Cardiovascular Digital Solutions Market Outlook:

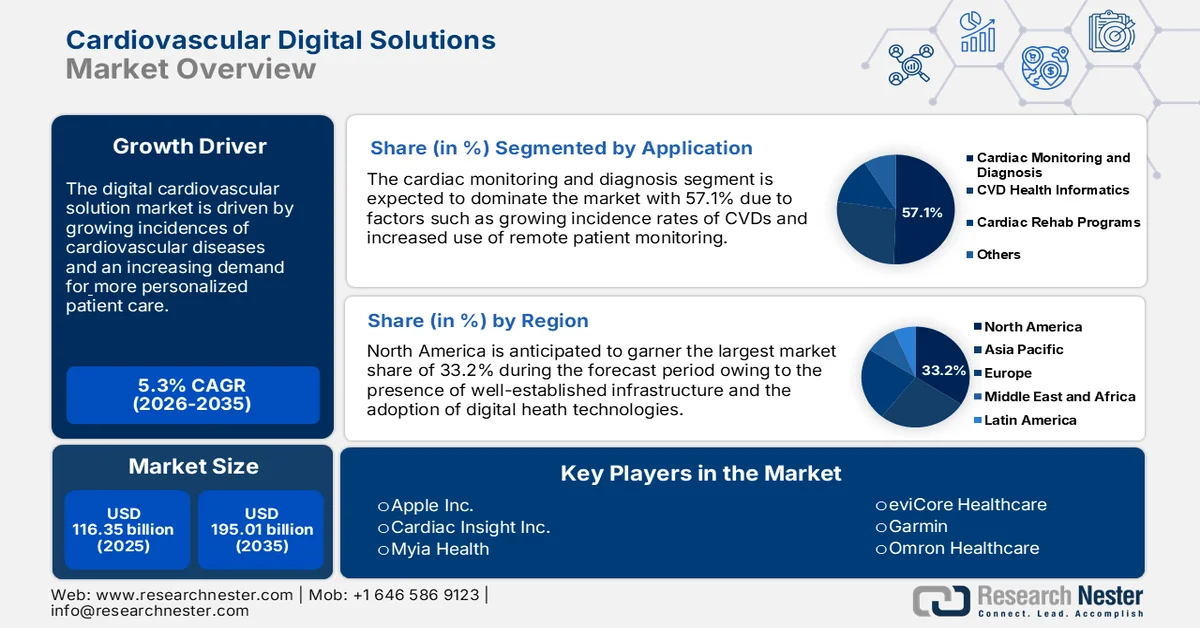

Cardiovascular Digital Solutions Market size was over USD 116.35 billion in 2025 and is poised to exceed USD 195.01 billion by 2035, witnessing over 5.3% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of cardiovascular digital solutions is estimated at USD 121.9 billion.

The market is driven by growing morbidity due to cardiovascular diseases (CVDs), advancements in telehealth, and an increasing demand for more personalized patient care. According to the World Health Organization (WHO) statistics, CVDs are a leading cause of death and accounted for 32% of global deaths in 2019. This compelling statistic sparks unique approaches to diagnosis, monitoring, and managing cardiovascular health. The increased usage of telemedicine, technological advancement of wearable devices, AI-driven analytics, and integration of digital health records are the growth drivers that enhance healthcare accessibility and improve clinical outcomes.

As the stakeholders increasingly discover the reliability of these solutions, cardiovascular digital solutions market growth witnesses robust support for that transformational shift in cardiovascular care delivery. The adoption of telehealth solutions has drastically increased, with a focus on advanced remote patient monitoring (RPM) systems. For instance, in February 2021, Remo Care Solutions announced the launch of Remo.Cardo, a remote cardiac monitoring device equipped with AI that monitors and accesses heart health in real time.

Key Cardiovascular Digital Solutions Market Insights Summary:

Regional Highlights:

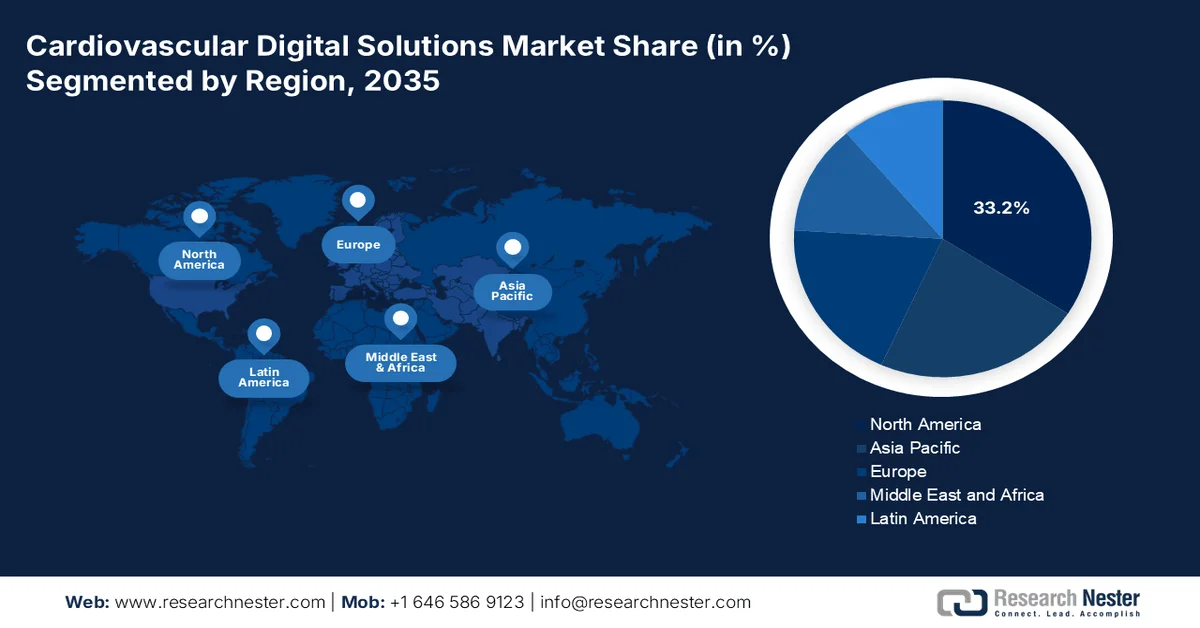

- North America is projected to secure a 33.2% revenue share of the cardiovascular digital solutions market by 2035, impelled by the rising prevalence of cardiac diseases, well-developed healthcare infrastructure, and increasing product launches and approvals for cardiovascular health

- Asia Pacific is anticipated to expand at a robust CAGR through 2026–2035, attributed to the rising prevalence of cardiovascular diseases, hypertension, and diabetes, unhealthy lifestyle adoption, and rapid integration of advanced digital solutions including AI, ML, and telemedicine

Segment Insights:

- Devices segment is projected to account for around 58.7% share of the cardiovascular digital solutions market by 2035, propelled by the increasing uptake of wearable technology, remote monitoring technologies, and the need for continuous, real-time health data

- Cardiac monitoring and diagnosis segment is set to capture over 57.1% share by 2035, driven by growing incidence rates of CVDs, increased use of remote patient monitoring, and constant improvements in wearable technology

Key Growth Trends:

- Rising prevalence of cardiovascular diseases

- Government initiatives and collaborations

Major Challenges:

- Cost and reimbursement issues

- Data security and cybersecurity risks

Key Players: Valve, Ubisoft, Nvidia, Activision Blizzard, Apple, TakeTwo Interactive, LG Electronics, Microsoft, Intel, Samsung, Amazon, Tencent, Meta, Electronic Arts, Sony.

Global Cardiovascular Digital Solutions Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 116.35 billion

- 2026 Market Size: USD 121.9 billion

- Projected Market Size: USD 195.01 billion by 2035

- Growth Forecasts: 5.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (33.2% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, Switzerland, United Kingdom

- Emerging Countries: China, India, Brazil, Mexico, South Korea

Last updated on : 25 February, 2026

Cardiovascular Digital Solutions Market - Growth Drivers and Challenges

Growth Drivers

- Rising prevalence of cardiovascular diseases: Cardiovascular disease tops the medical priorities list as several causes have been identified and related to driving the increasing incidence of CVD. Moreover, increasing population age also greatly contributes to the growing number of cardiovascular cases. This has resulted in rising product launches and technological advancements. For instance, in May 2022, AliveCor announced the launch of KardiaComplete, a complete heart health enterprise solution to enhance health outcomes and reduce overall costs of cardiac care and in September 2022, Wipro GE Healthcare announced the launch of its first “Made in India AI-powered cardiovascular lab- Optima IGS 320 to advance cardiac care in India.

- Government initiatives and collaborations: Government efforts and partnerships to prevent, diagnose, and treat several cardiovascular diseases is a key factor boosting cardiovascular digital solutions market growth. The alliances between the public sector, academic institutions, and private companies are also driving innovations as the health-based institutions are partnering with major companies such as Apple, Google, and Fitbit to make mobile and wearables integrated for self-continual monitoring of heart health with improved AI-based system platforms that process real-time data and identify anomalies to predict cardiovascular events. The cardiovascular digital health landscape will be viewed as further developments in real-time data sharing, interoperability across different devices and systems, and regulatory frameworks that support faster adoption. This will fuel innovation and a step towards greater access to advanced cardiovascular care.

Challenges

- Cost and reimbursement issues: Such digital solutions are associated with large investments in terms of infrastructure, technology, regulatory compliance, as well as clinical validation. In several countries, healthcare systems and insurers have not yet evolved with favorable reimbursement pathways for digital health tools, which hampers companies' recovery of their investments. In exchange, these solutions face a challenge in their adoption by healthcare providers and patients since most of these services are not reimbursed. This limits their adoption and slows cardiovascular digital solutions market growth.

- Data security and cybersecurity risks: Data security and cybersecurity threats are the biggest issues in the market as the patient information and data collected through these tools is very sensitive. Stricter regulatory standards such as HIPAA and GDPR compliance impose strict security but are insufficient to fight back against these advanced cyber threats. Such a breach would compromise patient privacy and, with it, undermine trust in digital solutions. This can hamper the overall cardiovascular digital solutions market growth to some extent during the forecast period.

Cardiovascular Digital Solutions Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.3% |

|

Base Year Market Size (2025) |

USD 116.35 billion |

|

Forecast Year Market Size (2035) |

USD 195.01 billion |

|

Regional Scope |

|

Cardiovascular Digital Solutions Market Segmentation:

Component (Devices, Software)

Devices segment is likely to account for around 58.7% cardiovascular digital solutions market share by 2035, owing to the increasing uptake of wearable technology, remote monitoring technologies, and the need for continuous, real-time health data. Continued advancements in technology and increased health consciousness are contributing to this growth. In August 2024, GE Healthcare announced the CE mark of its Vscan Air SL wireless handheld ultrasound solution for rapid cardiac assessment.

Application (Cardiac monitoring and diagnosis, CVD health informatics, Cardiac rehab programs)

By 2035, cardiac monitoring and diagnosis segment is set to capture over 57.1% cardiovascular digital solutions market share, owing to growing incidence rates of CVDs, increased use of remote patient monitoring, and constant improvements in wearable technology. The growth of this segment is brought about by new developments in wearable devices such as smartwatches and patch monitors, which enable the tracking of heart rates, ECG, and blood pressure. In March 2024, Wellysis partnered with Arthella Solutions to launch innovative remote monitoring services for cardiac health in the U.S.

Our in-depth analysis of the cardiovascular digital solutions market includes the following segments:

|

Component |

|

|

Application |

|

|

Deployment Mode |

|

|

End use |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cardiovascular Digital Solutions Market - Regional Analysis

North America Market Statistics

North America industry is likely to account for largest revenue share of 33.2% by 2035, owing to the rising prevalence of cardiac diseases, the presence of well-developed healthcare infrastructure, and increasing product launches and approvals for cardiovascular health.

The U.S. market is expected to expand at a robust rate during the forecast period. According to statistics released by the Centers for Disease Control and Prevention, CVD accounted for 37% of all deaths in the U.S. in 2021. With an emphasis on preventive care and shifting healthcare approaches towards a more preventive course, the need for sophisticated digital technologies has increased to monitor and track patients, advance early diagnosis, and reinforce the efficiency of treatments in the U.S.

In Canada, the cardiovascular digital solutions market is poised to register rapid growth between 2026 and 2035 owing to the rising incidence of heart diseases and increasing adoption of advanced digital healthcare. Companies are also focusing on developing advanced products and digital solutions for cardiac care. For instance, CIFAR launched two AI health solutions to cater to rising health problems in Canada, including cardiovascular diseases.

Asia Pacific Market Analysis

Asia Pacific cardiovascular digital solutions market is expected to expand at a robust CAGR during the forecast period owing to rising prevalence of cardiovascular diseases, hypertension, and diabetes, the high adoption of unhealthy lifestyles, and the rapid adoption of advanced cardiovascular digital solutions across several healthcare sectors. Moreover, the integration of AI, ML, and telemedicine in cardiovascular care solutions is expected to further accelerate market growth in the Asia Pacific.

In India, the cardiovascular digital solutions market is expected to register a rapid revenue CAGR between 2026 and 2035. This growth can be attributed to the high prevalence of heart diseases, rapid adoption of advanced healthcare technologies, and rising awareness about the importance of early detection and diagnosis. Companies are also investing in R&D investments to launch novel and effective cardiovascular digital solutions. In January 2023, Lupin Digital Health announced the launch of LYFE, a digital therapeutic solution for heart care. This solution is currently available in 10 cities, designed to reduce the risk of heart disease and enhance the quality of life of patients.

The cardiovascular digital solutions market in China is anticipated to expand at a rapid growth during the forecast period owing to the presence of robust healthcare infrastructure, rising prevalence of various cardiovascular diseases, and rising investments in R&D activities. For instance, in April 2020, Novartis launched a novel AI-enabled disease management tool in China to improve the rate of heart failure in the country.

Cardiovascular Digital Solutions Market Players:

- AliveCor, Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Baxter

- Cardiac Insight, Inc.

- Cardiotrack

- eviCore healthcare

- Garmin

- GE Healthcare

- HeartFlow

- iRhythm Technologies, Inc.

- Myia Health

- Omron Healthcare

- Qardio

- Verily Life Sciences LLC,

- Welch Allyn

Diverse companies, from the leading giants in the healthcare sector to the startup entities, are taking a leading role in this competition to advance the most innovative solutions that benefit patients with better outcomes in healthcare delivery. The major players in the region of these settings are focusing on implementing artificial intelligence, wearable devices, and data analytics for an effective resolution of chronic cardiovascular conditions. With these innovations, regulatory frameworks are constantly in motion, and landscapes transform themselves into something dynamic in a manner that opens vast growth opportunities for businesses fully committed to changing cardiovascular care with digital technology. Here is a list of key players operating in the global market:

Recent Developments

- In June 2024, Royal Philips announced the launch of its next-generation AI-enabled cardiovascular ultrasound solution to enhance cardiovascular ultrasound analysis and reduce the overall burden on echocardiography labs.

- In March 2024, the U.S. Food and Drug Administration approved a new indication for the injection of Wegovy, to lower the risk of heart attack, stroke, and cardiovascular death in obese or overweight adults with cardiovascular diseases.

- Report ID: 6544

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.