Diabetes Devices Market Outlook:

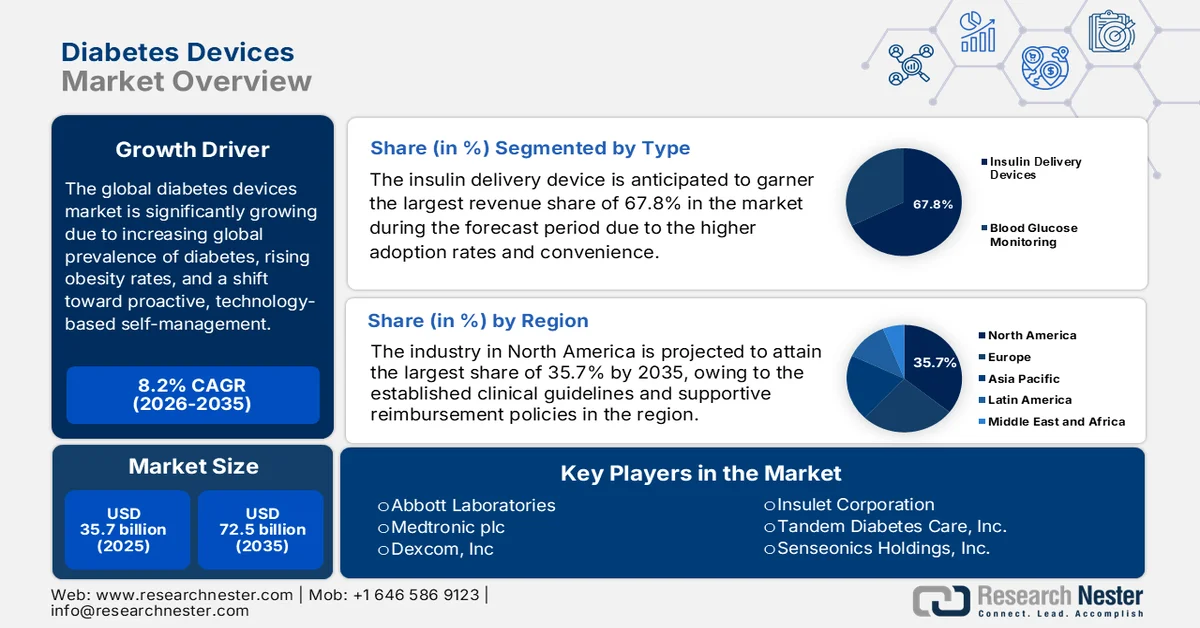

Diabetes Devices Market size was valued at USD 35.7 billion in 2025 and is projected to surpass USD 72.5 billion by the end of 2035, rising at a CAGR of 8.2% during the forecast period, i.e., 2026 to 2035. In 2026, the industry size of diabetes devices is evaluated at USD 38.6 billion.

The global diabetes devices market is undergoing a significant transformation, which is shaped by the increasing global prevalence of diabetes, rising obesity rates, and a shift toward proactive, technology-based self-management. Also, the rising awareness of long-term complications among the population is fueling robust market growth. According to the World Health Organization (WHO) November 2024 article, the number of people living with diabetes surged from 200 million three decades ago to 830 million in 2022, and the prevalence has been rising faster in low‑ and middle‑income countries. In 2022, 59% of adults who were aged 30 and above were not taking medication, whereas diabetes resulted in 1.6 million deaths in 2021. Mortality rates from diabetes have been rising continuously, denoting the urgent need for innovative devices and broader treatment coverage.

Top 10 Countries by Number of Adults (20-79 Years) Living with Diabetes in 2021 and Projected Estimates for 2045: Statistically Validated Forecasts

|

Rank (2021) |

Country or Territory |

Number of People with Diabetes (millions) |

Rank (2045) |

Country or Territory |

Number of People with Diabetes (millions) |

|

1 |

China |

140.9 |

1 |

China |

174.4 |

|

2 |

India |

74.2 |

2 |

India |

124.9 |

|

3 |

Pakistan |

33.0 |

3 |

Pakistan |

62.2 |

|

4 |

U.S. |

32.2 |

4 |

U.S. |

36.3 |

|

5 |

Indonesia |

19.5 |

5 |

Indonesia |

28.6 |

|

6 |

Brazil |

15.7 |

6 |

Brazil |

23.2 |

|

7 |

Mexico |

14.1 |

7 |

Bangladesh |

22.3 |

|

8 |

Bangladesh |

13.1 |

8 |

Mexico |

21.2 |

|

9 |

Japan |

11.0 |

9 |

Egypt |

20.0 |

|

10 |

Egypt |

10.9 |

10 |

Turkey |

13.4 |

Source: NIH

Furthermore, escalating demand for management solutions and significant trade flow are stimulating consistent growth in the diabetes devices market. According to the official statistics published by the U.S. International Trade Commission in March 2024, globally, more than 500 million people live with diabetes, and projections suggest nearly 800 million by 2045. In this context, the continuous glucose monitors (CGM) have become vital tools, with the global CGM market expected to grow at a 13% annual rate, with U.S. exports rising by 193.7% and imports by 229.5% between 2000 and 2021. In the U.S., diabetes cases have been continuously rising, thereby driving demand for CGMs. Commercially insured patients are 2.5 to 4.3 times more likely to use them than Medicaid enrollees. These utilization rates and the expanding global trade of insulin medications increase the demand for insulin delivery systems, hence reflecting a huge growth opportunity for the diabetes devices market’s expansion.

Top Global Exporters of Insulin Medicaments for Retail Sale - Trade Value & Volume Analysis, 2024

|

Country / Region |

Trade Value (USD ‘000) |

Quantity (Kg) |

|

Germany |

2,094,731.21 |

1,477,590 |

|

European Union |

1,930,898.52 |

8,706,430 |

|

France |

1,548,610.25 |

7,397,080 |

|

U.S. |

516,564.14 |

1,351,490 |

|

India |

146,316.71 |

2,598,720 |

|

Hungary |

110,495.30 |

613,692 |

|

Malaysia |

103,295.55 |

1,121,520 |

|

Italy |

98,626.23 |

328,017 |

|

Turkey |

72,295.47 |

140,330 |

|

Singapore |

66,973.07 |

471,701 |

|

Slovenia |

65,179.81 |

270,587 |

Source: WITS

Key Diabetes Devices Market Insights Summary:

Regional Highlights:

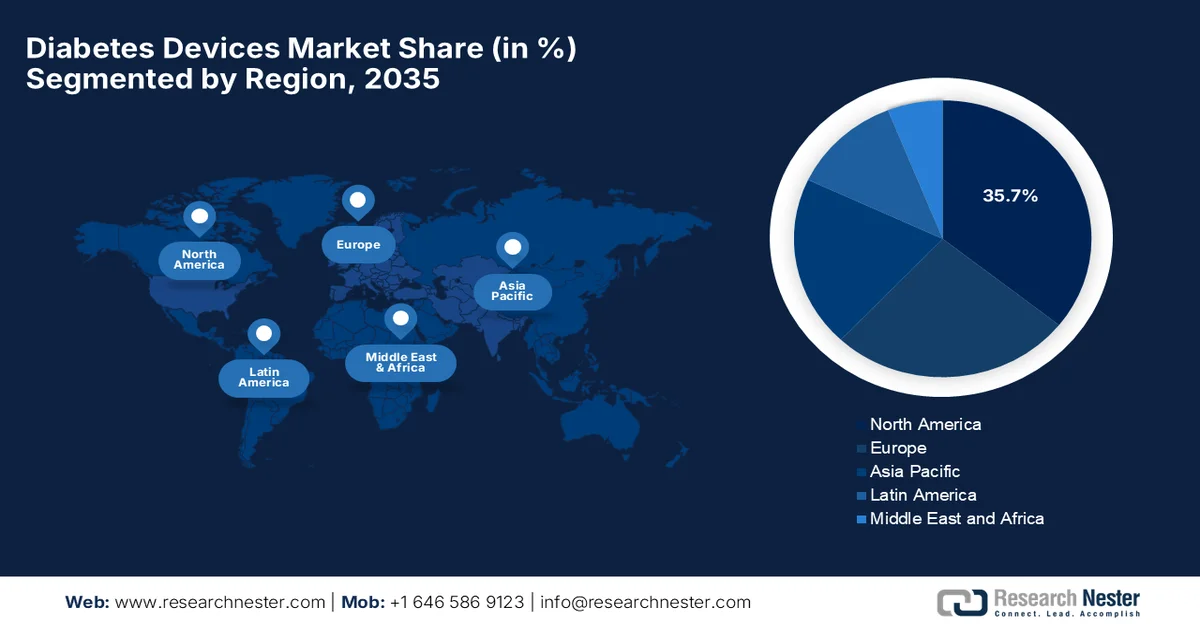

- North America is anticipated to dominate the diabetes devices market with a 35.7% share by 2035, attributed to strong reimbursement frameworks and supportive regulatory approvals for advanced monitoring technologies.

- Asia Pacific is expected to witness rapid expansion by 2035, impelled by increasing health awareness and the rise of affordable, locally manufactured diabetes care solutions.

Segment Insights:

- Insulin Delivery Device is projected to account for a 67.8% share by 2035 in the diabetes devices market, fueled by rising adoption and enhanced convenience through advanced technologies like patch pumps and smart insulin pens.

- Automated Insulin Delivery System is expected to witness substantial growth by 2035, propelled by integration with digital health platforms and smartphone applications improving real-time monitoring capabilities.

Key Growth Trends:

- Growing geriatric population

- Technological advancements & innovation

Major Challenges:

- Reimbursement and insurance limitations

- Competition from alternative therapies

Key Players: Abbott Laboratories, Medtronic plc, Dexcom Inc., Insulet Corporation, Tandem Diabetes Care Inc., Senseonics Holdings Inc., Eli Lilly and Company, Roche Diabetes Care, Ascensia Diabetes Care, Johnson & Johnson, Ypsomed AG, Omron Healthcare, Nipro Corporation, Terumo Corporation, LifeScan Inc., Sequel MedTech, Becton Dickinson & Co., Lupin Limited, DEKA Research & Development, Diatech Diabetes Inc., Zydus Lifesciences Limited, SOOIL Development Co. Ltd.

Global Diabetes Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 35.7 billion

- 2026 Market Size: USD 38.6 billion

- Projected Market Size: USD 72.5 billion by 2035

- Growth Forecasts: 8.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 26 March, 2026

Diabetes Devices Market - Growth Drivers and Challenges

Growth Drivers

- Growing geriatric population: Older adults are more prone to diabetes, and prevalence rates are higher among people aged above 65, creating a sustained demand in the diabetes devices market. Therefore, aging populations globally are increasing long-term demand for diabetes management devices. As per an article published by the University of Chicago Medical Center in April 2024, diabetes affects 38.4 million people, or 11.6% of the population in the U.S., and in terms of older adults, nearly 1 in 3 individuals aged 65 and above live with diabetes, which reflects age as a major risk factor. Besides, type 2 diabetes accounts for 90% to 95% of all cases, whereas about 2 million residents in the U.S. have Type 1 diabetes. The report highlights that complications are more severe in the older age group, which increases the risks of cardiovascular disease, kidney disease, neuropathy, and vision loss.

- Technological advancements & innovation: Rapid innovation is transforming the growth dynamics of the diabetes devices market. Devices such as continuous glucose monitoring, smart insulin pens, and automated, closed-loop insulin delivery systems are gaining enhanced popularity in technologically developed economies. In August 2024, the U.S. Food and Drug Administration (FDA) approved Insulet’s SmartAdjust technology for automated insulin dosing in adults with type 2 diabetes, thereby expanding its prior use in type 1 diabetes. The article notes that this interoperable glycemic controller efficiently connects with insulin pumps and continuous glucose monitors to automatically adjust insulin delivery. Hence, such regulatory support provides individuals with type 2 diabetes a new option to reduce the burden of daily insulin management, making it suitable for standard diabetes devices market growth.

- Shift toward home healthcare & self-management: There has been an increasing preference for home-based care and self-monitoring. Patients use devices to track glucose levels, administer insulin, and manage their condition independently. Therefore, this trend boosts the overall growth of the diabetes devices market. According to the article published by WHO in April 2024, self-care interventions, including the self-monitoring of blood glucose, are highly essential for diabetes management and can be performed independently at home. In addition, these interventions utilize user-friendly devices and digital tools, which allow individuals to manage their own health while complementing formal healthcare systems. WHO also underscores that such approaches improve accessibility, support universal health coverage, and enhance overall patient well-being, thus positively impacting the diabetes devices market’s growth and exposure.

Challenges

- Reimbursement and insurance limitations: While most of the developed economies offer suitable reimbursements, it is still inconsistent in emerging nations, which presents insurance coverage as a hurdle directly impacting the diabetes devices market. The aspect of high out-of-pocket costs for CGMs, insulin pumps, or test strips discourage widespread usage among patients from price-sensitive regions. Also, most of the insurers impose strict eligibility criteria or limit coverage duration. On the other hand, the delays in reimbursement approvals create financial uncertainty for both providers and patients. Market growth is often constrained in countries with inadequate public healthcare support. Therefore, manufacturers in this sector need to navigate complex payer landscapes, demonstrate cost-effectiveness, and advocate for broader coverage.

- Competition from alternative therapies: Companies involved in the diabetes devices market face incremental pressure from alternative approaches, i.e., oral medications, lifestyle changes, and emerging digital therapeutics. In this context, patients mostly prefer non-invasive treatments when compared to continuous monitoring or injections. Even the pharmaceutical companies developing advanced therapies can shift focus away from device adoption. Therefore, the existence of this competition encourages device manufacturers to differentiate products through superior accuracy and integration with holistic care plans, whereas failing to demonstrate clinical and quality-of-life benefits may reduce market penetration. Furthermore, new entrants with innovative, low-cost solutions can disrupt the well-established market dynamics.

Diabetes Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

8.2% |

|

Base Year Market Size (2025) |

USD 35.7 billion |

|

Forecast Year Market Size (2035) |

USD 72.5 billion |

|

Regional Scope |

|

Diabetes Devices Market Segmentation:

Type Segment Analysis

In terms of type, the insulin delivery device is anticipated to garner the largest revenue share of 67.8% in the diabetes devices market during the forecast period. The higher adoption rates and convenience are the major factors behind the subsegment’s dominance. The technological improvements, such as patch pumps and smart insulin pens, have readily enhanced ease of use and accuracy, thereby efficiently boosting overall adoption rates. In December 2025, Medtronic announced the launch of the MiniMed 780G system in the U.S., which is now integrated with Abbott’s Instinct sensor. The Instinct sensor is the world’s smallest and thinnest CGM, providing glucose readings that allow the system to automate insulin adjustments every five minutes. Therefore, such continued innovations expand the segment’s growth potential, supporting a smart, connected insulin delivery ecosystem.

Technology Segment Analysis

The automated insulin delivery system is predicted to grow at a significant rate in the diabetes devices market by the conclusion of the forecast period. The growth of the segment is mainly propelled by the integration with digital health platforms and smartphone applications, which enhances real-time monitoring. In May 2023, the U.S. FDA cleared the Beta Bionics iLet ACE Pump and iLet dosing decision software for people aged six and older with type 1 diabetes. Together with a compatible continuous glucose monitor, these devices form the iLet Bionic Pancreas, an automated insulin dosing system. In addition, the segment’s expansion will also be driven by increasing adoption in outpatient and pediatric care settings, wherein these algorithm-based insulin delivery reduces clinical burden and improves glycemic control metrics. Hence, such developments are positioning automated insulin delivery systems at the forefront of the shift toward data-driven, precision diabetes management.

End user Segment Analysis

Hospitals' sub-segment, which is under the end user segment, is expected to attain a lucrative revenue share in the diabetes devices market during the stipulated timeframe. The segment’s growth is largely attributable to a higher rate of hospital admissions for disease management, which is driving demand for advanced monitoring within clinical settings. Physician guidance plays a critical role in terms of device selection, as healthcare professionals recommend solutions that are suitable for individual patient needs. In December 2025, the American Diabetes Association (ADA) reported that hospitalized patients with diabetes benefit from diabetes or glucose management teams, which can improve glycemic control, reduce complications, and shorten hospital stays. Studies show that such teams lower rates of hyperglycemia and hypoglycemia by 30% to 40% when compared to usual care, and it reduces 30‑day readmission risks and healthcare costs, thus making them suitable for bolstering the segment’s growth.

Our in-depth analysis of the diabetes devices market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Technology |

|

|

End user |

|

|

Application |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Diabetes Devices Market - Regional Analysis

North America Market Insights

The North America diabetes devices market is predicted to account for the largest revenue share of 35.7% during the forecast period. The leadership of the region is effectively attributable to established clinical guidelines and reimbursement mechanisms that support diabetes device adoption. The region’s market is also supported by the U.S. FDA approvals for over-the-counter wearable sensors. As per the article published by ADA in June 2025, in a span of four years, Medicare fee‑for‑service beneficiaries with type 1 diabetes showed rising use of diabetes management devices. It states that among 321,000 patients, two‑thirds were aged above 65, and the prevalence of type 1 diabetes increased from 0.55% to 0.63%. Besides, the device usage grew from 43.3% to 59.9%, with yearly rise being 2.2% to 5.5%, which is largely driven by continuous glucose monitor adoption. About half of the devices were dependent on both CGMs and insulin pumps, reflecting Medicare’s expanded coverage and growing acceptance of advanced technologies.

The diabetes devices market in the U.S. is growing due to continued technological innovations and generous government funds. The market is currently making a shift from traditional monitoring toward integrated ecosystems that combine wearable sensors with automated insulin delivery systems. In February 2026, Congress passed bipartisan legislation extending the Special Diabetes Program (SDP) through December 2026, thereby increasing annual funding from USD 160 million to USD 200 million and boosting NIH diabetes research funding by a total of USD 10 million. The SDP, created by Congress and administered by the NIH, has contributed nearly USD 3.6 billion to type 1 diabetes (T1D) research, supporting breakthroughs and the first therapy shown to delay T1D onset. The article highlights that SDP has generated an amount of USD 50 billion in healthcare savings, underscoring its strong impact on patients, research, and taxpayers.

Expanding provincial and territorial coverage is the main factor which is responsible for the overall diabetes devices market growth in Canada. The market is evolving as government initiatives and private insurers are subsidizing wearable technologies to improve long-term health outcomes. In this context, in February 2024, the country’s government, through Bill C-64, announced that it is moving toward universal pharmacare by providing single-payer coverage for essential diabetes medications in partnership with willing provinces and territories. Along with this, a federal fund will support access to diabetes devices and supplies such as syringes, insulin pumps, glucometers, and continuous glucose monitors. This program standardizes coverage and affordability, and it aims to reduce the financial burden on patients and cost savings for the healthcare system.

APAC Market Insights

The Asia Pacific diabetes devices market is seeing rapid growth, propelled by rising health consciousness among the middle-class population. The region is characterized by the emergence of affordable domestic manufacturers along with localized production hubs, which are mainly aimed at addressing price-sensitive rural and semi-urban populations. Based on the government data from Japan, in January 2026, Light Touch Technology (LTT) Inc. developed a non-invasive blood glucose sensor using advanced mid-infrared laser technology. This particular device measures glucose levels through a fingertip in just five seconds by eliminating the need for painful blood draws and reducing infection risks. Hence, such instances indicate that the Asia Pacific is becoming a hub for patient-friendly healthcare solutions, wherein the continued advancements by local startups are addressing both medical needs and affordability.

The government initiatives for better, more accessible healthcare are driving the diabetes devices market in China. The country’s market also benefits from insatiable demand for CGM systems, insulin pumps, and digital health tools, which are influenced by the rise of e-commerce platforms, and they have become key distribution channels along with traditional hospital sales. In July 2024, the Healthy China Action diabetes prevention and control implementation plan 2024 to 2030 highlighted that prevention is highly essential by integrating medical treatment with public health education, and strengthening healthcare. It outlines measures such as nationwide awareness campaigns, early screening, standardized diagnosis and treatment, and the use of both traditional domestic and Western medications. In addition, by 2030, the plan aims to improve diabetes management, reduce complications, and build a supportive environment that enhances public health literacy and lowers the disease burden.

The diabetes devices market in India is gaining increased exposure owing to the presence of a large patient base, high-tech adoption in urban centers, and basic monitoring in rural areas. The rise in terms of telemedicine and mobile health apps is readily transforming the sector, as patients in the country look for digital ecosystems that provide remote doctor consultations along with glucose data tracking. As stated by Press Information Bureau (PIB) in January 2026, the Government of India, through the Technology Development Board (TDB) and Department of Science & Technology, entered into a partnership with Drstore Healthcare Service India Pvt. Ltd., and it is a collaborative R&D Programme to develop an advanced continuous glucose monitoring device incorporated with cardiovascular biomarkers. This innovation aims to enable monitoring of both diabetes and heart health, thereby supporting early detection and preventive care. Therefore, such projects strengthen India’s digital health ecosystem and promote affordable, scalable healthcare solutions.

Europe Market Insights

Europe diabetes devices market is forecasted to emerge as a powerful region in the global dynamics. The region’s growth is mainly attributable to universal healthcare systems and a strong emphasis on long-term cost-effectiveness. The government-led reimbursement programs drive the integration of automated insulin delivery systems and closed-loop technologies. As per the official data published in February 2026, the International Diabetes Federation (IDF) Europe is driving integrated, person-centred diabetes action across the continent, aligning with major regional and WHO initiatives. The focus is on breaking siloed care by linking diabetes with cardiovascular disease and other NCDs. Besides, IDF Europe is prioritizing innovation by advocating for simplified clinical trials. At the same time, it calls for robust oversight of medical devices and an Innovation Pathway to fast-track safe, effective breakthrough technologies for people with diabetes, hence making it suitable for standard diabetes devices market growth.

A highly structured statutory health insurance system that provides coverage for advanced technologies is rearranging the growth dynamics of the diabetes devices market in Germany. The national guidelines now prioritize continuous monitoring and pump therapy for a broad patient demographic. In the context, the country’s statutory health insurer, KKH, in April 2024 announced the expansion of coverage to include Abbott’s FreeStyle Libre 3 continuous glucose monitoring system for people with type 2 diabetes on basal insulin-supported oral therapy. This marks the first time CGM devices are reimbursed for such patients, thereby offering a painless alternative to routine blood tests, whereas the initiative aims to improve glucose control and prevent complications. From a strategic perspective, such instances in the country denote that policy-driven access to advanced diabetes technologies is a key factor that is responsible for reshaping diabetes devices market growth and adoption dynamics.

The UK diabetes devices market is strongly supported by a push for integrated care systems, where wearable sensors and insulin pumps are linked to digital platforms to streamline data sharing between patients and clinical teams. The country is considered to be a major hub for closed-loop technology trials, which is fostering a dynamic environment where manufacturers focus on cost-effectiveness in the long term. In January 2024, National Health Service England published a 5-year implementation strategy for hybrid closed-loop technologies by linking continuous glucose monitoring with insulin pumps, with the main goal to support people with type 1 diabetes. The phased rollout is focused on equitable access, targeting patients most likely to benefit, children, pregnant women, and adults with high HbA1c or disabling hypoglycaemia. The strategy also concentrates on workforce training, patient education, and cost-effective procurement in line with NICE guidance, whereas specialist centres lead in terms of early adoption.

Key Diabetes Devices Market Players:

- Abbott Laboratories (U.S.)

- Medtronic plc (U.S.)

- Dexcom, Inc. (U.S.)

- Insulet Corporation (U.S.)

- Tandem Diabetes Care, Inc. (U.S.)

- Senseonics Holdings, Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Roche Diabetes Care (Switzerland)

- Ascensia Diabetes Care (Switzerland)

- Johnson & Johnson (U.S.)

- Ypsomed AG (Switzerland)

- Omron Healthcare (Japan)

- Nipro Corporation (Japan)

- Terumo Corporation (Japan)

- LifeScan, Inc. (U.S.)

- Sequel MedTech (U.S.)

- Becton Dickinson & Co. (U.S.)

- Lupin Limited (India)

- DEKA Research & Development (U.S.)

- Diatech Diabetes Inc. (U.S.)

- Zydus Lifesciences Limited (India)

- SOOIL Development Co., Ltd. (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Abbott Laboratories is a global leader in diabetes care, which is best known for its FreeStyle Libre continuous glucose monitoring systems. The company is highly focused on sensor-based technology to reduce patient burden, thereby providing real-time glucose data for better self-management.

- Medtronic plc maintains a leading position in the diabetes devices market due to its expertise in insulin delivery and CGM technology. The firm’s devices emphasize integration with ultra-rapid-acting insulins and compatibility with various glucose sensors by targeting both type 1 and insulin-requiring type 2 diabetes populations.

- Dexcom, Inc. has established a leading position in the type 1 diabetes segment. Besides, the company proactively collaborates with technology partners with the main goal of improving patient adherence and enhancing overall personalized diabetes care.

- Insulet Corporation is a pioneer in terms of tubeless insulin pump technology through its Omnipod platform. In addition, the firm is highly focused on convenience, automation, and connectivity, which enables seamless integration with CGM devices for hybrid closed-loop therapy.

- Tandem Diabetes Care, Inc. is a prominent player that specializes in insulin delivery systems with improved hybrid closed-loop technology. Global distribution networks and continuous R&D to improve automation and connectivity are a few of the tactical strategies adopted by the firm to secure a leading market position in the years ahead.

Below is the list of some prominent players operating in the global diabetes devices market:

The global diabetes devices market is extremely competitive, and it is characterized by intense innovation and strategic positioning by key multinational and regional players. The U.S.-based firms, such as Abbott, Dexcom, and Insulet, lead in terms of continuous glucose monitoring and insulin delivery technologies, whereas companies from Europe, such as Roche and Ypsomed, are focused on integrated diabetes care solutions. Companies in this sector pursue advanced CGMs, hybrid closed‑loop systems, and digital integration, with a prime focus on regulatory approvals, reimbursement expansion, acquisitions, and partnerships to drive adoption and long‑term connectivity in diabetes management. In October 2025, DEKA Research & Development announced the acquisition of the core assets and intellectual property of Diatech Diabetes to strengthen its expertise in safe insulin infusion technology.

Corporate Landscape of the Diabetes Devices Market:

Recent Developments

- In March 2026, Lupin Limited announced a strategic licensing and supply agreement with Zydus Lifesciences Limited to expand access to Semaglutide Injection using a reusable pen device. Under this partnership, Lupin will co-market the product under Semanext and Livarise, whereas Zydus will continue with SEMAGLYN, MASHEMA, and ALTERME.

- In March 2026, Tandem Diabetes Care announced that its Tandem Mobi automated insulin delivery system is now compatible with Android smartphones in the U.S., expanding accessibility beyond iPhone users.

- In February 2026, Medtronic announced three of its milestones in the U.S. to expand access and flexibility for people with type 1 and insulin‑requiring type 2 diabetes. These include Medicare coverage for the MiniMed 780G system with Abbott’s Instinct sensor, U.S. FDA clearance for use with ultra-rapid-acting insulins, and approval of the system with the Instinct sensor for insulin‑requiring type 2 diabetes.

- In January 2026, Senseonics, in partnership with Sequel MedTech, announced the launch of the first integration of the Eversense 365 implantable CGM with the Twiist automated insulin delivery system, which offers type 1 diabetes patients personalized and long-term glucose monitoring.

- Report ID: 4642

- Published Date: Mar 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.