Enterprise Server Market Outlook:

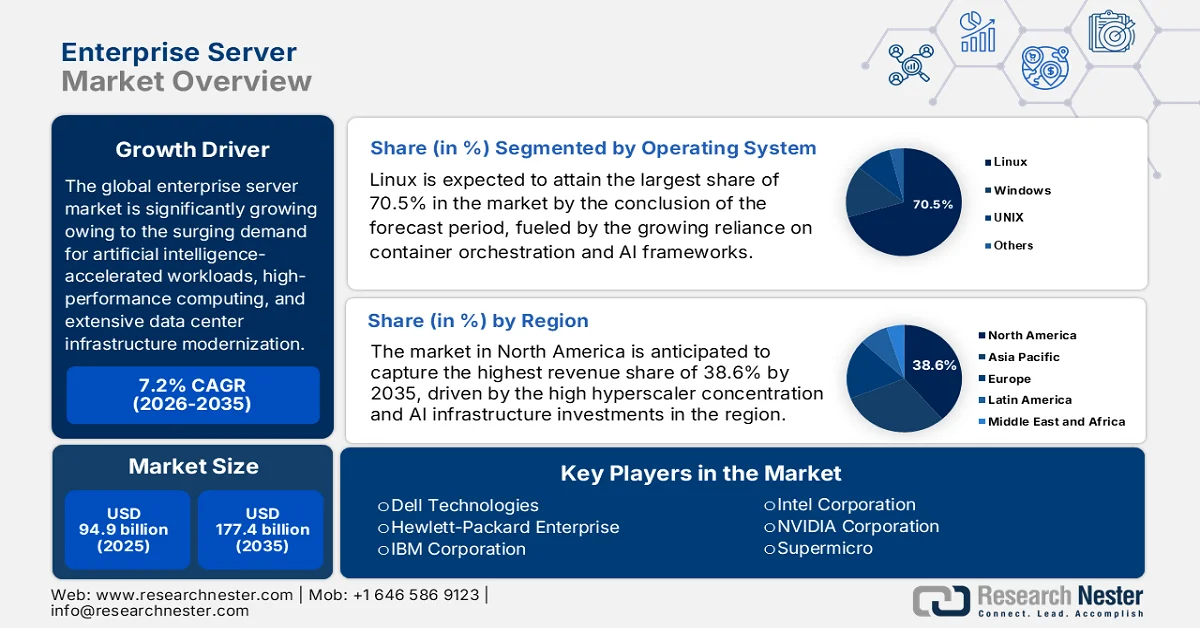

Enterprise Server Market size was valued at USD 94.9 billion in 2025 and is forecast to grow to USD 177.4 billion by 2035, registering a CAGR of 7.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of enterprise server is assessed at USD 101.7 billion.

The global enterprise server market is witnessing noteworthy growth, highly attributable to the surging demand for artificial intelligence-accelerated workloads, high-performance computing, and extensive data center infrastructure modernization. As per an article published by the Gitnux Organization in February 2026, the global data center capacity reached about 12,500 MW in 2023, with more than 1,200 MW added in a single year, whereas more than 5 GW is currently under construction worldwide. It also mentions that the U.S. leads with more than 5,381 data centers, and hyperscale operators now control roughly 55% of global capacity, driving rapid consolidation. Besides, the enterprise server market expansion continues along with AI growth, wherein the global revenue was USD 347 billion in 2023 and is projected to exceed USD 624 billion by 2029, thereby positively benefiting the enterprise server industry.

Global Hyperscalers & Data Center Operators Market Share, Scale & Infrastructure Statistics (2026)

|

Hyperscaler / Operator |

Key Statistic |

|

Equinix |

Operates 260+ data centers globally. |

|

Digital Realty |

Has 300+ data centers across 50 metros. |

|

Amazon Web Services |

Holds 31% cloud market share (Q4 2023). |

|

Microsoft Azure |

Holds 24% cloud infrastructure share. |

|

Google Cloud |

11% share, growing 28% YoY. |

|

Meta |

20+ data center campuses; added 5 in 2023. |

|

Oracle Cloud Infrastructure |

Grew 50% YoY in 2023. |

|

Alibaba Cloud |

Leads APAC with 40% market share. |

|

CoreSite |

Added 25 data centers via the American Tower acquisition. |

|

NTT Global Data Centers |

150+ facilities worldwide. |

|

Blackstone (QTS) |

USD 10 billion acquisition (largest data center deal). |

|

Iron Mountain |

Data center portfolio valued at USD 15 billion post-SPAC. |

|

CyrusOne |

Merged under the KKR portfolio; 50+ data centers. |

|

Switch |

7.2 million sq ft data center campus in Nevada. |

|

GDS Holdings |

140+ data centers in China. |

|

Vantage Data Centers |

Raised USD 6.4 billion for expansion. |

|

Cloudflare |

Edge network across 310+ cities. |

|

Top 10 operators |

Control 30% of global capacity. |

|

Apple |

Invested USD 10 billion in U.S. data centers since 2018. |

|

NVIDIA |

DGX SuperPOD powers 70% of top supercomputers. |

Source: Gitnux Organization

Furthermore, organizations across the globe are opting for hybrid and multi-cloud strategies in order to balance operational control with cloud-native speed, due to which the enterprise server market is shifting toward specialized, high-density, and energy-efficient systems. In this context, the article published by Gitnux Organization in February 2026 revealed that the global server market was USD 102.5 billion in 2023, driven by strong AI workloads, with hyperscale operators accounting for 42% of total revenue. It also mentions that the worldwide server shipments exceeded 11 to 12 million units, wherein the cloud providers purchased 58% of all servers, reflecting rapid enterprise digital transformation. At the same time, energy demand rose, with servers consuming around 200 TWh in 2022 and contributing to data center power usage of up to 340 TWh globally. Moreover, the hardware performance is advancing quickly, with GPU-accelerated servers growing 75% YoY and enterprise adoption of DDR5, NVMe, and high-core CPUs accelerating efficiency gains.

Key Enterprise Server Market Insights Summary:

Regional Highlights:

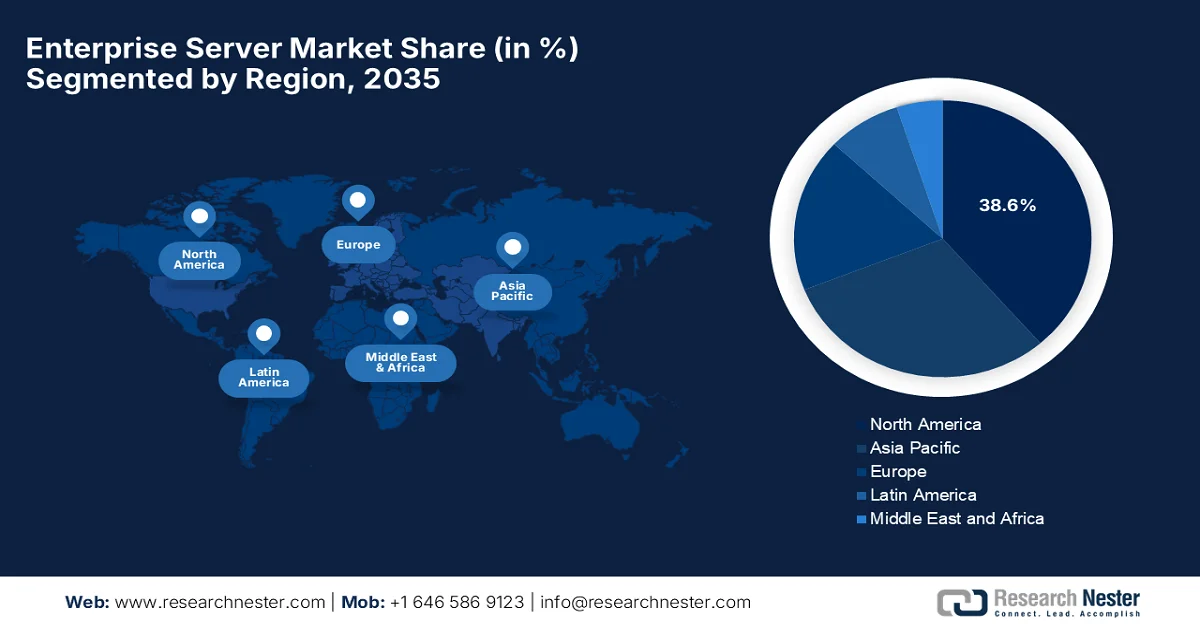

- North America enterprise server market is projected to hold a 38.6% share by 2035, propelled by high hyperscaler concentration and AI infrastructure investments

- Asia Pacific is set to witness the fastest growth during 2026–2035, fueled by intense digital transformation initiatives and rising demand for IoT and 5G-driven data-centric technologies

Segment Insights:

- The Linux segment is anticipated to capture a 70.5% share by 2035, driven by growing reliance on container orchestration and AI frameworks alongside increasing adoption of confidential computing technologies

- The rack server segment in the enterprise server market is expected to secure a considerable share by 2035, supported by scalability and efficiency in hyperscale data centers enabling cloud, AI, and high-performance computing workloads

Key Growth Trends:

- Rapid adoption of AI and machine learning workloads

- Hybrid cloud and multi-cloud expansion

Major Challenges:

- High capital and infrastructure costs

- Energy consumption and sustainability pressures

Key Players: Dell Technologies (U.S.), Hewlett Packard Enterprise (U.S.), IBM Corporation (U.S.), Intel Corporation (U.S.), NVIDIA Corporation (U.S.), Supermicro (U.S.), Oracle Corporation (U.S.), Cisco Systems (U.S.), AMD (U.S.), Microsoft Corporation (U.S.), Lenovo Group Limited (China), Fujitsu Limited (Japan), NEC Corporation (Japan), Hitachi Vantara (Japan), Atos SE (France), Siemens AG (Germany), Samsung Electronics (South Korea), SK hynix (South Korea), HCLTech (India), Tata Consultancy Services (India), Telekom Malaysia Berhad (Malaysia), Axiata Group (Malaysia).

Global Enterprise Server Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 94.9 billion

- 2026 Market Size: USD 101.7 billion

- Projected Market Size: USD 177.4 billion by 2035

- Growth Forecasts: 7.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Australia, Canada

Last updated on : 21 April, 2026

Enterprise Server Market - Growth Drivers and Challenges

Growth Drivers

- Rapid adoption of AI and machine learning workloads: Enterprises are making heavy investments in terms of servers that are optimized for AI training, inference, and GPU-accelerated computing. This is one of the strongest current drivers for the enterprise server market as organizations shift from traditional workloads to AI-native infrastructure. For instance, in March 2023, NVIDIA reported that its Hopper-based H100 GPUs were being widely adopted by major cloud providers such as AWS, Microsoft Azure, and Oracle to meet surging demand for generative AI training and inference. The H100, built on the Hopper architecture with a Transformer Engine, delivers major performance gains for large language models and other AI workloads when compared to the previous A100 generation. Furthermore, companies such as OpenAI, Meta, and Stability AI began integrating or planning to use H100 systems to accelerate research and production-scale AI systems, thus positively impacting the enterprise server market’s growth and exposure.

- Hybrid cloud and multi-cloud expansion: Most of the enterprises are making a shift towards hybrid IT architectures by combining on-premise servers with public cloud environments. This readily increases demand for enterprise servers that can best integrate with cloud platforms, support workload portability, and manage distributed environments more efficiently. In January 2026, the article published by In Education disclosed that hybrid cloud has become the default IT architecture, which is efficiently blending public cloud, private cloud, and on-premises systems into one flexible, resilient setup. It allows organizations to balance performance, security, compliance, and cost while adapting quickly to shifting demands and regulations, thus making it suitable for bolstering enterprise server market growth internationally.

- Growth of edge computing and IoT: The expansion in IoT devices, 5G networks, and real-time analytics is readily encouraging computing closer to the data source. This factor effectively drives demand for compact edge servers, low-latency processing systems, and distributed enterprise infrastructure. In October 2025, the article published by the Organization for Economic Co-operation and Development stated that in a span of five years, the fiber networks and 5G deployment rapidly expanded, thereby strengthening digital infrastructure, with 5G accounting for 37% of mobile broadband subscriptions and mobile data traffic growing by 20% on a yearly basis. It also stated that these technologies, along with IoT and AI, are driving demand for high-quality, low-latency connectivity and accelerating digital transformation across economies, thus benefiting the overall enterprise server market.

Challenges

- High capital and infrastructure costs: The enterprise servers, especially the AI-optimized ones, require extensive capital investments, which are influenced by expensive GPUs, CPUs, high-bandwidth memory, and specialized cooling systems. At the same time, rack-scale AI infrastructure exacerbates the total cost of ownership for enterprises. Along with hardware, organizations need to make investments in terms of power upgrades, data center expansion, and liquid cooling systems to support high-density compute environments. These burgeoning costs cause limitations to adoption among mid-sized enterprises, which in turn widens the digital infrastructure gap. On the other hand, the larger players in the enterprise server market face budget constraints when scaling AI workloads across multiple data centers. As a result, cost sensitivity has remained a strong barrier to widespread enterprise server modernization.

- Energy consumption and sustainability pressures: The emerging modern enterprise servers, especially the AI and GPU-intensive systems, consume huge amounts of power, which creates both operational and environmental obstacles. Therefore, data centers which are housing these servers necessitate improved cooling systems, which often include liquid cooling technologies, to manage heat density. At the same time, the rising electricity cost also impacts the total cost of ownership for enterprises that are operating large-scale server infrastructure. In addition, governments and regulatory bodies across different nations are imposing stricter sustainability and carbon emission requirements on data centers. In this context, companies are facing pressure to adopt energy-efficient architectures, optimize workload distribution, and transition to renewable energy sources. Energy efficiency has therefore become both a competitive differentiator and a major operational constraint in the enterprise server market.

Enterprise Server Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.2% |

|

Base Year Market Size (2025) |

USD 94.9 billion |

|

Forecast Year Market Size (2035) |

USD 177.4 billion |

|

Regional Scope |

|

Enterprise Server Market Segmentation:

Operating System Segment Analysis

In the operating system segment, Linux is expected to attain the largest share of 70.5% in the enterprise server market by the conclusion of the forecast period. The segment’s dominance is effectively fueled by the growing reliance on container orchestration and AI frameworks that require deep kernel-level control. Additionally, the increasing adoption of confidential computing technologies also strengthens the sub-segment’s position in security-focused and regulated workloads. In September 2024, Dell Technologies and Red Hat announced a collaboration to bring Red Hat Enterprise Linux AI to Dell PowerEdge servers to establish RHEL AI as a preferred platform for AI deployments. This particular partnership enables enterprises to more easily develop, test, and run large language models on validated, AI-optimized hardware, hence denoting a wider segment scope.

Server Type Segment Analysis

The rack server, which is a part of the server type segment in the enterprise server market, is anticipated to grow with a considerable share by the conclusion of the forecast period. Their scalability and efficiency in hyperscale data centers support cloud, AI, and high-performance computing workloads, are the main factors behind the segment’s leadership in this field. For instance, in August 2025, NVIDIA brought RTX PRO 6000 Blackwell GPUs into mainstream 2U rack servers from partners such as Cisco, Dell, HPE, Lenovo, and Supermicro for enterprise data centers. It mentioned that these rack-based systems deliver up to 45 times higher performance and much better efficiency than CPU-only servers, supporting AI, analytics, simulation, and graphics workloads, thus denoting an optimistic opportunity for the segment to grow in the next decade.

End use Industry Segment Analysis

By the end of 2035, the IT and telecom is expected to attain a significant revenue share in the enterprise server market. The subsegment’s leadership is mainly propelled by exponential data traffic growth, 5G deployment, IoT expansion, and cloud adoption. This accelerating demand requires a highly scalable and distributed server infrastructure to handle communication, data processing, and network virtualization workloads, thus positioning the segment for sustained growth in the years ahead. In September 2025, Dell Technologies introduced the PowerEdge XR8720t, the industry’s first single-server solution for Open RAN and Cloud RAN deployments, which will deliver breakthrough performance, scalability, and lower TCO for telecom and enterprise edge. It has up to 72 cores, 24x25G port density, and an Intel Xeon 6 SoC, which reduces operational complexity and future-proofs telecom and enterprise infrastructure for next-generation applications.

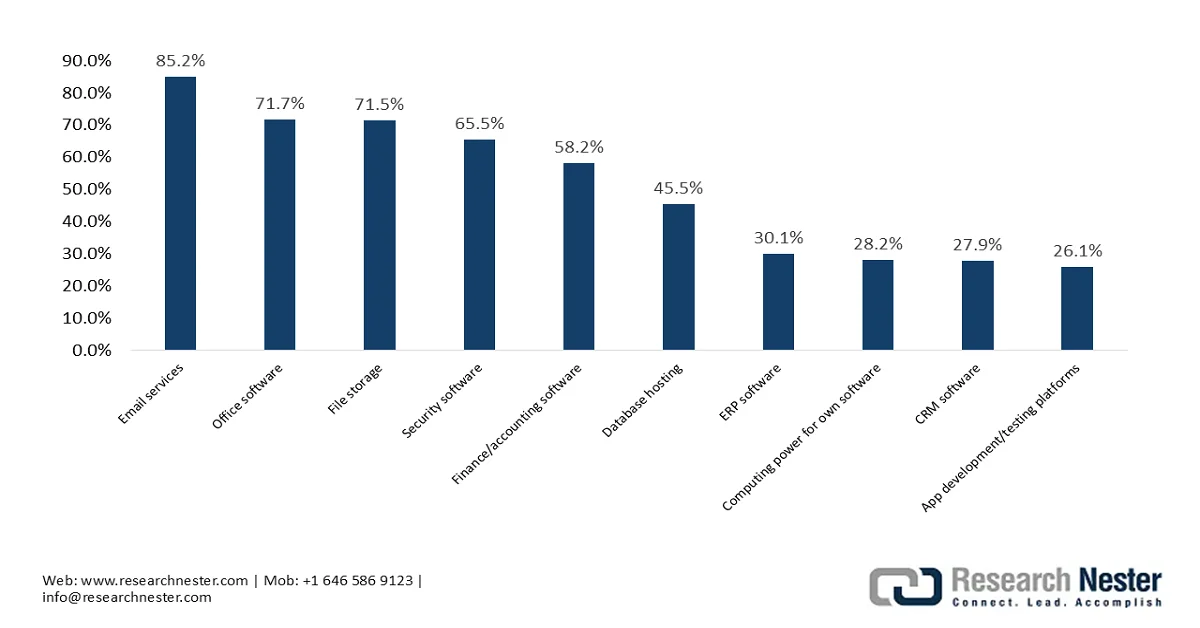

Most Used Cloud Computing Services in Europe Enterprises 2025

Source: Eurostat

Our in-depth analysis of the enterprise server market includes the following segments:

|

Segment |

Subsegments |

|

Operating System |

|

|

Server Type |

|

|

End use Industry |

|

|

Processor Type |

|

|

Deployment Type |

|

|

Organization Size |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Enterprise Server Market - Regional Analysis

North America Market Insights

By the end of 2035, the North America enterprise server market is expected to attain the largest revenue share of 38.6%. The region’s dominance is mainly propelled by high hyperscaler concentration and AI infrastructure investments. At the same time, the rising adoption of cloud computing, massive investments in AI-accelerated workloads, and a widespread shift toward hybrid cloud infrastructure are also driving the region’s leadership. In December 2025, the U.S. General Services Administration (GSA) reported that its strategy shifts U.S. federal IT procurement toward a unified enterprise model where the government acts as a single buyer for cloud computing and IT services, consolidating agreements across agencies. Besides, it has established major contracts with leading FedRAMP-authorized providers to standardize pricing, licensing, and security compliance under frameworks such as NIST and federal cybersecurity policy. This approach reduces fragmented purchasing and strengthens enterprise server and cloud infrastructure through centralized governance.

The intense, accelerated demand for AI and machine learning capabilities, moving beyond traditional data center modernization are certain factors which are responsible for uplifting enterprise server market in the U.S. Major technology providers are in the country are witnessing a remarkable surge in revenue and shipment volumes which is fueled by massive, ongoing investment in AI infrastructure, high-performance computing, and the need for specialized GPU-based hardware. In this context, HPE, in partnership with NVIDIA, in October 2025, announced that it is advancing secure AI adoption for governments and enterprises through turnkey AI factory solutions that simplify deployment and scale. It mentions that this expanded portfolio includes high-performance servers, sovereign AI cloud designs, and air-gapped environments to meet compliance and security needs. Hence, such innovations accelerate outcomes for smart cities, regulated industries, and enterprises.

The continued digital transformation and the modernization of legacy IT infrastructure across various sectors are driving a profitable business ecosystem for players who are operating in the enterprise server market in Canada. The country’s landscape is making a shift away towards hybrid and multi-cloud strategies, thereby increasing the need for versatile servers that can manage diverse workloads. Based on the government data, Shared Services Canada’s 2026-27 Departmental Plan outlines USD 2.3 billion in planned spending with 8,796 full-time staff to drive transformation, modernization, and digital sovereignty across government IT. It also mentioned that key priorities include reducing reliance on legacy systems, expanding enterprise platforms such as GCaPaaS, and rolling out the enterprise desktop service for secure, standardized workspaces, thus positively impacting the enterprise server market’s growth and exposure.

APAC Market Insights

The Asia Pacific enterprise server market is expected to grow at the fastest rate from 2026 to 2035. The region’s growth in this field is largely propelled by intense digital transformation initiatives, rising demand for data-centric technologies such as the IoT and 5G, which necessitate enhanced processing power at the edge. The market is witnessing a shift towards high-performance, rack-optimized, and modular server architectures to meet the needs of growing data centers, with a strong focus on sustainability and energy efficiency. In December 2025, the government of Australia announced a new Cloud Policy, which will be effective from July 2026, and it sets a unified framework for cloud adoption across the APS to modernize services. It establishes five core requirements, i.e., prioritizing cloud solutions, leveraging contemporary technology, adopting responsibly with strong security, improving cost transparency, and nurturing cloud skills.

The intense national investments in AI, cloud computing, and digital transformation, particularly within the telecommunications, government, and finance sectors, are responsibly positioning the enterprise server market in China for sustained and extensive growth. Domestic firms are dominating the landscape owing to the heightened demand for AI-optimized, rack-dense systems, along with a strong push for the localization of server technology. Based on government data published in October 2025, the country’s Ministry of Industry and Information Technology announced plans to develop more than 30 new national and industry standards for cloud computing by 2027. These standards will cover technologies, services, applications, management, and safety, with the main goal to regulate definitions and unify requirements across industries. This particular initiative also looks to align domestic and international benchmarks, strengthening China’s fast-growing cloud industry and thereby supporting industrial upgrades.

The increased data center construction, government initiatives, and the demand for high-performance AI and IoT infrastructure are the growth catalysts for the enterprise server market in India. At the same time, key players such as Dell, HPE, and Lenovo are leveraging this growth, influenced by the rising demand for both traditional and specialized data center solutions across different types of industries. As per an article published by Press Information Bureau (PIB) in December 2025, India is readily expanding its GI Cloud under the Digital India initiative, with almost 2,170 ministries already hosting applications and 26 empaneled providers certified to international security standards. Moreover, the current cloud data center capacity stands at 1,280 MW, projected to grow 4 to 5 times by 2030, driven by AI adoption and digital governance. Furthermore, major global investments are Google’s USD 15 billion AI Hub in Visakhapatnam and AWS’s USD 8.3 billion data center in Maharashtra, thus solidifying the country’s scalable and AI-ready cloud ecosystem.

Europe Market Insights

Europe enterprise server market is remarkably growing on the global dynamics positively influenced by the urgent need for data center upgrades within financial institutions. At the same time, high-density server deployments are increasing as companies are making a shift away from legacy infrastructure to optimized rack and multi-node systems that have higher priority energy efficiency. In this context, Eurostat in February 2026 reported that in 2025, 52.7% of the regional enterprises used paid cloud computing services, rising by 7.4 percentage points when compared to 2023, which reflects rapid enterprise adoption of cloud-based infrastructure for computing, storage, and software access. Usage was highest in countries such as Finland, which reflects strong digital infrastructure maturity across leading regional economies. Therefore, this data confirms that cloud computing has become a core enterprise IT foundation in Europe, directly driving demand for scalable enterprise server and data center infrastructure.

Europe Enterprise Cloud Adoption by Country 2025

|

Country |

% of enterprises using cloud services |

|

Finland |

79.2% |

|

Italy |

75.6% |

|

Malta |

74.9% |

|

EU average |

52.7% |

|

Romania |

24.9% |

|

Greece |

24.3% |

|

Bulgaria |

17.8% |

Source: Eurostat

The rise of Industry 4.0 and the increasing adoption of edge computing have largely focused on robust data security and compliance, supporting the growth of the enterprise server market in Germany. There has been a strong demand for energy-efficient solutions and private cloud infrastructure, which is efficiently spurred by strict local data sovereignty regulations and a national shift toward sustainable technology. In June 2025, Siemens, Cadolto, and Legrand together introduced a next‑generation modular edge data center in Frankfurt, especially designed for speed, scalability, and sustainability. It uses customizable prefabricated modules deployable in 6 to 12 months, thereby supporting workloads from standard processing to high‑density AI. In addition, Siemens is integrating smart infrastructure, flexible financing, and Cadolto and Legrand providing modular construction and IT systems, and the solution reduces CO₂ emissions by 30%, achieves a 90% recycling rate, thus denoting a positive enterprise server market outlook.

The UK enterprise server market maintains a strong position in the regional landscape, heavily driven by high-efficiency architectures and edge computing to handle surging digital workloads. Key trends reshaping the country’s market include increasing adoption of energy-efficient technology and AI-driven systems to support cybersecurity and data processing demands. Based on the government data published in November 2023, Microsoft announced a generous investment of USD 3.1 billion over three years to expand its next‑generation AI data centre infrastructure in the UK, the largest in its 40‑year history there. This particular plan includes deploying 20,000 advanced GPUs by the end of 2026, doubling data centre capacity across London, Cardiff, and northern England, and training 1 million people with AI skills, thus denoting an optimistic enterprise server market opportunity.

Key Enterprise Server Market Players:

- Dell Technologies (U.S.)

- Hewlett Packard Enterprise (U.S.)

- IBM Corporation (U.S.)

- Intel Corporation (U.S.)

- NVIDIA Corporation (U.S.)

- Supermicro (U.S.)

- Oracle Corporation (U.S.)

- Cisco Systems (U.S.)

- AMD (U.S.)

- Microsoft Corporation (U.S.)

- Lenovo Group Limited (China)

- Fujitsu Limited (Japan)

- NEC Corporation (Japan)

- Hitachi Vantara (Japan)

- Atos SE (France)

- Siemens AG (Germany)

- Samsung Electronics (South Korea)

- SK hynix (South Korea)

- HCLTech (India)

- Tata Consultancy Services (India)

- Telekom Malaysia Berhad (Malaysia)

- Axiata Group (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Dell Technologies is one of the most prominent players in this field, and it leads primarily through its PowerEdge server portfolio. The company has strategically aligned its infrastructure business with the rapid rise of AI workloads, positioning servers as part of end-to-end data center solutions rather than just being in standalone hardware.

- Hewlett Packard Enterprise is yet another central competitor in this field, and it has a strong focus on hybrid IT infrastructure. The firm is extensively focused on AI-native infrastructure, including integrated systems that support AI training and inference workloads.

- Lenovo Group Limited is identified as a major global server provider with strong manufacturing and supply chain capabilities across major markets. The company has been expanding into enterprise infrastructure, particularly in terms of AI-ready and hybrid cloud servers.

- IBM Corporation leads in high-end systems such as IBM Power servers, which are especially designed for mission-critical workloads. Besides, the firm’s server strategy is closely associated with hybrid cloud and AI integration through its broader IBM ecosystem, including Red Hat OpenShift.

- Supermicro has emerged as a fast-growing enterprise server provider, particularly in AI and high-performance computing infrastructure. The company specializes in terms of highly customizable, modular server designs that are extensively used in data centers and AI training environments.

Below is the list of some prominent players operating in the global enterprise server market:

The enterprise server market is facing intense competition, and it is dominated by the U.S.-based giants such as Dell, HPE, and IBM, which are rapidly shifting toward AI-optimized and cloud-integrated infrastructure. At the same time, chipmakers such as NVIDIA, Intel, and AMD play a central enabling role by defining server architecture through GPUs and CPUs. On the other hand, companies from the Asia Pacific, i.e., Lenovo, Fujitsu, NEC, and Samsung, are strengthening their presence through hybrid cloud and energy-efficient systems, whereas firms from Europe are focused on sovereign cloud and secure infrastructure. In April 2026, Lenovo completed the acquisition of Infinidat Ltd., which is a leading provider of high-end enterprise storage solutions, solidifying its global position in resilient, AI-ready data infrastructure. This particular move combines Lenovo’s scale and infrastructure portfolio with Infinidat’s expertise in mission-critical storage across industries such as finance, healthcare, and telecom.

Corporate Landscape of the Enterprise Server Market:

Recent Developments

- In April 2026, Supermicro introduced its new Gold Series enterprise server solutions, which offer over 25 pre-configured systems optimized for compute, AI, storage, and intelligent edge workloads. These ready-to-ship servers, validated and workload-optimized, significantly reduce deployment times by shipping within three business days.

- In January 2026, Lenovo introduced new Think System and Think Edge AI inferencing servers, which are especially designed to deliver real-time intelligence across industries and workloads of any size. These purpose-built systems are optimized with advanced GPU, memory, and networking capabilities to power enterprise AI inferencing from data centers to the edge.

- Report ID: 2709

- Published Date: Apr 21, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.