Metal Recycling Market Outlook:

Metal Recycling Market size was valued at USD 319.3 billion in 2025 and is projected to reach USD 649 billion by the end of 2035, rising at a CAGR of 8.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of metal recycling is evaluated at USD 345.4 billion.

The worldwide metal recycling market is poised for solid growth over the forecasted years, mainly propelled by rising demand for sustainable raw materials, stringent environmental regulations, and the need to reduce greenhouse gas emissions. In addition, the heightened demand for recycled ferrous and non-ferrous metals as critical raw materials in manufacturing and infrastructure also prompts a profitable business environment for pioneers in this field. According to the official statistics published by the USGS in 2025, domestic purchases of iron and steel scrap in the U.S. totaled an estimated amount of USD 19.7 billion. The majority of scrap was consumed by manufacturers of pig iron, raw steel, and steel castings to produce steel products, whereas ferrous castings accounted for most of the remaining usage. U.S. apparent consumption of iron and steel scrap reached 57 million tons in 2025, which is up from 55 million tons in 2024.

U.S. Iron & Steel Scrap Statistics 2021-2025: Production, Consumption, Prices, and Employment Trends

|

Salient Statistics |

2021 |

2022 |

2023 |

2024 |

2025 |

|

Production (million tons) |

|||||

|

Home scrap |

6.6 |

7.3 |

7.1 |

7.7 |

7 |

|

Net receipts |

65 |

62 |

59 |

57 |

58 |

|

Imports for consumption |

5.3 |

4.7 |

5.1 |

4.8 |

5 |

|

Exports |

18 |

18 |

16 |

15 |

13 |

|

Consumption (million tons) |

|||||

|

Reported |

59 |

56 |

55 |

55 |

57 |

|

Apparent |

58 |

57 |

55 |

55 |

57 |

|

Price, average, delivered - No. 1 heavy melting composite (USD /metric ton) |

417.66 |

381.72 |

333.28 |

314.85 |

319 |

|

Stocks, consumer, year-end (million tons) |

4.4 |

3.9 |

4.2 |

4 |

3.9 |

|

Employment, foundries (number) |

101,000 |

105,000 |

107,000 |

106,000 |

107,000 |

Source: USGS

Furthermore, the raw steel production, the primary consumer of scrap, increased to 82 million tons, with net shipments of steel mill products also totaling 82 million tons. The same data from USGS also disclosed that recycled iron and steel scrap is a critical raw material for the U.S. steel and foundry industries, which conserves 1.1 tons of iron ore, 0.6 tons of coking coal, and 0.05 tons of limestone per ton of steel recycled, by making the use of less energy when compared to primary production. The U.S. scrap recycling rate has averaged 80% to 90% over the past decade, with automobiles as the primary source, recycling more than 13 million tons annually from more than 280 shredders. In 2025, 89% of recycled scrap came from net receipts, with imports primarily from Canada (71%) and Mexico (15%), supporting both manufacturing and post-consumer recycling operations, hence denoting there is a huge growth opportunity for the market in the upcoming years.

U.S. Steel Scrap Sector 2024-2025: Prices, Production, Trade, and Capacity Utilization Trends

|

Category |

2024 |

2025 |

Notes |

|

Steel Mill Capacity Utilization (%) |

72-78 |

75-80 |

First 10 months of each year |

|

No. 1 Heavy Melting Steel Scrap Price (USD /ton) |

314.85 (annual avg) |

319.00 (annual avg) |

Monthly range in 2025: High USD 366.26 (March), Low USD 303.46 (November) |

|

Exports - Top Destinations (% by tonnage) |

- |

- |

Turkey 29%, Bangladesh 13%, India 10% (first 8 months of 2025) |

|

Value of Exports (USD billion) |

4.5 |

3.6 |

First 8 months of 2025 |

|

Imports - Top Sources (% by tonnage) |

- |

- |

Canada 62%, Mexico 25%, UK 4% (first 8 months of 2025) |

|

Value of Imports (USD billion) |

1.3 |

1.4 |

First 8 months of 2025 |

|

Global Finished Steel Demand |

- |

Unchanged |

Decline in China offset by growth in Egypt, India, Saudi Arabia, Vietnam |

|

Substitutes - Direct-Reduced Iron (million tons) |

8.1 |

7.8 |

Used as a substitute for scrap in the U.S. |

Source: USGS

Key Metal Recycling Market Insights Summary:

Regional Highlights:

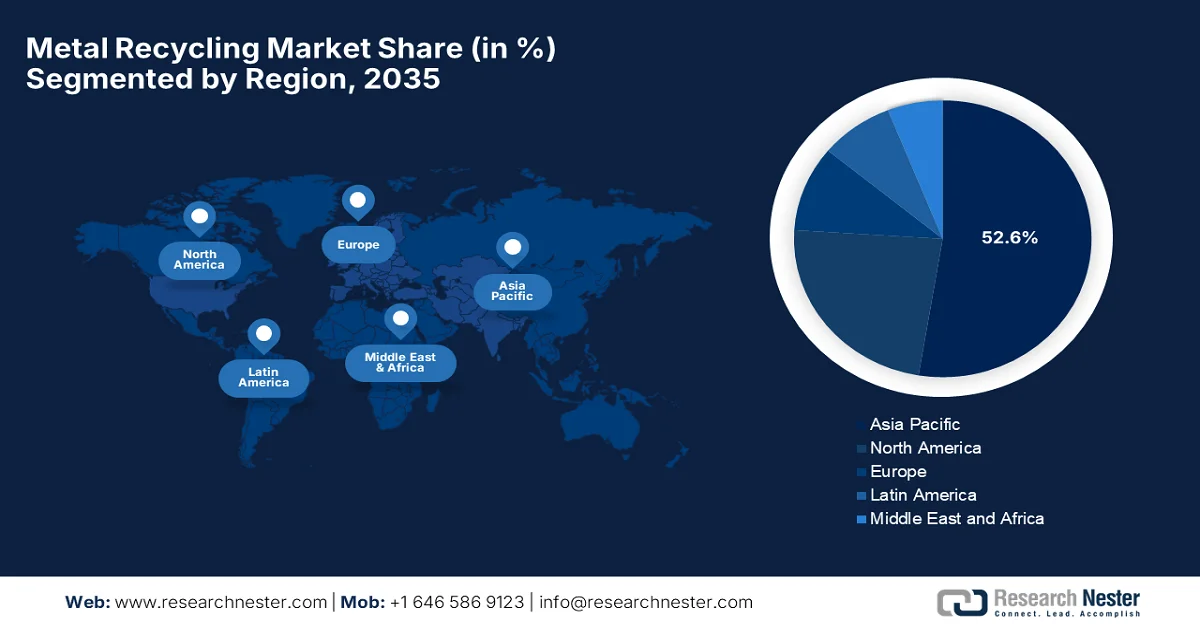

- The Asia Pacific metal recycling market is anticipated to secure a dominant 52.6% revenue share by 2035, attributed to extensive metal production capabilities alongside rapid industrialization and manufacturing expansion.

- North America is projected to witness considerable growth in the market during 2026–2035, impelled by a mature recycling ecosystem supported by advanced processing infrastructure and strong industrial demand.

Segment Insights:

- The construction sub-segment of the metal recycling market is projected to command a 40.6% share by 2035, fueled by accelerating urbanization and rising infrastructure investments.

- The steel segment is anticipated to maintain a significant revenue share during 2026–2035, propelled by its extensive utilization across automotive, construction, and consumer goods industries along with streamlined recycling processes.

Key Growth Trends:

- Increasing demand from industrialization & energy transition

- Cost & energy efficiency

Major Challenges:

- Environmental regulations and compliance costs

- Quality control and product standards

Key Players: Nucor Corporation (U.S.), ArcelorMittal S.A. (Luxembourg), Sims Metal Management Ltd. (Australia), Commercial Metals Company (U.S.), Schnitzer Steel Industries, Inc. (U.S.), European Metal Recycling Ltd. (UK), Aurubis AG (Germany), Novelis Inc. (U.S.), Ferrous Processing & Trading Co. (U.S.), DOWA Holdings Co., Ltd. (Japan), American Iron & Metal Co. (U.S.), OmniSource Corporation (U.S.), Tata Steel Ltd. (India), Kuusakoski Group Oy (Finland), SA Recycling LLC (U.S.), REAL ALLOY (U.S.), PSC Metals (U.S.), HKS Metals BV (Netherlands), Sunrise Metal Recycling Ltd. (UK).

Global Metal Recycling Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 319.3 billion

- 2026 Market Size: USD 345.4 billion

- Projected Market Size: USD 649 billion by 2035

- Growth Forecasts: 8.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (52.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, India, Japan, Germany

- Emerging Countries: South Korea, Brazil, Vietnam, Indonesia, Mexico

Last updated on : 19 February, 2026

Metal Recycling Market - Growth Drivers and Challenges

Growth Drivers

- Increasing demand from industrialization & energy transition: There has been a rise in infrastructure builds and expansion of manufacturing sectors such as automotive, construction, electronics, and fuel demand for metals. In this context, the recycled metals offer a sustainable supply to meet these needs, driving business in the metal recycling market. According to the article published by the World Economic Forum in April 2024, recycling energy-transition metals from batteries, electric vehicles, and renewable-energy systems is gaining momentum as electrification intensifies pressure on primary metal supplies. It also mentioned that since the demand for metals such as steel, aluminium, and copper is on the rise, the secondary sources are becoming highly essential to easing supply constraints and strengthening domestic supply security amid geopolitical risks and trade disruptions. Structural shifts such as supply-chain rebalancing, vertical integration, tighter scrap markets, and advances in recycling technology are expected to drive sustained investment in secondary metal markets.

- Cost & energy efficiency: The recycled metals are considered to be cheaper to process when compared to extracting and refining virgin ores. On the other hand, the aspects of lower energy consumption and reduced production costs make recycling economically attractive, particularly when the raw material prices are very high. Based on the data from the Ministry of Steel, which was published in July 2024, the government of India has launched multiple initiatives to decarbonize the steel industry, which include task forces, recycling policies, renewable energy missions, and efficiency schemes. Therefore, these efforts have already reduced CO2 emission intensity from 3.1 tonnes per ton of crude steel in 2005 to 2.5 tonnes in 2022. Looking ahead, short-term goals focus on energy efficiency and renewable energy, medium-term on green hydrogen and carbon capture, and long-term on disruptive technologies to achieve net-zero, hence positively impacting the market expansion.

- Growth in electronic & e-waste recycling: The surge in terms of electronic devices, i.e., smartphones, computers, batteries, increases e-waste, which is a rich source of valuable metals such as copper, gold, and palladium. Therefore, efficient recovery of these materials boosts the recycled metal supply chain. As stated by the Ministry of Mines in October 2025, it has issued detailed guidelines for the ₹1,500 crore (approximately USD 180 million) Critical Mineral Recycling Incentive Scheme under the National Critical Mineral Mission. The scheme mainly aims to develop domestic recycling capacity for critical minerals such as lithium, cobalt, and nickel from e-waste, spent lithium-ion batteries, and other scrap materials. This supports both new and existing recyclers to expand or modernize their operations and strengthen the domestic e-waste recycling value chain, boosting the growth of the metal recycling market.

Leading Global Recycled Steel Importers by Volume - January to September 2025

|

Country |

Recycled Steel Imports (million tonnes) |

Year-on-Year Change (%) |

Major Suppliers |

|

Turkey |

13.988 |

-6.8 |

U.S., Netherlands, UK, Belgium, Denmark |

|

India |

6.54 |

+2.8 |

U.S., UK, Brazil, Australia, Malaysia |

|

Vietnam |

3.255 |

-19.6 |

- |

|

Taiwan |

1.461 |

-35.5 |

- |

|

South Korea |

1.352 |

-28.2 |

- |

|

EU-27 |

3.758 |

+1.5 |

- |

|

U.S. |

3.472 |

+6.7 |

- |

|

Pakistan |

2.106 |

+29.4 |

- |

|

Thailand |

1.421 |

+61.8 |

- |

Source: BIR

Leading Global Scrap Iron Exporters by Trade Value - 2024

|

Country |

Export Value (USD Billion) |

|

U.S. |

6.33 |

|

Germany |

4.19 |

|

UK |

3.36 |

|

Netherlands |

3.02 |

|

France |

2.83 |

|

Japan |

2.6 |

|

Canada |

1.94 |

|

Belgium |

1.58 |

|

Poland |

1.37 |

|

Australia |

1.09 |

Source: OEC

Challenges

- Environmental regulations and compliance costs: This is the major barrier hindering the expansion of the metal recycling market. The facilities need to comply with the aspects of emissions controls, hazardous material handling, wastewater treatment, and disposal requirements. Meanwhile, non-compliance can lead to fines and operational shutdowns. Regulatory frameworks vary by region, since they implement distinct standards that complicate cross-border operations. In this context, upgrading infrastructure to meet these requirements necessitates substantial expenses, which can be challenging, especially for smaller recyclers. In addition, the evolving sustainability mandates for carbon emissions and circular economy practices increase operational complexity, causing obstacles to the market’s exposure in certain nations.

- Quality control and product standards: Maintaining consistent quality in recycled metals is yet another burden for the pioneers in the market, especially for applications in automotive, aerospace, and electronics sectors. Variability in terms of scrap composition, contamination from mixed materials, and processing inconsistencies can reduce product value. Clients across the globe are mostly looking for certified recycled content and traceability throughout the supply chain. Therefore, recyclers need to implement stringent quality control, advanced chemical testing, and certification systems to ensure compliance. Furthermore, investment in monitoring technologies, process optimization, and reporting mechanisms is highly essential to deliver high-grade recycled materials.

Metal Recycling Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.2% |

|

Base Year Market Size (2025) |

USD 319.3 billion |

|

Forecast Year Market Size (2035) |

USD 649 billion |

|

Regional Scope |

|

Metal Recycling Market Segmentation:

Application Segment Analysis

The construction sub-segment is expected to dominate with the largest share of 40.6% in the metal recycling market by 2035. The dominance of the subtype is mainly driven by urbanization and infrastructure investments, which require large volumes of steel and aluminum, directly boosting demand for recycled feedstock. As stated by High Speed Two in August 2023, its use of UK recycled steel is supporting hundreds of jobs across South Wales, Yorkshire, and Nottinghamshire by also reducing carbon emissions, with more than 20,000 tonnes already used and 140,000 tonnes in future orders. It also stated that CELSA Steel UK’s Cardiff sites employ 750 staff, and ROM GROUP’s Sheffield and Nottinghamshire facilities contribute to the production and fabrication of rebar and piling cages. Overall, HS2’s construction programme is injecting £23 billion into the domestic supply chain, and such demand helps stabilize long‑term revenue share for this segment.

Product Segment Analysis

The steel is projected to retain a significant share throughout the forecast period in the market due to its extensive use in automotive, construction, and consumer goods sectors. Globally, steel is the most recycled material, largely influenced by the fact that huge structures can be recovered and easily reprocessed. In addition, the simplicity of separating steel from the waste stream also supports and drives the steel recycling process. For instance, in December 2025, the TSR Group and thyssenkrupp Steel announced that they had signed a long-term agreement to supply TSR40, which is a high-quality recycled steel from post-consumer scrap, for use in blast furnaces. TSR40 forms the basis of Bluemint Recycled, a CO2-reduced steel available in all conventional grades, supporting decarbonization and circular economy efforts, hence denoting a positive market outlook.

End use Industry Segment Analysis

Automotive, which is a part of end use industry, is expected to grow with a considerable share in the metal recycling market during the discussed time period. The subsegment is mainly driven by the increasing demand for lightweight and high-strength materials to meet stringent fuel efficiency and emission standards. Metals such as aluminum and steel recycled from end-of-life vehicles reduce manufacturing costs and environmental impact. In addition, the adoption of recycled metals supports circular economy principles by enabling manufacturers to sustainably reuse resources without compromising performance. Advancements in terms of recycling technologies are also improving the quality and consistency of recovered metals, making them more attractive for automotive applications. The presence of all of these factors makes the automotive segment a major contributor to the growth of the metal recycling industry.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Product |

|

|

End use Industry |

|

|

Material Type |

|

|

Process Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Metal Recycling Market - Regional Analysis

APAC Market Insights

The Asia Pacific metal recycling market is forecasted to emerge as the dominant region, capturing the largest revenue share of 52.6% during the stipulated timeframe. The leadership of the region is mainly driven by extensive metal production capabilities. The region’s market is also driven by industrialization, urbanization, and the expansion of manufacturing sectors such as automotive, construction, and electronics. According to the official statistics published by World Steel Organization in August 2025, the Asia and Oceania region produced 110.4 million tonnes of crude steel in July 2025, and for the first seven months of 2025, the region’s output stood at 804.8 million tonnes, also down 1.8% year-on-year. Furthermore, countries such as China, India, Japan, and South Korea are making investments in recycling infrastructure, advanced processing technologies, and formalized collection systems to manage growing volumes of scrap.

Top Asia-Pacific Crude Steel Producing Countries - 2025 Production & Year-on-Year Change

|

Country |

2025 Production (Mt) |

2024 Production (Mt) |

% Change |

|

China |

960.8 |

1,005.1 |

-4.4 |

|

India |

164.9 |

149.4 |

+10.4 |

|

Japan |

80.7 |

84.0 |

-4.0 |

|

South Korea |

61.9 |

63.6 |

-2.8 |

|

Türkiye |

38.1 |

36.9 |

+3.3 |

Source: World Steel Organization

The evolving regulatory frameworks, which are aimed at establishing waste recycling systems is driving the growth of the metal recycling market in China. The country’s market also benefits from regulations to allow freer movement of recycled steel and battery waste materials signal efforts to support recycling industries and integrate recycled content into domestic supply chains. IEA in November 2025 revealed that the country’s 14th five-year plan on the circular economy, announced by the National Development and Reform Commission, aims to build a resource recycling industrial system and improve overall resource utilization by 2025. This particular plan has priority towards technological innovation, industrial development, and the recycling of critical minerals, including waste power batteries from new energy vehicles. It also promotes the creation of recycling networks, traceability systems, and standards to strengthen the domestic circular economy and hence support the growth of the metal recycling sector.

The industrial and infrastructure growth, coupled with national policies that efficiently promote scrap recovery and recycling processes are efficiently boosting the market in India. The supporting government initiatives and the development of certified processing zones enhance the availability of recycled metals for domestic industries. The Ministry of Mines, in October 2025, stated that it has launched an e-waste recycling drive under special campaign 5.0 by mainly focusing on scientific disposal and resource recovery from obsolete electronic equipment. The initiative operates across multiple cities with collaboration from the Jawaharlal Nehru Aluminium Research, Development & Design Centre. In addition, the campaign is partnering with Attero, and it has established collection points nationwide to recover valuable metals such as lithium, cobalt, nickel, and rare earth elements for domestic manufacturing, denoting a huge growth opportunity for the market’s expansion and exposure.

North America Market Insights

The North America metal recycling market is expected to grow at a considerable rate from 2026 to 2035. The region’s growth is mainly attributable to a mature recycling ecosystem with extensive processing infrastructure and strong industrial demand. The aspects, such as improved technologies and stringent environmental conditions, also promote sustainable metal recovery in this region. In August 2025, the U.S. Department of Energy announced plans to issue an amount of nearly USD 1 billion in funding opportunities to strengthen the critical minerals and materials supply chain. It also mentioned that the initiatives include programs for battery recycling, rare earth element recovery, and industrial byproduct processing, which are aimed at reducing reliance on foreign sources. In addition, these actions are designed to accelerate domestic mining, processing, and manufacturing technologies by making sure there is secure and sustainable access to essential materials for energy and industry.

Metal recycling is prominent in the domestic resource recovery, where there are major investments in facilities that process complex waste streams such as printed circuit boards and copper cables to produce recycled metals. Therefore, this focus on proper recovery technologies helps reduce dependency on imports and supports industries that require strategic metals, responsibly uplifting the U.S. metal recycling market. For instance, in April 2025, Flash Metals reported that it has secured a long-term supply agreement with Plastic Recycling Inc. to source up to 400 tons per year of PCB-rich electronic scrap by supporting its Flash Joule Heating demonstration plant in the U.S. Therefore, this guaranteed feedstock, combined with a prior agreement with Dynamic Lifecycle Innovations, ensures over 1,100 tons per year of high-value e-waste for domestic recovery of precious and strategic metals. Hence, the presence of such agreements strengthens the country’s domestic supply chains and reduces reliance on imported critical materials.

The higher capabilities, particularly in advanced metal recovery and processing is the main factor boosting the metal recycling market in Canada. Partnerships and expansions of recovery centers, especially, reflect efforts to boost domestic scrap collection and recycling, aligning with broader industrial demand and supply chain resilience goals. Government backing is yet another asset for this landscape, driving consistent business in this field. As of June 2025, reports published by the country’s government indicate that its minerals and metals policy has priority towards sustainable development in the minerals and metals sector by efficiently promoting partnerships with provinces, industry, Aboriginal communities, and other stakeholders. It also highlights the use and management of resources by including recycling as a strategy to provide secondary materials, reduce environmental impacts, and incorporate recovery into product design. Furthermore, this particular policy also supports Aboriginal involvement, science and technology, and international cooperation to ensure the industry’s long-term sustainability.

Europe Market Insights

Europe metal recycling market is considered to be one of the most influential and advanced industries internationally. The region’s growth is highly driven by strict waste regulations and well-established collection and processing networks. The region’s growth is also carried forward by domestic recycling capacities and strategies to secure material supply for manufacturing. As stated by IEA in October 2024, the European Critical Raw Materials Act, which was adopted by the European Commission in 2023, aims to secure a sustainable and resilient supply of critical raw materials by strengthening the EU value chain, diversifying imports, and enhancing monitoring and risk mitigation. It has set 2030 targets for domestic extraction, processing, and recycling, and promotes circularity through mandatory recycled content, improved collection, and recovery from waste, hence suitable for bolstering market growth in the years ahead.

The high volume of metal recycling influenced by rising investments in expanding recycling infrastructure and a strong industrial base that supports both ferrous and non-ferrous recovery are certain drivers responsible for uplifting the market in Germany. Policy frameworks in the country also encourage circular approaches in the manufacturing and construction sectors. In November 2025 IEA reported that the country’s National Circular Economy Strategy, which was announced in 2024, promotes high-quality metal recycling by concentrating on design for recyclability, developing knowledge on material flows, and optimizing technical sorting and processing systems. This particular policy supports economic viability for metal recovery, including from slag, and aligns with EU regulations such as the Critical Raw Materials Act and the Battery Regulation, hence making it suitable for standard market growth.

The UK metal recycling market has gained enhanced traction, highly driven by generous investments in advanced sorting technologies to improve recovery efficiency. Besides, the evolving national strategies mainly aim to balance domestic supply needs with export activities, particularly as electric arc furnace steel production grows and demands higher levels of scrap feed. In February 2025, the British Metals Recycling Association is encouraging the country’s government to improve business conditions for metal recyclers to support industry growth and the nation’s net-zero 2050 goals. A few of the main proposals were freer trade, lower energy costs, expanded kerbside collection for batteries, increased recycling facilities, and minimum recycled content in public projects. Furthermore, the BMRA highlights that metal recycling reduces CO₂, preserves natural resources, and that policy support could strengthen domestic steel supply while boosting sustainability across the metals value chain.

Key Metal Recycling Market Players:

- Nucor Corporation (U.S.)

- ArcelorMittal S.A. (Luxembourg)

- Sims Metal Management Ltd. (Australia)

- Commercial Metals Company (U.S.)

- Schnitzer Steel Industries, Inc. (U.S.)

- European Metal Recycling Ltd. (UK)

- Aurubis AG (Germany)

- Novelis Inc. (U.S.)

- Ferrous Processing & Trading Co. (U.S.)

- DOWA Holdings Co., Ltd. (Japan)

- American Iron & Metal Co. (U.S.)

- OmniSource Corporation (U.S.)

- Tata Steel Ltd. (India)

- Kuusakoski Group Oy (Finland)

- SA Recycling LLC (U.S.)

- REAL ALLOY (U.S.)

- PSC Metals (U.S.)

- HKS Metals BV (Netherlands)

- Sunrise Metal Recycling Ltd. (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Nucor Corporation is identified as one of the largest steel producers in the U.S. and a major force in metal recycling. The company operates as an extensive network of scrap yards and mini‑mills that recycle ferrous scrap into new steel products. In addition, Nucor makes investments in advanced melting technologies to improve yield and energy efficiency.

- ArcelorMittal is considered to be one of the world’s largest steel and mining companies, with a strong focus on metal recycling across its global operations. Besides, the company integrates recycling into its production process by utilizing scrap and electric arc furnaces to produce steel with reduced carbon emissions.

- Sims Metal Management Ltd. is a prominent player in this field that processes ferrous and non‑ferrous metals, serving both domestic and export markets. The company is mainly focused on expanding material recovery capabilities through investments in shredding, sorting, and logistics infrastructure.

- Commercial Metals Company is based in the U.S. and benefits from its operations in international markets as well. The firm has its strategic focus that includes enhancing operational efficiency through technology upgrades in shredding and sorting, and expanding scrap procurement channels.

- Schnitzer Steel Industries, Inc. is a central player in this field, which operates scrap processing facilities and steel fabrication plants by supplying recycled content to steel mills, foundries, and manufacturers. The company’s main strategy revolves around diversifying feedstock sources and leveraging logistics capabilities to serve both OEMs and industrial customers.

Below is the list of some prominent players operating in the global market:

The major players from North America, Europe, Asia Pacific dominate the international metal recycling market through extensive recycling networks and improved processing technologies. Leading firms such as Nucor Corporation, ArcelorMittal, and Sims Metal Management are making investments in capacity expansion, sustainability initiatives, and digital sorting systems with the main goal improve efficiency and reducing emissions. Meanwhile, the players from emerging markets such as Tata Steel are formalizing scrap supply chains with a primary goal support domestic steel production and circular economy goals. In September 2025, Aurubis AG reported that it had inaugurated its Aurubis Richmond facility in Georgia, which is the first U.S. multimetal recycling plant producing strategic metals such as copper, nickel, tin, and precious metals to support energy infrastructure, AI applications, data centers, and the defense industry, hence denoting a positive market outlook.

Corporate Landscape of the Metal Recycling Market:

Recent Developments

- In September 2o25 Aurubis AG secured a total of €200 million (approximately USD 220 million) loan from the European Investment Bank to expand copper refining in Bulgaria and enhance metal recycling at its Hamburg plant, supporting Europe’s critical raw materials supply.

- In June 2024, Mitsui & Co. announced that it had invested in MTC Business Private Ltd., to support India's growing demand for steel by expanding recycled metal supply chains, contributing to the decarbonization of the steel industry and the circular economy.

- Report ID: 3339

- Published Date: Feb 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.