Automotive Tinting Film Market Outlook:

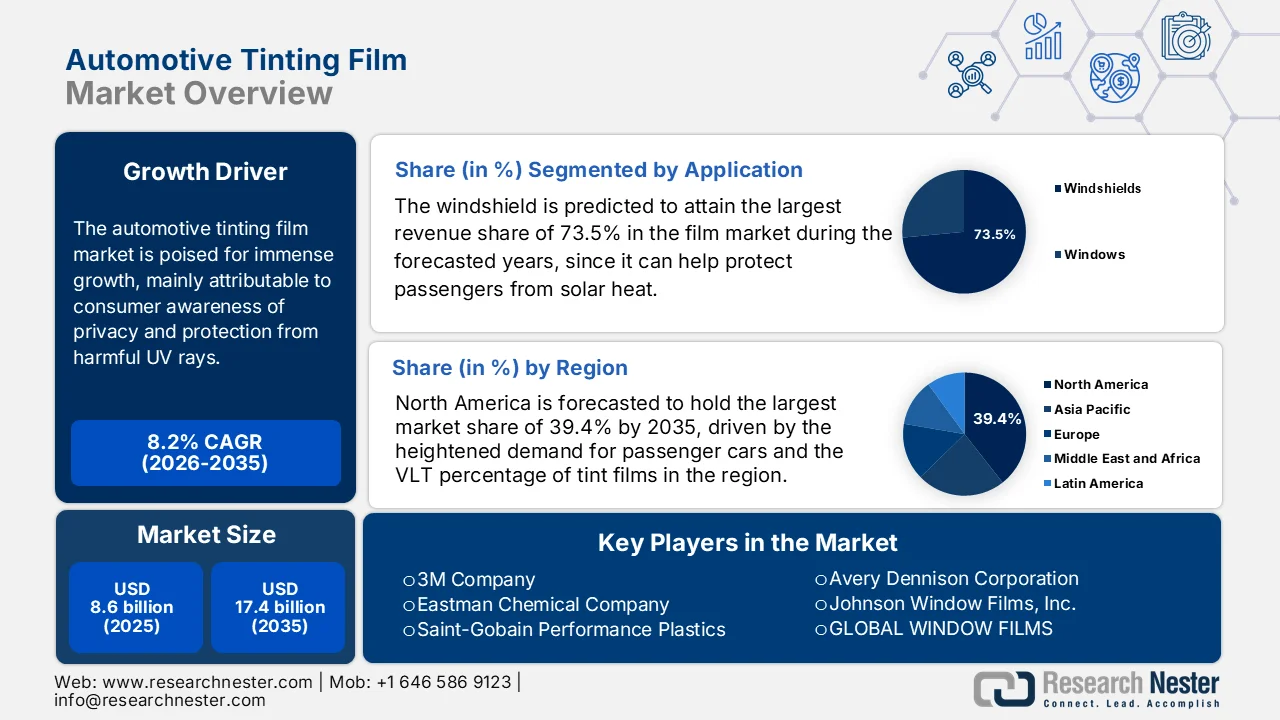

Automotive Tinting Film Market size was valued at USD 8.6 billion in 2025 and is projected to reach USD 17.4 billion by the end of 2035, rising at a CAGR of 8.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of automotive tinting film is evaluated at USD 9.3 billion.

The market is poised for immense growth, mainly attributable to consumer awareness of privacy and protection from harmful UV rays. In addition, the unprecedented growth in the automotive industry directly fuels demand for tinting films, as rising vehicle production and sales expand the customer base for aftermarket and OEM applications. According to the April 2025 PIB reports by NITI Aayog, India’s automotive industry is contributing 7.1% to national GDP and ranking 4th globally in vehicle production, and is rapidly scaling up with over 28 million units manufactured in 2023 to 2024. The country holds 3% share in global traded auto components, which is worth USD 20 billion, denoting an optimistic opportunity for the market’s exposure and expansion.

India Automotive Industry Growth Statistics 2025-2030: GDP, Production, Exports, Jobs & EV Targets

|

Indicator |

Value |

|

Share of Manufacturing GDP |

49% |

|

Global Vehicle Production Rank |

4th |

|

Vehicles Manufactured (2023-24) |

28 million+ |

|

Vision 2030 Target - Production |

USD 145 billion |

|

Vision 2030 Target - Exports |

USD 60 billion |

|

Jobs to be Generated by 2030 |

2 to 2.5 million |

|

Government Schemes Mobilized |

₹66,000+ crore |

|

EV Procurement Targets (PM E-Drive 2024-26) |

24.79 lakh 2-wheelers, 3.2 lakh 3-wheelers, 14,028 buses |

Source: PIB

Furthermore, regulations play a pivotal role in boosting the market as governments set standards on tint levels, safety compliance, and environmental sustainability, which directly influence product design as well as adoption. As stated by the government data in North Dakota, vehicle window tinting laws set clear limits to ensure safety and compliance. The front windshield must allow at least 70% light transmittance, meaning no more than 30% tint, below the AS‑1 line or the top five inches of the glass. Besides, effective from August 1, 2025, all other windows must allow at least 35% light transmittance, with factory tint included in the calculation to ensure total tint does not exceed legal limits. It also stated that rear windows may be fully tinted if the vehicle has outside mirrors on both sides, allowing zero light transmittance. Therefore, from a strategic perspective, such regulations will boost the market growth by driving demand for high-quality tinting films, encouraging innovation in products that meet safety and environmental standards.

Key Automotive Tinting Film Market Insights Summary:

Regional Highlights:

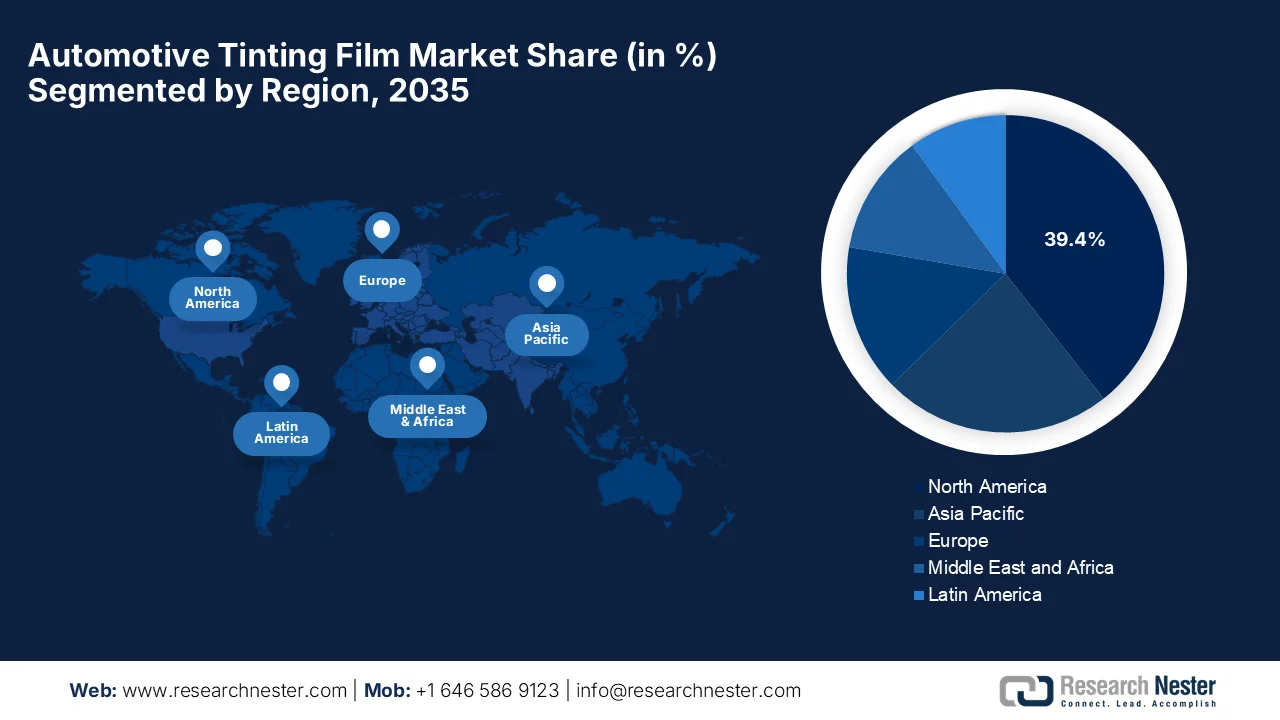

- North America automotive tinting film market is projected to command a 39.4% revenue share by 2035, impelled by heightened demand for passenger cars and evolving visible light transmission standards.

- Asia Pacific is anticipated to witness the fastest growth in the automotive tinting film market during 2026–2035, stimulated by rising security concerns, OEM adoption of tinted glass, and increasing need for heat-reducing and UV-protective films amid hot climatic conditions.

Segment Insights:

- In the automotive tinting film market, the windshield segment is forecasted to capture a dominant 73.5% revenue share by 2035, propelled by increasing integration of films that block solar heat and UV rays while enhancing glare reduction and driving visibility.

- Passenger car within the vehicle type segment is expected to secure a significant revenue share by 2035, driven by growing consumer demand for vehicle customization and rising passenger car production.

Key Growth Trends:

- Rising awareness of UV protection

- Heat reduction & enhanced comfort

Major Challenges:

- Regulatory and legal restrictions

- Technological compatibility and installation challenges

Key Players: 3M Company (U.S.), Eastman Chemical Company (U.S.), Saint‑Gobain Performance Plastics / Solar Gard (U.S.), Avery Dennison Corporation (U.S.), Johnson Window Films, Inc. (U.S.), GLOBAL WINDOW FILMS (U.S.), Madico, Inc. (U.S.), Huper Optik U.S. (U.S.), NEXFIL Co., Ltd. (South Korea), TintFit Window Films Ltd. (Europe), Solar Screen International SA (Switzerland), Hanita Coatings RCA Ltd. (Europe), Sekisui S Lec (Japan), Garware Hi Tech Films Ltd. (India), XPEL, Inc. (U.S.), Wintech Window Film (China), Rayno Window Film (U.S.), American Standard Window Films (U.S.), FilmTack Pte Ltd (Singapore), Al-Rabiya Auto Accessories (UAE), KROPELIN Window Film (Malaysia).

Global Automotive Tinting Film Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 8.6 Billion

- 2026 Market Size: USD 9.3 Billion

- Projected Market Size: USD 17.4 Billion by 2035

- Growth Forecasts: 8.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (39.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: China, India, Japan, South Korea, Singapore

Last updated on : 25 February, 2026

Automotive Tinting Film Market - Growth Drivers and Challenges

Growth Drivers

- Rising awareness of UV protection: The rising awareness about the risk posed by longer exposure to ultraviolet rays in vehicles increases adoption in this field since these tinting films can block the harm-causing UV rays. As of December 2024, data from the Skin Cancer Foundation states that UV window films are effective at protecting skin from the harmful sun exposure, which blocks more than 99% of UVA and UVB rays that can penetrate vehicle windows. It also stated that prolonged exposure to UVA, which passes through most side and rear car windows, contributes to skin aging and increases the risk of skin cancer, as seen in long-term drivers. Therefore, installing UV window film on vehicle windows offers a practical sun protection measure, reducing incidental sun damage and positively impacting the market growth.

- Heat reduction & enhanced comfort: In terms of warmer climates, tint films help reduce cabin temperature by blocking solar heat. This improves passenger comfort and lowers reliance on air conditioning, which is a valuable feature especially in regions with high temperatures. According to the article published by NIH in February 2024, a study in Heliyon observed the parking dilemma for solar-powered vehicles, showing that parking in the sun increases cabin temperatures by up to 76 °C when ambient temperatures reach 41 °C, thereby forcing drivers to use air conditioning and thus reducing vehicle range. This demonstrates that solar heat entering a car directly impacts interior comfort and energy use, denoting a huge growth opportunity for the automotive tinting film market. The study also encourages managing solar gain through strategies such as shading or glazing, which can improve passenger comfort and lower energy demands in hot climates.

- Energy efficiency & environmental consciousness: The automotive films can reduce solar heat gain, can indirectly improve fuel efficiency, i.e., lower AC usage and reduce emissions, thereby aligning with emerging sustainability trends. Improvements through nano‑ceramic and advanced polymer technologies also elevate energy performance, boosting business in the market. In this regard, Hyundai Motor and Kia, in August 2024, together reported that they unveiled their nano cooling film in Seoul, stating that it can lower vehicle interior temperatures by more than 12°C, reducing the need for air-conditioning and improving energy efficiency. It is also stated that this film uses a three-layer nano-material design that blocks solar heat and emits internal heat outward, maintaining transparency and comfort. Therefore, the continued innovations show that these automotive films enhance passenger comfort by also supporting fuel savings and environmental sustainability.

Challenges

- Regulatory and legal restrictions: The automotive tinting films are mostly subject to strict regulatory limits in terms of visible light transmission in most nations. Compliance is considered to be critical since these films are dark and can be illegal for road use, leading to fines or liability in accidents. Therefore, the varying regulations across regions create complexity for manufacturers and installers, who must ensure products meet local legal requirements by efficiently delivering heat rejection and UV protection. Furthermore, any changes in terms of legislation, such as stricter safety standards or visibility requirements, may impact product design, slow automotive tinting film market adoption, and increase costs for testing, creating hesitation among players to operate in this field.

- Technological compatibility and installation challenges: The modern vehicles consist of advanced electronics, sensors, cameras, and electric drivetrains, making metal-based or non-compliant films unsuitable due to potential interference. Therefore, ensuring film compatibility with modern vehicle systems is technically challenging, and it in turn necessitates significant R&D investment. Installation is also a major challenge since achieving a bubble-free, durable, and wrinkle-free application requires skilled labor and precision tools. Meanwhile, the aspect of inconsistent installation quality can result in customer dissatisfaction, film peeling, or damage to windows. In addition, expanding into new regions with different climate conditions and glass types requires specialized formulations, complicating supply chains and thereby limiting scalability for smaller players in the market.

Automotive Tinting Film Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.2% |

|

Base Year Market Size (2025) |

USD 8.6 billion |

|

Forecast Year Market Size (2035) |

USD 17.4 billion |

|

Regional Scope |

|

Automotive Tinting Film Market Segmentation:

Application Segment Analysis

The windshield is predicted to attain the largest revenue share of 73.5% in the automotive tinting film market during the forecasted years. The dominance of the subtype is mainly propelled by factors such as these films help protect passengers from solar heat and harmful UV rays, reduce glare, and ensure clear visibility for safer driving. Most of the automakers incorporate these films to enhance comfort, safety, and the driving experience. In April 2024, Hyundai Motor Company announced that it had launched the world’s first-ever nano cooling film, which is a transparent vehicle window film that is known to reduce interior temperatures by maintaining clear visibility. The film uses a three-layer nanostructure to block incoming solar heat and emit internal heat outward, improving comfort and energy efficiency. Hence, with such continued innovations, the segment is expected to witness exceptional growth in the years ahead.

Vehicle Type Segment Analysis

By the end of the forecast period, passenger car which are a part of the vehicle type segment is expected to garner a significant revenue share in the automotive tinting film market. The growth of the subtype is mainly propelled by growing consumer demand for vehicle customization. Also, the rise in passenger car production drives the market expansion, as a larger vehicle fleet increases the need for heat reduction and enhanced privacy features. According to the article published by FRED in March 2022, India recorded approximately 167,309 passenger car retail registrations, based on seasonally adjusted monthly data. Therefore, this figure highlights the continuing consumer demand for passenger vehicles in one of the world’s largest automotive sectors, which in turn drives growth in protective automotive tints, thereby reflecting the broader scope of the segment.

Installation Channel Segment Analysis

The aftermarket channel is likely to grow with a considerable share in the market during the stipulated timeframe. The segment’s leadership in this field is mainly propelled by consumer customization trends, broader product availability, and more flexible product choices when compared to OEM installation. This channel’s revenue is also fueled by growing installation networks and consumer demand for retrofit solutions. The aspects of regional differences in climate and sunlight intensity also encourage consumers to seek aftermarket solutions that are suitable for local conditions. In addition, the channel allows easier replacement and upgrades as films age or technologies improve. Therefore, some insurance providers and fleet operators actively recommend aftermarket tinting to enhance vehicle comfort and safety, thereby boosting adoption in the segment. Moreover, improvements in tinting technologies are making aftermarket options more attractive to tech-savvy consumers across the world.

Our in-depth analysis of the automotive tinting film market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Vehicle Type |

|

|

Installation Channel |

|

|

Film Type |

|

|

Purpose |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Tinting Film Market - Regional Analysis

North America Market Insights

The North America automotive tinting film market is projected to expand with the largest revenue share of 39.4% by the end of 2035. The growth of the region is highly driven by the heightened demand for passenger cars and the visible light transmission (VLT) percentage of tint films. The technological improvements, coupled with a priority for luxurious tints, also propels expansion of the region’s market. According to the government reports published in January 2026, in Washington State, the legal visible light transmission limits for vehicle window tinting vary by vehicle type and window position. For standard passenger cars, front and rear side windows as well as the rear windshield must allow at least 24% of visible light (≥24% VLT), whereas the front windshield may only have a non-reflective tinted strip at the top six inches. SUVs, trucks, and vans are allowed darker tints on rear windows with no minimum VLT, provided dual side mirrors are installed, and all vehicles must comply with a maximum 35% reflectivity limit and restrictions on certain colors, hence increasing the growth potential for the market.

The extensive road infrastructure, coupled with higher per capita income have resulted in rising automobile ownership, driving growth in the U.S. automotive tinting film market. The country is considered to be the leading revenue contributor for the regional market, owing to the increasing consumer interest in vehicle customization and personalization, which has boosted demand for tinting films. According to the official statistics published by FHWA in 2023, the total number of registered motor vehicles in the U.S. surpassed a value of approximately 284.6 million, reflecting the vast scale of the country’s automotive fleet. Therefore, this extensive vehicle base supports strong demand for aftermarket products such as automotive tinting films, based on factors such as vehicle maintenance and personalization, hence making it suitable for standard market growth in the upcoming years.

2023 U.S. Motor Vehicle Registrations by Category: Official Federal Highway Administration Data

|

Vehicle Category |

Registered Vehicles (2023) |

|

Light Duty Vehicles (Short WB) |

141,502,000 |

|

Motorcycles |

1,014,000 |

|

Buses |

1,576,000 |

|

Light Duty Vehicles (Long WB) |

53,228,000 |

|

Single-Unit Trucks |

11,957,000 |

|

Combination Trucks |

59,441,000 |

Source: FHWA

The rising consumer focus on thermal efficiency and tinting regulations in electric vehicles is the main factor responsible for uplifting Canada automotive tinting film market. This growth is also supported by the high volume of SUVs and light trucks, along with a growing network of professional installation services. As stated by BC Laws in December 2025 under the Motor Vehicle Act regulations (B.C. Reg. 235/2025), vehicles in British Columbia need to comply with strict equipment and safety standards. It states that windshields and windows cannot have materials that reduce light transmission beyond specified limits, and tinting is only allowed up to 75 mm from the top of the windshield, on side windows behind the driver, or on rear windows if dual exterior mirrors are installed. Further, all manufactured glass with integrated tint must meet minimum light transmittance standards under the country’s Motor Vehicle Safety Standards, ensuring legal visibility and road safety.

APAC Market Insights

Asia Pacific automotive tinting film market is anticipated to register the fastest growth from 2026 to 2035. The region’s growth in this field is highly driven by demand for security, which is driving popularity in emerging markets, whereas OEM adoption of tinted glass also supports market growth. In addition, the region’s hot climate with strong sunlight fuels the need for heat-reducing and UV-protective films. In this context, based on the government data from Hong Kong, its Transport Department revised vehicle glass requirements under Regulation 28 of the Cap. 374A, in April 2023, by setting minimum light transmission rates of 70% for front windscreen or driver compartment windows and 44% for other windows, which includes bus upper decks. It also notes that reflective films are generally prohibited, but vehicle owners can apply for an exemption to install non-reflective solar films as long as the LTR standards are maintained.

The booming automotive industry and strong consumer demand, a rise in passenger car sales, are certain drivers that are responsible for boosting the market in China. The vehicle production capabilities, coupled with government policies which are energy efficiency and reduced vehicle emissions, also encourage the adoption of automotive tinting films. According to the official statistics published by MIIT in January 2026, the country’s automobile production and sales reached 34.531 million and 34.4 million units in 2025, with new energy vehicles accounting for 16.626 million produced and 16.49 million sold, representing year-on-year increases of 29% and 28.2, and making up nearly 48% of total vehicle sales. Besides, the passenger vehicle production and sales also grew by over 10%, whereas commercial vehicle sales rose about 11% year-on-year, hence denoting a lucrative growth opportunity for the overall market in the country.

The intensifying tropical climate, coupled with the rising consumer preference for heat-rejection technologies are major fueling factor for the automotive tinting film market in India. The surging temperatures in the country are creating encouraging opportunities for pioneers offering nano ceramic films that enhance passenger comfort by offering superior heat reduction for vehicles. In this regard, the Indian Meteorological Department (IMD) in March 2024 published its annual climate summary 2023, observing that the annual mean land surface air temperature over the country was +0.65°C above the long-term average from previous decades. Besides, the year 2023 ranked as the second-warmest year when compared to previous years, which reflects elevated temperatures in the country. Therefore, this denotes that there is a huge need for improved heat-control solutions in vehicles, thereby supporting sustained growth in demand for automotive tinting films across India.

Europe Market Insights

The Europe automotive tinting film market is poised for extensive growth over the forecasted years. The region’s prominence in this field is majorly fueled by stringent regulations related to vehicle safety and energy efficiency, which are encouraging manufacturers to adopt tinting films that comply with regulatory standards while enhancing overall vehicle efficiency. As stated by the European Commission in December 2025, its automotive package sets a strong policy framework to support clean and competitive mobility. It properly reviews CO₂ emission standards for cars, vans, and heavy-duty vehicles, and introduces binding national targets for corporate fleets to adopt zero- and low-emission vehicles. Furthermore, by cutting red tape and simplifying rules, the package enhances efficiency and competitiveness while ensuring that safety is central to Europe’s automotive transition.

The strict technical and safety compliance standards, where films must carry certified markings and be professionally installed with documented approvals, are certain factors that are responsible for boosting the market in Germany. Therefore, this emphasis is on certified demand for advanced products that meet rigorous national and EU safety requirements. In April 2024, the Kraftfahrt-Bundesamt issued the Allgemeine Bauartgenehmigung certificate to BRITAX RÖMER Kindersicherheit GmbH for its EZ-cling window shades, approving the film for use on vehicle windows under §22a StVZO and the Fahrzeugteileverordnung. The approval requires the product to carry the KBA mark, be installed according to supplied instructions, and comply with specific safety limitations, such as single-sided application and rear-window mirror requirements, hence suitable for bolstering market growth.

The dynamic consumer landscape, which values both innovation and regulatory alignment, fuels the expansion and exposure of the market in the UK. Manufacturers and aftermarket providers in the country are responding to this with their continued innovations, aligning with evolving preferences for reliable and high-performance glass films. In this regard, in June 2025, 3M announced its plan for a new 15,250 sq ft training and skills development centre at Mira Tech Park, Warwickshire, which is mainly aimed at upskilling technicians in automotive refinish and industrial sectors. This facility will provide hands-on training in advanced automotive processes to meet the evolving consumer and industry demands for reliable, compliant automotive solutions. Therefore, from a strategic perspective, such steps from pioneers will elevate the market potential by enhancing the skillset of installers and fostering the adoption of advanced, quality tinting films.

Key Automotive Tinting Film Market Players:

- 3M Company (U.S.)

- Eastman Chemical Company (U.S.)

- Saint‑Gobain Performance Plastics / Solar Gard (U.S.)

- Avery Dennison Corporation (U.S.)

- Johnson Window Films, Inc. (U.S.)

- GLOBAL WINDOW FILMS (U.S.)

- Madico, Inc. (U.S.)

- Huper Optik U.S. (U.S.)

- NEXFIL Co., Ltd. (South Korea)

- TintFit Window Films Ltd. (Europe)

- Solar Screen International SA (Switzerland)

- Hanita Coatings RCA Ltd. (Europe)

- Sekisui S‑Lec (Japan)

- Garware Hi‑Tech Films Ltd. (India)

- XPEL, Inc. (U.S.)

- Wintech Window Film (China)

- Rayno Window Film (U.S.)

- American Standard Window Films (U.S.)

- FilmTack Pte Ltd (Singapore)

- Al-Rabiya Auto Accessories (UAE)

- KROPELIN Window Film (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- 3M Company benefits from a vast portfolio of ceramic, dyed, and reflective films under its 3M Window Film brand. The company is best known for its strong focus on R&D and innovation, and it has developed improved technologies that provide high heat rejection and UV protection without compromising visibility.

- Eastman Chemical Company is a major player in this field, which offers specialty films and coatings that are popular for their heat rejection, glare reduction, and durability. The company is mainly focused on technological differentiation, offering premium ceramic and carbon-based films that are suitable for modern vehicles and EVs.

- Avery Dennison Corporation is yet another prominent player that is best known for metal-free construction, nanotechnology, and superior UV/IR rejection products. Franchise training programs, international distribution, and partnerships with OEMs and aftermarket networks are the tactical strategies opted for by Avery that enable it to maintain its leading position in this sector.

- Solar Gard, which is a part of Saint‑Gobain Performance Plastics, specializes in terms of automotive and architectural window films, and it offers high-performance ceramic, carbon, and reflective films. The company’s strategy is mainly focused on innovation, durability, and compatibility with modern electronics, including EVs.

- Johnson Window Films, Inc. is a leading independent manufacturer of automotive and architectural films, which is well recognized for premium dyed, ceramic, and carbon products. The company highly concentrates on installer education, technical innovation, and aftermarket support.

Below is the list of some prominent players operating in the global automotive tinting film market:

The global automotive tinting film market hosts both internationally operating manufacturers and regional players having presence in North America, Europe, the Asia Pacific, and the Middle East. Major pioneers such as 3M, Eastman, and Solar Gard lead the market through technology innovation, extensive R&D, and international distribution networks, particularly in terms of advanced ceramic and nano‑film technologies. Meanwhile, the other players from India and South Korea are strengthening their presence, mainly focusing on regional partnerships and expanded manufacturing capacity to capture specific industrial segments. In October 2025, Tint World Automotive Styling Centers announced an investment from Susquehanna Growth Equity, which marks its first institutional capital to enhance operations, accelerate franchise development, and strengthen its global aftermarket position, hence positively impacting market growth.

Corporate Landscape of the Automotive Tinting Film Market:

Recent Developments

- In May 2025, Al-Rabiya Auto Accessories reported that it had launched the luminous carbon automotive window film across the Middle East, which is a durable, high-performance alternative to traditional films.

- In February 2025, Avery Dennison introduced the Encore automotive window films portfolio, which includes a three-tier lineup, i.e., Encore, Encore Supreme, and Encore Supreme IR, that are incorporated with dye-free nanotechnology to resist fading and enhance performance.

- Report ID: 4510

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Automotive Tinting Film Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.