Autonomous Mobile Robots Market Outlook:

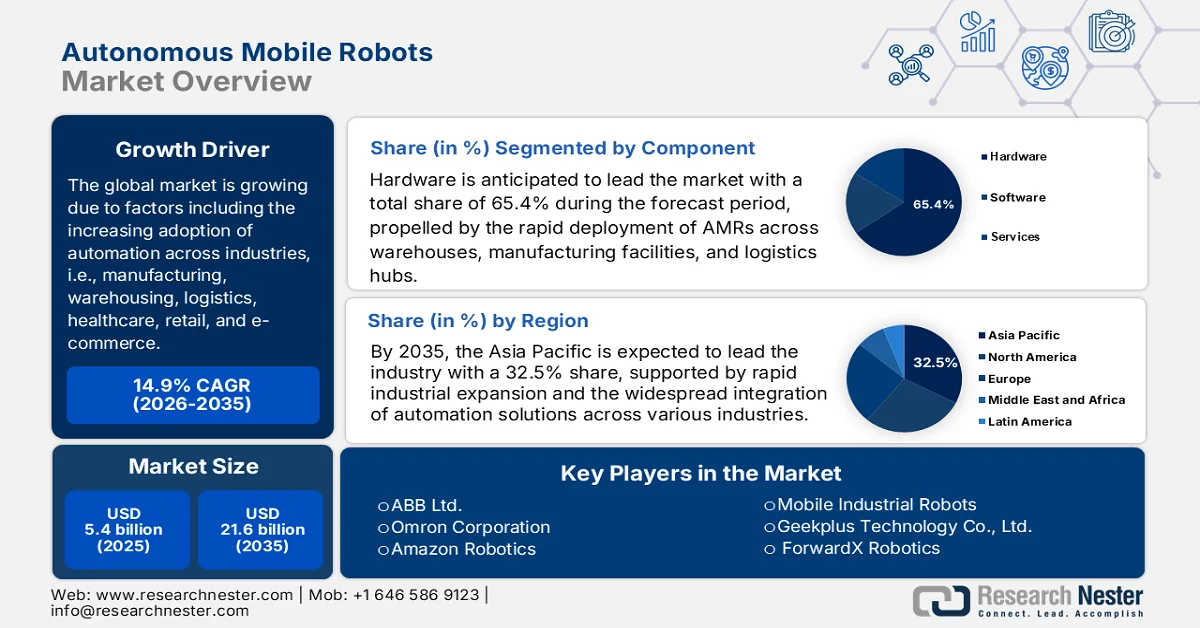

Autonomous Mobile Robots Market size was valued at USD 5.4 billion in 2025 and is projected to reach USD 21.6 billion by the end of 2035, registering around 14.9% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of autonomous mobile robots is estimated at USD 6.2 billion.

The global autonomous mobile robots (AMR) market is projected to experience a surging growth due to factors including the increasing adoption of automation across industries, i.e., manufacturing, warehousing, logistics, healthcare, retail, and e-commerce. Organizations across the globe are deploying these robots with a main goal to improve operational efficiency, enhance productivity, optimize material handling processes, and support flexible workflows in certain dynamic environments. In September 2024, the article published by the International Federation of Robotics stated that industrial automation is expanding, wherein more than 4.28 million industrial robots were operating in factories worldwide in 2023, and it is a 10% increase year-on-year. The report also outlined that annual installations were strong at 541,302 units, the second-highest level ever recorded, with Asia dominating global demand, thus denoting a huge opportunity for the market to grow in the upcoming years.

Global Industrial Robot Growth 2023-2024: Regional Installations, Market Share & Country-Wise Statistics

|

Region / Country |

Industrial Robot Installations (2023) |

Growth vs 2022 |

Notes |

|

Worldwide stock |

4,281,585 operational units |

+10% |

All-time high |

|

Global installations |

541,302 units |

-2% vs 2022 |

2nd highest ever |

|

Asia (total share) |

70% of new installs |

- |

Dominant region |

|

China |

276,288 |

-5% |

51% of global installs |

|

Japan |

46,106 |

-9% |

2nd largest market |

|

South Korea |

31,444 |

-1% |

4th largest globally |

|

India |

8,510 |

+59% |

Fastest growing |

|

Europe (total) |

92,393 |

+9% |

Record high |

|

Germany |

28,355 |

+7% |

Largest in Europe |

|

Americas (total) |

55,389 |

-1% |

Near record level |

|

U.S. |

37,587 |

-5% |

Largest in the Americas |

Source: IFR

Furthermore, the advancements in terms of AI, machine learning, sensor technologies, navigation systems, and connectivity solutions are enabling AMRs to operate more intelligently and autonomously, prompting a profitable business environment for the autonomous mobile robots market. The rising emphasis on smart factories, digital transformation initiatives, and collaborative human-robot operations is also expanding market opportunities. In December 2025, Hyundai Motor Group introduced its MobED platform at iREX 2025, which is its first mass-produced autonomous mobility robot that is designed for industrial and everyday use. This robot has been built on three pillars, i.e., adaptive mobility, intuitive autonomy, and infinite journey. MobED combines eccentric posture control, AI-powered navigation, and modular versatility to redefine robotics functionality, thus making it suitable for bolstering the market’s growth and exposure.

Key Autonomous Mobile Robots Market Insights Summary:

Regional Highlights:

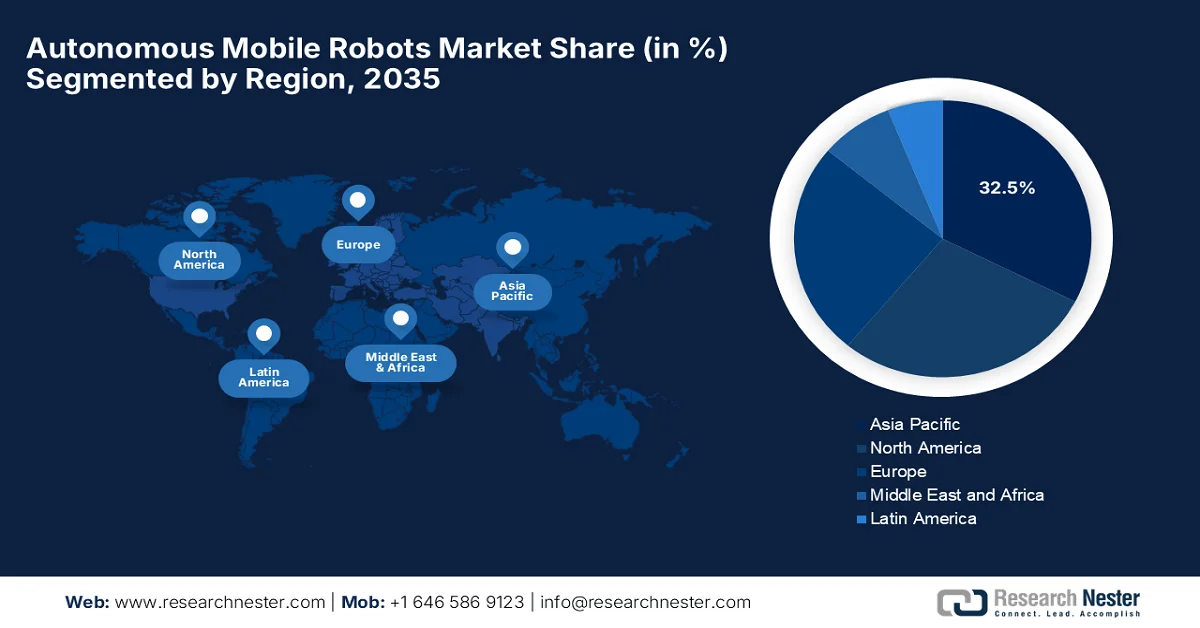

- Asia Pacific is projected to command 32.5% of the autonomous mobile robots market share by 2035, stimulated by continued industrial growth and increasing adoption of automation technologies

- North America is witnessing notable expansion in the market throughout 2026–2035, attributed to the strong emphasis on supply chain resilience, investments in advanced warehouse automation, and the scale of the regional e-commerce infrastructure

Segment Insights:

- Hardware is expected to account for 65.4% of the autonomous mobile robots market share by 2035, fueled by rapid AMR deployment across warehouses, manufacturing facilities, and logistics hubs alongside rising demand for LiDAR, sensors, cameras, controllers, and onboard computing systems

- Goods-to-person picking robots are anticipated to secure a considerable revenue share in the market by 2035, underpinned by increasing pressure to meet shorter delivery windows and manage rising order volumes across warehouses and distribution centers

Key Growth Trends:

- Growth of E-commerce and warehousing

- Labor shortages and workforce challenges

Major Challenges:

- High initial investment and integration complexity

- Safety, navigation, and operational reliability concerns

Key Players: ABB Ltd. (Switzerland) ,Omron Corporation (Japan) ,Mobile Industrial Robots (MiR) (Denmark) ,Locus Robotics (U.S.) ,Geekplus Technology Co., Ltd. (China) ,HIKROBOT (China) ,ForwardX Robotics (China) ,Seegrid Corporation (U.S.) ,Fetch Robotics (U.S.) ,Zebra Technologies Corporation (U.S.) ,KUKA AG (Germany) ,Daifuku Co., Ltd. (Japan) ,OTTO Motors (Canada) ,Amazon Robotics (U.S.) ,Aethon Inc. (U.S.) ,SEER Robotics (China).

Global Autonomous Mobile Robots Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.4 billion

- 2026 Market Size: USD 6.2 billion

- Projected Market Size: USD 21.6 billion by 2035

- Growth Forecasts: 14.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (32.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, Germany, South Korea

- Emerging Countries: India, Canada, Singapore, Mexico, United Arab Emirates

Last updated on : 15 June, 2026

Autonomous Mobile Robots Market - Growth Drivers and Challenges

Growth Drivers

- Growth of E-commerce and warehousing: The booming growth of e-commerce and retail is readily catalyzing adoption in the autonomous mobile robots (AMR) market in warehouses as well as fulfilment centers. On the other hand, high-order volumes, faster delivery expectations, and complex inventory systems require efficient automation, in which these AMRs help with reducing errors, thereby enabling faster, more reliable supply chain performance. For instance, in October 2023, Amazon introduced two new robotic solutions, which are called Sequoia and Digit, with the main goal of enhancing workplace safety and speeding up customer deliveries. Besides, Sequoia efficiently integrates mobile robots, gantry systems, robotic arms, and ergonomic workstations to process inventory up to 75% faster, whereas Digit is developed with Agility Robotics and is a bipedal mobile manipulator especially designed to handle repetitive tasks.

- Labor shortages and workforce challenges: The global labor shortages in warehousing and manufacturing are readily accelerating the adoption of autonomous mobile robots. Organizations across most nations are struggling to hire and retain workers for certain physically demanding tasks, which in turn is boosting uptake in the autonomous mobile robots (AMR) market. As per an article published by the World Economic Forum in September 2025, global labor industries in 2025 show low unemployment in many economies, with the OECD average around 4.9%, but with sharp regional variation, such as Mexico at 2.6% and South Africa at 32.9% joblessness. The report also outlined that labor participation is also shifting, such as the U.S. rate falling to 62.2%, when compared with 70.5% in New Zealand, reflecting ageing and structural exits from work. Overall, AI, digitalization, and green transition are reshaping demand for skills, prompting a huge growth opportunity for autonomous mobile robots.

Challenges

- High initial investment and integration complexity: One of the major challenges faced by the autonomous mobile robots market is the exponential investments which are required for deployment and integration complexity. These AMRs can reduce labor costs and improve operational efficiency in a span of years, but initial expenses associated with robot procurement, fleet management software, infrastructure upgrades, system customization, and employee training can be substantial, making it challenging for small and medium-sized enterprises. In addition, integrating AMRs with existing warehouse management systems, manufacturing execution systems, and enterprise resource planning platforms also requires specialized knowledge and extended implementation timelines. Apart from this, organizations that are operating in terms of legacy facilities may face additional compatibility issues that increase deployment complexity, thereby negatively impacting the market’s growth.

- Safety, navigation, and operational reliability concerns: There are advancements in terms of AI, sensors, and machine vision technologies, but ensuring safe and reliable AMR operation in dynamic environments is considered to be a challenge for the autonomous mobile robots (AMR) market. These robots need to continuously navigate around workers, forklifts, machinery, and unexpected obstacles, thereby also maintaining productivity and compliance with regular safety regulations. The existence of complex industrial settings with changing layouts, narrow aisles, and high traffic volumes can affect navigation accuracy as well as operational efficiency. Any type of system failure, collision, or navigation error may disrupt workflow and create safety risks in the work environment. In addition, manufacturers and logistics operators necessitate extensive testing and validation before large-scale deployment, thus creating barriers to widespread adoption in this field.

Autonomous Mobile Robots Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

14.9% |

|

Base Year Market Size (2025) |

USD 5.4 billion |

|

Forecast Year Market Size (2035) |

USD 21.6 billion |

|

Regional Scope |

|

Autonomous Mobile Robots Market Segmentation:

Component Segment Analysis

Under the component segment, hardware is anticipated to lead the autonomous mobile robots market with a total share of 65.4% during the forecast period. The segment’s dominance is largely propelled by the rapid deployment of AMRs across warehouses, manufacturing facilities, and logistics hubs. Simultaneously, there has been a strong demand for key components such as LiDAR, robot platforms, controllers, cameras, sensors, and onboard computing systems, which continues to fuel strong hardware investment. Ongoing advancements in sensing technologies and edge computing are efficiently enhancing navigation precision, operational reliability, and real-time decision-making capabilities. In addition, enterprises are highly focused on durable and scalable hardware solutions to support higher payload capacities, extended operating cycles, and hence denote a wider segment’s scope.

Type Segment Analysis

By the end of 2035, the goods-to-person picking robots segment, which is under the type segment, is expected to attain a considerable revenue share in the autonomous mobile robots (AMR) market. The segment’s growth is mainly driven by the pressure to meet shorter delivery windows and manage rising order volumes, which is boosting its adoption across warehouses and distribution centers. Goods-to-person systems also improve space efficiency and enable scalable operations, making them highly suitable for dense, high-throughput fulfillment environments. For instance, in May 2024, GXO has deployed a robotics solution in France, which integrates about 500 autonomous mobile robots to handle 70,000 bins across high-density storage racks. This system boosts productivity, accuracy, and safety while offering agility to meet seasonal demand shifts, thus contributing to the segment’s expansion.

Battery Type Segment Analysis

In the autonomous mobile robots market, the lead battery is forecasted to attain a notable share during the discussed timeframe. The extensive use of AGVs in cost-sensitive industries, where the low cost and dependable performance of lead-acid batteries align with operational and budget requirements, is the main factor behind the segment’s leadership. These lead-acid batteries provide a very stable and consistent power supply, thereby ensuring reliable AGV performance and durability across various working conditions. Therefore, this makes them highly suitable for industries that depend heavily on continuous material handling operations. In addition, their relatively low upfront cost when compared to alternative battery technologies makes them an attractive option for companies that are aiming to control capital expenditure while maintaining efficient automation systems.

Our in-depth analysis of the autonomous mobile robots (AMR) market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Type |

|

|

Battery Type |

|

|

Application |

|

|

Payload Capacity |

|

|

End use |

|

|

Navigation Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Autonomous Mobile Robots Market - Regional Analysis

APAC Market Insights

The Asia Pacific autonomous mobile robots market is anticipated to garner the highest share of 32.5% during the forecast period. The region’s dominance is effectively propelled by continued industrial growth and increasing adoption of automation technologies. Countries such as China, India, and Japan are making heavy investments in terms of smart manufacturing and digital infrastructure to enhance productivity and reduce dependence on manual labor. For instance, in October 2023, LexxPluss secured a generous amount of USD 19.4 million from NEDO to accelerate development of a new autonomous mobile robot for manufacturing and automotive industries, doubling payload capacity for EV components. This AMR uses laser-based navigation to adapt routes without magnetic tape, whereas the initiative supports automation of assembly-to-warehouse links, aligning with the global shift to electric vehicles.

The nation's massive manufacturing base, soaring e-commerce sector, and a strong national focus toward large-scale automation are certain factors driving the expansion of the autonomous mobile robots (AMR) market in China. The suitable government subsidies and aggressive smart-factory initiatives have created a highly supportive ecosystem for rapid technological iteration. In February 2026, the article published by China Power Organization stated that China has registered itself as a predominant leader in robotics adoption, by installing 295,000 new industrial robots in 2024, more than any other country worldwide. The article also outlined that the country’s robotics industry was valued at about USD 47 billion in 2024 and is projected to grow at around 23% annually through 2028. Furthermore, robot density reached 166 robots per 10,000 workers in 2024, thus reflecting rapid automation across manufacturing, electronics, automotive, and logistics sectors.

In India, the autonomous mobile robots market is gaining enhanced traction, powered by the structural modernization of the nation’s manufacturing infrastructure and the rapid expansion of digital commerce networks. The country’s market is being accelerated by the logistics and warehousing sectors, wherein these operators utilize intelligent fleets to streamline intense order sorting and optimize fulfillment centers. In March 2023, WEG announced the launch of the WMR autonomous mobile robot to optimize manufacturing operations and logistics, which is powered by SLAM-based natural navigation for dynamic obstacle avoidance and route re-planning. The robot enhances efficiency in repetitive transport tasks, supports Industry 4.0 goals, and runs fully on electric batteries, thus making it suitable for standard market growth.

North America Market Insights

The autonomous mobile robots (AMR) market in North America is expanding due to the high focus on supply chain resilience, investments in advanced warehouse automation, and the scale of the regional e-commerce infrastructure. The regional market benefits from the presence of well-established technology developers and exponential venture capital funding, which continuously drive innovation in artificial intelligence, cloud-based fleet orchestration, and edge computing. In December 2024, the article published by AAA stated that AMRs are evolving with new safety standards expected in North America, which include frameworks such as ANSI/RIA R15.08 in the U.S. Besides, these updates focus on improving system-level safety, cybersecurity, and large-scale fleet integration in industrial environments. In the U.S., global e-commerce hubs are deploying AMRs in collaborative warehouse systems, and e-commerce fulfillment centers use coordinated AMR fleets to move inventory directly to pickers, improving accuracy and productivity.

A profound nationwide focus on supply chain nearshoring and the rapid, continuous growth of the domestic e-commerce infrastructure are the main factors responsibly boosting the autonomous mobile robots market in the U.S. The market is characterized by an intense technological innovation, benefiting from substantial venture capital investments and a concentrated cluster of pioneering robotics companies who are specializing in AI, cloud-based fleet orchestration, and sensor fusion. In February 2024, OMRON Automation Americas announced the launch of the MD Series AMRs from Hoffman Estates, IL, which are especially designed to optimize material transport with rugged industrial-grade builds supporting 650kg and 900kg payloads. These robots deliver industry-leading speeds of 2.2 m/sec, up to 10 hours of operation per charge, and ultra-fast 20-minute charging.

In Canada, the autonomous mobile robots market has gained momentum largely due to the presence of logistics providers, cold-storage operators, and manufacturing facilities that are increasingly adopting intelligent mobile fleets to optimize material handling. The country’s market also benefits from the integration of robust, weather-resistant navigation systems and advanced sensor technologies that are capable of handling specialized industrial environments, from automotive assembly lines to food and beverage processing plants. In September 2023, OTTO Motors introduced the OTTO 1200 AMR, which is a compact heavy-duty robot capable of moving payloads up to 1,200 kg in tight spaces with unmatched throughput. The AMR consists of a patented adaptive fieldset technology, and it ensures high-speed maneuverability around people and equipment without compromising safety.

Europe Market Insights

The autonomous mobile robots (AMR) market in Europe is progressing at an extensive phase as the region’s automotive, aerospace, and pharmaceutical sectors are dependent on mobile automation to ensure high-precision material handling within highly complex manufacturing facilities. The region’s growth is closely associated with strict labor welfare regulations, where companies utilize intelligent fleets to relieve human workers from hazardous tasks and repetitive heavy lifting. For instance, in June 2026, Pudu Robotics, in partnership with Robobee, deployed 200 PUDU CC1 cleaning robots across Denner’s Switzerland supermarket network. The rollout is a part of Denner’s modernization agenda, which enhances hygiene standards, thereby reducing the cleaning burden on staff. These robots are proven in pilot trials, operate visibly during shopping hours, and are designed to collaborate with employees rather than replace them.

The country’s highly prominent automotive engineering sector, its pioneer status in Industry 4.0 initiatives, and strict workforce safety regulations are fueling the growth of the Germany autonomous mobile robots market. The country’s market also benefits from extensive focus on standardized frameworks and open communication protocols, which allow diverse robotic fleets from multiple vendors to collaborate smoothly within the same factory ecosystem. In July 2024, Germany launched the Robotics Institute Germany, which was backed by USD 21.6 million in funding from the Federal Ministry of Education and Research. It was led by the Technical University of Munich and supported by DFKI, whereas the consortium unites top universities and research institutions to strengthen Germany’s role in AI-based robotics. Further, the initiative is highly focused on research, talent development, and industry collaboration, positioning Germany as a global leader in intelligent robotics.

The autonomous mobile robots market in the UK is projected for surging growth, accelerated by a post-Brexit restructuring of the national labor market and a massive expansion of regional e-commerce fulfillment hubs. The autonomous mobile robots (AMR) market is also being propelled by the country’s burgeoning manufacturing sectors, particularly in automotive sub-assembly and pharmaceuticals, which are steadily deploying these flexible robotic solutions to achieve greater operational agility. In July 2025, DHL Supply Chain made a total investment of USD 700 million to deploy more than 1,000 additional robots across UK and Ireland operations, thereby supporting growth in e-commerce and life sciences healthcare. This builds on USD 1.15 billion already spent on automation, whereas the rollout includes Boston Dynamics Stretch Robots for container unloading, capable of handling 700 boxes per hour, alongside 750 assisted picking robots from Locus Robotics and 6 River Systems.

Key Autonomous Mobile Robots Market Players:

- ABB Ltd. (Switzerland)

- Omron Corporation (Japan)

- Mobile Industrial Robots (MiR) (Denmark)

- Locus Robotics (U.S.)

- Geekplus Technology Co., Ltd. (China)

- HIKROBOT (China)

- ForwardX Robotics (China)

- Seegrid Corporation (U.S.)

- Fetch Robotics (U.S.)

- Zebra Technologies Corporation (U.S.)

- KUKA AG (Germany)

- Daifuku Co., Ltd. (Japan)

- OTTO Motors (Canada)

- Amazon Robotics (U.S.)

- Aethon Inc. (U.S.)

- SEER Robotics (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ABB Ltd. is one of the most prominent and influential players in the autonomous mobile robots (AMR) market that is leveraging its extensive knowledge in industrial automation, robotics, and digital solutions. The company has efficiently strengthened its AMR portfolio with a higher focus on providing end-to-end automation solutions for manufacturing, warehousing, and logistics facilities.

- Omron Corporation has established itself as a key innovator in the AMR industry owing to the presence of its LD Series and HD Series mobile robots. The company combines autonomous navigation technologies with certain advanced sensing, machine control, and fleet management software, with the main goal of delivering scalable automation solutions.

- Teradyne, Inc. has registered itself as another major dominant force in the autonomous mobile robots (AMR) market. The firm offers a broad range of autonomous material transport solutions that are especially designed for manufacturing, logistics, and distribution environments.

- Mobile Industrial Robots is recognized as a pioneer in collaborative autonomous mobile robots for internal logistics, along with material handling. Besides, the company provides a portfolio of AMRs capable of transporting payloads that range from lightweight components to heavy industrial materials.

- Locus Robotics is a leading provider of warehouse-focused autonomous mobile robots, which is specializing in fulfillment and order-picking automation. The company has gained significant traction among e-commerce, retail, and third-party logistics operators, largely propelled by its robots-as-a-service business model and rapid deployment capabilities.

Here is a list of key players operating in the global autonomous mobile robots (AMR) market:

The global autonomous mobile robots market is witnessing intense competition amongst established automation providers, robotics specialists, and some of the emerging technology firms. Leading players in this sector are highly focused on product innovation, AI-powered navigation, fleet management software, and higher-payload AMR platforms, with a main goal to strengthen their market positions. Strategic initiatives such as mergers and acquisitions, partnerships with logistics and manufacturing companies, and expansion of regional distribution networks have become common in the autonomous mobile robot industry. Companies are also making investments in cloud-based fleet orchestration, autonomous material handling solutions, and interoperability with warehouse management systems. For instance, in November 2023, OMRON announced the launch of new MD-650 and MD-900 AMRs, which expand the lineup with medium payload capacity ranging from 650kg to 900 kg, and they will deliver high-speed transfers, advanced obstacle avoidance, and efficient fleet management.

Corporate Landscape of the Autonomous Mobile Robots Market:

Recent Developments

- In June 2026, OMRON Robotics introduced its next-generation LD Series autonomous mobile robots called the LD-150 and LD-300, and they are designed for high-throughput material transport with higher payload capacities, faster wireless charging, and advanced safety features.

- In March 2026, Hyundai Motor Group announced the launch of the MobED Alliance, which is a collaborative ecosystem designed to accelerate the commercialization of its MobED (Mobile Eccentric Droid) mobile robot platform in Korea. The initiative brings together industry partners, public agencies, and component suppliers to develop industry-specific robotic solutions.

- Report ID: 8613

- Published Date: Jun 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.