Semiconductor Intellectual Property Market Regional Analysis:

Asia Pacific Market Insights

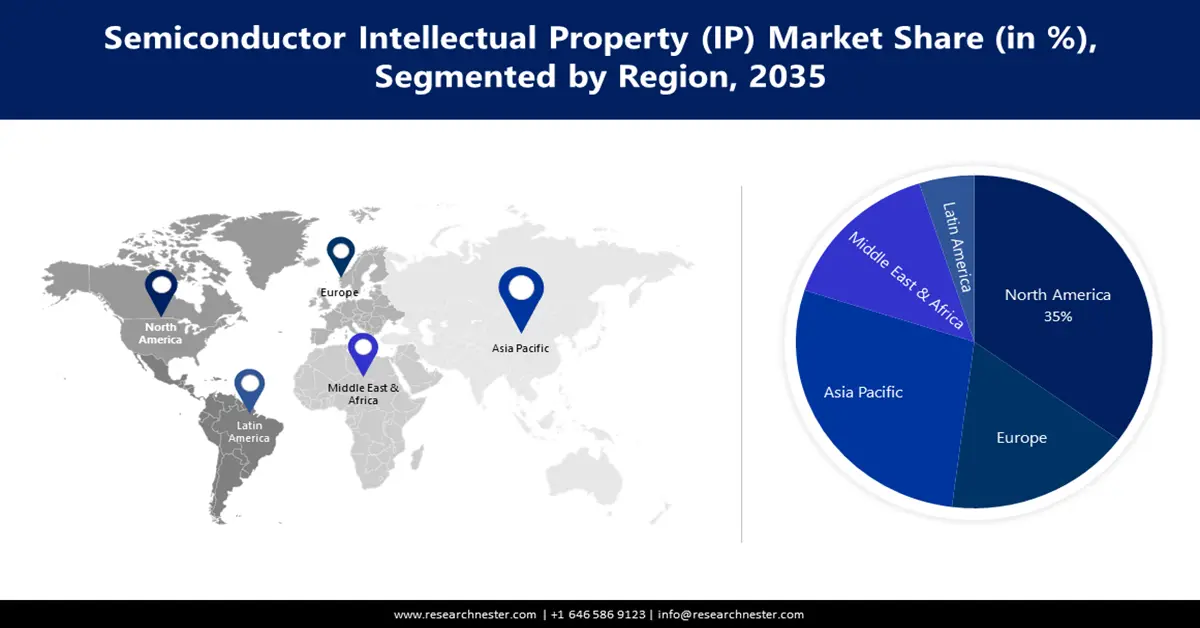

Asia Pacific semiconductor intellectual property market is expected to capture revenue share of over 54.8% by 2035. The rapidly expanding consumer electronics sector, swift digitalization of industries, growing adoption of autonomous vehicles, and advancements in semiconductor manufacturing are augmenting the overall semiconductor intellectual property market growth. Innovations in wireless communication technologies are further contributing to the SIP solution providers. India, China, Japan, and South Korea are the most opportunistic marketplaces for SIP solution producers.

China is the top producer of semiconductor technologies across the world owing to supportive government policies and schemes such as the Made in China 2025 initiative. The advancements in communication technologies are anticipated to directly uplift the profit shares of SIP producers. For instance, in September 2025, the Government of China revealed that over 4 million 5G base stations are installed across the country. China’s 5G base stations hold 42.0% of the global 5G standard essential patent declarations, with around 966 million 5G mobile subscribers.

In India, the rising demand for consumer electronics such as smartphones, tablets, computers, laptops, and electric vehicles is propelling the sales of semiconductor chips and wafers. The country’s supportive start-up ecosystem is creating a lucrative marketplace for companies eager to enter the semiconductor IP trade. The India Brand Equity Foundation (IBEF) report reveals that the country is estimated to surpass USD 300.0 billion in electronics manufacturing and exports of USD 120.0 billion by FY 25-26. The electronics system design & manufacturing (ESDM) market is significantly contributing to achieving the country's goal of generating USD 1 trillion from the digital economy by 2025.

North America Market Insights

The North America semiconductor intellectual property market is poised to increase at the fastest CAGR during the forecast period. The high adoption of digital technologies, growing investments in semiconductor manufacturing, and increasing adoption of autonomous vehicles are collectively contributing to the market growth. Both the U.S. and Canada are high-earning marketplaces for SIP providers.

The U.S. is one of the global leaders in semiconductor manufacturing especially for advanced applications such as artificial intelligence (AI), machine learning (ML), 5G, and autonomous vehicles. This further drives up the need for innovative semiconductor intellectual property licensing as companies need to stay competitive in the crowded landscape. The Semiconductor Industry Association (SIA) estimates that the CHIPS and Science Act is driving high private investments in semiconductor manufacturing in the country. As of August 2024, over 90 new semiconductor manufacturing projects were announced in the U.S., and since the introduction of the CHIPS and Science Act around USD 450.0 billion announced investments were recorded in the 28 states.

Canada’s burgeoning tech ecosystem is driving high demand for advanced semiconductor designs. The strong presence of digital solution producers coupled with advancements in wireless communication systems is augmenting the need for innovative semiconductor IP licensing. In April 2024, the government revealed an investment of around USD 41.57 billion for innovative semiconductor manufacturing and economic growth. The government’s continuous investment to drive innovations in quantum and semiconductor technologies is set to propel the overall SIP market growth in the coming years.