Drainage Catheter Market Outlook:

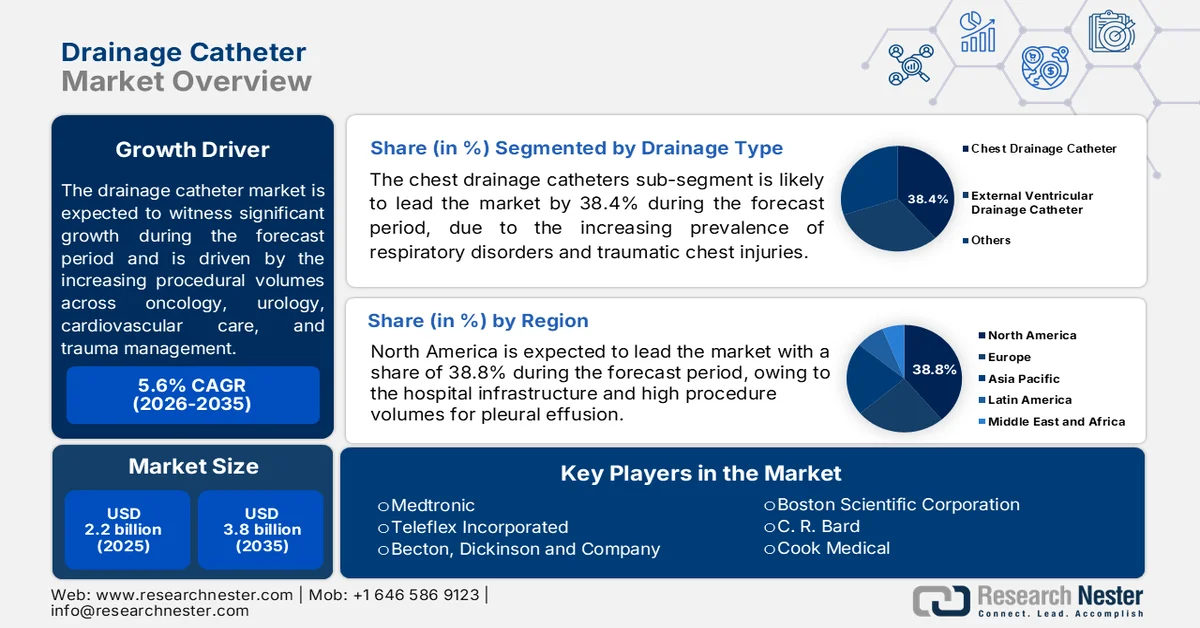

Drainage Catheter Market size was valued at USD 2.2 billion in 2025 and is poised to reach USD 3.8 billion by the end of 2035, expanding at around 5.6% CAGR during the forecast period i.e., 2026-2035. In 2026, the industry size of drainage catheter is evaluated at USD 2.3 billion.

The drainage catheter market is supported by increasing procedural volumes across oncology, urology, cardiovascular care, trauma management, and post-operative interventions in both developed and emerging healthcare systems. Rising hospitalization rates and the growing burden of chronic disease continue to expand demand for image-guided drainage procedures in acute and long-term care settings. According to the CDC, February 2024 data, nearly 129 million people in the U.S. are living with at least one major chronic disease, including cancer, cardiovascular disease, diabetes, or chronic kidney disease, all of which are associated with higher rates of surgical intervention, fluid management, and infection-related complications requiring catheter-based drainage support. Government-supported expansion of interventional radiology capacity and infection control programs is also contributing to procurement activity among hospitals and ambulatory surgical centers.

Besides, the world’s highest procedural and hospital treatment volumes are supported by aging populations and expanded healthcare access. The United Nations January 2023 data projects that the global population aged 65 years and older will more than double from 761 million in 2021 to 1.6 billion by 2050, increasing the prevalence of conditions such as urinary obstruction, cardiovascular disease, and postoperative complications that commonly require drainage interventions. Moreover, the WHO 2026 data estimates that 1 in 10 hospitalized patients develops healthcare-associated infections, reinforcing the need for advanced catheter systems with infection prevention and antimicrobial management capabilities. Procurement strategies across public hospitals are therefore increasingly focused on single-use systems, image-compatible catheter platforms, and products designed to reduce readmission rates and procedural complications.

Key Drainage Catheter Market Insights Summary:

Regional Highlights:

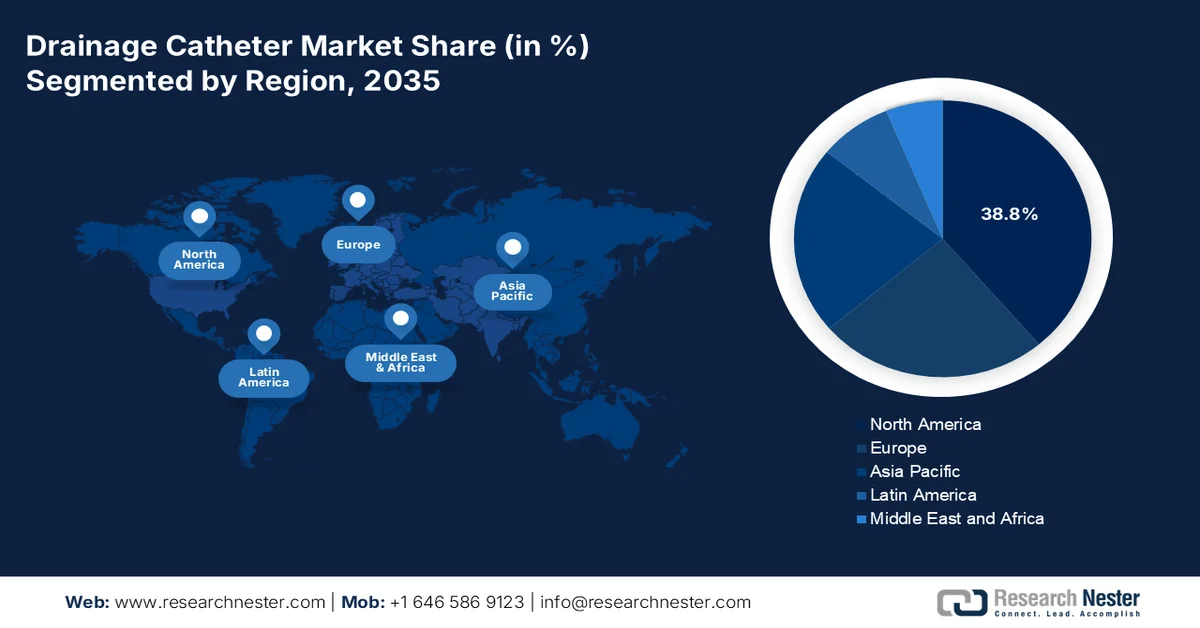

- The North America is anticipated to command 38.8% revenue share by 2035, fostered by strong hospital infrastructure, rising pleural drainage procedures, and increasing adoption of silicone-based single-use drainage systems

- Asia Pacific is forecast to witness a CAGR of 5.9% during 2026–2035 in the drainage catheter market, propelled by expanding hospital networks and rising pneumonia- and tuberculosis-related pleural complications across emerging economies

Segment Insights:

- Within the drainage catheter market, the chest drainage catheters segment is projected to capture 38.4% share by 2035, fueled by the growing prevalence of respiratory disorders, pleural effusion, traumatic chest injuries, and increasing cardiovascular and pulmonary surgeries

- The hospitals segment is expected to maintain a dominant position through 2035, stimulated by rising inpatient pleural drainage procedures and increasing demand for advanced active drainage and thrombolytic-compatible catheter systems

Key Growth Trends:

- Growth in cancer and oncology interventions

- Expansion of minimally invasive and image-guided procedures

Major Challenges:

- Raw material volatility and supply chain risks

- Regulatory hurdles and clinical evidence requirements

Key Players: Medtronic, Teleflex Incorporated, Becton, Dickinson and Company BD, Boston Scientific Corporation, C. R. Bard now part of BD, Cook Medical, Merit Medical Systems, Fresenius Medical Care, B. Braun Melsungen AG, Coloplast Group, Smiths Medical, Argon Medical Devices, Terumo Corporation, Nipro Corporation, ResMed, SIRADA Medical, Poly Medicure Limited, Vygon, Guerbet, Bearpac Medical, LLC.

Global Drainage Catheter Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.2 billion

- 2026 Market Size: USD 2.3 billion

- Projected Market Size: USD 3.8 billion by 2035

- Growth Forecasts: 5.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, Indonesia, Malaysia, South Korea, Thailand

Last updated on : 15 May, 2026

Drainage Catheter Market - Growth Drivers and Challenges

Growth Drivers

- Growth in cancer and oncology interventions: The increasing global cancer burden is creating a sustained demand for drainage catheters, which are used in pleural effusion management, biliary drainage, nephrostomy procedures, and postoperative fluid management. As per the WHO February 2024 data, nearly 20 million new cancer cases were reported globally. Many advanced-stage oncology patients require image-guided drainage interventions during chemotherapy, palliative care, or tumor-related obstruction treatment. Government support for oncology expansion programs is increasing the interventional radiology capacity in public hospitals. oncology-related catheter utilization is expected to rise further as healthcare systems expand minimally invasive cancer management pathways and outpatient procedural care models.

- Expansion of minimally invasive and image-guided procedures: Healthcare systems are increasingly prioritizing minimally invasive procedures to reduce hospitalization costs lower complication rates, and improve patient throughput, supporting higher adoption of drainage catheter market technologies. The U.S. continues emphasizing minimally invasive treatment pathways as part of healthcare quality improvement initiatives. Interventional radiology procedures using drainage catheters are increasingly replacing open surgeries for abscess drainage pleural effusions and biliary decompression. The National Institutes of Health (NIH) has also funded image-guided intervention programs supporting procedural innovation and outpatient care efficiency. Hospitals are expected to further prioritize catheter systems compatible with CT, fluoroscopy, and ultrasound-guided procedures due to operational efficiency and reduced inpatient burden, particularly in high-volume tertiary care centers across developed healthcare markets.

- Rising burden of pleural effusion: The increasing prevalence of pleural effusion is contributing to demand for the drainage catheter market across the pulmonary oncology and cardiovascular care settings. According to the NLM August 2021 study, nearly 1.5 million patients in the United States experience pleural effusion annually, primarily due to congestive heart failure, pneumonia, and cancer. The study further reported that 126,800 patients were hospitalized for pleural effusion, generating healthcare costs exceeding USD 5 billion. The growing clinical and economic burden is encouraging hospitals to adopt minimally invasive pleural drainage catheter market systems that support faster fluid management, lower complication rates, and reduced inpatient stays.

Challenges

- Raw material volatility and supply chain risks: The drainage catheter market depend on the specialized medical-grade polymers, which are subject to geopolitical instability, trade restrictions, and post-pandemic supply chain disruptions. Price volatility erodes margins for the manufacturers without long-term supplier contracts or dual sourcing strategies. Though the drainage catheter market is set to grow, the raw material cost fluctuations remain a persistent threat. Top companies overcome this via vertical integration and strategic polymer supplier partnerships, ensuring consistent production across their thoracic and abdominal drainage lines, while smaller competitors faced shortages and cost inflation.

- Regulatory hurdles and clinical evidence requirements: Regulatory bodies demand rigorous clinical validation for the drainage catheters, mainly for claims such as the lowest infection risk or superior drainage efficiency. smaller players in the drainage catheter market lack resources for the large-scale trials. FDA and CE mark processes require substantial documentation, and false claims attract penalties and forced rebranding. Top companies have invested in many clinical studies validating catheter technology, demonstrating a reduction in catheter-related bloodstream infections. This evidence base secured FDA approvals and the premium reimbursement positioning, creating a barrier for competitors lacking similar data.

Drainage Catheter Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.6% |

|

Base Year Market Size (2025) |

USD 2.2 billion |

|

Forecast Year Market Size (2035) |

USD 3.8 billion |

|

Regional Scope |

|

Drainage Catheter Market Segmentation:

Drainage Type Segment Analysis

Within the drainage type, the chest drainage catheters segment is poised to capture the share value of 38.4% by the end of 2035. The segment’s growth is primarily driven by the increasing prevalence of respiratory disorders, traumatic chest injuries, pleural effusion, and post-surgical thoracic complications requiring efficient fluid and air evacuation. Rising volumes of cardiovascular and pulmonary surgeries across hospitals and emergency care centers are further strengthening the demand for advanced chest drainage systems. Moreover, technological advancements such as anti-clogging catheter designs, minimally invasive insertion techniques, and integrated digital monitoring systems are improving patient outcomes and reducing hospitalization time. Growing adoption in intensive care units and emergency departments, combined with expanding healthcare infrastructure and higher critical care admissions globally, is expected to sustain strong drainage catheter market expansion throughout the forecast period.

End user Segment Analysis

The management of complicated pleural-pulmonary effusion and the empyema, requiring prompt antibiotics and drainage of the infected pleural fluid directly reinforces hospitals as the dominant end user sub-segment. According to the NLM October 2023 study, empyema carries a 15% mortality rate compared to simple effusion; early hospital-based pleural drainage is critical. However, about one-third of patients fail initial antibiotic and catheter drainage therapy, necessitating surgical intervention and extending hospital stays to 12 to 15 days, sometimes up to a month. Further drainage complexity increases due to loculations, septations, and high fluid viscosity. These factors drive sustained hospital demand for advanced active drainage catheters, pigtail designs, and thrombolytic-compatible systems. The inpatient pleural drainage procedures in U.S. hospitals are increasing annually, confirming hospitals’ clinical and economic centrality in managing complex pleural infections.

Catheter Design Segment Analysis

Pigtail catheters lead the catheter design segment due to their unique self-retaining curled tip, which prevents accidental dislodgement and allows safe, minimally invasive percutaneous drainage. As per the NLM April 2024 study, a randomized clinical trial of 40 patients directly supports the pigtail catheters as the leading catheter design sub-segment. The study compared bedside pigtail catheter placement with traditional 28 Fr tube thoracostomy for non-emergent traumatic pneumothorax. Pigtail catheters demonstrated a >50% reduction in the tube-site pain on the insertion day and for the following two days, with no significant difference in pain medication usage. Secondary outcomes, success rates, and complication rates were similar between the two groups. The study concluded that pigtail catheters offer less pain without compromising efficacy.

Our in-depth analysis of the drainage catheter market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Material |

|

|

Application |

|

|

End user |

|

|

Catheter Design |

|

|

Drainage Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Drainage Catheter Market - Regional Analysis

North America Market Insights

The North America dominated the drainage catheter market in 2025 and is poised to hold the regional revenue share of 38.8% by the end of 2035. The market is driven by a well-established hospital infrastructure and high procedure volumes for pleural effusion pneumonia-related complications and post-operative drainage. Demand for the drainage catheter market is shaped by the ongoing shifts from inpatient to outpatient settings, with ambulatory surgical centers and interventional radiology suites adopting pigtail catheters over traditional chest tubes. Public sector procurement, particularly via the Veterans Health Administration, has accelerated the transition to silicone-based single-use devices aligned with infection control mandates. Reimbursement structures continue to influence purchasing decisions, with hospitals favoring cost-effective, ready-to-use drainage kits. Further, the antimicrobial-coated catheters are gaining traction as the infection reduction remains a procurement priority across the major health systems.

Increasing urinary catheter utilization and the growing incidence of catheter-associated urinary tract infections are supporting demand growth of the drainage catheter market in the U.S. According to the Centers for Disease Control and Prevention, June 2025 data, nearly 75% of hospital-acquired urinary tract infections are linked to urinary catheters, while 15% to 25% of hospitalized patients require catheterization during treatment. Moreover, the NLM July 2023 study showed 30 million urinary catheters are inserted annually in the U.S., reflecting substantial procedural demand across hospitals and surgical centers. NLM January 2023 study depicts healthcare providers are increasingly adopting the advanced catheter systems, including balloon retained Foley and pigtail catheters, to improve drainage efficiency and reduce complications. Clinical studies have also demonstrated low complication and shorter discharge timelines with ultrasound-guided pigtail catheter procedures, supporting the broader adoption of the minimally invasive catheter-based drainage approaches in the acute and postoperative care settings.

Number of Patients Treated with Ultrasound-Guided Pigtail Catheter Drainage

|

Location of collection/abscess |

Number of patients |

Percentage (%) |

|

Liver |

18 |

37.5% |

|

Renal |

12 |

25% |

|

Ascites (Intra-peritoneal) |

6 |

12.5% |

|

Spleen |

6 |

12.5% |

|

Psoas muscle |

4 |

8.3% |

|

Pancreatic pseudocyst |

2 |

4.1% |

Source: NLM January 2023

The rising hospitalization volumes, aging demographics, and increasing government healthcare expenditure are shaping the drainage catheter market in Canada. According to the Elite Providers Hub for Progressive Play 2026 report, Canada’s total health spending reached USD 372 billion in 2024, representing about USD 9,547 per person, supporting continued procurement of hospital and interventional care devices. The Government of Canada reported in November 2024 that adults aged 65 years and older accounted for nearly 19% of the national population, increasing demand for urinary thoracic and postoperative drainage procedures associated with chronic diseases and surgical recovery. Moreover, the NLM July 2022 study recorded more than 3.1 million inpatient hospitalizations in Canada, reflecting a sustained procedural activity across the acute care facilities where drainage catheters are routinely utilized for infection control, fluid management, and minimally invasive interventions.

APAC Market Insights

Asia Pacific is projected to emerge as the fastest-growing region in the drainage catheter market and is expected to expand at a CAGR of 5.9% during the assessed period, 2026 to 2035. The drainage catheter market is driven by the significant diversity in healthcare infrastructure procurement models and clinical practices across established and emerging economies. Developed markets such as Japan, South Korea, and Austria prioritize premium silicon catheters and image-guided placement protocols similar to Western standards. Price-sensitive markets, including India, Indonesia, and Malaysia, see higher volumes of lower-cost polyurethane or PVC catheters often sourced from regional manufacturers. Increasing procedure volumes are supported by the expanding hospital networks and rising pneumonia and tuberculosis-related pleural complications across South and Southeast Asia.

The increasing incidence of pulmonary and extrapulmonary cancers is contributing to higher demand for pleural drainage catheters and indwelling pleural catheter systems, therefore driving the drainage catheter market in India. NLM October 2024 study shows that India has an estimated 2.5 million cancer cases with nearly 700,000 new registered cases and 556,000 cancer-related deaths annually. Malignant pleural effusion, a common complication in advanced cancers, frequently requires repeated therapeutic drainage and long-term fluid management. This growing healthcare burden is encouraging adoption of IPCs, which offer outpatient-based insertion, reduced hospitalization duration, lower re-intervention rates, and improved symptom control. Compared with conventional chest drain pleurodesis, IPC systems support ambulatory care and minimally invasive treatment pathways, making them relevant across resource-constrained and high-volume oncology care settings in India.

The Japan drainage catheter market is expanding rapidly and reached USD 61.60 million in 2025, and in 2026, the market is estimated at USD 66.96 million. Further, the market is set to reach USD 122.40 million by 2035 and is poised to expand at a CAGR 6.9% during the forecast period. The drainage catheter market is benefiting from increasing clinical research activity in malignant pleural effusion (MPE), neurovascular interventions, and colorectal cancer management. A 2025 first-in-human clinical study evaluating intrapleural TolueneSulfonamide for MPE incorporated catheter drainage as a core treatment component, reflecting rising adoption of minimally invasive pleural management approaches in oncology care. Moreover, the NLM January 2026 study shows Japan clinical studies involving 252 rectal cancer surgery patients across 47 specialized centers assessed transanal drainage tube (TDT) utilization in postoperative complication management. Japan is also advancing catheter navigation technologies, such as the LEONIS Mova steerable catheter, for complex transvenous embolization procedures, supporting innovation-driven demand growth across the interventional and surgical care settings.

Europe Market Insights

The Europe drainage catheter market is shaped by a mix of nationalized healthcare systems, centralized procurement frameworks, and country-specific reimbursement policies. Western European markets, including Germany, France, and the UK, emphasize the premium silicone and antimicrobial coated catheters with a strong preference for the pigtail designs in the interventional radiology and the pulmonology departments. South and East European countries exhibit higher price sensitivity, where the polyurethane and PVC catheters maintain a significant volume share. Public tenders via entities such as NHS Supply Chain in the UK and hospital consortia in Germany consolidate buyer power, compressing supplier margins. Adoption of the active drainage systems is growing, driven by infection reduction protocols and shorter hospital stay objectives.

Extensive healthcare infrastructure and rising medical expenditure are shaping the drainage catheter market in Germany. According to Germany’s Federal Ministry of Health, July 2025 data, national healthcare spending reached nearly USD 570 billion in 2022, accounting for more than 10% of the country’s GDP and exceeding USD 1.14 billion in healthcare expenditure per day. Germany also maintains a broad clinical care network comprising more than 1,800 hospitals, approximately 154,000 panel doctors, 33,700 outpatient psychotherapists, and nearly 17,000 pharmacies serving around 83 million residents. The large hospital base and high procedural volumes are increasing demand for thoracic, urological, cardiovascular, and postoperative drainage catheters used in surgical, oncology, and intensive care settings, while continued investment in hospital care is supporting the adoption of minimally invasive catheter-based interventions.

The growing population of long-term catheter users and the associated healthcare burden are contributing to the demand growth of the drainage catheter market in the UK. The NLM March 2024 study estimated that more than 90,000 people in the UK rely on long-term catheters, with prevalence rising from 0.14% in the general population to 1.22% among individuals aged over 80 years. The study also found that 71% of catheter users were above 70 years of age, reflecting increasing age-related demand for urinary drainage management. Long-term catheter care generated an estimated annual NHS expenditure of approximately USB 166.3 million, driven by hospitalizations, infections, catheter blockages, and community nursing support. Rising healthcare costs and complication rates are encouraging the adoption of improved catheter technologies and long-term drainage management solutions across UK healthcare settings.

UK Long-Term Catheter Utilization and Healthcare Cost Indicators, 2024

|

Market-Relevant Indicator |

Key Findings from UK Long-Term Catheter Study |

|

Community prevalence of long-term catheter use |

0.14% overall prevalence in the UK community population |

|

Catheter use among elderly population |

0.73% prevalence in people >70 years and 1.22% in people >80 years |

|

Estimated UK long-term catheter users |

More than 90,000 patients in the UK |

|

Gender distribution |

59.6% of users were male |

|

Elderly patient concentration |

71.2% of catheter users were above 70 years |

|

Catheter type usage |

60.8% used urethral catheters; 39% used suprapubic catheters |

|

Neurological condition-related catheterization |

57% of catheter users required catheters due to neurological disorders |

|

Average catheter duration |

Median duration ranged between 1–5 years |

|

Self-management trends |

47.1% of patients self-managed their catheters |

|

Hospital utilization |

13.6% of patients required inpatient hospital care related to catheter complications |

Source: NLM March 2024

Key Drainage Catheter Market Players:

- Medtronic (The U.S.)

- Teleflex Incorporated (The U.S.)

- Becton, Dickinson and Company (BD) (The U.S.)

- Boston Scientific Corporation (The U.S.)

- C. R. Bard (now part of BD) (The U.S.)

- Cook Medical (The U.S.)

- Merit Medical Systems (The U.S.)

- Fresenius Medical Care (Germany)

- B. Braun Melsungen AG (Germany)

- Coloplast Group (Denmark)

- Smiths Medical (UK)

- Argon Medical Devices (The U.S.)

- Terumo Corporation (Japan)

- Nipro Corporation (Japan)

- ResMed (The U.S.)

- SIRADA Medical (South Korea)

- Poly Medicure Limited (India)

- Vygon (France)

- Guerbet (France)

- Bearpac Medical, LLC (The U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Medtronic uses its global leadership in the minimally invasive therapies to offer advanced pleural and peritoneal drainage solutions. The company has integrated digital health features into its catheter systems, enabling the remote monitoring of the drainage volumes and pressure levels. Strategic initiatives include acquisitions of small-scale interventional device firms and expanding its portfolio in emerging markets.

- Teleflex Incorporated maintains a strong position in the drainage catheter market via its branded products used in chest and abdominal drainage. The company has adopted a strategy of continuous product innovation, including kink-resistant catheters and self-retaining loops for improved patient comfort. In 2025, the company made a net revenue of USD 3,047.3, maintaining a 2.4% growth as compared to 2023.

- Becton Dickinson and Company leverages its Bard acquisition to offer a comprehensive range of drainage catheters for urological, biliary, and abscess drainage. BD’s strategic focus includes developing closed system catheters that minimize the infection risk and integrating smart sensors for real-time output tracking. The company has initiated a partnership with hospital networks to standardize drainage protocols.

- Boston Scientific Corporation competes strongly in the drainage catheter market by focusing on interventional gastroenterology and nephrology applications, including nephrostomy and biliary drainage catheters. The company’s key strategic initiatives are the development of next-gen catheters with enhanced visibility under fluoroscopy and MRI-compatible materials. In 2024, the company made a net sale of USD 16.7 billion.

- C.R. Bard was a dominant player in the drainage catheter market, known for its Navarre and Dawson Mueller drainage catheters. Bard pioneered many catheter designs with locking pigtail loops and echogenic tips for ultrasound guidance. Its strategic initiatives included expanding into the home healthcare drainage kits and establishing direct distribution channels in APAC.

Here is a list of key players operating in the global drainage catheter market:

The global drainage catheter market is moderately fragmented, with the key players focusing on product innovation, minimally invasive designs, and geographic expansion. Leading companies are increasingly adopting strategies such as mergers and acquisitions, partnerships with healthcare providers, and development of antimicrobial or image-guided catheters to improve patient outcomes. For example, in April 2024, Vygon announced the acquisition of Macatt Medica, a Peruvian distribution company. Intense competition exists between U.S.-based giants and the established European firms, while Asia Pacific manufacturers are gaining traction via cost-effective solutions. Regulatory compliance and patient safety remain central, pushing firms to invest in advanced materials and ergonomic designs to reduce complications such as infections or blockages.

Corporate Landscape of the Drainage Catheter Market:

Recent Developments

- In January 2025, Guerbet, a global specialist in contrast agents and solutions for medical imaging, announced the divestment of assets of Accurate Medical Therapeutics, Ltd., the developer, manufacturer, and distributor of DraKon™ and SeQure® microcatheters, to Argon Medical, a leading provider of medical device solutions for Interventional Radiology, Vascular Surgery, Interventional Cardiology, and Oncology procedures.

- In January 2025, Argon Medical announced the acquisition of certain assets of Accurate Medical Therapeutics, Ltd., the manufacturer and distributor of the DraKon™ and SeQure® microcatheters, from Guerbet SA. The addition of the SeQure and Drakon microcatheters to Argon's portfolio extends the company's oncology offering to include therapeutic devices and accessories.

- In September 2024, Bearpac Medical, LLC announced the launch of the AESOP clinical trial for Assessing Experience, Safety, and Outcomes of the Passio Pump Drainage System – (AESOP). AESOP is a single center, crossover, non-blinded 1:1 randomised controlled trial, recruiting at North Bristol NHS Trust. Participants will be randomised to IPC insertion with either a Bearpac Passio catheter or a standard catheter (BD PleurX).

- Report ID: 4172

- Published Date: May 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.