Soil Conditioners Market Outlook:

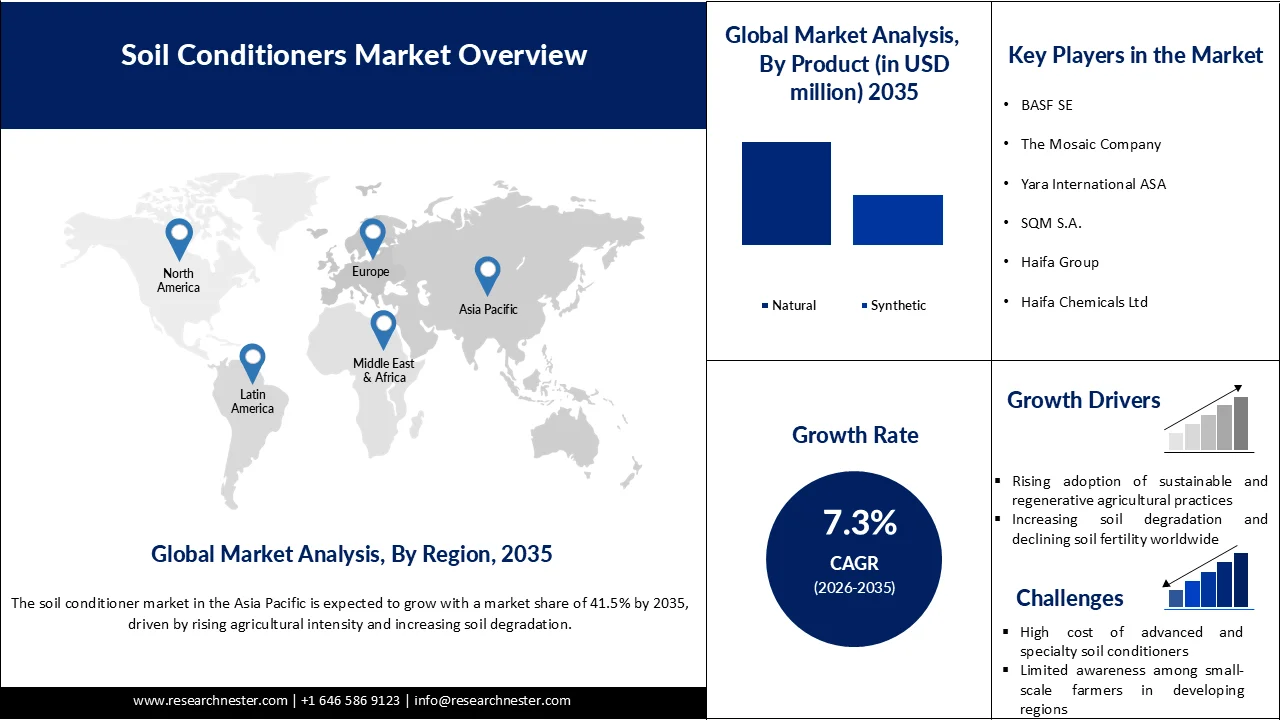

Soil Conditioners Market is valued at USD 8.52 billion in 2025 and is projected to reach USD 17.24 billion by 2035, growing at a CAGR of 7.3% during the forecast period, i.e., 2026-2035. In 2026, the industry size of soil conditioners is estimated at USD 9.14 billion.

The most significant primary growth driver for the global soil conditioners market is rampant soil deterioration and the loss of soil organic matter, which compels large-scale rehabilitation. Strategic use of farm waste in the form of manure and compost has dramatically enhanced soil fertility and environmental health. Various studies have shown that Vermicompost (VC) is a soil amendment that builds soil fertility by providing nutrients (NPK), improving microbial activity, improving water retention capabilities, making soil healthier and more productive, naturally. In alignment with this, USDA-supported programs, especially those targeting phosphorus and nitrogen management, have formally integrated soil conditioners into conservation practices. These initiatives are embedded in agricultural legislation aimed at reducing nutrient runoff and improving long-term farm productivity.

Global soil conditioner supply chains rely on crop by-products like composted manure and crop residues, which are commonly recovered from farm or municipal waste streams. Manufacturing operations (i.e., pelletizing and granulation) are becoming more centralized in stand-alone plants operating drum or disc granulators. Constructing manufacturing plant capacity has been facilitated by the integration of soil amendments into fertilizer plants to offer more throughput and product consistency. USDA's Agricultural Marketing Service (AMS) trade reports show increased organic equivalence arrangements for the exportation of soil amendment between the U.S., Canada, the EU, Japan, and Korea under the National Organic Program.

Key Soil Conditioners Market Insights Summary:

Regional Highlights:

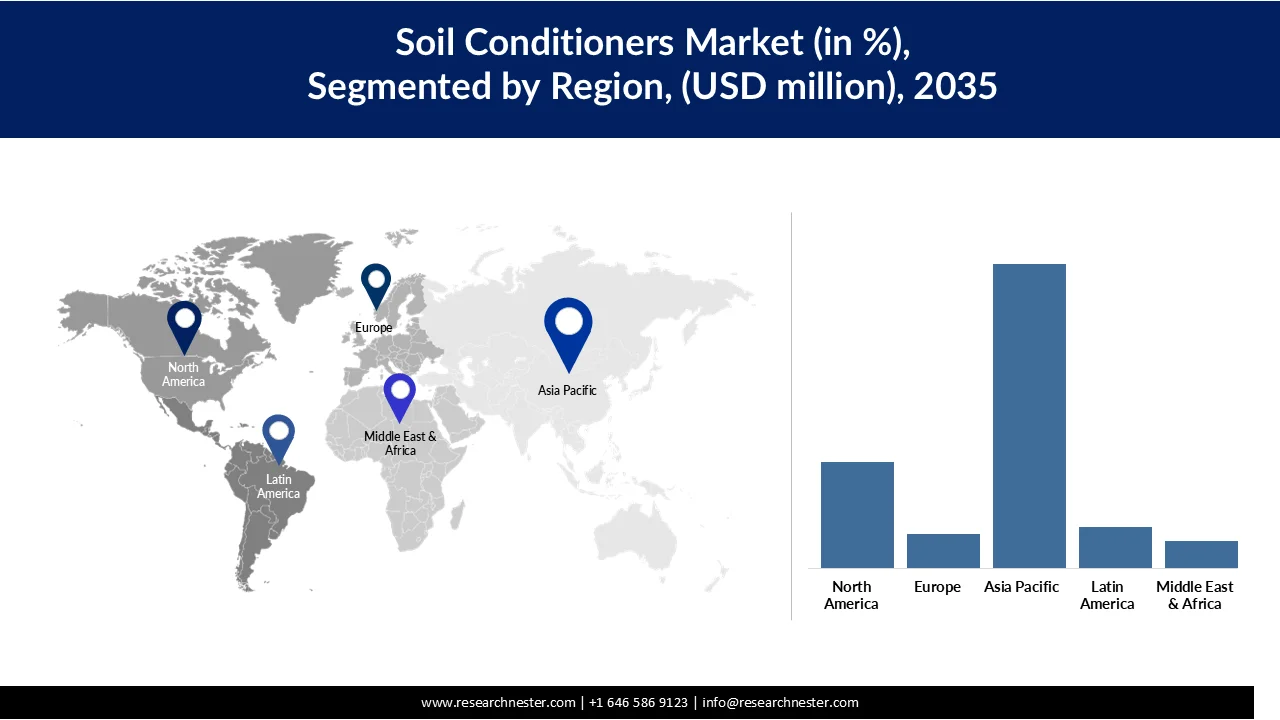

- The soil conditioners market in Asia Pacific is projected to hold a 41.5% share by 2035, driven by rising agricultural intensity and increasing soil degradation

- North America is expected to command a 37.8% share of the market by 2035, fueled by increasing concerns over soil degradation and the need for sustainable agricultural practices

Segment Insights:

- The natural segment in the soil conditioners market is projected to account for 66.7% share by 2035, propelled by increasing demand for sustainable and eco-friendly agricultural inputs

- The loam segment is anticipated to capture a 33.4% share by 2035, driven by its balanced composition of sand, silt, and clay enhancing agricultural productivity

Key Growth Trends:

- Global push for sustainable agriculture

- Climate change and soil degradation challenges

Major Challenges:

- Supply chain fragmentation and raw material volatility

- Regulatory ambiguity and compliance burden

Key Players: BASF SE, The Mosaic Company, Yara International ASA, SQM SA, Haifa Group, Haifa Chemicals Ltd, Coromandel International Ltd, UPL Limited, Koppert Biological Systems, Bio-Green Australia, LG Chem Ltd.

Global Soil Conditioners Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 8.52 billion

- 2026 Market Size: USD 9.14 billion

- Projected Market Size: USD 17.24 billion by 2035

- Growth Forecasts: 7.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41.5% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, India, Germany, Brazil

- Emerging Countries: Indonesia, Vietnam, Mexico, Turkey, Thailand

Last updated on : 31 March, 2026

Soil Conditioners Market - Growth Drivers and Challenges

Growth Drivers

- Global push for sustainable agriculture: This strong push toward sustainable agriculture is one major driver for the demand for soil conditioners. By the end of 2022, 96.4 million hectares were under organic management, representing a 26.6% increase, or 20.3 million hectares, from 2021. Australia rose by an incredible +17.3 million hectares to remain the country with the largest organic agriculture area at 53 million hectares, followed by India, which is second (4.7 million hectares), with significant growth. The organic farming area increased across all continents. Oceania has more than half of the organic area (53.2 million hectares), followed by Europe with 18.5 million hectares and Latin America with 9.5 million hectares. This expansion is further supported by rising awareness of soil health, increasing adoption of eco-friendly farming practices, and regulatory support for reducing chemical inputs. Soil conditioners play a crucial role in improving soil structure, enhancing nutrient retention, and boosting crop productivity, making them essential for sustainable and organic farming systems.

- Climate change and soil degradation challenges: Climate change will increase agricultural losses and production disruptions due to the exacerbation of soil decline from drought, flooding, and erosion. Soil conditioners can mitigate these effects by basically controlling the temperature and moisture absorption, structuring better availability of organic matter, hence rendering the crop tolerant to unfavorable conditions. Areas experiencing desertification, including parts of Africa, Australia, and the Middle East, are increasingly implementing conditioners to restore productivity. This driver is enabled by global climate resilience programs and international funding. Thus, soil conditioners are seen to be adopting broader resilience and adaptation strategies and land restoration.

- Technological advancements in product formulation: Advances in material science and microbiology are driving the development of innovative soil conditioners that are more targeted, biodegradable, and easily removable, leading to improved efficiency and sustainability in agriculture. New developments include slow-release carriers of nutrients, conditioners containing bio-stimulants, and products that are specifically microbe-laden and type of soil-specific. Collectively, these developments will improve effectiveness, reduce application rates or at least frequency, and yield measurable benefits, driving original commercial-scale farmers to adopt conditioned soil on their farms. The added benefit of precision agriculture tools (seeders) allows farmers to use the conditioners as intended by eliminating application rates and measuring cost in precision with environmental impact.

Challenges

- Supply chain fragmentation and raw material volatility: The soil conditioners market relies significantly on organic waste material such as compost, manure, and seaweed extracts, whose supply is unbalanced through seasonality and regional inefficiency in collection. Further, logistics disruption during the COVID-19 period and the ensuing Ukraine conflict led to a shortage and increased transport prices. This disintegrated supply chain inhibits large-scale, homogenous production as well as impinges on price stability. As a result, the sector has higher costs of input, lower incentives for investing in new capacity, and lower margins. All these issues combined restrict scalability and hamper market development in developed economies and emerging economies.

- Regulatory ambiguity and compliance burden: Unstable and changing environmental regulations from country to country, particularly in the EU, U.S., and India, offer global producers compliance challenges. Lack of harmonized certification of bio-based or organic soil conditioners restricts product approval and market access. Moreover, uncertainty about government regulations regarding permitted input sources (e.g., farm versus industrial compost) adds operational uncertainty. Small and medium-sized businesses struggle to cope with testing and documentation needs, as seen through increased operating expenses. Such regulation fragmentation discourages innovation and cross-border commerce, which decelerates the pace of international soil conditioners market development.

Soil Conditioners Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.3% |

|

Base Year Market Size (2025) |

USD 8.52 billion |

|

Forecast Year Market Size (2035) |

USD 17.24 billion |

|

Regional Scope |

|

Soil Conditioners Market Segmentation:

Product Segment Analysis

The natural segment is expected to hold 66.7% of the soil conditioners market share, due to increasing demand for sustainable and eco-friendly agricultural inputs. Farmers are shifting toward organic and bio-based soil conditioners such as compost, manure, and biochar to improve soil fertility without harmful chemical residues. Rising awareness about soil degradation and the need to restore soil health is further accelerating adoption. Additionally, government support for organic farming and restrictions on chemical fertilizers in several regions are boosting demand for natural alternatives. These products enhance soil structure, water retention, and microbial activity, leading to improved crop yields. Growing consumer preference for organic food is also encouraging farmers to adopt natural soil conditioners. As a result, the segment continues to expand and plays a key role in overall market growth.

Soil Type Segment Analysis

The loam segment is expected to hold a 33.4% soil conditioners market share by 2035, due to its balanced composition of sand, silt, and clay, making it ideal for agricultural productivity. Loam-based soil conditioners improve soil structure, aeration, and drainage while maintaining adequate moisture retention, which supports healthy root development. Farmers widely prefer loam soils as they enhance nutrient availability and reduce the need for excessive chemical inputs. The segment is also benefiting from increasing demand for high-yield and quality crops, particularly in intensive farming systems. Additionally, loam conditioners help restore degraded soils and improve long-term soil fertility. Their versatility across different crop types and climatic conditions further boosts their adoption. As a result, the loam segment continues to play a significant role in driving overall market expansion.

Crop Type Segment Analysis

The cereals & grains segment is expected to grow at a significant soil conditioners market share by 2035, due to the extensive cultivation of staple crops such as wheat, rice, and corn across large agricultural areas. Continuous and intensive farming practices in this segment often lead to soil degradation and nutrient depletion, increasing the need for soil conditioners. These products help improve soil structure, enhance water retention, and boost nutrient availability, thereby supporting higher crop yields. Additionally, maintaining soil health is critical for ensuring the consistent production of cereals and grains, which are essential for global food security. The segment also benefits from growing demand for sustainable farming practices, encouraging the use of organic and natural soil conditioners. Government initiatives aimed at improving agricultural productivity further support adoption. As a result, the cereals and grain segment significantly contributes to overall market growth.

Our in-depth analysis of the soil conditioners includes the following segments:

|

Segments |

Subsegments |

|

Product |

|

|

Solubility |

|

|

Soil Type |

|

|

Crop Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Soil Conditioners Market - Regional Analysis

Asia Pacific Market Insights

The soil conditioners market in Asia Pacific is expected to grow with a market share of 41.5% by 2035, driven by rising agricultural intensity and increasing soil degradation. This has pushed farmers toward adopting soil restoration solutions such as conditioners to maintain productivity. The region holds a significant share of the global soil conditioners market, supported by its large population and growing food demand. Rapid urbanization and excessive fertilizer use have led to declining soil fertility, increasing the need for soil amendments. Additionally, government initiatives promoting sustainable agriculture and regenerative farming practices are further accelerating market adoption across the region.

China soil conditioners market is expanding rapidly due to intensive agricultural activity and strong government-led sustainability efforts. According to data from the Food and Agriculture Organization (FAO), China applied approximately 52.51 million tons of chemical fertilizers in 2020, reflecting large-scale input use in agriculture. Additionally, FAO-based data indicate that fertilizer consumption levels remained high at around 394.02 kg per hectare of arable land around 2020, highlighting significant soil stress from intensive farming. The continued high input intensity has contributed to soil degradation, increasing the need for soil conditioners and organic amendments. In response, government policies promoting reduced fertilizer usage and sustainable farming practices are supporting market growth. These factors, combined with rising demand for improved soil health and crop productivity, are driving the adoption of soil conditioning solutions across China.

India soil conditioners market is growing steadily, supported by an increasing focus on soil health and sustainable farming practices. According to the Food and Agriculture Organization, India had over 2.3 million hectares under organic agriculture in 2020, reflecting a rising shift toward sustainable inputs and soil improvement practices. Additionally, data from the World Bank indicate that fertilizer consumption in India stood at approximately 165 kg per hectare of arable land in 2020, highlighting continued pressure on soil health. Rising soil erosion, land degradation, and nutrient depletion are encouraging farmers to adopt soil conditioners to improve productivity. Government initiatives such as soil health management programs are further promoting adoption. Furthermore, the need to enhance crop yield to meet growing food demand is accelerating market expansion across the country.

North America Market Insights

North America leads the overall market revenue of soil conditioners, with an expected share of around 37.8% by 2035. The market is growing steadily due to increasing concerns over soil degradation and the need for sustainable agricultural practices. This has created strong demand for soil improvement solutions across the region. North America benefits from advanced farming technologies, widespread adoption of regenerative agriculture, and supportive government programs promoting soil health. Additionally, rising demand for organic food and environmentally sustainable inputs is accelerating the adoption of soil conditioners. Investments in precision agriculture and improved soil management practices are further strengthening market growth.

The soil conditioners market in the U.S. is expanding significantly due to large-scale commercial agriculture and increasing soil health concerns. Additionally, data from the U.S. Department of Agriculture Natural Resources Conservation Service indicate that soil erosion remains a persistent challenge, driving the need for restoration practices. Government-backed conservation and soil health initiatives are encouraging the adoption of soil conditioners. The growing shift toward organic farming and sustainable agriculture is further boosting demand. Moreover, advancements in agri-tech and precision farming are supporting efficient soil management solutions across the country.

Canada soil conditioners market is growing steadily, driven by strong government support for sustainable agriculture and climate-resilient farming. Initiatives such as the Agricultural Climate Solutions program are promoting soil health improvement and carbon sequestration practices. The country is increasingly adopting regenerative farming techniques, including the use of organic soil conditioners to enhance soil structure and fertility. Additionally, rising awareness of environmental sustainability and soil conservation is encouraging farmers to shift toward eco-friendly inputs. Expanding organic farming practices and policy support are further driving market growth. These factors collectively position Canada as a key contributor to the North American soil conditioners market.

Europe Market Insights

The soil conditioners market in Europe is growing steadily, driven by widespread soil degradation and strong regulatory support for sustainable agriculture. According to the European Commission, around 60–70% of soils in the EU are unhealthy, highlighting the urgent need for soil improvement solutions. Additionally, organic farming expanded to nearly 14.7 million hectares in 2020, reflecting a shift toward sustainable inputs. Increasing adoption of regenerative agriculture and strict environmental policies are accelerating demand for soil conditioners. Investments in soil restoration and climate-resilient farming are further supporting market growth across the region.

France soil conditioners market is expanding due to intensive agricultural practices and increasing focus on soil sustainability. Soil degradation caused by urbanization and continuous cultivation is driving the need for soil enhancement solutions. Government policies promoting agroecology and reduced chemical usage are supporting market growth. Additionally, rising consumer demand for organic food is encouraging farmers to adopt soil conditioners. The expansion of precision farming and sustainable land management practices is further boosting demand.

Germany soil conditioners market is growing steadily, supported by strong environmental policies and increasing adoption of sustainable agriculture. Soil degradation and nutrient imbalances are encouraging the use of soil conditioners to improve fertility and productivity. Government initiatives promoting climate-smart agriculture and soil conservation are further driving adoption. Additionally, increasing awareness of soil health among farmers and the expansion of organic farming are supporting market growth. Technological advancements in precision agriculture are also enhancing soil management efficiency.

Key Soil Conditioners Market Players:

- BASF SE (Germany)

- The Mosaic Company (U.S.)

- Yara International ASA (Norway)

- SQM S.A. (Chile)

- Haifa Group (Israel)

- Haifa Chemicals Ltd (Israel)

- Coromandel International Ltd (India)

- UPL Limited (India)

- Koppert Biological Systems (Netherlands)

- Bio-Green Australia (Australia)

- LG Chem Ltd (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BASF SE is a leading player in the soil conditioners market, offering a wide range of agricultural solutions, including soil health enhancers and performance chemicals. The company focuses on improving soil structure, nutrient efficiency, and water retention through advanced formulations. Its strong R&D capabilities enable the development of sustainable and high-performance soil solutions. BASF’s global presence and integrated supply chain further strengthen its position in the market.

- Syngenta AG plays a significant role in the soil conditioners market through its focus on sustainable agriculture and soil health improvement. The company provides biological and chemical solutions that enhance soil fertility and crop productivity. It invests heavily in innovation to develop eco-friendly soil treatment products. Syngenta’s strong farmer network and global distribution channels support widespread adoption.

- UPL Limited is a prominent player offering a diverse portfolio of soil conditioners, bio-stimulants, and crop protection products. The company emphasizes sustainable farming practices and soil regeneration solutions. Through its global reach, UPL delivers cost-effective and innovative soil health products to a wide customer base. Strategic acquisitions and partnerships have strengthened its presence in the agricultural inputs market.

- Coromandel International Ltd. is a key contributor to the soil conditioners market, particularly in Asia. The company provides organic and specialty nutrient products aimed at improving soil fertility and crop yield. It actively promotes balanced nutrient management and soil health awareness among farmers. Its extensive distribution network and farmer outreach programs support strong market penetration.

- Evonik Industries AG offers specialty chemicals that are used in soil conditioning applications to improve nutrient availability and soil performance. The company focuses on innovation-driven solutions that enhance agricultural productivity while maintaining environmental sustainability. Its expertise in specialty additives enables the development of efficient soil enhancement products. Evonik’s global footprint and technological capabilities make it a strong market participant.

Below is the list of the key players operating in the global soil conditioners market:

The global soil conditioners market is characterized by the presence of diversified multinational companies focused on product innovation, sustainability, and strategic partnerships to expand their global footprints. Leaders like BASF SE and The Mosaic Company leverage advanced R&D capabilities to develop eco-friendly and bio-based soil conditioners. Regional players such as Coromandel International and UPL Limited are expanding through acquisitions and localized product lines tailored to emerging markets like India. Japanese manufacturers Mitsubishi Chemical and Sumitomo Chemical emphasize technological advancements in organic and specialty conditioners to meet stringent environmental regulations. Collaborations and investments in sustainable agriculture continue to shape competitive dynamics globally.

Corporate Landscape of the Global Soil Conditioners Market:

Recent Developments

- In November 2025, BASF announced the registration of Integral Pro, a biological seed treatment designed to protect crops from soil-borne diseases and enhance plant growth. The product, part of BASF’s BioSolutions portfolio, utilizes beneficial bacteria to create a protective barrier around seeds. It improves crop resilience and supports sustainable farming practices by reducing reliance on chemical inputs. The solution is set to be available across the European Union from 2026. This highlights BASF’s commitment to biological soil and crop health solutions.

- In October 2025, BASF announced the launch of its xarvio HEALTHY FIELDS platform integrated with the AI-based Humus soil improvement service. The solution was introduced in Japan to support rice farmers using dry direct-seeding cultivation. It combines digital farming tools with soil enhancement capabilities to improve crop yield and soil health. The service addresses challenges such as poor soil conditions and uneven productivity. This initiative reflects BASF’s focus on integrating soil conditioning with digital agriculture solutions.

- Report ID: 7864

- Published Date: Mar 31, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.