Aortic Stenosis Treatment Market - Regional Analysis

North America Market Insights

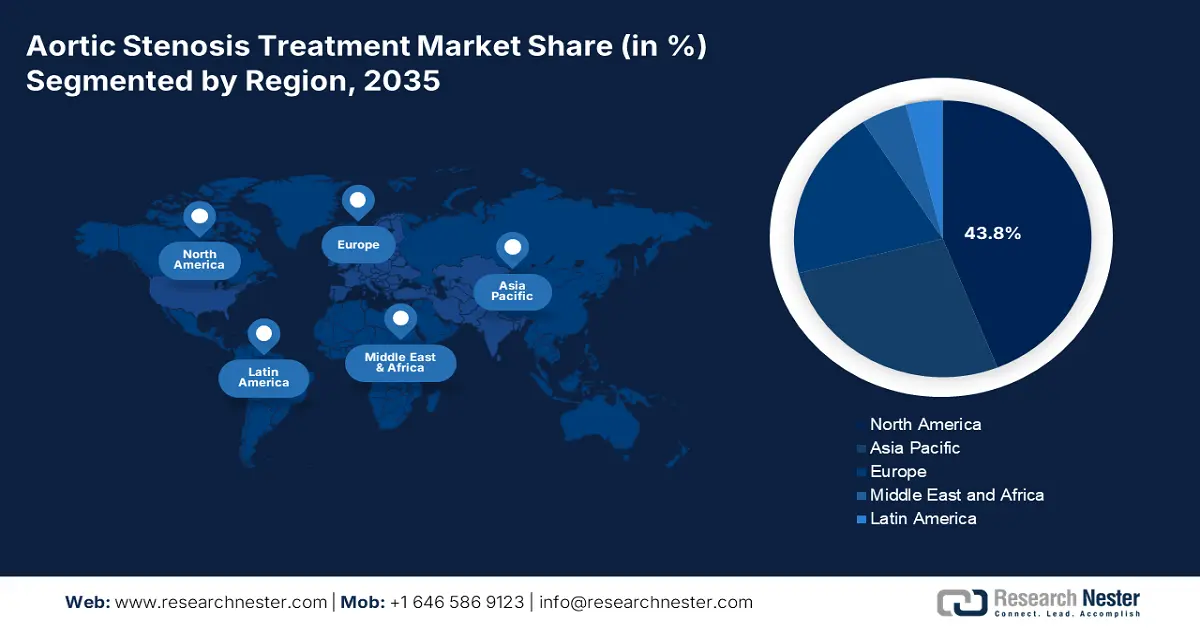

The aortic stenosis treatment market in North America dominates the market and is expected to hold the market share of 43.8% at a CAGR of 8.5% by 2035. The market growth is driven by the widespread adoption of Transcatheter Aortic Valve Replacement (TAVR) and expanding insurance reimbursements. The U.S. and Canada together dominates the market position and hold significant revenue. The growth can be attributed to the strong government healthcare spending, supportive regulatory environments, and extensive hospital infrastructure. Increase in aging population, rising valvular disease incidence, and a mature medtech industry pipeline will drive increasing treatment volumes and the need for new surgical and non-surgical treatments.

The U.S. aortic stenosis treatment market is growing steadily with rising elderly populations and robust institutional backing from federal medical programs. The CMS has increased reimbursement coverage of TAVR for patients with intermediate and low risk, resulting in wider availability across public hospitals. Increased life expectancy, enhanced device security, and national investment in managing heart disease through the U.S. Department of Health & Human Services (HHS) make the treatment market one of the most valued cardiovascular segments.

Asia Pacific Market Insights

The Asia-Pacific is the fastest-growing aortic stenosis treatment market and is poised to hold the market share of 17.8% at a CAGR of 9.9% by 2035. The market is driven by growing elderly populations, enhanced awareness, and government spending on cardiovascular treatment. Major players are Japan, China, India, South Korea, and Malaysia, with increasing demand for Transcatheter Aortic Valve Replacement (TAVR) due to its minimally invasive nature and adaptability to age cohorts. Also, the development of cardiac care facilities in India and China's secondary cities is making it possible to access diagnostic and interventional procedures on a wider scale.

China holds the largest share in the aortic stenosis treatment market in the APAC region and is anticipated to hold the market share. Moreover, the National Health Commission of China has given priority to structural heart disease under its 14th Five-Year Plan, further increasing financing for TAVR training and facilities. Also, the rapidly aging population of the country has a larger pool of patients. For instance, Beijing has made its priority for elder care and health services with the help of the “silver economy”.

Europe Market Insights

The aortic stenosis treatment market in Europe is set for strong growth and is expected to hold a significant market share by 2034. The market is driven by a mix of supportive reimbursement policies, sophisticated healthcare infrastructure, and growing acceptance of minimally invasive therapies such as TAVR. Aging populations are driving demand, especially in nations with well-developed public healthcare systems such as Germany, France, and the UK. European markets are further supported by cross-border collaborative funding through the EU4Health and European Health Data Space (EHDS) programs.

Germany is the highest shareholder in the aortic stenosis treatment market and is expected to retain its market share. The market is driven by sophisticated tertiary care networks and a rising elderly population. The government has robust reimbursement frameworks under GKV statutory health insurance, including TAVR patients. Strategic position as a med-tech manufacturing base strengthens Germany's access to next-generation valves, increasing local and EU-wide supply. According to the German Federal Bureau of Statistics, between 2011 and 2022, 336,879 aortic valve procedures were performed even in patients of age below 40 years.