Cloud Electronic Design Automation Market Outlook:

Cloud Electronic Design Automation (EDA) Market size was valued at USD 3.26 billion in 2025 and is expected to reach USD 8.3 billion by 2035, registering around 9.8% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of cloud electronic design automation is evaluated at USD 3.55 billion.

The market has a lot of opportunities as the Internet of Things (IoT) grows. Important players can collaborate closely with up-and-coming IoT development firms. As a result, these partnerships will support the market expansion. By 2023, there will be about 15.14 billion IoT devices.

In addition, Artificial Intelligence (AI) and Machine Learning (ML) influence almost every industry, including electronics, healthcare, automotive, aerospace, and defense. Businesses are increasing the range of products they offer in the previously listed categories by integrating AI and ML into their products. EDA providers can benefit from these implementations of the offered technologies, which call for the usage of sophisticated electronic parts and processors. Software developers can shift from manual to automated process testing with the aid of artificial intelligence. During the projected time, these variables would support the expansion of the electronic design automation software industry.

Key Cloud Electronic Design Automation (EDA) Market Insights Summary:

Regional Highlights:

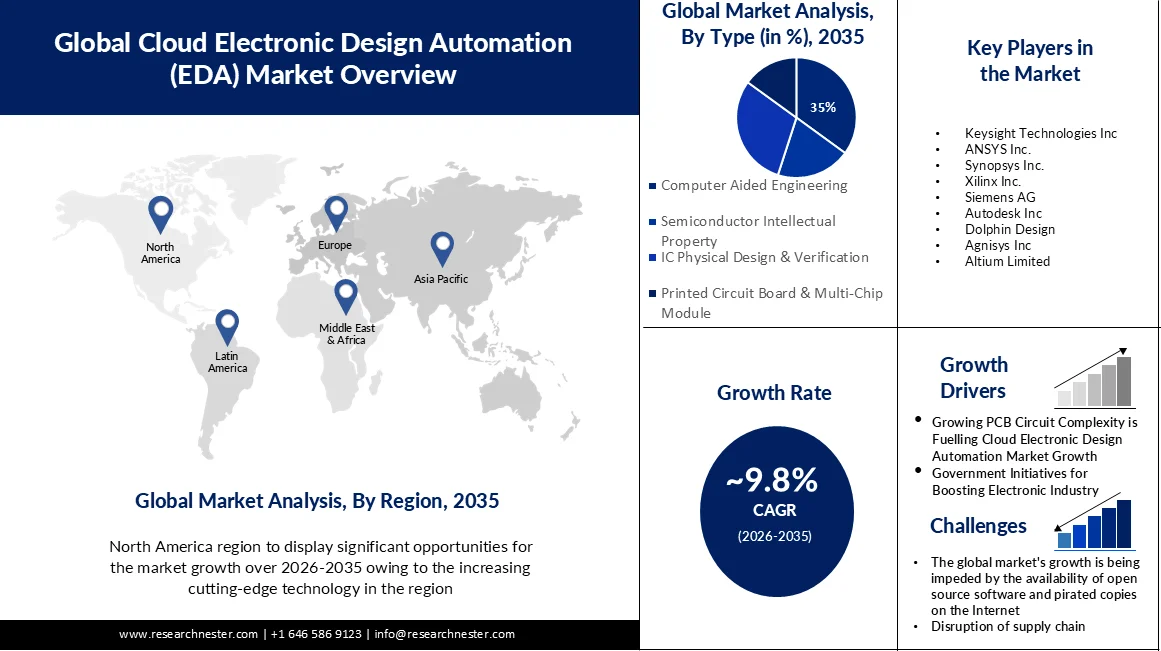

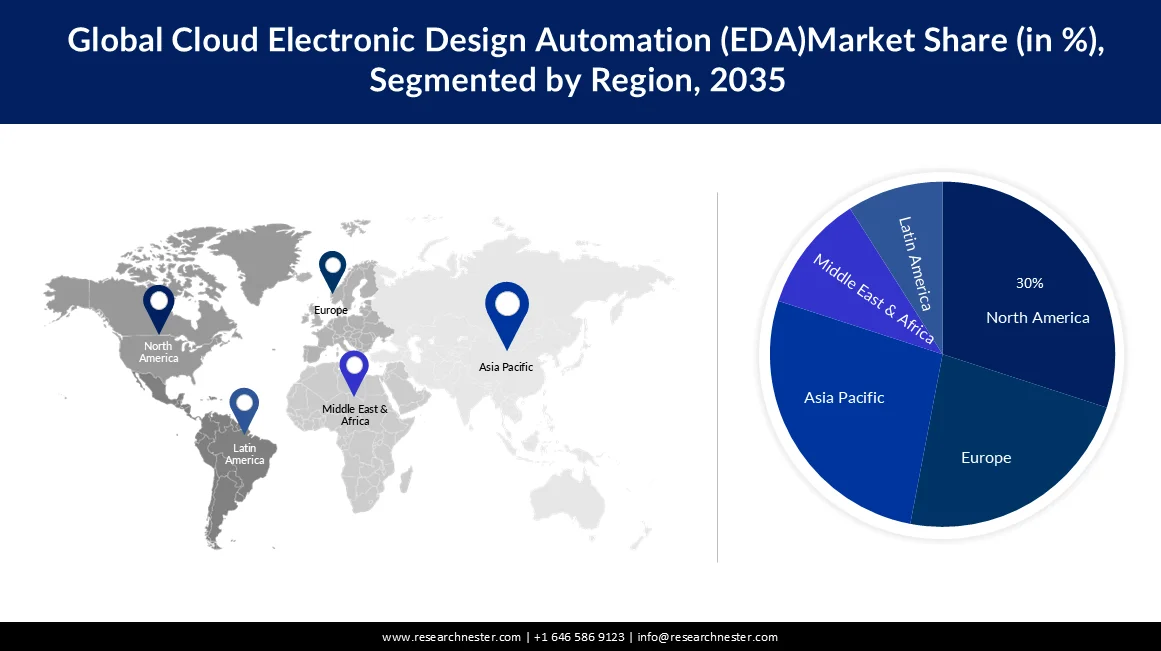

- North America in the cloud electronic design automation (eda) market is projected to command around 30% revenue share by 2035, attributed to early adoption of advanced technologies such as 5G and AI alongside strong industry collaboration and supportive wireless infrastructure.

- Asia Pacific is anticipated to capture nearly 27% revenue share by 2035, stimulated by increasing SoC design complexity and rising reliance on scalable cloud-based solutions across semiconductor enterprises.

Segment Insights:

- The computer aided engineering segment of the cloud electronic design automation (eda) market is projected to account for a 35% share by 2035, propelled by the accelerating transition to cloud-based integrated software solutions that minimize prototyping costs and enhance computing efficiency.

- The consumer electronics segment is expected to secure around 30% revenue share by 2035, fueled by rising demand for smart devices and strengthened collaborations between OEMs and leading SoC and IC manufacturers.

Key Growth Trends:

- Growing PCB Circuit Complexity is Fuelling Cloud EDA Market Growth

- Government Initiatives for Boosting Electronic Industry

Major Challenges:

- The global market's growth is being impeded by the availability of open-source software and pirated copies on the Internet

- One market constraint is the disruption of the manufacturing industries' worldwide supply chain during the forecast period.

Key Players: Quaker Houghton International Inc., FUCHS PETROLUB SE, Chemetall GmbH, TotalEnergies SE, Bechem Lubrication Technology, LLC, Petrofer AG.

Global Cloud Electronic Design Automation (EDA) Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.26 billion

- 2026 Market Size: USD 3.55 billion

- Projected Market Size: USD 8.3 billion by 2035

- Growth Forecasts: 9.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (30% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Taiwan, Japan, China, Germany

- Emerging Countries: China, India, Japan, South Korea, Singapore

Last updated on : 25 February, 2026

Cloud Electronic Design Automation Market - Growth Drivers and Challenges

Growth Drivers

- Growing PCB Circuit Complexity is Fuelling Cloud EDA Market Growth- Several wires and components must be implemented when building a circuit, and an engineer must take a variety of factors into account when constructing, including input signals, the desired output, and error tolerance. When building a complex circuit, there are more parts and wires involved, which raises the possibility of errors. There is a fair bit of drafting required because the design is somewhat large. If the user has grasped the fundamentals at any time, there is no need to draw the remaining circuitry because the section ends with a completed schematic. On the other hand, an engineer can simulate the circuit design and gain insight into the challenges that arise in real-time when implementing the circuit using cloud electrical design automation software. A cloud-based electronic design automation tool with auto-placement, auto-routing, and auto-tuning capabilities can greatly minimize errors and simplify fabrication. Time is saved since possible mistakes are fixed before the prototype is built. The cloud electronic design automation (EDA) market is growing as a result of these features and advantages.

- Government Initiatives for Boosting Electronic Industry- Governments from several nations, including Saudi Arabia, France, Canada, Australia, India, China, Brazil, and Canada, are promoting digitization in the electronics sector, which is driving the rise of electronic design automation software. For example, the Indian government stated in November 2022 that it will provide funds of approximately USD 122 million to support chip design start-ups throughout the nation. The purpose of this grant is to support Indian start-ups involved in semiconductor design. Through 2030, these government measures will have a favorable impact on the EDA software market.

- Growing Demand for EDA in Automotive Industry- The cloud electronic design automation market is expanding rapidly due to the increasing need for electronic design automation (EDA) technologies in the automobile industry. With the increasing complexity of modern automobile electronics, EDA tools are essential for developing sensors, control systems, and integrated circuits (ICs). They give engineers working on automobiles the ability to create complex electronic parts that guarantee energy economy, safety, and communication. The need for EDA tools has increased dramatically in tandem with the popularity of electric and driverless vehicles, spurring innovation and improving the driving experience in general.

Challenges

- The global market's growth is being impeded by the availability of open-source software and pirated copies on the Internet- Numerous features-rich electrical design automation programs are offered for free over the Internet. Furthermore, the widespread use of pirated software in nations like the USA, Russia, and China forces software providers to provide their products at a discount. This is a significant element that is anticipated to limit cloud electronic design automation (EDA) market expansion.

- One market constraint is the disruption of the manufacturing industries' worldwide supply chain during the forecast period.

- Inadequate research and development constitute a cloud EDA market constraint during the forecast period.

Cloud Electronic Design Automation Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.8% |

|

Base Year Market Size (2025) |

USD 3.26 billion |

|

Forecast Year Market Size (2035) |

USD 8.3 billion |

|

Regional Scope |

|

Cloud Electronic Design Automation Market Segmentation:

Type Segment Analysis

The computer aided engineering segment is anticipated to hold 35% share of the global cloud electronic design automation market by 2035. The growing need for integrated software solutions to get rid of multiple prototype products and product recall concerns, the sharp shift from on-premise computing to cloud-based computing, and the increased outsourcing of manufacturing processes to emerging economies are all contributing factors to the segment's growth. Purchases of gear, software licensing, installation, and support costs are reduced by cloud computing. In the upcoming years, it is anticipated that this will improve the utilization of CAE software even further. Moreover, companies are setting up a private cloud with improved computing and storage capacities utilizing the Hyper-Converged Infrastructure (HCI) platform. Throughout the projection period, these elements would support the segment's expansion even more. By 2025, 200 ZB of data will be kept in the cloud. The cloud stores 60% of all corporate data worldwide.

Vertical Segment Analysis

The consumer electronics segment in the cloud electronic design automation (EDA) market is attributed to hold the largest revenue share of about 30% during the forecast period. Electronics makers would be encouraged to use EDA due to the increasing need for smart gadgets. To improve the quality of their smart products, consumer electronics OEMs are teaming up with top System-on-Chip (SoC) and IC producers, such as Qualcomm Technologies, Inc., Texas Instruments Incorporated, NXP Semiconductors, and Intel Corporation. For example, to speed up 3D-IC design, Cadence Design Systems and Samsung Foundry, a South Korean supplier of foundry technologies, increased their collaboration in October 2022. The extended relationship with Samsung Foundry's 3D-IC technique will make the Cadence Integrity 3D-IC platform available. Customers may maximize the performance, power, and area of each die by using the Cadence platform.

Our in-depth analysis of the global cloud electronic design automation market includes the following segments:

|

Type |

|

|

Vertical |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cloud Electronic Design Automation Market - Regional Analysis

North American Market Insights

Cloud electronic design automation market in the North America is expected to hold the largest revenue share of about 30% during the forecast period. The early adoption of cutting-edge technology, such as 5G, machine learning, and artificial intelligence, among others, and the rise of several industries, including consumer electronics and automotive, are responsible for the region's success. This has been a significant factor in the demand in the area. For instance, U.S.-based EDA solution supplier Cadence Design Systems, Inc. stated in June 2022 that it will expand its partnership with U.S.-based technological solution provider Arm Limited. Using Arm Total Compute Solutions 2022 (TCS22) and Cadence digital and verification technologies, the businesses will collaborate to accelerate the development of mobile device silicon. For 5nm and 7nm nodes, Cadence will provide its RTL-to-GDS digital flow Rapid Adoption Kits in an effort to assist clients in achieving optimum power and enhancing productivity. North America is anticipated to have growth throughout the projection period because to its strong wireless infrastructure and government assistance.

APAC Market Insights

The cloud EDA market in the Asia Pacific region is projected to hold the second-largest revenue share of about 27% during the projected period. Novel deploy mentalities have been necessary due to the growing complexity of SoC designs. Cloud technologies help address these issues since they are scalable. The ability to access cloud-based solutions from anywhere in the company is their primary advantage. As a result, to build complex electrical systems, semiconductor businesses are depending more and more on cloud-based technologies. Over the projection period, these variables would support the region's growth even more.

Cloud Electronic Design Automation Market Players:

- Cadence Design Systems Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Keysight Technologies Inc

- ANSYS Inc.

- Synopsys Inc.

- Xilinx Inc.

- Siemens AG

- Autodesk Inc

- Dolphin Design

- Agnisys Inc

- Altium Limited

Recent Developments

- Cadence Design Systems announced low-power IP for the PCI Express 5.0 specification that targets hyper-scale computing, networking, and storage applications that are made on TSMC N5 process technology. In addition, PCIe 5.0 technology consists of a PHY, companion controller, and Verification IP (VIP) targeted at SoC designs for very high bandwidth to suit the applications.

- Keysight Technologies Inc. acquired Quantum Benchmark, a leader in error diagnostics, error suppression, and performance validation software for quantum computing. Quantum Benchmark provides software solutions for improving and validating quantum computing hardware capabilities by identifying and overcoming the unique error challenges required for high-impact quantum computing

- Report ID: 5532

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.