Ceramic Tiles Market Outlook:

Ceramic Tiles Market size was valued at USD 226.9 billion in 2025 and is projected to reach USD 420.6 billion by the end of 2035, rising at a CAGR of 7.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of ceramic tiles is assessed at USD 243 billion.

The international market is undergoing significant transformations owing to the rise of construction and infrastructure activities across the globe, supported by sustained residential and non-residential building programs in major economies. The continued trade activity denotes that there is a heightened demand for these tiles across different nations. According to the official statistics published by Cerambath Organization in June 2025, China’s total ceramic tile trade reached USD 276 million in March 2025, which marks a year-on-year increase of 12.52%, with exports at USD 261 million, up by 9.97%, and imports at USD 14.36 million, rising by 94.28%. The export volume for the month totaled 42.98 million square meters, which is up 42.44%, with an average price of USD 0.34/kg or USD 6.08/square meter, hence increasing the market’s growth potential.

China Ceramic Tile Exports March 2025: Top 10 Countries, Trade Value, and Year-on-Year Growth Analysis

|

Country/Region |

March 2025 Export Value (USD) |

% of Total |

March 2024 Export Value (USD) |

Year-on-Year Change (%) |

|

Philippines |

29,624,775 |

11.34% |

16,689,672 |

77.50% |

|

Thailand |

22,000,354 |

8.42% |

12,985,173 |

69.43% |

|

South Korea |

16,931,244 |

6.48% |

14,020,882 |

20.76% |

|

Vietnam |

16,536,272 |

6.33% |

15,408,376 |

7.32% |

|

Malaysia |

15,117,575 |

5.79% |

13,379,372 |

12.99% |

|

Australia |

14,815,614 |

5.67% |

15,505,008 |

-4.45% |

|

Singapore |

11,408,916 |

4.37% |

6,492,891 |

75.71% |

|

Cambodia |

10,740,230 |

4.11% |

6,907,872 |

55.48% |

|

Hong Kong (China) |

9,600,633 |

3.67% |

37,353,391 |

-74.30% |

|

Israel |

9,479,082 |

3.63% |

1,225,597 |

673.43% |

Source: Cerambath.org

Furthermore, the market is pivoting toward premium products, wherein the manufacturers are increasing their production capabilities to meet the heightened demand. According to the IBEF reports published in January 2026, India’s ceramic tile sector has evolved into a global manufacturing powerhouse, wherein Morbi, Gujarat, produces up to 90% of the country’s tiles across more than 1,800 facilities. The sector reached a market value of Rs. 62,000 crore (USD 6.99 billion) in FY2024, effectively fueled by domestic consumption of 2,000 million sq. m and exports of 590 million sq. m. India ranks as the second-largest producer, consumer, and exporter globally, with strong growth in premium products, digital sales platforms, and eco-friendly manufacturing. In addition, the aspects of urbanization, rising incomes, and export diversification into Asia, Africa, and Latin America continue to bolster sustained expansion.

India Ceramic Tile Industry FY24: Market Size, Production, Consumption, and Export Statistics

|

Metric |

Value |

Value (USD) |

|

Domestic Consumption |

2,000 million sq. m |

USD 4.73 billion |

|

Export Volume |

590 million sq. m |

USD 2.25 billion |

|

Sanitaryware Market Size |

Rs. 8,000 crores |

USD 901.8 million |

|

Per Capita Tile Consumption |

0.50 sq. m/person |

- |

|

Global Production Share |

15.4% (2023) |

- |

|

Export Growth in Africa |

68.8% volume increase |

- |

|

Export Growth in the EU |

60 million sq. m (+75%) |

- |

Source: IBEF

Key Ceramic Tiles Market Insights Summary:

Regional Highlights:

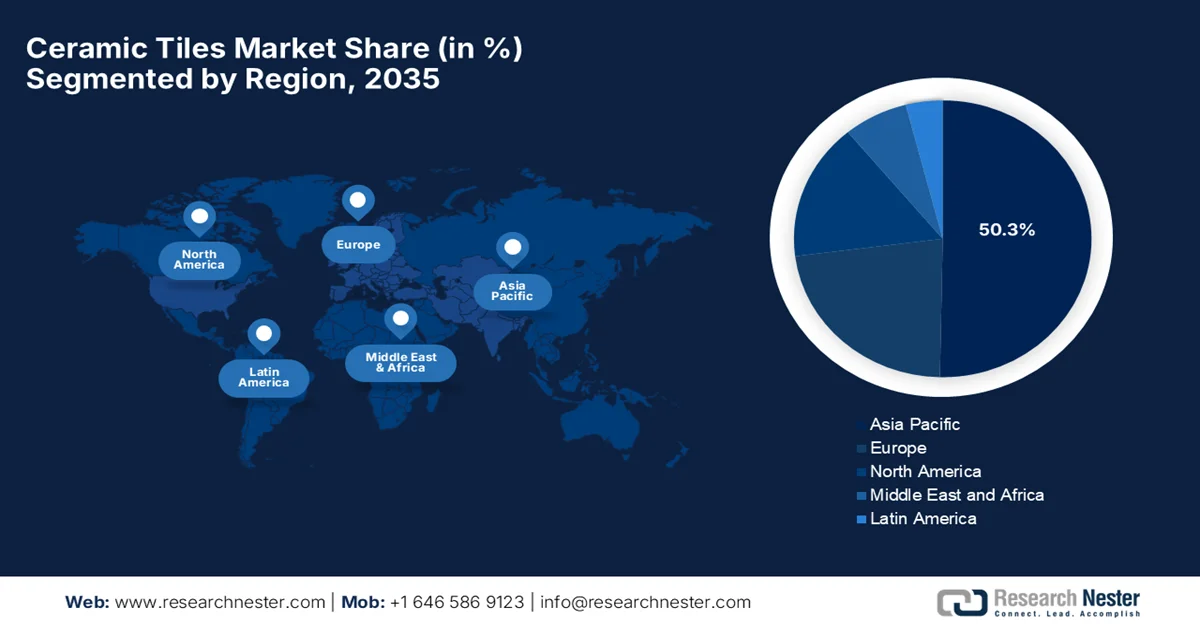

- Asia Pacific ceramic tiles market is projected to capture a 50.3% revenue share by 2035, driven by rising middle-class population, accelerating urbanization, sustainability initiatives, and expanding construction activities.

- Europe is anticipated to witness steady expansion through 2026–2035, impelled by heightened demand for premium designs and sustainable building materials supported by decarbonization initiatives.

Segment Insights:

- Floor type segment in the ceramic tiles market is expected to account for a 61.6% revenue share by 2035, driven by its durability, low maintenance, and design flexibility across residential and commercial flooring applications.

- Porcelain tiles segment is poised to register considerable growth by 2035, propelled by superior water resistance, low porosity, and high strength suited for heavy-traffic environments.

Key Growth Trends:

- Rapid construction growth

- Rising consumer preference for aesthetics

Major Challenges:

- High raw material costs

- Fluctuating demand in the construction sector

Key Players: Mohawk Industries Inc. (U.S.), Grupo Lamosa S.A.B. de C.V. (México), Marco Polo Group (China), SCG Ceramics Public Co. Ltd. (Thailand), RAK Ceramics P.J.S.C (UAE), Pamesa Grupo Empresarial S.A. (Spain), Guangdong Newpearl Ceramics Co., Ltd. (China), Johnson Tiles / H&R Johnson (India), Porcelanosa Grupo A.I.E. (Spain), Florida Tile (U.S.), Villeroy & Boch AG (Germany), Crossville Inc. (U.S.), Iris Ceramica Group (Italy), Noritake Co., Ltd. (Japan), Somany Ceramics Ltd. (India), Kajaria Ceramics Ltd. (India), Cersanit Group (Poland), Lasselsberger Group AG (Austria), Kale Group (Turkey)

Global Ceramic Tiles Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 226.9 Billion

- 2026 Market Size: USD 243 Billion

- Projected Market Size: USD 420.6 Billion by 2035

- Growth Forecasts: 7.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (50.3% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: China, India, United States, Italy, Spain

- Emerging Countries: Vietnam, Indonesia, Brazil, Mexico, Saudi Arabia

Last updated on : 23 February, 2026

Ceramic Tiles Market - Growth Drivers and Challenges

Growth Drivers

- Rapid construction growth: The expansion of residential, commercial, and public infrastructure projects is a primary driver for the ceramic tiles market. As cities grow and new housing developments rise, demand for ceramic tiles for flooring, walls, cladding, and interior design increases at a significant rate. In this context, NAHB revealed that in 2024, U.S. housing starts totaled 1.36 million units, whereas the single-family starts rose 6.5% to 1.01 million amid strong demand despite high mortgage rates and limited buildable lots. It also stated that December alone saw total starts jump 15.8% to 1.50 million units, with single-family up 3.3% and multifamily surging 61.5%, marking the highest pace since February 2024, hence denoting a positive outlook for the market’s exposure and expansion in the upcoming years.

- Rising consumer preference for aesthetics: There has been an emerging trend of architectural and interior designs that necessitate customized tile formats, providing encouraging business opportunities for pioneers in the market. According to the article published by Frontiers in July 2025, it examined how media-inspired home décor influences consumer behavior, showing that individuals mostly use on-screen aesthetics to personalize their living spaces. In addition, through interviews with expatriates in the UAE, the research found that consumers adopt décor reflecting TV and film styles as a form of self-expression, identity construction, and emotional engagement. Therefore, this particular trend highlights the growing preference for customized and aesthetically driven home interiors, supporting demand for products such as ceramic tiles.

- Rising disposable incomes: The rising incomes and expanded consumer spending on home improvements and lifestyle upgrades readily increase the demand for ceramic tiles, particularly in emerging markets. As stated by the Ministry of Statistics & Program Implementation (MoSPI), India’s economy remained highly resilient in FY 2023‑24, wherein the country’s real GDP displayed a rise by 7.6%, supported by strong performance in the construction sector, 10.7%. It also stated that the 3rd quarter 2023‑24 GDP grew 8.4% at constant prices, which reflects constant sectoral contributions, including construction and industrial production. Therefore, these trends indicate higher economic activity and consumer spending potential, creating favorable conditions for demand in housing, interior design, and customized home décor products, such as in the ceramic tiles market.

Challenges

- High raw material costs: The market is mainly dependent on raw materials such as clay, feldspar, silica, and kaolin. Therefore, any fluctuations in its prices due to mining restrictions, cross-border issues, and transportation costs can impact production expenses. In the case of smaller manufacturers, these cost pressures can reduce profit margins or force price increases, thereby causing reductions in demand in price-sensitive markets. In addition, sourcing quality raw materials is also challenging, particularly for companies that are operating in regions with limited local deposits. In this context, manufacturers need to balance cost, quality, and availability, which can constrain production planning and investment in advanced tile designs. Furthermore, the surging raw material costs also hinder the ability to offer affordable premium aesthetic tiles.

- Fluctuating demand in the construction sector: The ceramic tiles market is closely associated with residential, commercial, and infrastructure construction. Economic slowdowns, rising interest rates, or any type of delays in terms of government infrastructure projects can result in reduced tile demand. On the other hand, seasonal variations, changing real estate trends, or geopolitical events that affect investment in construction also impact consumption. Since tiles are durable, high-involvement purchases, demand is often deferred during uncertain periods, affecting manufacturers’ revenue as well as their inventory management. In addition, the rising construction material costs can prompt builders and homeowners to choose alternative flooring solutions, such as vinyl, laminate, or cement-based tiles.

Ceramic Tiles Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.1% |

|

Base Year Market Size (2025) |

USD 226.9 billion |

|

Forecast Year Market Size (2035) |

USD 420.6 billion |

|

Regional Scope |

|

Ceramic Tiles Market Segmentation:

Application Segment Analysis

The floor type is expected to emerge with the largest revenue share of 61.6% in the market during the forecast period. They are the most widely used surface material in residential and commercial flooring, prompted by their durability, low maintenance, and design flexibility. For instance, in February 2025, Topps Tiles announced that it had launched Alusid’s mas floor tile range, which is the company’s first product specifically designed for flooring, made from 95% to 98.5% recycled industrial waste. The company also stated that mas reduces carbon emissions by 51% and water use by 44% when compared to standard tiles, combining sustainability with stylish design. Hence, such developments from pioneers across the globe will position the subtype at the forefront of revenue generation in this field.

Product Segment Analysis

The porcelain tiles, which are a part of the product segment is anticipated to grow at a considerable rate in the ceramic tiles market by 2035. The growth of the subtype is mainly propelled by its superior water resistance, low porosity, and strength versus standard ceramic tiles. Their high performance in heavy‑traffic zones such as kitchens, lobbies, and commercial spaces bolsters long-term revenue share. In this context, VitrA Tiles in October 2025 reported that it has launched its 100% recycled porcelain tile at Cersaie 2025, which is sourced entirely from production waste without compromising on any technical performance or aesthetics. Besides, this innovation deliberately promotes a circular economy by reducing reliance on virgin raw materials, lowering carbon footprint, and improving energy efficiency through shorter production times, hence denoting a positive market outlook.

End use Segment Analysis

Residential subtype is predicted to be the largest end use segment with a significant revenue stake in the market. The growth is mainly based on factors such as global urbanization and population growth, which are expanding housing units, renovation spending, and interior customization. In addition, the increasing disposable incomes and changing lifestyle preferences are encouraging homeowners to make investments in home renovations and interior customization, which includes premium flooring, wall finishes, and decorative tiles. Besides the government housing initiatives and real estate expansions in emerging economies, market growth is also supported over the forecasted years. Therefore, the combination of functional performance and design appeal positions residential applications as the largest end-use segment in the ceramic tiles industry.

Our in-depth analysis of the ceramic tiles market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Product |

|

|

End use |

|

|

Project Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Ceramic Tiles Market - Regional Analysis

APAC Market Insights

The Asia Pacific ceramic tiles market is predicted to be the dominant landscape with the largest revenue share of 50.3% by 2035. The region’s leadership is driven by the rising middle-class population, sustainability initiatives, and increasing construction activities. Urbanization has been rising in countries, fueling the growth of residential, commercial, and industrial projects, thereby heightening the demand for ceramic tiles. In this context, ITA in August 2024 disclosed that Japan looks for carbon neutrality by 2050, necessitating all new residential and commercial buildings to be zero-energy houses or zero-energy buildings to meet net-zero energy consumption standards through renewable energy, high-efficiency insulation, and energy-saving technologies. Therefore, construction companies need to use low-CO2 products and processes, with some contractors setting even stricter internal CO2 reduction targets, such as creating CO2-absorbing concrete or reusing steel and concrete materials. Hence, this boosts demand for sustainable ceramic tiles used in ZEH and ZEB constructions.

The infrastructure field and export capacity are the topmost contributors to growth in the China market. The country is one of the largest landscapes that is witnessing extensive investments in urban and rural infrastructure are driving strong demand for ceramic tiles in both residential and commercial projects. In addition, the government initiatives are proactively promoting urbanization and economic development, which are significant contributors. Based on the government data, which was published in January 2024, the country is actively promoting the use of eco-friendly building materials, aiming for the sector’s annual revenue to exceed 300 billion yuan (approximately 42.2 billion) by 2026, and more than 10% annual growth is expected between 2024 and 2026. This plan is mainly focused on improving production techniques, adopting green energy, reducing consumption, and encouraging recycling to cut pollution and carbon emissions, hence driving demand for sustainable construction materials.

Top 10 China Provinces Leading Ceramic Tile Exports in March 2025 - Detailed Export Value & Growth Analysis

|

Province |

March 2025 Export (USD) |

Proportion of Total (%) |

March 2024 Export (USD) |

Year-on-Year Change (%) |

|

Guangdong |

100,154,423 |

38.33 |

86,513,458 |

15.77 |

|

Fujian |

46,165,660 |

17.67 |

41,921,387 |

10.12 |

|

Zhejiang |

19,110,513 |

7.31 |

31,948,749 |

-40.18 |

|

Xinjiang Uygur Autonomous Region |

18,795,774 |

7.19 |

4,981,618 |

277.30 |

|

Hubei |

16,431,560 |

6.29 |

11,249,478 |

46.07 |

|

Shandong |

15,257,012 |

5.84 |

17,266,135 |

-11.64 |

|

Guangxi Zhuang Autonomous Region |

12,340,805 |

4.72 |

12,249,585 |

0.74 |

|

Jiangsu |

7,131,510 |

2.73 |

5,857,158 |

21.76 |

|

Heilongjiang |

5,117,438 |

1.96 |

1,321,052 |

287.38 |

|

Sichuan |

4,169,050 |

1.60 |

12,222,224 |

-65.89 |

Source: Cerambath.org

The burgeoning rates of government-backed infrastructure initiatives are the main factors fueling the ceramic tiles market in India. The country’s market is shifting from a fragmented, utility-based sector into a technologically improved international powerhouse. This shift is mainly influenced by factors such as urbanization and initiatives, i.e., Smart Cities Mission and Pradhan Mantri Awas Yojana, which have created a strong demand for residential and commercial flooring solutions. In the financial year 2025-26, as reported by the government of India, under PMAY‑Urban 2.0, it has allocated strong central assistance to various states for housing projects. The primary releases were USD 51.4 million to Uttar Pradesh for 71,127 houses, USD 8.16 million to Chhattisgarh for 141 BLC projects, and significant amounts to other states for multiple BLC projects, reflecting active implementation of affordable housing initiatives and their mounting support across urban infrastructure development, boosting demand in the ceramic tiles industry.

Europe Market Insights

The heightened demand for premium products and exclusive designs is fueling the growth of the market in Europe. The region represents higher construction standards with an increased importance for sustainable building materials. In December 2025, the European Commission-funded INNOVATILE project under the Interreg NEXT MED Programme launched a new sustainable technology to reduce the environmental impact of ceramic tile manufacturing, with potential production cost savings of around 10%. For this project, the total regional contribution was €2.49 million (approximately USD 2.70 million), representing 89% of the €2.8 million (approximately USD 3.05 million) total budget. In addition, the initiative aims to achieve a 25% to 30% reduction in energy demand and greenhouse gas emissions and a 10% to 20% decrease in water and raw material consumption by efficiently promoting the use of secondary raw materials to support decarbonization in Europe’s ceramic tile sector.

Germany ceramic tiles market has gained enhanced traction, especially in terms of residential and commercial sectors of construction. Consumers in the country are looking for eco-friendly, energy-efficient, and design-driven products, contributing to wider adoption in premium residential projects and upscale commercial spaces. In 2023, AGROB BUCHTAL GmbH reported that it had supplied its KeraTwin ceramic façade system for the Ilot Queyries residential complex in Bordeaux by providing architects with energy-efficient ceramic solutions for new buildings and renovations. The system allows horizontal, vertical, and diagonal installation, offering aesthetic flexibility while promoting resource conservation and sustainability. From a strategic perspective, such instances in the country will bolster the market by encouraging innovation among manufacturers and reinforcing Germany’s leadership in eco-conscious construction practices.

The structural shift towards high-performing materials is the main factor boosting growth in the France ceramic tiles market. The industry is also driven by a renovation and replacement culture, bolstered by government-backed energy retrofit subsidies and a post-pandemic rise in home-improvement projects. From May 2024, the country’s government has updated MaPrimeRénov to simplify energy renovation for homeowners by allowing single-gesture projects, such as wall or roof insulation, without requiring an energy performance diagnostic. Besides, this scheme offers two tracks, one is a path by gesture for individual upgrades and an accompanied route for major renovations. It also stated that the aid levels depend on household income, wherein very low-income households will be eligible for up to €70,000 (USD 76,000) for renovations, by supporting wider adoption of high-performance building materials in France.

North America Market Insights

The North America ceramic tiles market has acquired a prominent position in the global dynamics, mainly influenced by builders, designers, and homeowners who value materials that combine style, durability, and environmental friendliness. Trends show that there has been a move toward digitally printed and large-format tiles that offer customized aesthetics and modern design flexibility, especially in urban housing and upscale commercial spaces. In June 2025, AHF Products announced that it had launched the Crossville Sand Garden porcelain tile collection, which was showcased at NeoCon 2025, consisting of large-format tiles with hyper-realistic textures inspired by natural dry gardens. It uses Visual Touch technology, and the collection combines tactile authenticity with the latest designs, making it suitable for standard market growth.

The advanced manufacturing innovations and architectural trends that are focused on exclusive interiors are certain drivers responsible for uplifting the market in the U.S. Technologies such as digital inkjet printing and anti-slip surface coatings are gaining momentum, and along with construction growth, this design-centric demand is also driving the country’s market. According to the data kept forward by the U.S. Census Bureau in January 2026, total U.S. construction spending in October 2025 reached a seasonally adjusted annual rate of USD 2,175.2 billion, which marks a up 0.5% from September. It also stated that the private construction showcased a rise 0.6% to USD 1,651.3 billion, wherein the residential spending increasing 1.3% to USD 913.9 billion. Furthermore, the public construction was at USD 524.0 billion, supported by educational and highway construction, reflecting continued building activity across these sectors.

The ceramic tiles market in Canada witnesses significant imports due to the absence of sufficient domestic production. The market is witnessing growth largely fueled by a growing urban population and robust activity in both new residential construction and the renovation of existing homes, as well as commercial spaces. Based on the government data in 2023, the country, particularly for finishing ceramics, was mostly dependent on Portugal. Besides, it included APEX Granite & Tile Inc. (Surrey, BC), HY‑East Holding Corporation (Calgary, AB), Olympia Tile International Inc. (Toronto, ON), and TM Tilemart Ltd. (Surrey, BC), collectively accounting for nearly 80% of imports, which were valued at CAD 371,000. Therefore, this illustrates the market’s import-driven structure, serving demand across residential and commercial construction and renovation projects.

Key Ceramic Tiles Market Players:

- Mohawk Industries Inc. (U.S.)

- Grupo Lamosa S.A.B. de C.V. (México)

- Marco Polo Group (China)

- SCG Ceramics Public Co. Ltd. (Thailand)

- RAK Ceramics P.J.S.C (UAE)

- Pamesa Grupo Empresarial S.A. (Spain)

- Guangdong Newpearl Ceramics Co., Ltd. (China)

- Johnson Tiles / H&R Johnson (India)

- Porcelanosa Grupo A.I.E. (Spain)

- Florida Tile (U.S.)

- Villeroy & Boch AG (Germany)

- Crossville Inc. (U.S.)

- Iris Ceramica Group (Italy)

- Noritake Co., Ltd. (Japan)

- Somany Ceramics Ltd. (India)

- Kajaria Ceramics Ltd. (India)

- Cersanit Group (Poland)

- Lasselsberger Group AG (Austria)

- Kale Group (Turkey)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Mohawk Industries Inc. is one of the world’s largest flooring manufacturers, which is best known for its broad portfolio of products spanning luxury and affordable tiles. The company benefits from advanced manufacturing technologies and extensive global distribution networks, which position it as a crucial player in the ceramic tiles industry.

- Grupo Lamosa S.A.B. de C.V. is a specialist player in ceramic and porcelain tiles that has a strong focus on quality, durability, and design innovation. Besides, the company makes extensive investments in capacity expansion and technological upgrades to solidify its competitive edge in this sector.

- SCG Ceramics Public Co. Ltd. is based in Thailand, and the firm has very strong manufacturing capabilities and innovative product lines. The company is mainly focused on large-format tiles, digital printing technology, and sustainability practices, aligning with global trends.

- Pamesa Grupo Empresarial S.A. is identified as one of Europe’s premier ceramic tile manufacturers, which is best known for high-quality, design-oriented products that blend traditional craftsmanship with technology. The company makes increased investments in R&D, focusing mainly on eco-friendly production methods and digital printing.

- Johnson Tiles, which is a subsidiary of H&R Johnson, is yet another leading player in this market, which is offering a variety of products suitable for various consumer segments. The company combines domestic manufacturing expertise with international quality standards, maintaining a strong domestic presence.

Below is the list of some prominent players operating in the global market:

The global ceramic tiles market is concentrated among a mix of flooring conglomerates as well as specialized tile manufacturers. Mohawk Industries leads the market with extensive global production and a strong brand portfolio, whereas Grupo Lamosa and SCG Ceramics leverage regional strengths in North America and the Asia Pacific. Meanwhile, the Europe-specific players such as Pamesa and Iris Ceramica Group emphasize premium design and export growth. Capacity expansion, brand acquisitions, and product innovation are the major tactical strategies opted for by the pioneers in this field. In June 2023, H & R Johnson, which is a division of Prism Johnson Limited, reported that it held a grand product launch in Kolkata, introducing more than 3,000 new tile designs. The company also reported that there is an upcoming opening of a manufacturing plant in Panagarh, West Bengal, thereby solidifying its position as a leading pioneer, hence denoting a positive market outlook.

Corporate Landscape of the Ceramic Tiles Market:

Recent Developments

- In 2025, Eczacıbaşı Tiles Group stated that its VitrA’s CementEra series and Villeroy & Boch’s MetalCraft series achieved the red dot design award in the product design category. CementEra has concrete-inspired textures, whereas MetalCraft leverages advanced porcelain technology for wall and floor applications.

- In September 2024, Niro Ceramic Group introduced its new showroom in Shah Alam, along with the launch of its latest tile collections by highlighting innovation, sustainability, and modern large-format slab trends.

- Report ID: 4504

- Published Date: Feb 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.