China), Yangzi Carbon (China), Sanergy Group (China), SGL Group (Germany), El 6 Group (France), ENERGOPROM Group (Russia), Graphite Cova GmbH (Germany), Redox (Australia), Graphite India Limited (India).

Global Graphite Electrodes Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 17.3 billion

- 2026 Market Size: USD 18.1 billion

- Projected Market Size: USD 26.3 billion by 2035

- Growth Forecasts: 4.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (51.5% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: China, United States, Japan, Germany, India

- Emerging Countries: South Korea, Australia, Vietnam, Indonesia, Brazil

Last updated on : 12 March, 2026

Graphite Electrodes Market - Growth Drivers and Challenges

Growth Drivers

- Increase in high-quality steel demand: This particular demand is characterized by stringent adherence to composition standards, consistent performance characteristics, and superior physical properties, which is fueling the graphite electrodes market. According to official statistics published by OECD in May 2025, there has been a substantial increase in the steelmaking capacity by almost 6.7%, which is equivalent to 165 million metric tons. In addition, Asia -based economies are projected to account for 58% of the newest capacity, which is led by a significant increase in China and India. Moreover, the cross-border investment is involved in nearly 16% of the overall tonnage, with China deliberately playing a crucial role in such investment, thereby making it suitable for boosting the market growth.

- Surge in non-ferrous metals production: The expansion of non-ferrous metal production, including zinc, nickel, copper, and aluminum, has created an electrode demand that is independent of steel industry cycles. Besides, as per an article published by the IEA Organization in March 2026, there has been a surge in copper prices that has briefly surpassed USD 14,600 per ton in January 2026, which has exceeded USD 12,000 per ton in December 2025. Therefore, these unprecedented price levels have been fueled by short-term developments, which include supply disruptions at different major mines and the development of U.S.-based copper inventories, owing to tariff uncertainty, which is responsible for bolstering the graphite electrodes market expansion.

- Focus on graphite energy storage: The explosive growth of the lithium-ion battery industry has created the mere demand for synthetic graphite, which is positively impacting the graphite electrodes market worldwide. As stated in an article published by the IEA Organization in May 2024, the clean tech demand for graphite accounts for 1,292 kilotons as of 2023, which is further expected to increase to 6,013 kilotons by the end of 2030 and 9,839 kilotons by 2040. Simultaneously, this particular mineral storage caters to 3,340 kilotons for other uses in 2023, which is also projected to account for 4,406 kilotons by 2030 and 6,185 kilotons by 2040. Besides, in terms of secondary reuse and supply, graphite energy storage accounts for 308 kilotons in 2023, along with 1,333 kilotons in 2030 and 2,489 kilotons in 2040, thereby supporting the graphite electrodes market expansion.

Challenges

- Raw material supply concentration and geopolitical vulnerability: The critical roadblock facing the graphite electrodes market is the extreme concentration of raw material supply, particularly needle coke, combined with escalating geopolitical tensions that threaten to disrupt access to critical inputs. Needle coke constitutes electrode production cost and relies on specialized petroleum refining capacity concentrated in a handful of plants globally. This concentration creates significant supply risk, exacerbated by three compounding factors, including competition from the lithium-ion battery sector for high-purity graphite, tightening environmental regulations in producing countries, and the weaponization of graphite supply chains for geopolitical advantage. The competition from battery manufacturers represents a structural shift in graphite demand that will only intensify.

- Structural oversupply and irrational pricing pressure: The most immediate and severe challenge confronting the graphite electrodes market is a profound structural oversupply that has driven pricing to unsustainably low levels, creating what industry executives describe as the most difficult market environment in nearly a decade. This oversupply is not primarily a demand-side problem but rather a supply-side imbalance driven by aggressive capacity expansion in China and India. The resulting market dynamics have become increasingly dysfunctional, with competitor pricing behavior described as increasingly aggressive and arguably irrational as exports from these manufacturing powerhouses flood global markets at prices that undercut production costs for established manufacturers.

Graphite Electrodes Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.8% |

|

Base Year Market Size (2025) |

USD 17.3 billion |

|

Forecast Year Market Size (2035) |

USD 26.3 billion |

|

Regional Scope |

|

Graphite Electrodes Market Segmentation:

Application Segment Analysis

Based on the application, the electric arc furnace (EAF) steelmaking segment in the graphite electrodes market is anticipated to garner the highest share of 82.4% by the end of 2035. The segment’s upliftment is highly driven by its crucial role in serving as the primary conductor to develop intensified electric arcs that have the capability to scrap steel. According to official statistics published by the World Steel Association in 2025, each and every ton of steel produced has resulted in emitting 2.1 tons of carbon dioxide as of 2024. Besides, 1,886 million tons of steel have also been produced, and the overall emission from industries accounted for an order of 4.1 billion tons of carbon dioxide, of which 75% cater to direct emissions. These particular emissions demonstrate 7% to 8% of international anthropogenic greenhouse gas emissions, thus driving the segment’s exposure.

End user Industry Segment Analysis

The steel industry segment, which is part of the end user industry, is projected to hold the second-highest share in the graphite electrodes market during the forecast period. The segment’s growth is highly fueled by acting as the primary conductor of high-voltage electricity to melt scrap metal within the EAF. As per an article published by the World Steel Organization in October 2025, the worldwide steel demand as of 2025 successfully reached 1.749 million tons as of 2025 in comparison to 2025. This, however, is predicted to account for a modest rebound by 1.3% as of 2026, thus deliberately pushing the global demand to 1,773 million tons. Besides, the steel demand in developing economies, excluding China, is experiencing strong growth with a 3.4% surge in 2025, and an estimated 4.7% increase by the end of 2026, thereby making it suitable for bolstering the segment’s expansion.

Grade Segment Analysis

By the end of the stipulated timeline, the ultra-high power (UHP) electrodes sub-segment, part of the grade segment, is projected to hold the third-highest share in the graphite electrodes market. The sub-segment’s expansion is highly propelled by its exceptional electrical conductivity, thermal resistance, and mechanical strength compared to High Power (HP) and Regular Power (RP) grades. These advanced electrodes are manufactured using high-quality raw materials, primarily premium-grade needle coke with a low coefficient of thermal expansion, and undergo sophisticated processing techniques, including multiple graphitization cycles. The resulting product exhibits lower electrical resistance, superior thermal shock resistance, and the capacity to withstand continuous current densities, thus making them indispensable for high-productivity EAF operations.

Our in-depth analysis of the graphite electrodes market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

End user Industry |

|

|

Grade |

|

|

Manufacturing Process |

|

|

Raw Material |

|

|

Electrode Diameter |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Graphite Electrodes Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the graphite electrodes market is anticipated to garner the largest share of 51.5% by the end of 2035. The market’s upliftment in the region is highly attributed to the manufacturing supremacy, electric battery supply chain integration, and government strategic initiatives. According to official statistics published by the USGS Government in 2022, the region significantly accounts for 91.5% of the world’s tungsten production, which is followed by 77.1% of graphite, 75.7% of hydraulic cement, 75.1% of tin, 72.1% of raw steel, and 62.5% of bauxite. Besides, China accounts for 82.3% of tungsten production, followed by 5.4% in Vietnam. Meanwhile, Australia caters to 30% of bauxite, China with 19.9%, India with 6.3%, and Indonesia with 4.7%. Therefore, with countries accounting for different minerals, the market is gradually gaining increased exposure.

The graphite electrodes market in China is growing significantly, owing to accessibility to localized needle coke, heavy steel exports, EAF installation programs, the presence of a supportive policy framework, and graphite smelting. As per a data report published by the USGS Government in March 2025, the smelter production in the country caters to 10 commonly utilized nonferrous metals, including zinc, titanium, tin, nickel, mercury, magnesium, lead, copper, antimony, and aluminum, denoting an increase to 67.9 million metric tons. Moreover, the fixed asset investment in the nonferrous metal mining and processing sector has increased by 8.4%, while the processing industry increased by 15.7%. Besides, the export valuation of nonferrous metals surged by 26.7% to USD 66.3 billion, and the valuation of imports upsurged by 18.7% to USD 261 billion, thus fueling the market growth.

The robust government downstreaming strategies and tactical positioning in the electric vehicle supply chain, wide-ranging non-metallic mineral downstreaming, escalation in mineral processing capabilities, and the presence of abundant natural resources are responsible for bolstering the graphite electrodes market in Indonesia. Based on government estimates published by the ITA in November 2025, the mining equipment industry was worth USD 2.5 billion, along with an expected 8.1% growth by the end of 2031. This industry’s growth is highly fueled by an increase in the demand for mineral resources and supportive governmental reforms. Meanwhile, the underground mining equipment sector is predicted to grow by 9.1% by the end of 2030 and gradually reach USD 397.5 million, thereby making it suitable for uplifting the graphite electrodes market in the overall country.

Industrial Size Analysis for Mining Equipment in Indonesia (2020-2025)

|

Components (USD Million) |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

|

Total Exports |

540.8 |

808.9 |

1,130.0 |

1,065.4 |

1,150.3 |

1,345.5 |

|

Total Imports |

1,871.5 |

3,804.4 |

6,410.1 |

5,961.1 |

5,686.8 |

4,947.5 |

|

Exports to the U.S. |

26.4 |

66.3 |

123.6 |

158.4 |

121.0 |

99.2 |

|

Imports from the U.S. |

137.7 |

153.3 |

233.6 |

282.0 |

218.7 |

175.4 |

|

Trade Surplus/Deficit |

111.3 |

86.9 |

109.9 |

123.6 |

97.7 |

76.1 |

|

Exchange Rate |

14,582 |

14,308 |

14,850 |

15,237 |

- |

- |

Source: ITA

Europe Market Insights

Europe in the graphite electrodes market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the carbon border adjustment mechanism, green steel transition, transformation in the steel industry, diversification in the raw material supply chain, battery recycling and circular economy initiatives, technological advancement and AI adoption, along with defense applications as emerging demand. According to official statistics published by the Transport Environment Organization in December 2024, locally recycled batteries tend to offer metals for more than 2 million electric vehicles by the end of 2030. Besides, end-of-life batteries and scrap from battery gigafactories in the region have the potential to offer 14% of all lithium, which is followed by 16% of nickel, 17% of manganese, and a quarter of cobalt demand, thus boosting the market growth.

Projected Battery Electric Vehicle Production from Recycled Material in Europe (2030-2040)

|

Battery Type |

2030 |

2035 |

2040 |

|

Manganese |

1.5 million |

2 million |

3.8 million |

|

Lithium |

1.3 million |

2.4 million |

5.2 million |

|

Nickel |

1.6 million |

3.9 million |

7.6 million |

|

Cobalt |

2.4 million |

9.9 million |

15.4 million |

Source: Transport Environment Organization

The graphite electrodes market in Germany is gaining increased traction, owing to the largest steel producer with an increase in yearly steel output, suitable funding opportunities for securing supply chains, and creating domestic processing capabilities. As stated in an article published by the Clean Energy Wire Organization in December 2025, the country covers almost 56% of electricity utilization with renewables as of 2025. In this regard, there has been an increase in the solar power output by 18.7%, while the robust growth in installed capacity can be sustained with over 17 gigawatts added to the system. Besides, the wind power output in the nation accounted for 5.2% as of 2025. Additionally, onshore turbines with a capacity of 5.2 GW have been successfully added to the domestic grid, marking a surge from 3.3 GW in the previous year, thereby making it suitable for fueling the graphite electrodes market development.

The aspects of infrastructure investment, renewable energy deployment, tactical government intervention, massive mining exploration, utilization of artificial intelligence, and identification of the latest graphite resources are certain factors that are proliferating the graphite electrodes market in Spain. As per a data report published by OECD in June 2025, Andalusia accounts for 35% of national mining production and 30% of employment in the overall industry. Besides, the overall country holds a tactical relevance for the regional mineral supply chain, significantly contributing 90% of the nation’s metallic mineral output and hosting processing facilities for notable minerals, such as strontium, tin, iron, and copper. Additionally, the country is considered home to almost 470 active mines and different explorative projects for zinc, cobalt, tin, and copper, thus driving the market expansion.

North America Market Insights

North America in the graphite electrodes market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by an expansion in EAF steelmaking, generous investment in the electric vehicle battery supply chain, tactical minerals initiatives, utilization synergies and carbon capture, and technological innovation in graphite manufacturing. According to official statistics published by the Alliance for Innovation and Infrastructure in September 2024, the steel consumption in the U.S. has consistently accounted for nearly 100 million metric tons per year, while the regional steel production averaged almost 85 million metric tons. Additionally, 70% and 90% of yearly steel consumption has been produced domestically, while 14% is exported, thereby denoting a huge growth opportunity for the market in the region.

The graphite electrodes market in the U.S. is gaining increased exposure, owing to suitable growth in infrastructure and automotive demand, strategic focus on domestic supply chain and tariffs, and the vertical integration for raw material security. Based on government estimates published by Congress in March 2026, the automotive manufacturing industry in the country significantly accounts for 4.8% of gross domestic product and readily employs 10.1 million people through both direct and indirect employment opportunities. In addition, domestic automotive manufacturers, such as Chrysler, General Motors, and Ford, collectively account for more than 75% of sales in the country. Moreover, worldwide automotive manufacturers invested USD 124 billion in U.S.-based operations as of 2025 and successfully produced 4.9 million vehicles, thus enhancing the market demand.

The development of a domestic electric vehicle battery supply chain, government funding and strategic initiatives, high-profile international offtake agreements, and focus on geopolitical supply chain sovereignty are certain factors that are responsible for uplifting the graphite electrodes market in Canada. As stated in an article published by the ITA in September 2024, Honda Motor Co., Ltd. declared its plans to develop a wide-ranging electric vehicle value chain in the country with an estimated investment of USD 11 billion. This includes investment by joint venture partners for strengthening its electric vehicle supply capability and preparing for a future increase in demand in the overall region. Besides, Volkswagen and Stellantis notified large-scale investments of USD 5.1 billion and USD 3.7 billion respectively to develop a Gigafactory of electric batteries in Ontario, thus positively impacting the market growth.

Key Graphite Electrodes Market Players:

- Resonac (Japan)

- GrafTech International (U.S.)

- Tokai Carbon (Japan)

- Showa Denko K.K (Japan)

- Nippon Carbon Co., Ltd (Japan)

- SEC Carbon, Ltd (Japan)

- Fangda Carbon New Materials Technology Co., Ltd. (China)

- Graphite India Limited (GIL) (India)

- HEG Limited (India)

- Jilin Carbon Group Ltd (China)

- Kaifeng Carbon Co., Ltd (China)

- Kaifeng Pingmei (China)

- Nantong Yangzi Carbon Co., Ltd. (China)

- Yangzi Carbon (China)

- Sanergy Group (China)

- SGL Group (Germany)

- El 6 Group (France)

- ENERGOPROM Group (Russia)

- Graphite Cova GmbH (Germany)

- Redox (Australia)

- Graphite India Limited (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Resonac has strategically consolidated its electrode manufacturing by closing facilities in China and Malaysia to focus on high-value-added products. This rationalization allows the company to prioritize technological innovation and operational efficiency in the UHP segment.

- GrafTech International is aggressively defending its market position by pivoting to the U.S. market, where it has captured significant volume growth and insulated itself from global price pressures. The company's strategy centers on leveraging its vertical integration into needle coke production to maintain a cost advantage and supply stability for its clients.

- Tokai Carbon is actively restructuring its global footprint by reducing capacity in Japan and Europe to optimize its asset base for higher profitability. This move reflects a broader industry trend of mature-market players consolidating to focus on premium, high-margin electrode grades.

- Showa Denko K.K has transitioned its graphite electrode operations under the Resonac umbrella, focusing on technological leadership and high-performance materials. The company prioritizes the development of advanced electrodes that enable improved energy efficiency and productivity for electric arc furnace steelmakers.

- Nippon Carbon Co., Ltd leverages its long-standing expertise in carbon technology to serve specialized industrial applications beyond conventional steelmaking. The company maintains a focus on niche segments where its technical precision and product quality provide a distinct competitive advantage.

Here is a list of key players operating in the global graphite electrodes market:

The worldwide graphite electrodes market is currently defined by a structural oversupply, leading to intense pricing pressure and a highly competitive environment. The market is dominated by a handful of major players from Japan, the U.S., China, and India, who collectively hold a significant market share, particularly in the high-value ultra-high power (UHP) segment. In response to challenging market conditions, key players are adopting divergent strategies. Major manufacturers, such as GrafTech International, are focusing on volume growth in strategic regions, including the U.S., aggressive cost reduction, and optimizing their product mix towards premium grades. Conversely, in December 2025, Graphite India Limited and Kivoro effectively signed an outstanding distribution and commercial-based partnership agreement to bring Kioro’s graphene-specific heat transfer additive technology to the corrugated paperboard industry in India, thus bolstering the graphite electrodes industry globally.

Corporate Landscape of the Graphite Electrodes Market:

Recent Developments

- In March 2026, NextSource Materials Inc. has successfully entered into a binding deal with Syrah Resources Limited for generously supplying natural graphite fines for NextSource’s planned battery anode facility, particularly in the UAE.

- In September 2025, ExxonMobil deliberately entered into a tactical agreement to acquire the technology and U.S.-specific assets of Superior Graphite, as well as selected international offices for developing a strong and synthetic graphite supply chain.

- In September 2025, TACC Limited significantly signed a technical collaboration agreement with Ceylon Graphene Technologies to combinedly escalate the commercialization and large-scale adoption of graphene, along with its derivatives.

- Report ID: 8433

- Published Date: Mar 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.