Psychedelic Drugs Market Outlook:

Psychedelic Drugs Market size was valued at USD 4.3 billion in 2025 and is projected to reach USD 15.5 billion by the end of 2035, rising at a CAGR of 13.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of psychedelic drugs is estimated at 4.9 billion.

The worldwide psychedelic drugs market is re-emerging within the regulated clinical research framework, driven by the federal funding expanding clinical trials, and the measurable mental health burden. According to the World Health Organization, September 2025 data, nearly 1 in 7 people in the world live with a mental disorder, underscoring the sustained demand for novel psychiatric interventions. Moreover, as per the National Institute of Mental Health, September 2024 data, 23.1% of the U.S. population experiences mental illness, supporting the continued investigation of MDMA assisted therapies. On the other hand, the NLM May 2025 study shows that nearly 444,397,716 incident cases were registered regarding mental illness in 2021. Besides the increased grant support for the psychedelic research funding studies on psilocybin and related compounds for depression, substance use disorders, and trauma-related conditions via the National Institute on Drug Abuse and other institutes.

Moreover, there are hundreds of active and completed studies evaluating the psilocybin and related compounds across the indications, including major depressive disorder, treatment-resistant depression, and alcohol use disorder, indicating a structured clinical development pipeline. This research expansion aligns with the broader federal mental health spending as the U.S. national health expenditure reached USD 4.9 trillion in 2033, as per the American Hospital Association December 2024 data, with the mental health and substance use services representing a significant and growing share. Further, the federal research funding, expedited regulatory designations, and state-level program implementation are shaping a structured B2B ecosystem encompassing clinical research organizations, licensed manufacturers, behavioral health providers, and public health systems.

Key Psychedelic Drugs Market Insights Summary:

Regional Highlights:

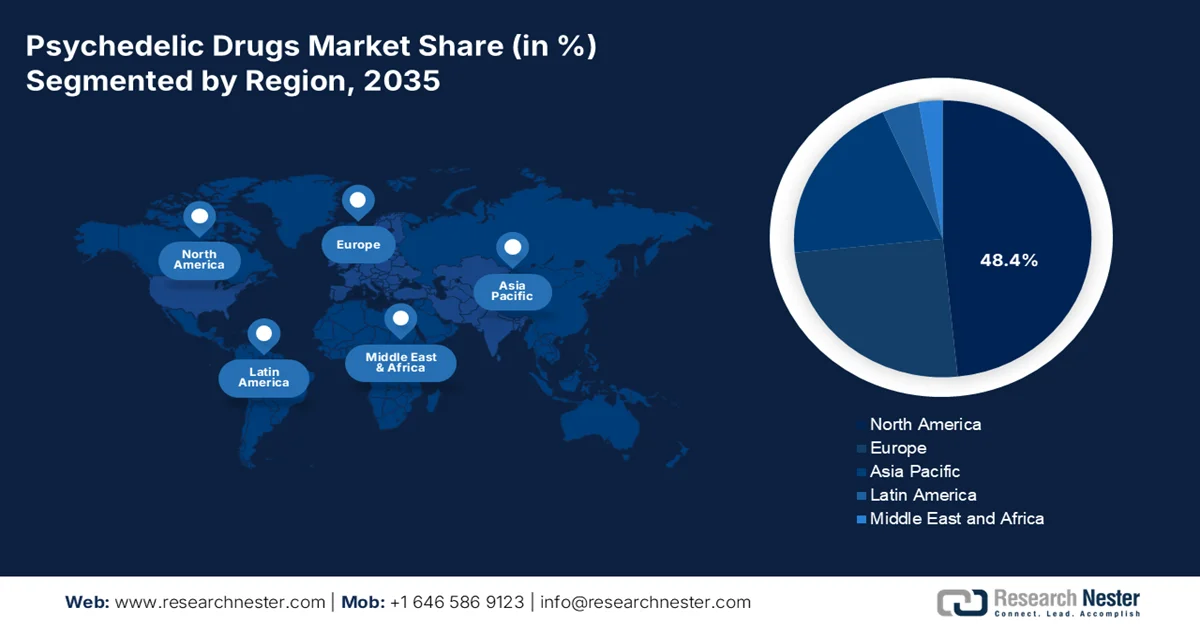

- By 2035, North America is anticipated to hold a 48.4% revenue share in the psychedelic drugs market, attributed to regulatory modernization, established research infrastructure, and concentrated government mental health funding.

- Asia Pacific is forecast to expand at a CAGR of 18.8% during 2026–2035, impelled by rising mental health awareness, government research initiatives, and evolving regulatory frameworks.

Segment Insights:

- By 2035, the synthetic segment is projected to capture a 68.5% share of the psychedelic drugs market, propelled by the pharmaceutical industry’s preference for chemically consistent, patentable, and scalable manufactured compounds.

- Over the forecast period 2026–2035, the oral sub segment is anticipated to lead the route of administration channel, driven by patient familiarity, ease of self-administration, and established clinical usage history.

Key Growth Trends:

- High disease burden of depression and serious mental illness

- Rising PTSD prevalence

Major Challenges:

- High treatment delivery costs

- Clinical trial design complexities

Key Players: COMPASS Pathways PLC, Pfizer Inc., Eli Lilly and Company, Cybin Inc., ATAI Life Sciences, MindMed (Mind Medicine Inc.), Janssen Pharmaceuticals, Johnson & Johnson, Jazz Pharmaceuticals plc, Hikma Pharmaceuticals PLC, F. Hoffmann-La Roche AG, Gilgamesh Pharmaceuticals, MiHKAL GmbH, Otsuka Pharmaceutical Co., Ltd., Bioxyne Limited, Clearmind Medicine Inc., Sunward Pharmaceutical Sdn Bhd, Mind Pharmaceuticals, Revive Therapeutics, Seelos Therapeutics.

Global Psychedelic Drugs Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.3 billion

- 2026 Market Size: USD 4.9 billion

- Projected Market Size: USD 15.5 billion by 2035

- Growth Forecasts: 13.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (48.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Canada, Germany, United Kingdom, Switzerland

- Emerging Countries: Japan, Australia, Netherlands, Spain, South Korea

Last updated on : 19 February, 2026

Psychedelic Drugs Market - Growth Drivers and Challenges

Growth Drivers

- High disease burden of depression and serious mental illness: The demand for psychedelic drugs market is structurally reinforced by the high psychiatric disease prevalence. According to the National Institute of Mental Health, September 2024 data, in 2022, 15.4 million adults lived with serious mental illness, and 10.2 million (66.7%) received mental health treatment in the past year. Persistent treatment resistance in a subset of these patients has intensified government-backed exploration of alternative interventions. Public health systems are under pressure to reduce long-term disability and hospitalization costs associated with chronic depression. For manufacturers and clinical service providers, high untreated or treatment-resistant populations translate into scalable institutional demand once regulatory pathways are secured.

U.S. Adults with Serious Mental Illness

|

Metric |

Percentage |

|

Male |

59.3 |

|

Female |

71.4 |

|

Overall |

66.7 |

Source: NIMH September2024

- Rising PTSD prevalence: The rising cases of PTSD are the key demand catalyst in the psychedelic drugs market. According to the U.S. Department of Veterans Affairs, March 2026 data, nearly 6% of the U.S. population will experience PTSD during their lifetime, while the prevalence among the veterans can range significantly depending on the service era. On the other hand, significant fund is allocated toward the mental health services. Moreover, the FDA has granted breakthrough therapy designation to the MDMA assisted therapy for PTSD, surging the clinical development pathways. Further, the veteran health systems represent early institutional adoption channels due to concentrated patient pools and federal reimbursement backing. Government-backed veteran healthcare financing significantly lowers commercialization risk for PTSD-focused psychedelic therapies.

- Funding for mental health research: The government's investment in mental health research is expanding the scientific foundation for psychedelic therapies. The NIMH 2024 reports depict that the NIMH supports more than 3,000 research grants and sustains the neuroscience infrastructure necessary for psychedelic research. Moreover, the President's Budget request is USD 2.5 billion in 2024. This institutional commitment provides the foundational science that de-risks subsequent clinical development by private manufacturers. The National Institute on Drug Abuse also contributes by funding studies on therapeutic uses of controlled substances, creating a strong public research ecosystem that validates the therapeutic potential of psychedelic compounds and promotes the private sector investment in late-stage clinical trials.

Challenges

- High treatment delivery costs: The intensive therapeutic model required for the psychedelic treatment creates prohibitive scalability costs. The take-home antidepressants a psychedelic session requires hours of professional supervision, preparation, and integration support, occupying clinical space and trained staff for an entire day. Moreover, the manufacturers in the psychedelic drugs market face pressures to demonstrate cost-effectiveness while the per-patient delivery cost remains high.

- Clinical trial design complexities: Functional unbinding presents a methodological challenge in the psychedelic drugs market that complicates regulatory approval pathways. In standard double-blind trials, the participants and researchers can't know who received the drug versus placebo, but with the psychedelics, the profound subjective experience makes the blinding nearly impossible. This uncertainty creates the investor's hesitation, as the path to approval remains less clear than for conventional medicines.

Psychedelic Drugs Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

13.7% |

|

Base Year Market Size (2025) |

USD 4.3 billion |

|

Forecast Year Market Size (2035) |

USD 15.5 billion |

|

Regional Scope |

|

Psychedelic Drugs Market Segmentation:

Source Segment Analysis

The synthetic segment is expected to dominate the psychedelic drugs market, accounting for a 68.5% share by 2035. This dominance is driven by the pharmaceutical industry’s preference for chemically consistent patentable and scalable manufactured compounds over variable natural products. Moreover, the regulatory bodies, such as the FDA, are more easily able to evaluate the standardized drug substances, making synthetic analogs for approval. According to the NLM November 2023 study, lysergic acid diethylamide is a laboratory-manufactured synthetic psychedelic, and magic mushrooms fall under the natural source segment since psilocybin occurs naturally in certain mushroom species within the market.

Route of Administration Segment Analysis

The oral sub segment is leading the route of administration channel in the psychedelic drugs market. Its dominance is attributed to patient familiarity, ease of self-administration, and an established history of use in both the clinical and research settings. The oral routes, including the capsules and sublingual tablets, allow for controlled release and are the primary method being tested in the major clinical trials. Moreover, the oral formulations offer advantages in terms of scalable manufacturing, convenient storage, and simplified distribution compared to parenteral routes, making them commercially attractive for large patient populations. Further regulatory pathways are often more streamlined for oral dosage forms due to well-established pharmacokinetic profiles and safety data frameworks supporting faster clinical adoption and market penetration.

End user Segment Analysis

The specialty mental health centers are expected to be the leading sub-segment in the psychedelic drugs market. The segment is dominating as the psychedelic-assisted therapy requires a controlled clinical environment with specially trained staff to administer treatment and provide the necessary psychological support before, during, and after sessions. These specialized centers are better equipped than the general hospitals to meet the rigorous infrastructure is underscored by the widespread prevalence of mental health disorders. According to the PIB November 2025 data, nearly 10.6% of adults in India are living with a mental health disorder. This growing patient pool, combined with increasing government focus on expanding mental healthcare infrastructure and trained psychiatric professionals, is further strengthening the demand for specialized, supervised psychedelic treatment settings.

Our in-depth analysis of the psychedelic drugs market includes the following segments:

|

Segment |

Subsegments |

|

Drug Type |

|

|

Source |

|

|

Application |

|

|

Route of Administration |

|

|

Distribution Channel |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Psychedelic Drugs Market - Regional Analysis

North America Market Insights

The North America is projected to maintain its dominance in the market with the regional revenue share of 48.4% by 2035. The market is driven by regulatory modernization, established research infrastructure, and concentrated government mental health funding. The region benefits from the FDA breakthrough therapy designations for multiple psychedelic compounds and an expanding network of state-regulated psilocybin service centers. Canada’s existing special access program for psychedelic therapies and Health Canada’s clinical trials authorizations create a favorable regulatory environment. The presence of major clinical-stage biotechnology companies in the U.S. and Canada is surging the drug development timelines. According to the NLM study in August 2023, the healthcare cost for the mental health patient was nearly USD 4 million in 2021, indicating an active growth in the psychedelic drugs market in North America.

The surging federal research investment, rising behavioral health burden, and structured regulatory oversight are fueling the psychedelic drugs market in the U.S. According to the NIH's September 2024 study, only 3.0 million people in the U.S. received treatment for the mental illness, highlighting a substantial untreated population. The treatment access disparities are evident with the makes 41.6% with the AMI receiving care compared to females, indicating a demographic gap that alternative therapeutic delivery models may seek to address. On the other hand, the U.S. Department of Veterans Affairs in March 2025 reports that 5% people had experienced PTSD annually. Moreover, the CDC August 2023 data shows that suicide mortality increased from 48,183 deaths in 2021 to 49,449 in 2022, a 2.6% rise. These public health metrics reinforce ongoing federal mental health investment and regulatory engagement around innovative psychiatric treatments, thereby surging the market growth.

Mental Illness Treatment Received Among the U.S. Population by Age

|

Age |

Percentage |

|

18-25 |

49.1 |

|

26-49 |

50.0 |

|

50+ |

52.7 |

Source: NIMH September2024

The rising mental health burden, federal health expenditure growth, and structured regulatory exemptions for controlled substances are propelling the psychedelic drugs market in Canada. According to the Government of Canada, in September 2024, 5 million Canadians aged 15 and older met diagnostic criteria for a mood, anxiety, or substance use disorder in 2022. Additionally, the federal Budget 2023 committed USD 198.3 billion over 10 years in health transfers to provinces based on the Government of Canada's March 2023 data, including targeted funding to improve mental health and substance use services. These commitments, combined with formalized compassionate access pathways and increasing institutional research activity, position Canada as a regulated clinical development environment for market growth.

APAC Market Insights

The Asia Pacific is projected to experience the fastest growth and is poised to grow at a CAGR of 18.8% during the forecast period 2026 to 2035. The market is driven by the rising mental health awareness, government research initiatives, and evolving regulatory frameworks. Japan has established clear clinical trial pathways with multiple pharmaceutical companies conducting neuroscience research via PMDA consultants. On the other hand the China maintains strict controlled substance regulations and supports research into novel CNS treatments via government-funded institutions. The region benefits from established pharmaceutical manufacturing infrastructure and growing government investment in mental health services, positioning a crucial and futuristic psychedelic drugs market in the Asia Pacific.

The psychedelic drugs market in India is supported by the rapid expansion of the public mental health infrastructure, insurance alignment, and growing adoption of interventional psychiatry models. According to the MOHFW March 2025 data, the District Mental Health Programme has been sanctioned across 767 districts under the National Mental Health Programme, strengthening outpatient, inpatient, and community-based psychiatric services nationwide. Moreover, more than 1.75 lakh Ayushman Arogya Mandirs now include mental, neurological, and substance use disorder services under Comprehensive Primary Health Care. Access is further supported via the Tele MANAS initiative with 53 operational cells handling over 19.67 lakh calls. Additionally, the NLM December 2024 study indicates that with an estimated 80% psychiatric treatment gap, expanding institutional infrastructure, digital outreach, and insurance coverage collectively position India as an evolving market for advanced, regulated psychiatric interventions in the long term.

The strict narcotics control laws, expanding mental health service capacity, and rising psychiatric disease burden are accelerating the psychedelic drugs market in China. Under China’s Narcotics Control Law, psychedelic substances are classified as controlled drugs, and clinical research requires central regulatory approval through national health and drug authorities, limiting commercial activity to approved scientific settings. According to the Asia Society, December 2022 data, China has more than 95 million people living with depression, making it one of the largest affected populations globally. Moreover, the People’s Republic of China's July 2025 report states that the public health insurance coverage has also broadened, with the basic medical insurance system covering over 95% of the population, improving access to reimbursable psychiatric services, and driving demand within large state-run hospital networks.

Europe Market Insights

The psychedelic drugs market in Europe is significantly expanding and is defined by coordinated regulatory engagement and substantial public funding for mental health innovation. The European Medicines Agency’s Committee for Medicinal Products for Human Use has provided scientific advice to multiple psychedelic drug developers, creating a harmonized regulatory pathway across the member states. The countries are establishing compassionate use frameworks with Germany's Federal Institute for Drugs and Medical Devices and the United Kingdom's Medicines and Healthcare products Regulatory Agency, engaging with developers on regulatory pathways. The market benefits from concentrated research infrastructure with academic institutions in Switzerland, the UK, and Germany conducting government-funded trials investigating psilocybin for depression and anxiety disorders, creating a foundation for future commercial adoption across the region's national health systems.

The rising economic burden, disability impact, regulatory approach, and integrated healthcare infrastructure are propelling the psychedelic drugs market in Germany. According to the NLM article published in October 2024 in Germany, the healthcare costs range from €524.5 million to €3.3 billion annually, while depression contributes an additional €1 to €5.2 billion in direct costs, with indirect costs from absenteeism and social benefits reaching €10 to €16 billion per year. PTSM patients incur average per-patient costs of approximately €43,000, nearly three times higher than individuals without PTSD, largely due to prolonged illness duration and high comorbidity rates of 50% to 100% with conditions such as major depressive disorder and substance use disorder. Moreover, the PTSD accounts for roughly 200,000 disability adjusted life years annually, while the depression contributes 470,000 DALYs, underscoring the sustained demand for the psychedelic drugs.

The psychedelic drugs market in UK is driven by active clinical development, NHS integration, and regulated deployment of prescription digital and investigational therapies for depression. The launch of Rejoyn in June 2025, a prescription-only digital therapeutic for depressive disorder within select NHS Trusts, indicates the growing institutional acceptance of the regulated non-traditional treatment modalities in the publicly funded care settings. On the other hand, the NIHR Oxford Health Clinical Research Facility initiated the COMP006 Phase III study evaluating COMP360 psilocybin for the treatment of treatment-resistant depression in October 2024, targeting patients who have not responded to at least two antidepressants. The study includes a 52-week follow-up period, reflecting long-term outcome assessment within a controlled NHS-affiliated research environment. The combination of NHS-based pilot deployments, MHRA-regulated clinical trials, and late-stage international Phase III programs signals that the UK is positioning itself as a structured clinical adoption market.

Key Psychedelic Drugs Market Players:

- COMPASS Pathways PLC (UK)

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Cybin Inc. (Canada)

- ATAI Life Sciences (Germany)

- MindMed (Mind Medicine Inc.) (U.S.)

- Janssen Pharmaceuticals (Belgium)

- Johnson & Johnson (U.S.)

- Jazz Pharmaceuticals plc (Ireland)

- Hikma Pharmaceuticals PLC (UK)

- F. Hoffmann-La Roche AG (Switzerland)

- Gilgamesh Pharmaceuticals (U.S.)

- MiHKAL GmbH (Switzerland)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Bioxyne Limited / Breathe Life Sciences (Australia)

- Clearmind Medicine Inc. (Israel)

- Sunward Pharmaceutical Sdn Bhd (Malaysia)

- Mind Pharmaceuticals (U.S.)

- Revive Therapeutics (Canada)

- Seelos Therapeutics (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- COMPASS Pathways is a clinical-stage biotechnology company focused on advancing the psychedelic drugs market via its proprietary COMP360 psilocybin therapy. The company is conducting the largest randomized controlled double blind psilocybin treatment clinical program undertaken for the treatment resistant depression. In 2024, the company invested over USD 119,039 in research and development.

- Pfizer Inc. is a global leader in the psychedelic drugs market and maintains a significant presence via its extensive research infrastructure and manufacturing capabilities. As one of the major players in the market, the company's involvement signals the growing mainstream acceptance of psychedelic-based therapeutics. According to the 2024 annual report, the company has made a net savings of USD 63,627 million.

- Eli Lilly and Company brings decades of experience in central nervous system therapeutics to the evolving psychedelic drugs market. With the rich history and a strong portfolio of mental health treatment, including antidepressants, Lilly possesses the clinical development expertise and commercial infrastructure that could prove valuable as psychedelic therapies advance toward regulatory approval

- Cybin Inc has established itself as a leader in the psychedelic drugs market via its proprietary molecule platform and comprehensive intellectual property portfolio. The company is advancing a deuterated psilocin analog for major depressive disorder with the Breakthrough Therapy designation from the FDA.

- ATA Life Sciences is a clinical-stage biopharmaceutical company pursuing a diversified portfolio strategy within the psychedelic drugs market, with operations based in both the U.S. and Germany. The company has recently reported positive topline data for treatment-resistant depression, demonstrating rapid, robust, and durable antidepressant effects with a single dose.

Here is a list of key players operating in the global market:

The psychedelic drugs market is defined by a dynamic mix of specialized biotech firms and established pharmaceutical giants, with the competitive landscape heavily concentrated in North America and Europe. Strategic initiatives are largely focused on clinical stage development, with the key players advancing in the psychedelic compounds via late-stage trials for indications such as treatment-resistant depression and PTSD. A notable trend is the increasing number of strategic collaborations and partnerships, indicating growing interest from Big Pharma in novel psychoplastogens and CNS treatments. For example, in September 2023, Cybin announced the agreement with Fluence to support the scaling of EMBARK training for the CYB003 phase 3 trial. Additionally, companies are actively securing intellectual property and expanding their manufacturing capabilities to establish strong market positions.

Corporate Landscape of the Psychedelic Drugs Market:

Recent Developments

- In August 2025, AbbVie and Gilgamesh Pharmaceuticals Inc. announced a definitive agreement under which AbbVie will acquire Gilgamesh's lead investigational candidate, currently in clinical development for the treatment of patients with moderate-to-severe major depressive disorder (MDD).

- In November 2024, Monash biotech spinout develops a new class of drugs to combat depression, the world’s shadow pandemic. The company is pioneering the development of next-generation medicines, targeting serotonin signalling in the brain, which plays a crucial role in mood regulation.

- In March 2024, the biopharmaceutical company Mind Medicine (MindMed) Inc. announced that the U.S. Food and Drug Administration (FDA) has granted breakthrough therapy designation to one of the company’s products in development, MM120, an innovative LSD formulation, targeting the treatment of Generalized Anxiety Disorder.

- Report ID: 4153

- Published Date: Feb 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Psychedelic Drugs Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.