Anti-Drone Market Outlook:

Anti-Drone Market was valued at USD 3.5 billion in 2025 and is expected to reach USD 18.7 billion by 2035, reflecting a CAGR of 20.5% over the forecast period from 2026 to 2035. In 2026, the industry size of anti-drone is estimated at USD 4.2 billion.

The anti-drone market is poised for tremendous growth in the coming years as expanding commercial drone usage is driving the need for responsible airspace monitoring and management systems. Rising concerns over security threats to airports, military bases, public events, and energy facilities are encouraging the adoption of advanced detection and mitigation technologies. According to the official statistics that were kept forward by the U.S. Government Accountability Office (GAO) in March 2024, the number of unmanned aircraft systems in the U.S. is increasing, wherein the Federal Aviation Administration (FAA) forecasts that the commercial drone fleet will grow from about 727,000 in 2022 to 955,000 by 2027. This expansion has resulted in safety and security concerns around airports. According to the Transportation Security Administration (TSA), more than 2,000 drone sightings have been reported near U.S. airports since 2021, which also includes 63 incidents between 2021 and 2022 where pilots took evasive action, highlighting operational risks to aviation safety.

Furthermore, growth in the anti-drone market is stimulated by governments, defense organizations, and critical infrastructure operators that are prioritizing protection against unauthorized or hostile unmanned aerial vehicles (UAVs). Industry collaboration and growing awareness of drone-related risks are expected to support the continued expansion of the anti-drone market globally. In November 2025, the Department of Homeland Security’s Counter-Unmanned Aircraft Systems (C-UAS) Grant Program, which is administered by FEMA, allocates a total of USD 500 million to strengthen state and local capabilities in detecting, identifying, tracking, and mitigating unlawful drone activity. It also stated that for fiscal year 2026, USD 250 million is prioritized for 11 states hosting FIFA World Cup events and the National Capital Region during America 250 celebrations, both designated as SEAR 1 or 2 events. The remaining USD 250 million will be distributed in the financial year 2027 across all 56 states and territories with a prime focus on expanding national detection and response capacity.

Key Anti-drone Market Insights Summary:

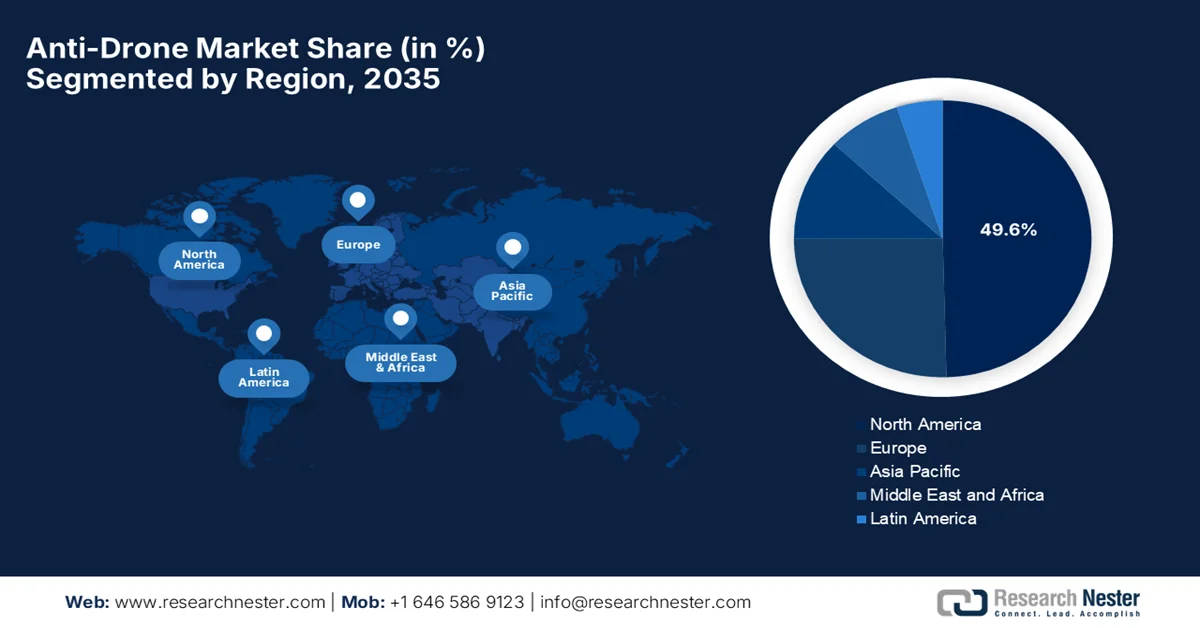

Regional Highlights:

- North America is projected to command a 49.6% share of the anti-drone market by 2035, supported by expanding defense budgets and advanced multi-sensor counter-UAS deployments across critical infrastructure accelerated by rising drone threats to energy assets.

- Asia Pacific is expected to witness the fastest expansion in the forecast period 2026–2035, encouraged by increasing government initiatives and adoption of advanced drone detection and mitigation technologies for infrastructure security stimulated by strengthened regulatory frameworks and defense modernization programs.

Segment Insights:

- The RF jammer segment in the anti-drone market is projected to secure a 60.5% revenue share by 2035, supported by its operational reliability and widespread deployment in defense systems impelled by the need to disrupt hostile drone communication links.

- The ground-based segment is anticipated to hold a considerable share in the forecast period 2026–2035, strengthened by increasing deployment of stationary counter-drone defense systems for critical infrastructure and military installations propelled by rising investments in fixed security infrastructure.

Key Growth Trends:

- Increasing military budgets

- Growth of recreational drones

Major Challenges:

- Regulatory and legal concerns

- Cybersecurity and system vulnerabilities

Key Players: RTX Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, Dedrone Holdings Inc., WhiteFox Defense Technologies, Inc., Fortem Technologies, Inc., The Boeing Company, Thales Group, Leonardo S.p.A., Saab AB, Rheinmetall AG, DroneShield Ltd., QinetiQ Group PLC, ELTA Systems Ltd., Sentrycs Ltd., Zen Technologies Ltd., Indrajaal Pvt. Ltd., Paras ANTI-Drone Technologies Pvt. Ltd., LIG Nex1 Co., Ltd., Rohde & Schwarz GmbH & Co. KG, Ondas Inc., Airbus Helicopters, Volatus Aerospace

Global Anti-drone Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.5 billion

- 2026 Market Size: USD 4.2 billion

- Projected Market Size: USD 18.7 billion by 2035

- Growth Forecasts: 20.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (49.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, India, United Kingdom, Israel

- Emerging Countries: Japan, South Korea, Australia, Germany, France

Last updated on : 11 March, 2026

Anti-Drone Market - Growth Drivers and Challenges

Growth Drivers

- Increasing military budgets: Countries across the globe are increasing their military spending in order to protect borders and strategic assets, and this is the main factor driving investments in counter-UAV technologies. According to the official statistics, which were reported by the Stockholm International Peace Research Institute in April 2025, global military expenditure reached a significant value of USD 2,718 billion in 2024, which marks a 9.4% year-on-year increase. It also notes that the military spending has grown continuously for 10 years, increasing 37% between 2015 and 2024, wherein the global military burden reached 2.5% of world GDP. The rise was driven by heightened geopolitical tensions, particularly conflicts such as the Russia–Ukraine war and conflicts in the Middle East, which can lead many countries to further increase defense budgets, thus benefiting the overall anti-drone market.

Global Military Expenditure 2024: Top Spenders, Regional Trends, and NATO Spending Insights

|

Key Fact |

Value |

|

Top 5 military spenders |

U.S., China, Russia, Germany, India (60% of world spending) |

|

U.S. military spending |

USD 997 billion |

|

China military spending |

USD 314 billion |

|

Russia's military spending |

USD 149 billion (↑ 38%), 7.1% of GDP |

|

Ukraine's military spending |

USD 64.7 billion (↑ 2.9%), 34% of GDP, 8th largest spender |

|

Total military spending in Europe |

USD 693 billion (↑ 17%), all countries ↑ except Malta |

|

NATO's total spending |

USD 1,506 billion (55% of global), European NATO: USD 454 billion |

|

NATO members ≥2% GDP on military |

18 members (up from 11 in 2023) |

Source: SIPRI

- Growth of recreational drones: The number of drones that are used in agriculture, logistics, photography, surveillance, and construction is growing at a rapid pace. This increases the risk of airspace violations and privacy breaches, encouraging organizations to adopt anti-drone solutions. In February 2026 Press Information Bureau (PIB) reported that India has built a regulated drone ecosystem that hosts more than 38,500 registered drones and 39,890 DGCA-certified remote pilots, thereby supporting applications across agriculture, infrastructure, disaster management, railways, and defense. Government initiatives such as the SVAMITVA Scheme and Namo Drone Didi have leveraged drones for land surveys, crop management, and women’s SHG empowerment, whereas the policies such as the Drone Rules 2021 and subsequent amendments have simplified regulations, expanded commercial operations, and enabled widespread adoption, hence denoting a huge growth potential for the anti-drone market.

- Increasing R&D and industry collaboration: Defense companies and tech firms are collaborating to develop next-generation counter-drone systems. Besides the investments in AI, machine learning, and sensor fusion technologies are accelerating the anti-drone market growth. In March 2025, Raytheon, which is an RTX business, reported that it had received a follow-on contract from the U.S. Army Futures Command to advance its Rapid Campaign Analysis and Demonstration Environment (RCADE) for large-scale modeling and simulation of multi-domain operations. The company also stated that this partnership enables continuous experimentation, allowing the Army to integrate real-world threats with AI-based analysis to inform strategic force design and decision-making, hence positively impacting anti-drone market growth.

Challenges

- Regulatory and legal concerns: The anti-drone market needs to navigate through highly complex regulatory and legal hurdles, which are influenced by the restrictions on counter-UAS operations in civilian airspace. Most of the countries have strict laws governing the use of jamming and drone neutralization technologies, as these can interfere with communications and public safety. In this context, obtaining approvals for deployment requires lengthy government certification processes, particularly in the case of airports, urban areas, and critical infrastructure sites. Therefore, companies operating in this field need to ensure compliance with local, national, and international airspace laws while also maintaining operational effectiveness. Hence, these legal complexities can delay product deployment, increase compliance costs, and cause restrictions on anti-drone market expansion.

- Cybersecurity and system vulnerabilities: Counter-UAS systems are networked and AI-based, which makes them highly sensitive to cyberattacks, hacking, and spoofing. If adversaries compromise detection and tracking capabilities, drones could bypass defenses or hijack counter-drone systems, which in turn creates operational risks in the anti-drone market. The integration of cloud-based analytics, command-and-control software, and autonomous platforms represents additional attack vectors. Ensuring robust cybersecurity protocols, encryption, and resilience against electronic countermeasures is a continuous challenge that is restricting growth in this sector. Companies need to make investments in threat modeling, penetration testing, and real-time monitoring to maintain system integrity.

Anti-Drone Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

20.5% |

|

Base Year Market Size (2025) |

USD 3.5 billion |

|

Forecast Year Market Size (2035) |

USD 18.7 billion |

|

Regional Scope |

|

Anti-Drone Market Segmentation:

Technology Segment Analysis

The RF jammer is expected to be the dominant segment, capturing 60.5% of revenue share in the anti-drone market over the forecast period. These RF jammers work by disrupting the communication channels between a hostile drone and its operator, including video feeds, telemetry, command, control, and navigation systems, effectively forcing the drone to return home or grounding it in place. Its reliability, simplicity, and effectiveness have made it the most dominating and widely adopted counter-drone technology among military and security users. In February 2025, Adani Defence & Aerospace, in collaboration with DRDO, reported that it had unveiled India’s vehicle-mounted counter-drone system, which is a public-private initiative under the DRDO Transfer of Technology framework. The system integrates high-energy lasers, jammers, radar, electro-optical sensors, and a 7.62 mm gun on a mobile 4×4 platform for real-time detection, tracking, and neutralization of drones up to 10 km.

Platform Segment Analysis

In the platform segment, the ground-based segment will grow at a considerable share in the anti-drone market during the discussed timeframe. The segment’s growth is mainly propelled by rising investments in stationary defense systems for critical infrastructure and military installations. Their scalability and effectiveness in large-area coverage underscore the segment’s strong growth in the upcoming years. In this regard, Zen Technologies Limited, in June 2024, reported that it had delivered its Hard-Kill Anti-Drone System (Zen ADS HK) to the Army Air Defence College in Odisha, thereby enhancing India’s defense capabilities against drone threats. It also stated that the system integrates an Electro-Optical Tracking System, Laser Range Finder, and automatic gun platform compatibility, providing all-weather, accurate drone neutralization. Hence, with such continued developments, the segment is gaining increased exposure in defense solutions.

End use Segment Analysis

Based on end use segment, the government and defense subsegment is predicted to grow at a significant rate in the anti-drone market by the end of 2035. The rising defense budgets and increasing investment in modernizing military capabilities are the major influential factors behind the subtype’s leadership. The rising threats from unmanned aerial systems have underscored the need for drone defense technologies, in turn encouraging governments to procure or develop robust solutions. Besides the conflicts such as the Russia-Ukraine war, which indicate the importance and effectiveness of counter-drone systems in modern warfare, allowing more countries to integrate these technologies into their defense infrastructure. Furthermore, this trend, combined with an extended focus on safeguarding critical assets, positions the government and defense segment as the forefront of growth, with strong adoption expected across both developed and emerging economies.

Our in-depth analysis of the anti-drone market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Platform |

|

|

End use |

|

|

Method |

|

|

System Type |

|

|

Component Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Anti-Drone Market - Regional Analysis

North America Market Insights

North America is expected to be the largest regional market with a share of 49.6% by the end of 2035. The anti-drone market in North America is extensively supported by the rising defense spending, advanced counter-drone deployments at airports and critical infrastructure, and continued adoption of multi-sensor AI-enabled systems. As stated by Fortem Technologies in December 2025, it has entered into a partnership with Southern States LLC to enhance the protection of the U.S. power grid against drone threats by integrating Fortem’s TrueView radar, SkyDome software, and DroneHunter interceptors into Southern States’ Airspace Awareness product line. Besides, this collaboration equips utilities with advanced, AI-based solutions to detect, track, and neutralize unauthorized drones by targeting critical grid infrastructure. Therefore, rising drone threats to energy assets denote there is a huge growth opportunity for the region’s anti-drone market.

The U.S. anti-drone market has a stronger growth potential facilitated by the technological evolution, fueled primarily by escalating national security concerns and a surge in unauthorized aerial activity near sensitive sites. The country’s landscape is reshaped by burgeoning government investment in defense and homeland security, focusing mainly on systems that utilize electronic disruption, kinetic interception, and laser precision. In February 2026, the U.S. Department of War reported that Joint Interagency Task Force 401, which was established to rapidly deliver counter-UAS capabilities, marked six months of significant progress by accelerating system deployments and clarifying policies to protect critical military sites from drone threats. It also underscored that this task force enhanced homeland defense through scalable solutions, centralized procurement, and coordination with law enforcement for grants supporting major events such as the 2026 FIFA World Cup.

FY2025 U.S. Defense Budget Allocations for Counter-Unmanned Aircraft Systems (Counter-UAS) Programs

|

Account |

Line |

Line-Item Title |

DOD Request (USD million) |

House-Passed H.R. 8070 (USD million) |

SASC-Reported S. 4638 (USD million) |

Enacted Legislation P.L. 118-159 (USD million) |

|

Missile Procurement, Army |

010 |

Counter Small Unmanned Aircraft Systems Intercept |

117.4 |

314.8 |

202.2 |

302.3 |

|

Other Procurement, Army |

078 |

Counter Small Unmanned Aircraft Systems |

280.1 |

445.5 |

345.6 |

280.1 |

|

Procurement, Marine Corps |

010 |

Ground-Based Air Defense |

369.3 |

333.3 |

369.3 |

364.3 |

|

Research, Development, Test & Evaluation, Army |

078 |

Maneuver-Short Range Air Defense |

315.8 |

253.2 |

315.8 |

284.5 |

|

Research, Development, Test & Evaluation, Army |

088 |

Counter Small Unmanned Aircraft System Advanced Development |

60 |

64.5 |

80 |

80 |

|

Research, Development, Test & Evaluation, Army |

155 |

Counter-Small Unmanned Aircraft Systems Sys Dev & Demonstration |

59.6 |

59.6 |

64.1 |

64.1 |

|

Research, Development, Test & Evaluation, Navy |

205 |

Marine Corps Air Defense Weapon Systems |

74.1 |

88.2 |

74.1 |

88.5 |

Source: Congress.gov

Strong government backing and a more flexible regulatory environment for legitimate drone operations are responsible for uplifting the anti-drone market in Canada. The defense sector in the country has accelerated the acquisition of counter-UAS systems to support international commitments and protect overseas personnel. As of July 2025, Canada’s IDEaS program under the Department of National Defence and Canadian Armed Forces allocated funds for innovative Counter Uncrewed Aerial Systems projects to detect and defeat micro and mini drones, with an initial 9-month funding of up to USD 375,000 and potential follow-on support up to USD 1,500,000 for promising concepts. The 2024 round included initiatives such as Lockheed Martin Canada’s Defensive Autonomous Swarm Hunt, TensorOne’s Drone Against Drone Interceptor, and Queen’s University’s ACID-DL system to support scalable, AI-enabled, and laser-based solutions that integrate into broader military command and control systems.

APAC Market Insights

The anti-drone market in the Asia Pacific is expected to register the fastest growth from 2026 to 2035. The region’s pace of progress in this sector is highly influenced by governments and private sectors that are adopting advanced detection and mitigation technologies to safeguard critical infrastructure and urban areas from unauthorized drone activities. In January 2026 government of Australia reported that it strengthened the country’s counter-drone capabilities by enacting the Defence Amendment Regulations 2025, thereby empowering the ADF and law enforcement to detect, disable, or destroy threatening drones. It also stated that an industry advisory panel and the Defence Project Land 156 Standing Offer Panel were established to accelerate the development and deployment of CsUAS technologies, thereby enhancing the protection of critical infrastructure and national security. Hence, these initiatives reflect a push to incorporate advanced counter-drone solutions across defense and government operations.

An emphasis on indigenous technological innovation is responsible for fueling the anti-drone market in China. The country’s government has been putting constant efforts into developing smart cities with enhanced security frameworks, which also led to increased deployment of automated drone detection and neutralization solutions. Based on the government data, which was published in September 2025, China showcased its anti-unmanned aerial vehicle systems during the V-Day military parade in Beijing, consisting of an integrated anti-UAV missile-gun system, high-energy laser weapons, and high-power microwave weapons. In addition, this demonstration highlighted the People’s Liberation Army’s advanced, state-driven counter-drone capabilities and their prominent role in modernizing national defense, hence contributing to wider anti-drone market expansion.

There is a huge opportunity for India anti-drone market, which benefits from a surge in public-private partnerships focused on developing homegrown counter-UAS technologies. The government’s push for self-reliance in defense manufacturing and the rising awareness of drone threats in sensitive border regions readily accelerate the adoption of mobile and vehicle-mounted anti-drone platforms. According to the article published by PIB in May 2025, Operation SINDOOR underscores the country’s technological self-reliance in national security by combining indigenous drones, counter-UAS systems, and advanced air defense networks with the main goal to neutralize cross-border threats with precision. Besides, the operation demonstrated proper integration of legacy and modern platforms, electronic warfare, and satellite support, by ensuring minimal impact on civilian and military infrastructure, hence making it suitable for standard anti-drone market growth.

India Defence & Drone Sector: Official Government Data, Production, Exports & Strategic Growth (2023-2029)

|

Metric |

Value (USD) |

Notes |

|

Indian Drone Market Projection |

11 billion |

By 2030 |

|

Share of Global Drone Market |

12.2% |

By 2030 |

|

Defence Exports FY 2024-25 |

2.83 billion |

34-fold increase since 2013-14 |

|

Indigenous Defence Production FY 2023-24 |

15.24 billion |

Record domestic production |

|

Target Defence Exports by 2029 |

6 billion |

Part of the Make in India initiative |

|

Target Defence Production by 2029 |

36 billion |

Focus on self-reliance |

Source: PIB

Europe Market Insights

The anti-drone market in Europe is growing significantly by attaining the second-largest revenue share during the forecast period. The region’s growth is majorly fueled by strong regulatory support and the establishment of standardized frameworks for drone usage and countermeasures. Collaborative initiatives among member states promote information sharing and joint development of interoperable counter-UAS technologies soldifying the continent’s ability to protect critical infrastructure effectively. In this context, Ondas Holdings in December 2025 stated that it had secured a second USD 8.2 million counter-UAS order from a major Europe based security authority to deploy Iron Drone Raider systems at another international airport, thereby expanding its footprint in critical infrastructure protection. The autonomous system, which is integrated by Airobotics, provides real-time detection, assessment, and neutralization of drone threats through a multi-layered architecture combining kinetic, cyber, and sensing capabilities.

The priority towards the advancement of multi-sensor fusion technologies and cyber-defense integration efficiently fuels the anti-drone market in Germany. The country’s market is reshaped by the booming domestic defense industry, wherein companies such as Rheinmetall AG and Hensoldt AG are leading in terms of the development of advanced electronic sensors and integrated radar systems. This expansion is supported by substantial government investment and participation in international defense collaborations, particularly within the framework of NATO modernization programs. In February 2026, the federal government reported that Germany Bundestag passed amendments to the Aviation Security Act with the main goal of strengthening drone defence, allowing the armed forces expanded powers to assist police in countering unlawful drone activity. It also states that the reforms simplify and accelerate decision-making for deploying military support, transferring authority to the Federal Ministry of Defence.

The increasing investments in research and development underscore the anti-drone market’s growth in the UK. The country’s government supports innovative solutions by combining electronic warfare and kinetic interception to address drone misuse in urban environments. In addition, the heightened security measures for major public gatherings and transport hubs drive demand for versatile and scalable counter-UAS technologies. In February 2026, the UK government reported that the defence personnel will be granted new powers under the Armed Forces Bill to defeat rogue drones threatening UK military sites, which is followed by a sharp rise to 266 incidents in 2025, and it is double the previous year. The legislation empowers authorised personnel to neutralise aerial, land, and maritime drones without police assistance, strengthening base security. Backed by around USD 270 million in counter-drone investment, these measures form part of wider efforts to enforce restricted airspace and protect Britain’s defence infrastructure.

Key Anti-Drone Market Players:

- RTX Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Dedrone Holdings Inc. (U.S.)

- WhiteFox Defense Technologies, Inc. (U.S.)

- Fortem Technologies, Inc. (U.S.)

- The Boeing Company (U.S.)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Rheinmetall AG (Germany)

- DroneShield Ltd. (Australia)

- QinetiQ Group PLC (UK)

- ELTA Systems Ltd. (Israel)

- Sentrycs Ltd. (Israel)

- Zen Technologies Ltd. (India)

- Indrajaal Pvt. Ltd. (India)

- Paras ANTI‑Drone Technologies Pvt. Ltd. (India)

- LIG Nex1 Co., Ltd. (South Korea)

- Rohde & Schwarz GmbH & Co. KG (Germany)

- Ondas Inc. (U.S.)

- Airbus Helicopters (France)

- Volatus Aerospace (Canada)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- RTX Corporation, through its Raytheon Technologies and Collins Aerospace divisions, is a dominant force in this field that benefits from an extensive portfolio of radar, electronic warfare, and kinetic and non-kinetic counter-UAS solutions. The company benefits from global defense contracts to invest heavily in sensor fusion and directed‑energy systems.

- Lockheed Martin Corporation is also a central player in this field, which is building on decades of aerospace and defense R&D to deliver advanced counter-UAS systems that blend radar and electronic disruption technologies. Its solutions are increasingly deployed in military and allied defense programs.

- Dedrone Holdings Inc. is identified as a leading innovator in airspace security software and sensor fusion platforms. These platforms are highly focused on the detection and mitigation of unauthorized drones by using AI-driven analytics, cloud integration, and multi-sensor data fusion.

- Thales Group leverages its deeper knowledge in aerospace electronics, radar systems, and secure communications to build counter-drone solutions that are suited for critical infrastructure, civil aviation, and defense clients. Besides, the firm also emphasizes global deployments and strategic collaborations with regional integrators to strengthen interoperability and local presence.

- DroneShield Ltd. is a specialized anti-drone technology company that is best known for its RF-centric detection, jamming systems, and portable mitigation tools such as DroneGun and DroneSentry devices. The firm’s solutions are especially designed for fast deployment by defense, law enforcement, and infrastructure protection units worldwide.

Below is the list of some prominent players operating in the global anti-drone market:

The anti-drone market hosts both leading defense primes and specialized tech firms that are making heavy investments in R&D, AI integration, and multi-sensor architectures to differentiate their product offerings. On the other hand, established aerospace and defense pioneers are highly focused on expanding their product portfolios and government contracts, whereas agile innovators focus on advanced detection, electronic warfare, and autonomous mitigation technologies. Strategic initiatives such as partnerships, acquisitions, and cross-domain integration are common as players are concentrated on expanding global footprints and enhancing interoperability with broader airspace and battlefield systems. In January 2026, HENSOLDT and TYTAN Technologies reported that they signed a Memorandum of Understanding to collaborate on counter-UAS systems and critical infrastructure protection, thereby creating rapidly deployable, battlefield-proven solutions.

Corporate Landscape of the Anti-Drone Market:

Recent Developments

- In March 2026, Ondas Inc. notified that its subsidiary, Airobotics Ltd., received a USD 20 million initial purchase order as prime contractor for a multi-year AI-driven autonomous border protection program. The program will deploy drones, command-and-control software, and integrated ground infrastructure to provide national border defense.

- In March 2026, Airbus Helicopters reported that its subsidiary, Survey Copter, was selected by the European Defense Agency for the M2UAS project, which is a 48-month program with a budget of USD 1.2 million to develop a hybrid, multi-mission uncrewed aircraft based on the Capa-X platform.

- In March 2026, Volatus Aerospace announced that it had launched SKYDRA, which is its first Software-as-a-Service (SaaS) platform for counter-unmanned aircraft system operational planning and simulation.

- Report ID: 3095

- Published Date: Mar 11, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.