Cookware Market Outlook:

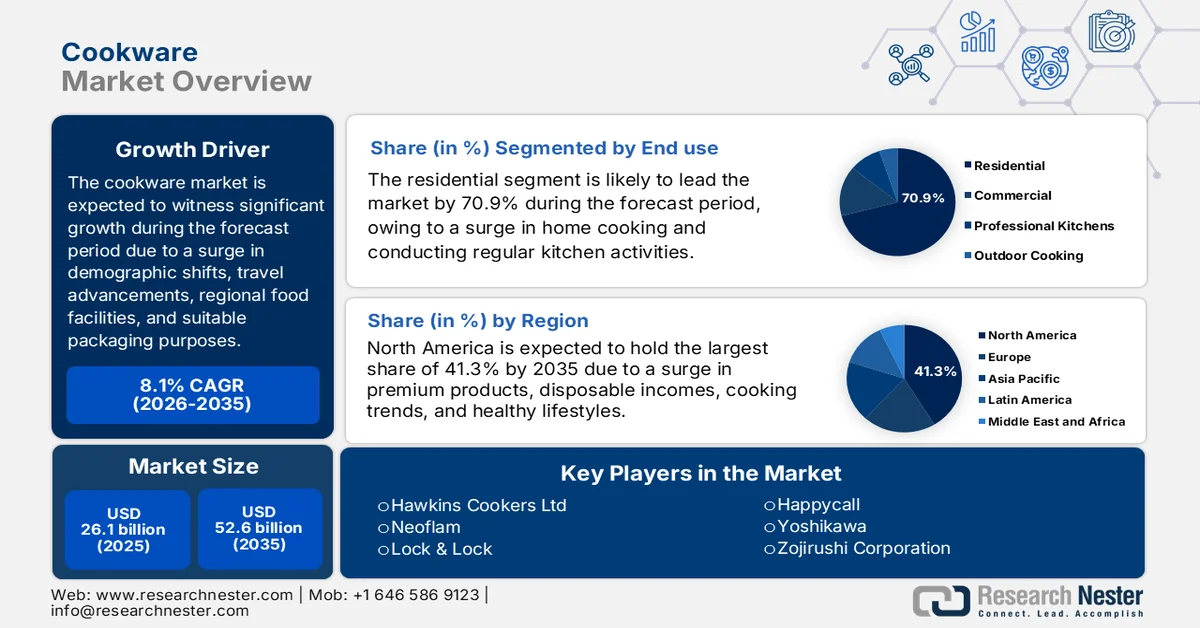

Cookware Market size was valued at USD 26.1 billion in 2025 and is projected to reach USD 52.6 billion by the end of 2035, with a CAGR of 8.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of cookware is estimated at USD 28.2 billion.

The worldwide cookware market is gradually being uplifted by certain factors that are shaping the overall operational landscape. These factors include demographic transitions, increased urbanization, cultural exchange through digital media and travel, growth in regional food businesses, climate consciousness for packaging purposes, and the aging population. According to official statistics published by the USDA Government in January 2025, there has been an increase in the demand for food imports by 12%, particularly in China. Besides, as per an article published by the World Health Organization (WHO) in January 2026, in terms of nutrition, the adult population needs to consume energy, 15% of which derives from fat, which accounts for 30% of overall daily calories. Therefore, with increased demand and nutrient focus, there is a huge growth in the cookware market globally.

Furthermore, the aspect of color psychology, kitchen aesthetics as a purchase motive, a rise in heritage and regional craftsmanship, and the presence of try-before-you-buy and subscription-based cookware models are certain trends that are responsible for bolstering the cookware market globally. As stated in an article published by NLM in July 2023, in terms of craftsmanship, steel cookware is readily utilized for food preparation that comprises 18% of chromium, 8% of nickel, along with 70% to 73% of iron. These particular chemical elements tend to discharge from the material into the food, but these are more thermostable than aluminum cookware and have the capacity to withstand sweltering temperatures. Besides, the utilization of X-ray fluorescence (XRF) is increasingly utilized to determine the elemental composition, based on which there is a continuous supply of kitchenware and tableware, which caters to the market development globally.

2024 Global Kitchenware and Tableware Export/Import Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

China |

1.4 billion |

- |

|

India |

15 million |

- |

|

Vietnam |

103 million |

- |

|

U.S. |

- |

463 million |

|

Japan |

- |

262 million |

|

Germany |

- |

152 million |

|

Global Trade Valuation |

2.2 billion |

|

|

Global Trade Share |

0.0098% |

|

|

Export Growth |

5.7% |

|

Source: OEC

Key Cookware Market Insights Summary:

Regional Highlights:

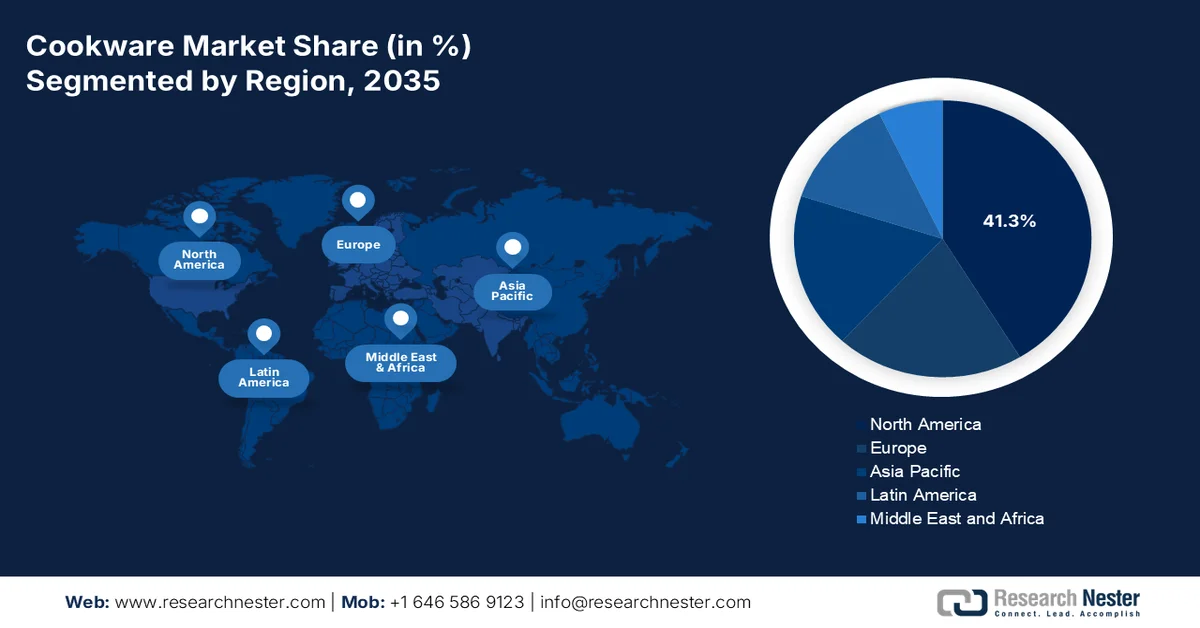

- North America cookware market is projected to dominate with a 41.3% share by 2035, bolstered by rising preference for premium cookware and increasing home cooking duration among consumers

- Asia Pacific is anticipated to register the fastest growth over 2026-2035, stimulated by rapid urbanization and expanding middle-class population

Segment Insights:

- Residential segment in the cookware market is expected to hold a 70.9% share by 2035, propelled by the universal prevalence of daily home cooking activities across households

- Offline sub-segment is likely to secure the second-highest share by 2035, fueled by consumer preference for physical product evaluation before purchase

Key Growth Trends:

- Increase in culinary education

- Surplus in kitchen commercial

Major Challenges:

- Intense price competition and margin erosion

- Health, safety, and regulatory compliance

Key Players: Groupe SEB (France), Newell Brands (U.S.), Zwilling J.A. Henckels (Germany), WMF Group (Germany), Fissler GmbH (Germany), Meyer Corporation (U.S.), Tramontina S.A. (Brazil), TTK Prestige Ltd (India), Hawkins Cookers Ltd (India), Neoflam (South Korea), Lock & Lock (South Korea), Happycall (South Korea), Yoshikawa (Japan), Zojirushi Corporation (Japan), Tiger Corporation (Japan), The Vollrath Company, LLC (U.S.), Le Creuset (France), IKEA (Sweden), Carote (China), Williams Sonoma (U.S.).

Global Cookware Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 26.1 billion

- 2026 Market Size: USD 28.2 billion

- Projected Market Size: USD 52.6 billion by 2035

- Growth Forecasts: 8.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (41.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: Vietnam, Indonesia, Brazil, Mexico, Thailand

Last updated on : 17 April, 2026

Cookware Market - Growth Drivers and Challenges

Growth Drivers

- Increase in culinary education: The increasing growth of long-term cooking content on social media platforms, as well as dedicated recipe applications, is directly expanding the cookware market globally. The purpose of these platforms and applications is to make people aware of different culinary practices, along with cooking strategies. For instance, according to official statistics published by the IEA Organization in 2026, 2.3 billion people globally, which is nearly 1/3rd of the worldwide population, prefer cooking meals over basic stoves and open fires. Besides, the number of people without accessibility to clean cooking is projected to decline from 2.3 billion to 1.8 billion by the end of 2030. Therefore, the utilization of social media and application-based content has resulted in people gaining access to clean cooking, which is positively uplifting the market across different regions.

Overall People Accessing Clean Cooking by Region (2020-2030)

|

Regions/Countries |

2020 |

2030 |

|

Sub-Sahara Africa |

80 million |

1,192 million |

|

India |

514 million |

452 million |

|

China |

394 million |

172 million |

|

Indonesia |

137 million |

45 million |

|

Rest of the world |

198 million |

212 million |

|

Other Asia |

63 million |

374 million |

Source: IEA Organization

- Surplus in kitchen commercial: The cyclical replacement of cookware in the hospitality industry creates a secondary supply system that drives the growth of the cookware market. As stated in a data report published by the United Cities and Local Governments (UCLG) in September 2025, the worldwide food system is considered one of the major drivers of climate modification, which presently accounts for approximately 25% to 30% of the overall greenhouse gas emissions. Based on this food system, large-scale restaurants are focused on replacing their cookware on fixed schedules regardless of the condition. In addition, this particular kitchen surplus is currently captured by specialized resellers that professionally certify and restore commercial-based pieces for home use, thus proliferating the cookware market expansion.

- Shift from microwave to stovetop in emerging countries: The fundamental transition in cooking energy facilities across Southeast and South Asia is also fueling the sustained cookware demand worldwide. As per an article published by NLM in October 2024, 26% of the population across India, Nigeria, and Benus State highly depend on conventional stoves that are powered by biomass for cooking purposes. Moreover, based on an article published by the FSR Global Organization in January 2026, the aspect of household air pollution from cooking fuels significantly caused roughly 2.8 million deaths globally as of 2023. In addition, the air pollution in India, originating from household cooking smoke, is effectively responsible for over 2 million deaths in the year, which has made it the utmost public health risk in the nation, thereby enhancing the increased demand for kitchen cooktops.

Challenges

- Intense price competition and margin erosion: The cookware market faces relentless price pressure from low-cost manufacturing hubs, particularly in regions with lower labor and material costs. This eventually forces established brands to constantly defend their market share against aggressive discounting by new entrants and private labels. Large retailers leverage their buying power to demand lower wholesale prices, squeezing margins for manufacturers who must maintain quality. Simultaneously, consumers have grown accustomed to frequent sales events and expect premium features at economy prices. This dynamic makes it difficult for companies to invest in research and development or premium marketing campaigns. Small and mid-sized players struggle to survive unless they carve out a niche or differentiate through design or material innovation.

- Health, safety, and regulatory compliance: The aspect of growing consumer awareness regarding toxic coatings, heavy metals, and chemical leaching presents a formidable challenge for manufacturers in the cookware market. Moreover, regulatory bodies across North America and Europe are continuously updating safety standards for non-stick coatings, including restrictions on PFAS, PFOA, and other perfluorinated compounds. Besides, compliance requires constant reformulation of materials, extensive third-party testing, and recertification processes that add significant operational complexity. Brands that fail to meet these evolving standards face product recalls, lawsuits, and irreversible reputational damage. Simultaneously, the rise of social media has amplified consumer skepticism, with viral videos questioning the safety of scratched non-stick pans or discolored ceramic surfaces.

Cookware Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.1% |

|

Base Year Market Size (2025) |

USD 26.1 billion |

|

Forecast Year Market Size (2035) |

USD 52.6 billion |

|

Regional Scope |

|

Cookware Market Segmentation:

End use Segment Analysis

Based on end use, the residential segment in the cookware market is anticipated to garner the highest share of 70.9% by the end of 2035. The segment’s upliftment is primarily attributed to the aspect that cooking at home remains a universal daily activity across all demographics and economies. According to official statistics published by NLM in March 2022, in terms of demographics, it is predicted that by the end of 2026, the middle-class population, especially in India, will expand from an estimated 53.3 million households, which is 267 million individuals, to roughly 113.8 million households, accounting for 547 million individuals. Besides, in terms of cooking meals, there has been a rising trend for the per capita yearly purchase of edible oils, catering to 0.44 kg and 4%, with a subsequent increase in oil consumption in urban India, thus fueling the segment growth.

Distribution Channel Segment Analysis

By the end of the forecast period, the offline sub-segment, part of the distribution channel segment, is projected to account for the second-highest share in the cookware market. The sub-segment’s growth is highly driven by consumers insistance on physical interaction with products before committing. Shoppers want to lift a pan to assess its weight, run fingers across the cooking surface to feel smoothness, tap the base to gauge thickness, and test handle ergonomics for comfort and balance. These tactile evaluations are impossible to replicate through digital interfaces. Department stores and specialty kitchenware retailers provide curated environments where trained staff answer questions about material properties, compatibility with specific cooktops, and long-term maintenance requirements. Hypermarkets serve value-seeking consumers who compare multiple brands side-by-side, evaluating price against perceived build quality.

Functionality Segment Analysis

The multifunctional sub-segment, part of the functionality segment, is expected to grab the third-highest share in the cookware market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by its importance in adding texture and taste by facilitating the retention and distribution of heat. As per an article published by Current Research in Food Science in 2024, functional-based temperature models are readily applicable for cooking food with a pH of 5.0 to 6.0 within a suitable temperature range between 50 degrees Celsius and 100 degrees Celsius. Besides, the pH models for cooking are significantly designed for food with a pH of 3.0 to 6.0 at boiling temperatures. Therefore, with such pH and suitable temperature considerations, there is a huge growth opportunity for the sub-segment, which is responsible for boosting the cookware market growth.

Our in-depth analysis of the cookware market includes the following segments:

|

Segment |

Subsegments |

|

|

|

Distribution Channel |

|

|

Functionality |

|

|

Price Range |

|

|

Product |

|

|

Material |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cookware Market - Regional Analysis

North America Market Insights

North America in the cookware market is anticipated to garner the largest share of 41.3% by the end of 2035. The market’s upliftment in the region is primarily attributed to the robust consumers’ inclination towards premium and advanced products, an increase in disposable income, the established existence of manufacturers, cooking trends and health-conscious lifestyles, as well as e-commerce expansion. According to official statistics published by NLM in August 2025, there has been an increase in cooking preference among men from 36% to 52%, and for women from 69% to 72%, particularly in the U.S. In addition, the mean time cooking interest among the male population surged from 45 minutes per day to 50 minutes per day, and for women, it was 71 minutes per day. Therefore, this increase in cooking duration is highly responsible for driving the cookware market growth in the region.

U.S. Adults Cooking Weighted Percent Analysis (2003-2023)

|

Year |

Men |

Women |

|

2003 |

36% |

69% |

|

2004 |

37% |

69% |

|

2005 |

38% |

68% |

|

2006 |

38% |

67% |

|

2007 |

395 |

66% |

|

2008 |

40% |

68% |

|

2009 |

41% |

71% |

|

2010 |

43% |

70% |

|

2011 |

42% |

68% |

|

2012 |

41% |

67% |

|

2013 |

43% |

70% |

|

2014 |

44% |

71% |

|

2015 |

44% |

72% |

|

2016 |

47% |

72% |

|

2017 |

47% |

71% |

|

2018 |

47% |

70% |

|

2019 |

49% |

72% |

|

2021 |

52% |

74% |

|

2022 |

52% |

73% |

|

2023 |

52% |

72% |

Source: NLM

The cookware market in the U.S. is growing significantly, owing to the resilience of the home cooking culture, the influence and expansion of e-commerce, an increase in the kitchen renovation effect, and a surge in the need for smart cookware. As stated in an article published by the NKBA Organization in September 2025, this particular organization is effectively worth USD 230 billion kitchen and bath sector, which represents almost 55,000 regional kitchen and bath professionals in the country. Based on this presence, 76% of the domestic population expect the kitchen footprint to enhance in the upcoming 3 years. This particular evolution has catered to homeowners' desire for cohesive and connected design between space for wellness, functionality, and entertainment, thereby making it extremely suitable for bolstering the market expansion in the country.

The strong growth of the e-commerce retail, the entry of direct-to-consumer (DTC) brands, an increase in the demand for durable and premium products, and the strong awareness of sustainability and health are factors that are driving the cookware market in Canada. Based on government estimates published by the ITA in July 2025, the e-commerce industry significantly accounts for 6.1% of the overall domestic retail sales in December 2024, along with online retail sales totaling an estimated USD 3.1 billion. Despite earlier projections that estimated the country’s e-commerce industry was worth USD 65.5 billion as of 2024, current estimates acknowledge that it has reached roughly USD 89.4 billion in gross merchandise value (GMV). Additionally, this particular industry is further expected to continue its upward trend, with revenues poised to reach USD 104 billion by the end of 2029, thus fueling the cookware market growth in the country.

APAC Market Insights

The Asia Pacific in the cookware market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by rapid urbanization, a rise in disposable incomes, the presence of a strong manufacturing ecosystem, a surge in the need for stainless steel, induction-based and ceramic-coated cookware, expansion in digitalized retail, and government-based platforms. According to official statistics published by the World Bank Organization in February 2026, the region’s low-income population resides in urban locations, accounting for a 47%, in comparison to 34%. Despite this, urban areas in the region are continuing to offer better prospects for upward mobility into the middle class, catering to 44% other than 22% for rural areas, thereby creating a huge growth opportunity for the market in the overall region.

The cookware market in China is gaining increased traction, owing to the existence of huge manufacturing capabilities, well-established supply chains, a large-scale domestic consumer base, an increase in consumers’ preference for urbanized and health-conscious lifestyles, organizational contributions, and suitable government approaches. As stated in an article published by the CEPR Organization in March 2026, there has been an increase in the country’s worldwide exports from 3.5% to 14.6% as of 2022, with export units ranging from 40% to 60% of other regions. Besides, there has been an increase in direct subsidies that eventually raises the probability of exporting by almost 0.9%, while a similar increase has raised the export valuation by approximately 10%, thus enhancing the overall supply chain system in the overall domestic market’s exposure.

The aspects of ongoing changing lifestyles, a rise in premiumization and disposable incomes, consumers’ health consciousness and transition to toxin-free cookware, an expansion in DTC and e-commerce channels, growth of Tier-2 and Tier-3 cities, an increase in the need for induction-compatible cookware, and the growing interest in home cooking are certain trends that are responsible for boosting the cookware market in India. As per an article published by the NCBI in January 2023, the domestic population is almost 17.7% of the overall population, readily surpassing China. In addition, there has been an estimated increase in population by 1.5 billion by the end of 2030, as well as 1.6 billion by the end of 2050, and meanwhile, 600 million population is projected to reside in urban areas and is poised to demand a continuous supply of healthy and safe food from hinterlands, thus enhancing the demand of premium cookware.

Europe Market Insights

Europe in the cookware market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by sustained home-cooking trends, an increase in the requirement for premium cookware products, a pronounced transition to induction-compatible and eco-friendly cookware, along with consumers' favoring durable stainless steel and innovative non-stick products. According to official statistics published by the ECOS Organization in June 2024, the installed stock of gas cookers is extremely high in the Netherlands, with more than 65% of households, or almost 5.4 million households. Despite this, the latest sales are ensuring modifications and further demonstrating the future of cooking in the region as electric. Besides, online retailers in Germany and Austria provide a 4-hob induction cooktop at USD 176.6, while Romania accounts for a retailer selling for USD 197.9, along with Italy accounting for USD 200.1, thus driving the market upliftment in the region.

The cookware market in Germany is gaining increased exposure, owing to robust manufacturing capabilities, high-quality standards, consumer preference for premium kitchen products, notable cookware manufacturers, a well-established industrial base, and the presence of modernized retail chains. Based on government estimates published by the USDA in September 2022, the country’s nominal GDP has successfully reached USD 4.2 trillion, which has effectively positioned the country as the 4th largest economy globally. Based on this growth, the imports of food products significantly reached USD 108.5 billion, demonstrating an increase by 7.7%. Meanwhile, 79% of these imports evolved from other regional member states. Therefore, with this remarkable growth in the economy and food products, there is a huge demand for the market in the overall country.

An increase in consumer preference for consuming health food preparations in high-quality and non-toxic cookware, the government’s strong industrial investment strategy, robust culinary culture, a rise in the demand for stainless steel and ceramic cookware, and the leadership in advocating regional industry policies are certain drivers for fueling the cookware market in France. As per an article published by OEC in April 2026, the domestic imports of ceramic products were worth USD 2.4 billion as of 2024, with exports of USD 724 million products to Italy. Likewise, the country also exported USD 827 million of such products, significantly making it the 13th largest exporter globally. In this regard, the country exports USD 78.5 million worth of products to Germany, which is followed by USD 76.3 million to the U.S., USD 71.4 million to Belgium, and USD 56.1 million to the UK, thus bolstering the market upliftment.

Key Cookware Market Players:

- Groupe SEB (France)

- Newell Brands (U.S.)

- Zwilling J.A. Henckels (Germany)

- WMF Group (Germany)

- Fissler GmbH (Germany)

- Meyer Corporation (U.S.)

- Tramontina S.A. (Brazil)

- TTK Prestige Ltd (India)

- Hawkins Cookers Ltd (India)

- Neoflam (South Korea)

- Lock & Lock (South Korea)

- Happycall (South Korea)

- Yoshikawa (Japan)

- Zojirushi Corporation (Japan)

- Tiger Corporation (Japan)

- The Vollrath Company, LLC (U.S.)

- Le Creuset (France)

- IKEA (Sweden)

- Carote (China)

- Williams Sonoma (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Groupe SEB maintains its leadership through a multi-brand portfolio that spans value-oriented to premium cookware, covering nearly every price tier globally. The company aggressively expands into emerging markets by adapting product designs to local cooking traditions while leveraging its non-stick coating expertise.

- Newell Brands capitalizes on its extensive housewares ecosystem, cross-promoting cookware with complementary kitchen storage and food preparation products. The company focuses on direct-to-consumer channels and continuous material innovation to differentiate its heritage brands in a crowded marketplace.

- Zwilling J.A. Henckels positions itself at the luxury end of the cookware market, emphasizing centuries-old craftsmanship and premium material selection to justify elevated pricing. The brand has successfully expanded beyond knives into complete cookware systems while maintaining its precision-engineering reputation through German and Japanese production facilities.

- WMF Group distinguishes itself through professional-grade cookware that bridges commercial kitchen durability with residential aesthetic preferences. The company leverages its hospitality industry relationships to create halo effects, where restaurants use signals of quality to home consumers seeking chef-approved equipment.

- Fissler GmbH focuses exclusively on ultra-premium cookware, refusing to compete in mid-range or value segments to preserve brand exclusivity. The company invests heavily in proprietary manufacturing techniques, including unique handle attachment systems and precision-machined cooking surfaces that cannot be easily replicated by mass-market competitors.

Here is a list of key players operating in the global cookware market:

The global cookware market remains highly fragmented, with the top three manufacturers accounting for an estimated share of the total market. In this regard, Groupe SEB of France leads the industry through strategic acquisitions, including Tefal, Moulinex, and Krups, while aggressively expanding non-stick technology and eco-design initiatives. Simultaneously, Newell Brands leverages its extensive brand portfolio, including Calphalon, Rubbermaid, and Pyrex, focusing on e-commerce and material science innovation. Besides, in January 2025, Tefal and Paul Bocuse launched an outstanding and iconic latest collection that embodies suitable challenges and creates premium kitchenware collections that are easily accessible to many consumers. Therefore, with such product launches, there is a huge growth opportunity for the cookware industry globally.

Corporate Landscape of the Cookware Market:

Recent Developments

- In February 2026, Rhenus and Zwilling significantly expanded the tactical partnership to include the Wesel site in Europe, with the intention to provide multi-year planning and operational outlook and is effectively accompanies by generous investment in modernized logistics processes.

- In November 2025, Auguste Escoffier School of Culinary Arts partnered with ZWILLING for equipping students with professional grade toolkits and offer opportunities to support futuristic culinary students through the ZWILLING Culinary Edge Scholarship.

- Report ID: 8517

- Published Date: Apr 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.