E-Methanol Market Outlook:

E-Methanol Market size was over USD 2.1 billion in 2025 and is estimated to reach USD 26.8 billion by the end of 2035, expanding at a CAGR of 32.7% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of e-methanol is assessed at USD 2.7 billion.

The worldwide market is gradually entering a transformative phase, with an accelerated adoption across industries beyond aviation and shipping. Unlike conventional methanol, e-methanol is readily produced from captured carbon dioxide and renewable hydrogen, thereby positioning the market as the ultimate cornerstone of the low-carbon economy. According to official statistics published by the International Journal of Hydrogen Energy in May 2025, the generation of renewable electricity has surged globally, while renewables' share of final energy consumption in Europe has increased from 9.6% to 22.1%. Besides, the worldwide hydrogen demand is projected to exceed 17,000 tWh by the end of 2050. Additionally, there are over 448 hydrogen projects globally that are focused on improving hydrogen-based power plants, thereby bolstering the market’s demand.

Different Hydrogen Power Plant Technology Cost Assumption Analysis (2025)

|

Technology Type |

Investment % per year |

Volume (EUR/mWh) |

Investment (EUR/MW) |

Lifetime |

Efficiency per unit |

|

Wind Offshore |

2.3 |

0.02 |

1,682,122.6 |

30 |

1 |

|

Solar Utility |

2.4 |

0.003 |

383,731.2 |

40 |

1 |

|

Electrolyzer |

4 |

0.004 |

1,500,000 |

25 |

0.6 |

|

Hydrogen Pipeline |

3.1 |

0.003 |

303.6 |

50 |

1 |

|

Hydrogen Storage Compressor |

4 |

0.004 |

87,690 |

15 |

1 |

|

Hydrogen Storage Rank |

2 |

0.002 |

13,500 |

20 |

0.99 per day |

|

Water Desalination Unit |

4 |

0.003 |

34,796.4 |

30 |

1 |

Source: International Journal of Hydrogen Energy

Furthermore, the integration into data centers and digital infrastructure, effectively with traditional fuels, carbon credit certification and trading, as well as localized micro-production units, are certain trends that are fueling the market globally. As per an article published by the World Bank Organization in 2026, carbon pricing presently covers nearly 28% of international emissions and has mobilized more than USD 100 billion for public budgets as of 2024. Besides, the carbon credit supply has continued to outstrip demand, significantly moving the international pool of unretired credits to nearly 1 billion tons in the same year. Besides, as per the November 2025 OECD article, there has been stabilization in the carbon tax at about 5% in 2023. Moreover, the coverage by emissions trading systems has doubled and increased from 10% to 22%, thereby proliferating the market’s exposure globally.

Emissions Trading Systems Coverage Analysis for Carbon Pricing (2018-2025)

|

Industry Type |

2018 |

2021 |

2023 |

2025 |

|

Agriculture and Fishing |

2% |

4% |

4% |

4% |

|

Buildings |

4% |

8% |

8% |

8% |

|

Electricity |

18% |

56% |

59% |

59% |

|

Industry |

15% |

15% |

15% |

37% |

|

Off-Road Transport |

5% |

6% |

7% |

9% |

|

Road Transport |

4% |

6% |

6% |

6% |

|

Other Greenhouse Gas Emissions |

3% |

3% |

3% |

9% |

|

Total Domestic Greenhouse Gas |

10% |

20% |

22% |

29% |

|

International Maritime |

- |

- |

- |

8% |

Source: OECD

Key E-Methanol Market Insights Summary:

Regional Highlights:

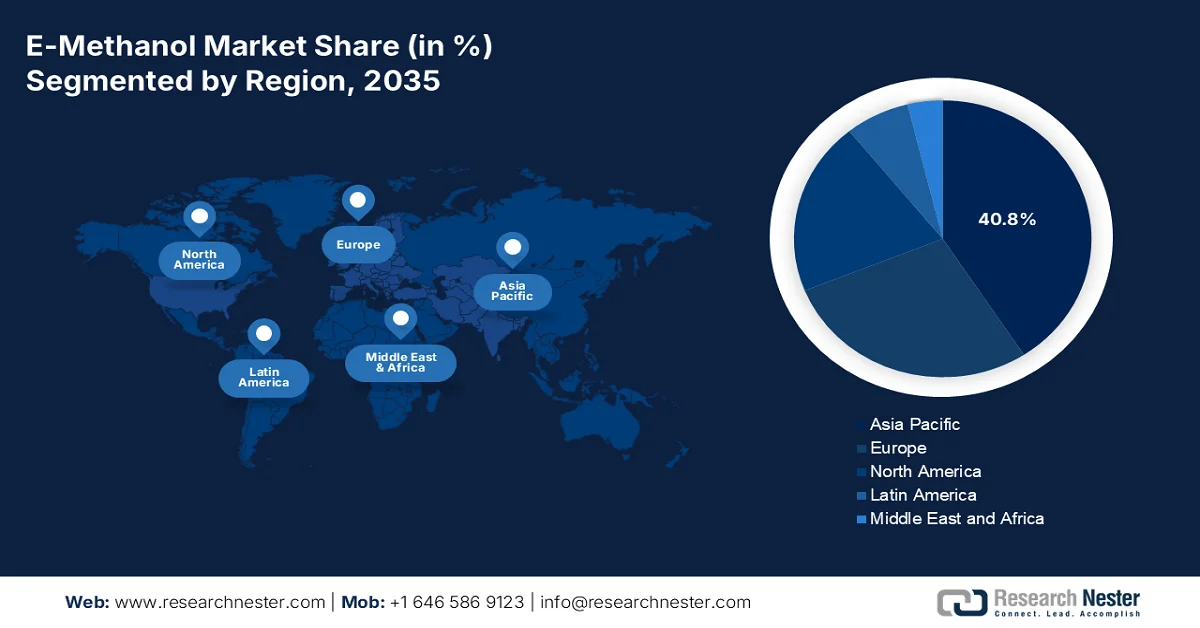

- The Asia Pacific region is projected to secure a 40.8% share by 2035 in the e-methanol market, underpinned by rising industrial demand, stringent decarbonization policies, and large-scale investments in renewable fuels.

- North America is expected to register the fastest growth through 2026–2035, stimulated by industrial decarbonization mandates, strong public spending, and expanding support for carbon capture and hydrogen.

Segment Insights:

- The renewable energy sources sub-segment within the feedstock segment is forecast to command a 55.8% share by 2035 in the e-methanol market, bolstered by its critical role in enabling carbon neutrality and supplying clean electricity for green hydrogen production.

- The transportation segment under end user is projected to hold the second-largest share by the end of the forecast period, accelerated by stringent maritime and aviation decarbonization regulations and mandatory lifecycle carbon intensity reductions.

Key Growth Trends:

- Increased demand in defense and military industries:

- Focus on urban air quality regulations

Major Challenges:

- High production expenses and infrastructure limitations

- Regulatory uncertainty and policy fragmentation

Key Players: Methanex Corporation (Canada), OCI N.V. (Netherlands), Carbon Recycling International (Iceland), European Energy A/S (Denmark), Liquid Wind AB (Sweden), Proman AG (Switzerland), Mitsubishi Gas Chemical Company, Inc. (Japan), Mitsui & Co., Ltd. (Japan), ENEOS Corporation (Japan), Maersk (Denmark), BASF SE (Germany), LyondellBasell Industries (Netherlands), SABIC (Saudi Arabia), ChemChina (China), Reliance Industries Limited (India), Petronas Chemicals Group Berhad (Malaysia), POSCO Holdings Inc. (South Korea), Woodside Energy Group Ltd. (Australia), BP Plc (UK), TotalEnergies SE (France).

Global E-Methanol Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.1 billion

- 2026 Market Size: USD 2.7 billion

- Projected Market Size: USD 26.8 billion by 2035

- Growth Forecasts: 32.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (40.8% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Australia, Saudi Arabia, United Arab Emirates

Last updated on : 10 February, 2026

E-Methanol Market - Growth Drivers and Challenges

Growth Drivers

- Increased demand in defense and military industries: Globally, defense agencies are evaluating the market as a clean fuel alternative for field power units and naval vessels that are driving the niche demand. According to official statistics published by the World Economic Forum in February 2025, the International Maritime Organization (IMO) has positively responded with its 2023 greenhouse gas approach, readily demanding a 205 reduction in shipping emissions by the end of 2030 and further accelerating to 70% to 80% by the end of 2040. Besides, FlagshipONE in Sweden has demonstrated that e-methanol can gain net emissions as low as -1.3 kg of carbon dioxide per kg of fuel with carbon capture credits, thereby making it suitable for bolstering the market’s demand.

- Focus on urban air quality regulations: Cities with critical pollution, particularly in Beijing and Delhi, are significantly incentivizing the e-methanol market adoption in public transport fleets for diminishing particulate emissions. As stated in an article published by NLM in January 2023, 40% of urban residents have been affected by health risks from transportation-based air pollution. Additionally, there are various urban air pollution causes, including dust, the construction sector, cooking firewood, motor cars, combustion engines, and manufacturing. Besides, transportation networks, industries, and other businesses have closed, while pollution levels across India, China, and New York have dropped by 30%, 25%, and 50%, respectively, thereby denoting a huge growth opportunity for the market globally.

- Industrial symbiosis with steel and cement plants: The captured carbon dioxide from robust industries is being readily repurposed for the market production, thus developing circular economy synergies. Besides, based on government estimates published by the PIB Government in October 2024, the steel output in India has successfully expanded at an outstanding 6% yearly growth rate, surpassing China’s 1% and also outshining international steel production. Additionally, in the past 5 years, there has been a worldwide increase in steel capacity by almost 62 million tons. Meanwhile, as per the November 2024 GCC Association Organization data report, the cement industry is committed to producing net-zero concrete by achieving 20% reduction in carbon dioxide per ton of cement by the end of 2030, thereby proliferating the market’s exposure.

Challenges

- High production expenses and infrastructure limitations: One of the most significant challenges facing the global e-methanol market is the high cost of production. E-Methanol requires renewable hydrogen and captured carbon dioxide, both of which are capital-intensive processes. Besides, electrolyzers remain expensive, and scaling them to industrial levels requires billions in investment. Additionally, carbon capture technologies are still in their early stages, with limited commercial deployment. This makes the cost of e-methanol significantly higher than conventional methanol or fossil fuels, limiting adoption in price-sensitive markets. Infrastructure is another bottleneck: large-scale renewable energy facilities, hydrogen pipelines, and methanol storage or distribution networks are not yet fully developed.

- Regulatory uncertainty and policy fragmentation: The market is heavily dependent on government regulations and international climate policies. While regions, such as Europe, have strong mandates under the European Green Deal and the Fit for 55 package, other regions lack consistent frameworks. For instance, while the International Maritime Organization (IMO) has set decarbonization targets for shipping, enforcement mechanisms vary widely across countries. In the U.S., federal support exists through the DOE and EPA, but state-level policies differ, creating uncertainty for investors. In Asia, China has ambitious renewable energy targets, but methanol policies are fragmented across provinces. This lack of harmonization creates risk for companies investing in global supply chains, as compliance costs differ regionally.

E-Methanol Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

32.7% |

|

Base Year Market Size (2025) |

USD 2.1 billion |

|

Forecast Year Market Size (2035) |

USD 26.8 billion |

|

Regional Scope |

|

E-Methanol Market Segmentation:

Feedstock Segment Analysis

The renewable energy sources sub-segment, which is part of the feedstock segment, is anticipated to garner the highest share of 55.8% in the market by the end of 2035. The sub-segment’s upliftment is highly driven by its importance of ensuring carbon neutrality and providing the clean electricity that is required for green hydrogen generation through electrolysis. Based on government estimates published by the ITA in January 2024, India’s peak need for energy has significantly reached a record high of 223 GW as of June 2023, denoting a surge by 3.4% than 2022. This growth is effectively supported by favorable geopolitics, government policies, urbanization, and industrial development, thus leading to the country achieving 400 GW as an exceeded installed capacity. Therefore, with this continuous growth, there is a huge growth opportunity for the sub-segment in the country and globally.

Total Installed Capacity Analysis by Power Source in India (2022-2023)

|

Source Type |

March 2022 (GW) |

May 2023 (GW) |

Energy Mix |

|

Coal |

204.0 |

205.2 |

49.1% |

|

Lignite |

6.62 |

6.62 |

1.6% |

|

Gas |

24.89 |

24.82 |

6% |

|

Diesel |

0.51 |

0.58 |

0.1% |

|

Hydro |

46.7 |

46.8 |

11.2% |

|

Nuclear |

6.78 |

6.78 |

1.6% |

|

Renewables |

109.8 |

125.6 |

30.2% |

|

Overall |

399.4 |

417.6 |

100% |

Source: ITA

End user Industry Segment Analysis

By the end of the forecast period, the transportation segment in end user is projected to hold the second-largest share in the e-methanol market. The segment’s growth is highly attributed to maritime and aviation sectors, which face stringent decarbonization mandates under the International Maritime Organization (IMO 2030/2050) and the International Civil Aviation Organization (ICAO CORSIA framework). Shipping companies such as Maersk and CMA CGM have already committed to using green methanol as a primary fuel for their next-generation vessels. Aviation is also exploring e-methanol-derived synthetic fuels as alternatives to kerosene. Moreover, the key driver is regulatory compliance, with governments in Europe, North America, and Asia enforcing lifecycle carbon intensity reductions and incentivizing the adoption of low-carbon fuels.

Application Segment Analysis

The fuel production sub-segment in the e-methanol market is expected to account for the third-largest share during the stipulated duration. The sub-segment’s development is highly fueled by the urgent need to decarbonize shipping, aviation, and power generation, where e-methanol serves as a versatile, low-carbon alternative to fossil fuels. Unlike conventional methanol, e-methanol is produced from renewable hydrogen and captured CO₂, offering a carbon-neutral lifecycle. The DOE’s Hydrogen and Fuel Cell Technologies Office in the U.S. has invested billions into renewable hydrogen projects, directly enabling large-scale e-methanol production. Similarly, Europe’s Fit for 55 package mandates reductions in transport emissions, thereby positioning e-methanol as a key compliance fuel.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Feedstock |

|

|

End user Industry |

|

|

Application |

|

|

Purity Levels |

|

|

Source Type |

|

|

Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

E-Methanol Market - Regional Analysis

APAC Market Insights

The Asia Pacific e-methanol market is anticipated to garner the largest share of 40.8% by the end of 2035. The market’s upliftment in the region is highly attributed to industrial demand, strong decarbonization policies, large-scale investments in renewable fuels, and an increase in the focus on innovative energy and power technologies. According to official statistics published by the IMF Organization in January 2026, the region significantly produces almost 80% of the global coal, along with 8% of international oil and 15% of worldwide gas. In addition, the region also comprises the largest coal importers and exporters, as well as nations declaring the objective to upscale the utilization and production of renewable energy, effectively signaling the commencement of the overall region’s energy transition, along with suitable opportunities for growth and development.

The e-methanol market in China is growing significantly, owing to an increase in industrial scale, government subsidies, a surge in maritime demand, and increased focus on energy security. As per an article published by the IEF Organization in February 2023, renewable methanol fuel is intended to be a part of a domestic future low-emissions energy mix, reducing carbon dioxide by almost 95%. Besides, the government has issued standard guidelines on methanol as a vehicle fuel, thereby prompting the rollout of methanol infrastructure and vehicles. For instance, Shanxi Province has developed over 200 methanol refueling stations, while at present, the country utilizes methanol as a vehicle fuel, ranging from 5% to 100%. This has deliberately resulted in the aspect of encouraging the take-up of entirely methanol-based vehicles, thereby making it suitable for boosting the market in the country.

The aspect of government funding, an upsurge in the industrial demand, generous policy support, and an increase in energy diversification are suitable for uplifting the market in India. Based on government estimates published by the PIB Government in January 2026, there has been an increase in natural gas pipelines by 25,400 km, thus ensuring almost 100% of geographical coverage throughout the nation. Besides, ethanol blending has successfully reached 19.0% between 2024 and 2025, deliberately approaching 20% of the initial target. Moreover, the country’s energy demand is predicted to expand rapidly in comparison to any other economy by 2035. In addition, the country is also projected to account for more than 23% of international incremental energy demand by the end of 2050, thus bolstering the market’s growth.

North America Market Insights

North America e-methanol market is expected to emerge as the fastest-growing region during the forecast period. Industrial decarbonization mandates, robust government expenditure, increased priority on renewable fuels, and generous funding for carbon capture and hydrogen highly propel the market’s development in the region. Based on government estimates published by the EPA Government in April 2025, the top ten industries in the region significantly account for 7.1 trillion pounds, denoting over 98% of the overall production volume. Besides, coal and petroleum production manufacturing, along with chemical manufacturing, accounted for 64% and 14% of the production volume, respectively. Moreover, the continuous increase in production volumes of chemicals is readily fueling the market’s exposure in the overall region.

Chemicals in North America with the Highest Recorded Production Volumes (2025)

|

Chemical Name |

Industry or Chemical Group |

Production Volume Range (lb/year) |

Number of Reporting Sites |

|

Sulfite liquors and cooking liquors |

Pulp and paper industry |

More than 200 billion |

96 |

|

Residues (petroleum) and vacuum |

Petroleum and petroleum products |

More than 200 billion |

93 |

|

Ethanol |

Organic chemicals |

100 to less than 110 billion |

267 |

|

Carbon dioxide |

Inorganic chemicals |

90 to less than 100 billion |

117 |

|

Sulfuric acid |

Acids |

70 to less than 80 billion |

175 |

|

Ethene |

Organic chemicals |

60 to less than 70 billion |

32 |

Source: EPA Government

The e-methanol market in the U.S. is gaining increased traction, owing to federal budget allocation, the presence of advanced chemical and semiconductor safety programs, the EPA green chemistry program, and generous grants provision for renewable hydrogen projects. As per a data report published by the National Archives in 2023, the approximate overall spending on sustainable chemistry research and development, as well as related activities across the Federal government, amounts to USD 1.4 billion for more than 4 years, with the Department of Energy stating the highest sustainable chemistry spending, offering USD 730 million. Additionally, this is followed by USD 364 million by NSF, USD 218 million by DoD, and USD 91 million by HHS. Besides, the allied products and chemical sectors in the country generously contributed 21% of the domestic manufacturing gross domestic product (GDP) and shipped USD 1.0 trillion in plastics, chemicals, and chemical-based products, thus driving the market’s growth.

The aspects of federal clean energy investments, the net-zero emissions by 2050 plan, and the support for renewable fuels in aviation and shipping for renewable fuels are responsible for propelling the e-methanol market in Canada. As stated in an article published by Natural Resources Canada in January 2025, the Energy Innovation Program (EIP) provides an overall USD 50 million for more than 5 years for pre-commercial production and industrial fuel switching of clean fuels. In addition, there is also the provision of almost USD 3 million for over 5 years for projects to support the upgradation and development of hydrogen standards and codes. Besides, heavy industry in the country accounted for 77 megatons of carbon dioxide, demonstrating 11% of domestic emissions, thereby denoting an optimistic outlook for the overall market’s expansion.

Europe Market Insights

Europe e-methanol market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by the Fit for 55 package and the regional Green Deal, sustainable energy adoption, along with an increase in aviation and shipping. According to official statistics published by the Methanol Organization in 2024, an increase in the 32% target to almost 40% renewable energy sources in the region’s total energy mix by 2030 under the Renewable Energy Directive (RED III) denotes a positive signal to the national industry and governments’ commitment to climate modifications. Regarding this, RED III has mandated that Renewable Fuels of Non-Biological Origin (RFNBOs) tend to account for nearly 42% of hydrogen utilization in the industrial sector by the end of 2030, thereby making it suitable for uplifting the market in the region.

The e-methanol market in Germany is gaining increased exposure, owing to government-funded decarbonization programs, robust industrial demand, generous funding provision for carbon capture and hydrogen projects, and transition to low-carbon feedstocks. As stated in a data report published by the Renewable Energy Institute Organization in January 2022, renewables account for 65% of overall power consumption based on Renewables Energy Sources Act, the Atomic Energy Act, and the Act to Reduce and End Coal-Fired Power Generation. Besides, the aspect of achieving climate neutrality by 2050, along with 55% of greenhouse gas emissions reduction by the end of 2030. Moreover, the country’s Federal Constitution also constitutes the objective of 88% reduction by the end of 2040, thereby creating a huge growth opportunity for the overall market.

The adoption of maritime fuel, strong renewable energy policies, and cost-effective hydrogen production are factors that are readily responsible for driving the e-methanol market in Norway. According to official statistics published by Renewable Energy in October 2025, the large run-of-river as well as small hydropower deliberately exhibit the highest production densities, accounting for 350 to 396 GWh/km2. Additionally, onshore wind demonstrates the lowest production density, accounting for 55 GWh/km2, thus indicating low land utilization. Besides, the country has aimed to become carbon neutral by the end of 2030 and diminish emissions of greenhouse gases by 50% to 55% by the end of 2050. This is possible by following regional plans to significantly elevate Europe’s 2030 objective target for renewables to 45% of the total renewable energy mix, thus bolstering the market’s exposure in the country.

Key E-Methanol Market Players:

- Methanex Corporation (Canada)

- OCI N.V. (Netherlands)

- Carbon Recycling International (Iceland)

- European Energy A/S (Denmark)

- Liquid Wind AB (Sweden)

- Proman AG (Switzerland)

- Mitsubishi Gas Chemical Company, Inc. (Japan)

- Mitsui & Co., Ltd. (Japan)

- ENEOS Corporation (Japan)

- Maersk (Denmark)

- BASF SE (Germany)

- LyondellBasell Industries (Netherlands)

- SABIC (Saudi Arabia)

- ChemChina (China)

- Reliance Industries Limited (India)

- Petronas Chemicals Group Berhad (Malaysia)

- POSCO Holdings Inc. (South Korea)

- Woodside Energy Group Ltd. (Australia)

- BP Plc (UK)

- TotalEnergies SE (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Methanex Corporation is the world’s largest methanol producer and has been actively investing in renewable methanol projects. The company is partnering with shipping and energy firms to expand green methanol supply, positioning itself as a key player in maritime decarbonization.

- OCI N.V. is a global leader in methanol and ammonia production, with strong operations in Europe and the U.S. The company is scaling renewable methanol capacity to meet rising demand in shipping and industrial sectors, supported by Europe-based climate policies.

- Carbon Recycling International pioneered commercial-scale renewable methanol production using captured carbon dioxide and hydrogen. Its flagship plant in Iceland demonstrates the viability of e-methanol as a sustainable fuel, making CRI a technology leader in carbon recycling.

- European Energy A/S is developing large-scale Power-to-X projects, including e-methanol plants that integrate renewable electricity and carbon capture. The company has signed supply agreements with Maersk, reinforcing its role in decarbonizing global shipping.

- Liquid Wind AB focuses on producing e-methanol from renewable electricity and biogenic carbon dioxide, with multiple projects underway in Sweden. Its partnerships with energy firms and shipping companies highlight its ambition to become a leading supplier of green maritime fuels.

Here is a list of key players operating in the global market:

The international market is highly competitive, with leading players pursuing strategic alliances, government-backed projects, and technological innovation to secure market share. Companies such as Methanex, OCI, and European Energy are scaling renewable methanol plants, while Asia-based giants, such as ChemChina and Reliance Industries, leverage domestic demand and government subsidies. Partnerships with shipping majors highlight the maritime sector’s pivotal role, while Europe-specific Green Deal funding and U.S. DOE initiatives further accelerate the adoption. Besides, in October 2025, DNV launched the sector’s first public tender portal for e-methanol procurement within Europe and the UK. This particular initiative readily connects a notable e-methanol producer with industrial offtakers across regional economies, thus developing a pathway for the e-methanol industry globally.

Corporate Landscape of the E-Methanol Market:

Recent Developments

- In April 2025, HIF Global significantly signed a Heads of Agreement (HoA) for the planned long-lasting sale and purchase of nearly 100,000 tons per annum of e-methanol from the company’s international e-fuels production portfolio for industrial and shipping applications.

- In March 2025, BASF and Forestal de Atlántico S.A. deliberately signed an early disclosure deal, effectively aimed at progressing the e-methanol production through carbon capture solutions.

- In October 2024, Carbon Recycling International (CRI) announced the signing of an outstanding deal with Tianying Group for leveraging its methanol synthesis technology in its large-scale e-methanol production project in Liaoyuan. This has marked China’s first-ever large-scale project using CRI’s proprietary technology for producing e-methanol from carbon dioxide.

- Report ID: 8386

- Published Date: Feb 10, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.