Bipolar Electrosurgical Devices Market Outlook:

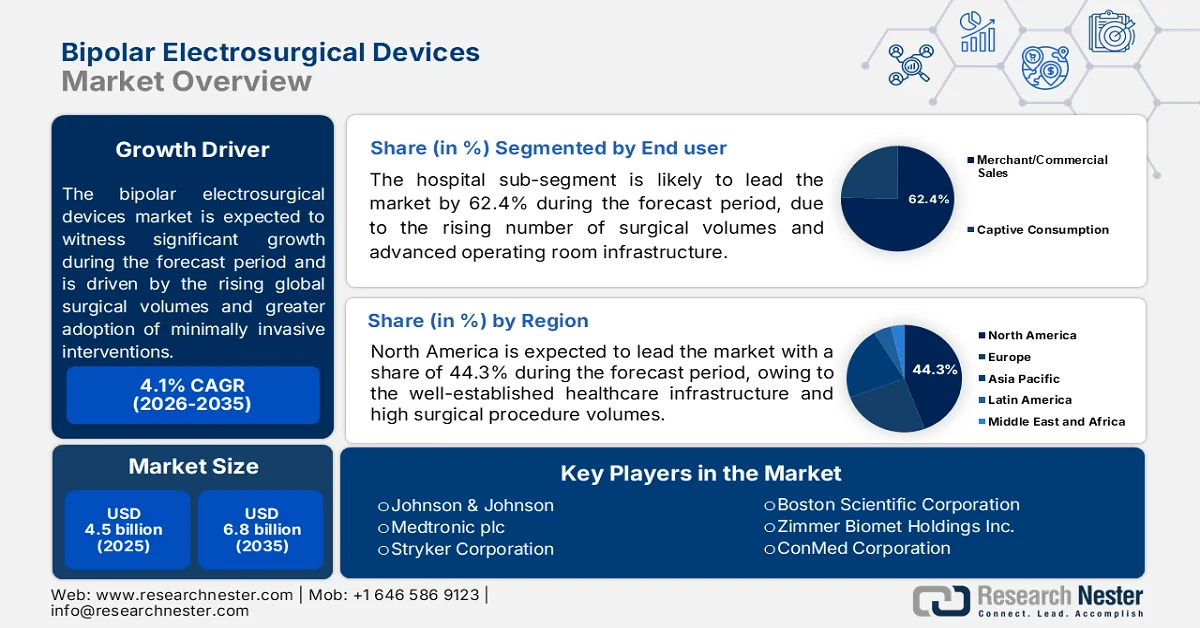

Bipolar Electrosurgical Devices Market size was valued at USD 4.5 billion in 2025 and is expected to reach USD 6.8 billion by the end of 2035, registering around 4.1% CAGR during the forecast period i.e., 2026-2035. In 2026, the industry size of bipolar electrosurgical devices is estimated at USD 4.7 billion.

The bipolar electrosurgical devices market is expanding in line with the rising global surgical volumes, increasing oncology procedures, and greater adoption of minimally invasive interventions across hospital networks and ambulatory surgical centers. The World Health Organization's November 2023 data reported that noncommunicable diseases account for approximately 74% of global deaths, with cancer remaining a major contributor to surgical demand. The WHO February 2024 report indicates that 20 million new cancer cases globally, increasing the need for precision-based surgical interventions in gynecology, oncology, gastroenterology, and cardiovascular procedures. Moreover, the surgical site infection reduction and intraoperative bleeding control as critical hospital quality priorities are supporting procurement of advanced electrosurgical systems with controlled thermal spread and vessel sealing capabilities.

Demand is further supported by aging demographics and rising chronic disease treatment volumes across Europe and Asia Pacific healthcare systems. According to the Office for National Statistics, in November 2022, adults aged 65 years and older represented more than 18% of the population across OECD countries in recent assessments, contributing to higher procedural demand for orthopedic, urologic, and gastrointestinal surgeries. Government-backed healthcare infrastructure expansion programs in emerging economies are also increasing access to surgical care, particularly in secondary and tertiary hospitals. In addition, reimbursement support for the minimally invasive and outpatient procedures in the developed healthcare systems is pushing the hospitals to upgrade energy-based surgical platforms that improve operative precision and reduce hospitalization duration.

Key Bipolar Electrosurgical Devices Market Insights Summary:

Regional Highlights:

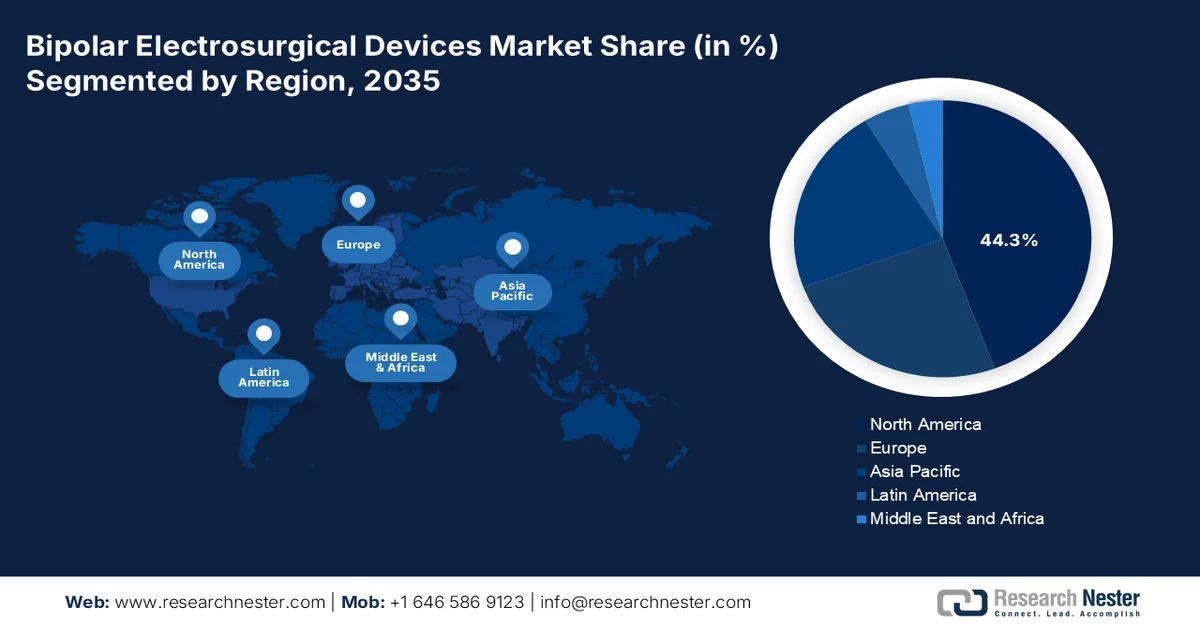

- North America bipolar electrosurgical devices market is anticipated to capture 44.3% revenue share by 2035, attributed to expanding minimally invasive surgeries, advanced healthcare infrastructure, and strong focus on patient safety and surgical precision

- Asia Pacific is projected to witness considerable growth throughout 2026-2035, fueled by rising healthcare infrastructure investments, growing surgical volumes, and increasing adoption of minimally invasive procedures

Segment Insights:

- The hospitals segment in the bipolar electrosurgical devices market is expected to account for 62.4% share by 2035, propelled by rising surgical procedure volumes, advanced operating room infrastructure, and increased investment in reusable bipolar systems

- The minimally invasive surgery segment is set to maintain its leading position during 2026-2035, reinforced by growing preference for precise coagulation, faster patient recovery, and advancements in bipolar vessel sealing technologies

Key Growth Trends:

- Increasing cancer surgery volumes

- Rising focus on surgical safety and infection reduction

Major Challenges:

- Risk of clinical complications

- Tariff pressures and supply chain disruptions

Key Players: Johnson & Johnson (The U.S.), Medtronic plc (The U.S.), Stryker Corporation (The U.S.), Boston Scientific Corporation (The U.S.), Zimmer Biomet Holdings Inc. (The U.S.), ConMed Corporation (The U.S.), Integra LifeSciences Holdings Corporation (The U.S.), Encision Inc. (The U.S.), Kirwan Surgical Products LLC (The U.S.), Symmetry Surgical Inc. (The U.S.), Olympus Corporation (Japan), Karl Storz SE & Co. KG (Germany), Erbe Elektromedizin GmbH (Germany), B. Braun Melsungen AG (Germany), KLS Martin Group (Germany), BOWA-electronic GmbH & Co. KG (Germany), Smith & Nephew plc (UK), LED SpA (Italy), XcelLance Medical Technologies Pvt. Ltd. (India), Micro-Tech (China).

Global Bipolar Electrosurgical Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.5 billion

- 2026 Market Size: USD 4.7 billion

- Projected Market Size: USD 6.8 billion by 2035

- Growth Forecasts: 5.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (44.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Mexico, Saudi Arabia

Last updated on : 15 May, 2026

Bipolar Electrosurgical Devices Market - Growth Drivers and Challenges

Growth Drivers

- Increasing cancer surgery volumes: The growing cancer volumes are driving the demand for bipolar electrosurgical devices in tumor resections and minimally invasive oncology procedures. The NLM study published in March 2024 showed that nearly 32 million cancer-related operations were performed annually and are estimated to reach 45 million by 2030. Governments are expanding the oncology treatment infrastructure and surgical capacity. The U.S. National Cancer Institute (NCI) allocated funds in cancer research and treatment-related funding supporting hospitals adopting the precision surgical technologies. Bipolar electrosurgical devices are increasingly preferred in oncological surgeries because they enable controlled thermal spread near delicate tissues and vessels. Public cancer control programs in Europe and Asia are also increasing the surgical intervention rates, mainly for colorectal, cervical, liver, and breast cancers. Hospitals are integrating advanced energy devices to improve operating efficiency and reduce postoperative complications during complex cancer surgeries.

- Rising focus on surgical safety and infection reduction: Government healthcare agencies are strengthening the regulations and clinical guidelines related to surgical safety, increasing the adoption of precision electrosurgical technologies. The U.S. CDC continues to emphasize prevention of surgical site infections, which affect millions of patients globally and increase hospitalization costs. Bipolar electrosurgical systems support safer tissue dissection and controlled coagulation, reducing collateral tissue damage compared to conventional monopolar systems in specific procedures. Public hospitals are adopting advanced vessel sealing and smoke reduction technologies to improve operating room safety standards. Moreover, in Europe, healthcare authorities are also implementing stricter operating room efficiency and sterilization protocols under patient safety initiatives. These procurement patterns are particularly evident in high-volume surgical specialties such as gynecology, neurosurgery, and ENT procedures.

- Rising government funding for surgical infrastructure modernization: Government-backed hospital modernization programs are increasing the procurement of advanced electrosurgical systems, including bipolar devices. According to the Public Citizen, June 2024 data, the Centers for Medicare and Medicaid Services projected health care spending would reach USD 7.7 trillion by 2032, representing 19.7% of the U.S. economy. Public investments are supporting the operating room expansion, outpatient surgery capacity, and energy-efficient surgical technologies. In Europe, the EU4Health programme allocated funds to strengthen healthcare systems and improve the surgical preparedness across member states. These funding initiatives are enabling the hospitals to replace conventional surgical systems with advanced bipolar platforms that improve coagulation precision and reduce blood loss. This trend is visible in tertiary care hospitals managing oncology, cardiovascular, and gastrointestinal procedures with higher surgical volumes.

Challenges

- Risk of clinical complications: Patient safety concerns represent a formidable regulatory and liability challenge for new tissue damage, unintended burns, nerve damage, and surgical smoke generation. Clinical studies have questioned whether newer bipolar technologies provide superior hemostatic outcomes compared to standard unipolar devices, with recent randomized controlled trials failing to support superiority claims for saline-coupled bipolar sealers. This clinical uncertainty creates a high evidentiary burden for manufacturers seeking regulatory approval and hospital adoption.

- Tariff pressures and supply chain disruptions: Global trade tensions, mainly U.S. tariffs implemented, have severely impacted the medical device manufacturing economies. Bipolar electrosurgical systems depend on the advanced components, including stainless steel electrodes, heat-resistant polymer handles, and the electronic modules commonly sourced from China, Germany, or Japan. These components face significant tariff exposure, increasing the manufacturing costs and reducing profit margins for new entrants who lack diversified supply chains. Global supply chains face extended customs procedures, longer lead times, and increased logistics costs, potentially delaying production and export of bipolar electrosurgical units.

Bipolar Electrosurgical Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.1% |

|

Base Year Market Size (2025) |

USD 4.5 billion |

|

Forecast Year Market Size (2035) |

USD 6.8 billion |

|

Regional Scope |

|

Bipolar Electrosurgical Devices Market Segmentation:

End user Segment Analysis

Under the end user segment, hospitals remain the dominant sub-segment in the bipolar electrosurgical devices market and are poised to hold the share value of 62.4% by the end of 2035. The dominance is due to the rising number of surgical volumes, advanced operating room infrastructure, and the ability to invest in reusable bipolar generators and instruments. According to the NLM study published in February 2023, U.S. hospitals have performed more than 15 million inpatient surgeries requiring electrosurgical devices, with bipolar technology usage growing annually, resulting in average intraoperative blood loss compared to conventional methods. Hospitals continue to prioritize bipolar systems for minimally invasive procedures driven by value-based care models that reward fewer complications and shorter lengths of stay.

Surgery Type Segment Analysis

The minimally invasive surgery sub-segment is the leading segment in the bipolar electrosurgical devices market. Bipolar devices are preferred in MIS for precise coagulation and reduced thermal spread, which is critical in laparoscopic and robotic procedures. According to the NLM March 2026 study, MIS procedures accounted for 28,243,407 procedures, driven by faster recovery times and lower infection rates. Moreover, millions of MIS procedures requiring bipolar electrosurgery were performed in U.S. hospitals. The shift toward outpatient and same‑day discharge surgeries further accelerates adoption. With ongoing advancements in bipolar vessel sealing, MIS is expected to maintain its leadership. Additionally, the integration of artificial intelligence into bipolar generators for real-time tissue feedback is poised to further enhance the surgical outcomes in MIS.

Modality Segment Analysis

Standalone bipolar generators are the leading modality sub‑segment of the modality, holding the largest share in 2035. These dedicated units offer precise control of bipolar energy output, minimizing stray current and collateral tissue damage compared to combined monopolar/bipolar generators. According to FDA medical device registration data, many new standalone bipolar generator models were cleared for marketing, reflecting strong manufacturer and clinical interest. The U.S. surgical facilities reported that operating rooms primarily use standalone bipolar generators for delicate procedures such as neurosurgery and gynecology. Their lower risk of capacitive coupling and compatibility with advanced vessel‑sealing instruments make them the preferred choice for safety‑focused surgical teams, driving continued revenue leadership.

Our in-depth analysis of the bipolar electrosurgical devices market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Application |

|

|

End user |

|

|

Modality |

|

|

Surgery Type |

|

|

Component |

|

|

Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Bipolar Electrosurgical Devices Market - Regional Analysis

North America Market Insights

North America dominated the bipolar electrosurgical devices market in 2025 and is projected to hold the regional revenue share of 44.3% by 2035. The bipolar electrosurgical devices market is supported by a well-established healthcare infrastructure and high surgical procedure volumes. The region benefits from continuous operating room modernization efforts and the expansion of ambulatory surgical centers that prioritize precise energy-based hemostasis. Increasing adoption of minimally invasive and robotic-assisted surgeries further drives demand for bipolar instruments due to their superior thermal control and reduced collateral tissue damage. Additionally, harmonized regulatory pathways between the U.S. and Canada facilitate efficient device approvals and market entry. The presence of major manufacturers and a strong emphasis on patient safety and surgical outcomes continue to reinforce North America's dominant position in the global landscape.

The increasing adoption of minimally invasive gynecological and laparoscopic procedures across hospitals and ambulatory surgical centers is shaping the bipolar electrosurgical devices market in the U.S. According to the NLM study published in January 2025, hysterectomy remains one of the most commonly performed surgeries in the U.S., with nearly 90% conducted for benign conditions such as uterine fibroids, endometriosis, and abnormal uterine bleeding. Since most hysterectomies now utilize minimally invasive techniques, demand for bipolar vessel sealing devices has increased significantly as these procedures require advanced electrosurgical instruments for vascular sealing and tissue dissection. The transition away from conventional monopolar systems toward advanced bipolar technologies is also accelerating due to lower thermal injury risk and improved operative efficiency. FDA-cleared systems, such as LigaSure, as stated in the NLM January 2025 study, are used in more than 25 million procedures globally, further supporting recurring procurement demand across U.S. surgical facilities.

The rising surgical procedure volumes increased chronic disease burden, and substantial federal healthcare investment is fueling the bipolar electrosurgical devices market in Canada. According to the NLM June 2022 study, surgeons performed more than 2.3 million procedures, reflecting a sustained demand for the advanced surgical technologies across hospitals and minimally invasive care settings. In February 2023, the Government of Canada announced a healthcare investment package of USD 198.6 billion over 10 years, including USD 46.2 billion in new funding to strengthen healthcare infrastructure, reduce surgical backlogs, and improve access to modern medical technologies through the Canada Health Transfer and provincial agreements. Demand for bipolar electrosurgical systems is also increasing because chronic diseases continue to drive surgical intervention rates nationwide. According to the Government of Canada, September 2023 data, approximately 45.1% of Canadian adults lived with at least one chronic disease in 2021. These trends are increasing the hospital adoption of advanced bipolar vessel sealing technologies for cardiovascular, oncological, thoracic, and gastrointestinal surgeries requiring precise coagulation and reduced tissue trauma.

Chronic Disease Risk Factors, aged 18 & Older, 2023 (in %)

|

Factor |

Population Center |

Rural Area |

|

Overweight |

35.8 |

34.3 |

|

Obesity |

29 |

36.7 |

|

Arthritis |

19.5 |

26.2 |

|

High Blood Pressure |

19.4 |

22.1 |

|

Diabetes |

7.8 |

9.1 |

|

Heart Disease |

6.0 |

7.7 |

|

Stroke |

1.1 |

1.6 |

Source: Government of Canada, March 2025

APAC Market Insights

Asia Pacific is projected to expand at a considerable during the assessed period, 2026 to 2035. The bipolar electrosurgical devices market is driven by the large-scale healthcare infrastructure investments and rapidly expanding surgical volumes. Countries such as China, India, Japan, and South Korea are witnessing a steady shift toward minimally invasive procedures where the bipolar devices are preferred for their precision and reduced thermal spread. Government-led hospital modernization programs and increasing medical tourism further support bipolar electrosurgical devices market expansion. Additionally, rising geriatric populations and the growing prevalence of chronic diseases requiring surgical intervention are stimulating the adoption. Local manufacturing initiatives and technology transfer agreements are making advanced bipolar systems more accessible across both urban and semi-urban healthcare facilities.

Rising surgical volumes, increasing healthcare expenditure, and rapid development of public hospital infrastructure are driving the bipolar electrosurgical devices market in India. According to the IBEF November 2025 data, nearly USD 11.50 billion is allocated to the healthcare sector, supporting the expansion of tertiary care services, medical technology adoption, and surgical capacity enhancement across government hospitals. The demand for advanced electrosurgical devices is also increasing with the growth of chronic disease burden and surgical interventions. Moreover, the NLM March 2024 study indicates that non-communicable diseases account for more than 60% of total deaths in India, increasing procedural demand for oncology, cardiovascular, gastrointestinal, and gynecological surgeries. Further, the Digital Sansad February 2025 report indicated that Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) reported over 8.59 crore hospital admissions, increasing utilization of minimally invasive and electrosurgical procedures in empaneled hospitals nationwide. These factors are pushing the healthcare providers to procure advanced bipolar vessel sealing and coagulation systems that improve surgical efficiency and reduce perioperative complications.

The Japan bipolar electrosurgical devices market is expanding rapidly and is valued at USD 183.52 million in 2025 and is expected to reach USD 379.08 million in 2035, and is poised to expand at a CAGR 7.24% and is poised to reach USD 202.15 million by the end of 2026. The bipolar electrosurgical devices market is growing due to rising surgical demand, aging demographics, and continued healthcare investment. According to the J Stage 2022 report, national medical expenditure exceeded JPY 43 trillion, supporting hospital technology upgrades and the minimally invasive surgery adoption. The NLM July 2024 study reported that nearly 29% of the population was aged 65 years and older, increasing demand for cardiovascular, oncological, and gastrointestinal surgeries. Additionally, MHLW reimbursement expansion for laparoscopic and robotic-assisted procedures has accelerated procurement of advanced bipolar vessel sealing systems across Japan hospitals.

Europe Market Insights

Europe represents a mature and steadily growing bipolar electrosurgical devices market for bipolar electrosurgical devices, characterized by strong regulatory oversight and widespread adoption of minimally invasive surgical techniques. The region benefits from the well-funded public healthcare systems that prioritize operating room modernization and patient safety standards. Countries such as Germany, France, Italy, and the UK lead in the surgical volume with the increasing utilization of bipolar devices in the general gynecologic and urologic procedures. The European Union's focus on standardizing medical device regulations under the MDR has raised quality benchmarks, promoting the hospitals to replace legacy equipment with compliant advanced bipolar systems. Additionally, rising ambulatory surgery adoption and robotic-assisted procedure volumes further drive demand. Manufacturers offering compact, user-friendly bipolar generators with robust clinical documentation find favorable conditions across both Western and Central European bipolar electrosurgical devices markets.

The increasing surgical backlogs, rising chronic disease prevalence, and continued public healthcare investment are driving the bipolar electrosurgical devices market in the UK. NLM October 202 study reported that the elective care waiting list exceeded 7 million cases in 2024, increasing demand for advanced surgical technologies that improve operating room efficiency and reduce procedure times. To address these pressures, the UK government and NHS announced multi-year healthcare funding support, with the Department of Health and Social Care allocating more than USD 256 billion for the health and social care services as per the FEE August 2025 data. Demand for the bipolar electrosurgical systems is also supported by the rising disease burden. As of 2026, Derbyshire County Council reported that cancer accounted for 134,000 deaths in England in 2023, while cardiovascular diseases remained a leading cause of hospitalization. These trends are accelerating hospital procurement of advanced bipolar vessel sealing and minimally invasive surgical technologies across gynecological, colorectal, cardiothoracic, and oncological procedures.

The bipolar electrosurgical devices market in Germany is expanding due to rising surgical demand, increasing healthcare expenditure, and strong hospital infrastructure modernization initiatives. According to the Destatis April 2023 data, healthcare expenditure exceeded USD 512 billion in recent national assessments, reflecting continued investment in hospital services, surgical technologies, and advanced medical equipment procurement. Demand for bipolar electrosurgical systems is also increasing because Germany has one of Europe’s largest aging populations, with individuals aged 67 years and older projected to reach 20.5 million by the mid-2030s, as per Destatis December 2025 data. This is driving higher volumes of cardiovascular, orthopedic, oncological, and gastrointestinal surgeries. In addition, cancer remains among the leading causes of mortality in Germany, contributing to increased minimally invasive and precision-based surgical procedures. Hospitals are therefore accelerating the adoption of advanced bipolar vessel sealing technologies to improve operative efficiency, reduce blood loss, and support high procedural throughput across public and university healthcare facilities.

Key Bipolar Electrosurgical Devices Market Players:

- Johnson & Johnson (The U.S.)

- Medtronic plc (The U.S.)

- Stryker Corporation (The U.S.)

- Boston Scientific Corporation (The U.S.)

- Zimmer Biomet Holdings Inc. (The U.S.)

- ConMed Corporation (The U.S.)

- Integra LifeSciences Holdings Corporation (The U.S.)

- Encision Inc. (The U.S.)

- Kirwan Surgical Products LLC (The U.S.)

- Symmetry Surgical Inc. (The U.S.)

- Olympus Corporation (Japan)

- Karl Storz SE & Co. KG (Germany)

- Erbe Elektromedizin GmbH (Germany)

- B. Braun Melsungen AG (Germany)

- KLS Martin Group (Germany)

- BOWA-electronic GmbH & Co. KG (Germany)

- Smith & Nephew plc (UK)

- LED SpA (Italy)

- XcelLance Medical Technologies Pvt. Ltd. (India)

- Micro-Tech (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Johnson & Johnson is dominating the bipolar electrosurgical devices market and uses its Ethicon division to offer advanced energy devices. The company focuses on integrating bipolar technology with smart generators that provide real-time feedback on tissue impedance, improving surgical precision and reducing thermal spread. In 2025, the company reported a sales growth of 2025 of 9.1% to USD 24.6 billion in Q4.

- Medtronic plc has strengthened its position in the bipolar electrosurgical devices market by featuring the Vessel Sealing System. The company’s strategy emphasizes combining bipolar energy with an advanced hemostasis algorithm to reduce operative time and complications. Medtronic is also investing in cloud-connected electrosurgical generators that capture bipolar device usage data for surgical analytics.

- Stryker Corporation actively competes in the bipolar electrosurgical devices market via its surgical technologies division, offering the PEAK PlasmaBlade bipolar system that uses pulsed plasma energy for cutting and coagulation with minimal lateral thermal damage. The key strategic initiatives include developing disposable bipolar pencils and forceps that optimize electrical current delivery.

- Boston Scientific emphasizes bipolar solutions for gastroenterology and pulmonary interventions, such as bipolar resection devices used in endoscopy. In the bipolar electrosurgical devices market, the company’s strategy involves leveraging its acquisition of endoscopic technology firms to refine bipolar hemostasis catheters and polypectomy snares. In 2025, the company made a net sale of USD 20 billion.

- Zimmer Biomet Holdings Inc. leads the bipolar electrosurgical devices market primarily via its orthopedically focused energy platforms with bipolar forceps and probes for soft tissue management in joint replacement and spine surgeries. Strategic initiatives involve developing bipolar devices optimized for use with robotic instruments to reduce the contamination risks.

Here is a list of key players operating in the global bipolar electrosurgical devices market:

The global bipolar electrosurgical devices market is highly competitive, characterized by the presence of several multinational corporations and specialized medical technology firms. Major players are focusing on strategic initiatives such as geographic expansion into emerging bipolar electrosurgical devices markets, mergers and acquisitions, and the development of advanced energy-based devices to improve surgical precision and patient safety. For example, in February 2025, Micro-Tech officially completed the acquisition of a 51% stake in Creo Medical S.L.U. (CME). For instance, companies are launching hybrid products that combine ultrasonic and bipolar energy to enhance the hemostatic cutting and vessel sealing. Moreover, the bipolar electrosurgical devices market leaders are pursuing regulatory approvals for next-gen generators and investing in R&D to create cost-efficient materials.

Corporate Landscape of the Bipolar Electrosurgical Devices Market:

Recent Developments

- In September 2025, Medtronic, a global leader in healthcare technology, announced the launch of two advanced surgical energy generators in India under the Valleylab™ FT10 series, the Valleylab™ FT10 Electrosurgical Generator (VLFT10FXGEN) and the Valleylab™ FT10 Vessel Sealing Generator (VLFT10LSGEN).

- In March 2025, Johnson & Johnson MedTech, a global leader in surgical technologies and solutions, announced the launch of the DUALTO™ Energy System. This surgical solution combines multiple energy modalities into an integrated platform for use across open and minimally invasive surgery.

- In January 2024, Olympus Corporation announced the commercialization of its new ESG-410™ Surgical Energy Platform for conventional monopolar and bipolar, advanced energy applications, now including ultrasonic dissection and hybrid energy.

- Report ID: 450

- Published Date: May 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.