Medical Imaging Market Outlook:

Medical Imaging Market size was valued at USD 43.8 billion in 2025 and is projected to reach USD 74.1 billion by the end of 2035, rising at a CAGR of 5.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of medical imaging is estimated at USD 46.1 billion.

The global market is shaped by the public health demand, demographic pressures, and sustained government investment in diagnostic infrastructure. The aging populations and the rising burden of non-communicable diseases are increasingly driving the imaging volumes across hospitals and diagnostic centers. According to the WHO, October 2025 data, 1 in 6 individuals globally will be aged above 60 years. Moreover, the November 2025 WHO report depicts that the non-communicable diseases account for approximately 74% of the global deaths, with cardiovascular disease, cancer, and neurological disorders all relying on imaging for diagnosis, staging, and monitoring. Further, the federal investment in hospital infrastructure, trauma care, oncology networks, and stroke centers continues to sustain baseline demand for advanced imaging capacity across public and private healthcare systems.

Besides, the high prevalence of neurological disorders in the U.S. is driving the growth of the medical imaging market. According to the NLM study in November 2025, nearly 80.3 million individuals in the U.S. are affected by nervous system disorders, reflecting the urgent need for MRI, CT, PET, and functional imaging for diagnosis, monitoring, and disease progression assessment. Moreover, stroke, Alzheimer’s disease, migraine, and diabetic neuropathy are the key contributors to DALYs and require longitudinal and follow-up imaging, hence increasing scan volumes over time. Overall, the market is sustained by the institutional procurement cycles, public healthcare budgets, and policy-driven demand tied to chronic disease management, emergency care, and population-level screening rather than short-term commercial dynamics.

U.S. Nervous System Disorders Burden

|

Metric |

Data Point |

|

Total U.S. population |

332.7 million |

|

Population affected by nervous system disorders |

180.3 million |

|

Share of population affected |

~54% of U.S. population |

|

Total disability-adjusted life years (DALYs) |

16.6 million |

|

Tension-type headache |

121.9 million |

|

Migraine |

57.7 million |

|

Diabetic neuropathy prevalence |

17.1 million |

|

Stroke |

3.9 million DALYs |

|

Alzheimer’s disease & dementias DALYs |

3.3 million DALYs |

|

Change in prevalence vs. 1990 |

−0.2% |

|

Change in attributable deaths vs. 1990 |

−14.6% |

|

Change in years lived with disability (YLDs) vs. 1990 |

+9.8% |

Source: NLM November 2025

Key Medical Imaging Market Insights Summary:

Regional Highlights:

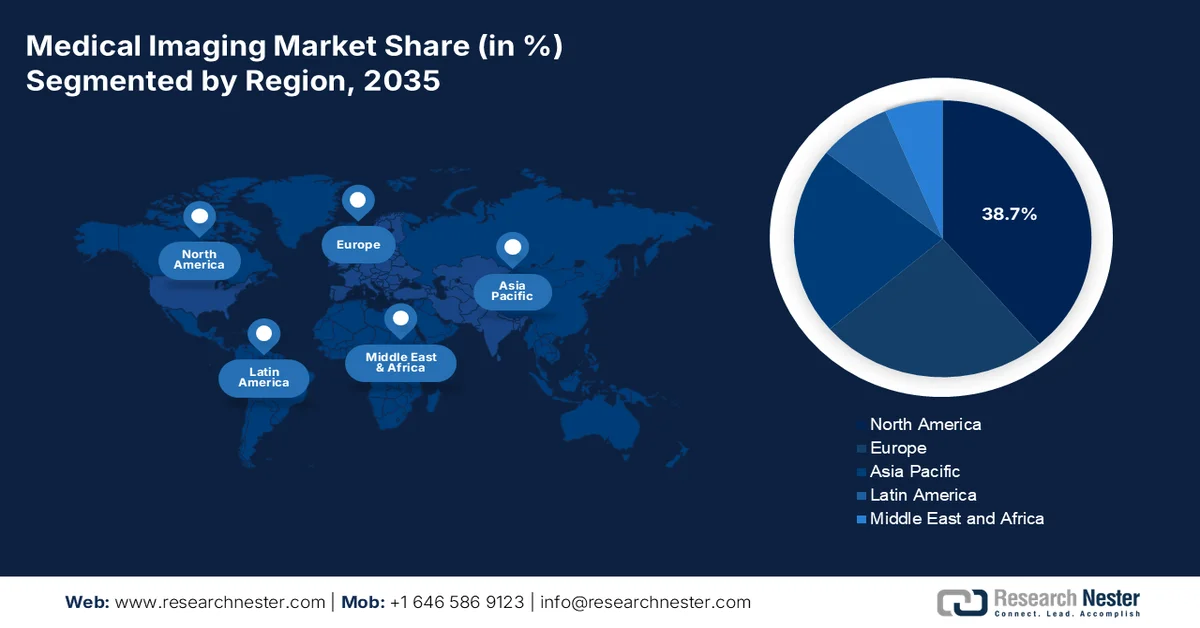

- North America is projected to command a 38.7% revenue share by 2035 in the medical imaging market, attributed to rapid adoption of advanced technologies and substantial government and private healthcare investments.

- Asia Pacific is anticipated to register a CAGR of 7.2% during 2026–2035, fueled by rising healthcare expenditure and significant government investments in public health infrastructure.

Segment Insights:

- The fixed or stationary systems segment of the medical imaging market is projected to account for a 70.3% share by 2035, propelled by sustained hospital capital investments and government-backed infrastructure upgrades aimed at expanding tertiary and quaternary care capacity.

- The hospitals sub segment is anticipated to secure the largest share of the market by 2035, driven by high patient inflow and the availability of skilled radiologists with 24/7 diagnostic capability.

Key Growth Trends:

- Rising government expenditure on diagnostic and hospital infrastructure

- Expansion of cancer screening programs

Major Challenges:

- Stringent regulatory and approval hurdles

- Reimbursement uncertainty and pricing pressure

Key Players: GE HealthCare, Siemens Healthineers, Philips, Canon Medical Systems, Fujifilm Healthcare, Hologic, Agfa-Gevaert, Samsung Medison, Shimadzu, Mindray Medical, Carestream Health, Esaote, Varex Imaging, Konica Minolta, Planmeca, Bruker, Canon Inc., ContextVision, MIM Software, Siemens AG

Global Medical Imaging Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 43.8 billion

- 2026 Market Size: USD 46.1 billion

- Projected Market Size: USD 74.1 billion by 2035

- Growth Forecasts: 5.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: - United States, Germany, Japan, China, United Kingdom

- Emerging Countries: - India, South Korea, Brazil, Singapore, Canada

Last updated on : 11 February, 2026

Medical Imaging Market - Growth Drivers and Challenges

Growth Drivers

- Rising government expenditure on diagnostic and hospital infrastructure: The public healthcare budgets remain the primary demand anchor for the market, mainly in tertiary hospitals and trauma centers. According to the OECD November 2025 data, the average health expenditure across the member countries reached 9.3% of GDP in 2024, with diagnostics embedded within the capital and outpatient care budgets. In the U.S., the CMS January 2026 data depict that healthcare spending exceeded USD 5.3 trillion in 2024, with hospital and outpatient diagnostic services among the fastest-growing categories. Moreover, Europe governments continue to allocate structural funds to modernize the imaging infrastructure under the national cancer and cardiovascular strategies. These investments directly support the procurement of CT, MRI, and ultrasound systems through public tenders rather than discretionary purchases

- Expansion of cancer screening programs: The government-backed screening initiatives are a sustained demand driver for the medical imaging market, mainly for CT, MRI, mammography, and nuclear imaging. According to the WHO's February 2024 data, 1 in 5 people develop cancer in their lifetime, prompting countries to expand early detection programs. In the EU, the population-based cancer screening is formally supported under the Europe’s Beating Cancer Plan, increasing the imaging volumes across the public hospitals. In the U.S., the CDC indicates the breast, cervical, and lung cancer screening programs that rely on diagnostic imaging. Further, the demand growth is volume-led rather than price-led, favoring suppliers with scalable installation, maintenance, and workflow integration capabilities.

Global Cancer Mortality by Cancer Type

|

Cancer Type |

Deaths (Million) |

Share of Total Cancer Deaths (%) |

|

Lung cancer |

1.8 |

18.7% |

|

Colorectal cancer |

0.9 |

9.3% |

|

Liver cancer |

0.76 |

7.8% |

|

Breast cancer |

0.67 |

6.9% |

|

Stomach cancer |

0.66 |

6.8% |

Source: WHO February 2024

- Diagnostic access in low- and middle-income countries: The NLM October 2021 study depicts that nearly 47% of the population in the global has limited access to diagnostic tests and imaging, prompting multilateral and government-led capacity building initiatives. The program is supported by the WHO and national ministries that focus on deploying basic imaging in public hospitals. These initiatives are procurement-driven and volume-focused. Besides, the government and multilateral agencies are prioritizing the decentralized imaging deployment cost-effectively, including district hospitals and primary care centers, to reduce the late-stage disease diagnosis. Moreover, the WHO 2026 data shows that basic imaging access can address 70% of clinical diagnostics needs in low-resource settings, making a sustained demand driver in the market rather than one time infrastructure investment.

Challenges

- Stringent regulatory and approval hurdles: Entering the medical imaging market requires a complex, lengthy, and costly regulatory pathway. The process demands extensive clinical data, rigorous quality system compliance, and significant investment. The delays can delay the product launches and revenue projections. Various top companies have undergone a multi-year FDA process to expand their indicators. Though the FDA review for 510(k) can take months, the complex submissions can take far longer, tying up capital.

- Reimbursement uncertainty and pricing pressure: Profitable market entry is contingent on securing favorable reimbursement codes from payers such as the U.S. CMS. Without established CPT codes, hospitals cannot bill for procedures using new technology. The pricing pressure is also intense; CMS and other global health systems frequently cut reimbursement rates. Top players have overcome this by providing robust clinical evidence for their 3D mammography, which has led to a unique reimbursement code, but such victories require extensive, costly health economics studies.

Medical Imaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

5.4% |

|

Base Year Market Size (2025) |

USD 43.8 billion |

|

Forecast Year Market Size (2035) |

USD 74.1 billion |

|

Regional Scope |

|

Medical Imaging Market Segmentation:

Portability Segment Analysis

The fixed or stationary systems are projected to hold the largest share value of 70.3% in the market by 2035. These high-capability systems, such as 3T MRI and advanced CT scanners, are vital for the comprehensive diagnosis in core clinical settings. A recent advancement in the fixed medical imaging system was in August 2022, when GE Healthcare released the next-generation premium fixed X-ray system to bring a personal assistant to radiology departments. Moreover, the dominance of the fixed system is supported by the sustained hospital capital investments and government-backed infrastructure upgrades aimed at expanding tertiary and quaternary care capacity. Further, the fixed systems enable higher patient throughput, superior image resolution, and seamless integration with PACS and AI-based diagnostic workflows, reinforcing their preference over portable alternatives.

End user Segment Analysis

The hospitals sub segment is leading in the end-user segment and is expected to hold the largest share value in the market. The dominance is driven by the role as centralized hubs for critical and complex diagnostic procedures requiring a full array of high-end fixed imaging modalities. Their significant capital allows for investments in the latest MRI, CT, and hybrid PET CT systems. Moreover, the growth is fueled by the high patient inflow, the integration of advanced imaging with electronic health records, and the establishment of specialized imaging centers within the hospital networks. According to the NLM June 2022 study, nearly 72 million scans were performed in U.S. hospitals, representing a substantial portion of all imaging volumes and reinforcing the hospital's pivotal market position. Moreover, the availability of skilled radiologists and 24/7 diagnostic capability is prompting hospitals to adopt medical imaging technologies.

Application Segment Analysis

The oncology sub-segment is leading in the market. The segment is driven by the critical and growing reliance on medical imaging across the cancer care sector, from screening and diagnosis to staging, treatment planning, and therapy response monitoring. The increasing global cancer prevalence, with the technological advancement in precision imaging, such as PET-CT and PET MRI, boosts its top position. Moreover, these modalities provide vital metabolic and anatomical data for personalized medicine. As per the CDC January 2025 data, nearly 36.7 million new cancer cases were reported in the U.S., indicating the immense and sustained clinical demand for advanced diagnostic imaging in oncology. Moreover, the rising adoption of AI-enabled analysis of images enhances the diagnostic accuracy and treatment outcomes, boosting the imaging utilization in cancer care pathways.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Modality/Product |

|

|

Application |

|

|

End user |

|

|

Technology |

|

|

Portability |

|

|

Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Medical Imaging Market - Regional Analysis

North America Market Insights

North America is the dominant one and is poised to hold the regional revenue market share of 38.7% by 2035. The market is driven by the rapid adoption of advanced technology, high healthcare expenditure, and a strong focus on diagnostic precision. The key drivers include the high prevalence of chronic diseases, favorable reimbursement frameworks for advanced imaging procedures, and substantial government and private investment in healthcare infrastructure. The dominant trend is the strategic shift from the volume based to value-based care, surging the integration of AI and cloud-based solutions to improve operational efficiency and diagnostic accuracy. Moreover, the market growth is boosted by the continuous technological advancement and demographic trends.

The sustained federal healthcare spending, stable reimbursement, and rising diagnostic utilization are driving the medical imaging market in U.S. According to the NLM January 2026 study, 2,041,910 new cancer cases were registered with 618,120 cancer deaths in the U.S. in 2025, highlighting the rising need for medical imaging devices for diagnosis. On the other hand, the CDC's October 2024 reports that nearly 919,032 people died from cardiovascular disease in 2023, where diagnostic imaging is heavily embedded. Further, the NLM December 2025 has indicated that the U.S. FDA has approved over 690 machine learning enabled medical devices supporting the continuous replacement and upgrade cycles. Moreover, the active approval of the medical imaging devices also surges the demand for advanced technological medical imaging devices. Overall, the data highlights that the market is showing active growth in the country.

Recent FDA PMA Approvals of Medical Imaging Devices

|

Product Name |

Company (PMA Applicant) |

Approval Date |

Clinical / Market Relevance |

Market Segment Linkage |

|

VARIPULSE Platform (Catheter, Generator, Pump, Interface Cable) |

Biosense Webster, Inc. |

November 6, 2024 |

Supports image-guided cardiac electrophysiology procedures; used alongside real-time imaging and mapping systems |

Image-guided interventions, interventional cardiology, hospital EP labs |

|

Oncomine Dx Target Test |

Life Technologies Corporation |

October 17, 2024 |

Companion diagnostic enabling molecular profiling to guide oncology treatment decisions |

Molecular diagnostics, imaging-supported precision oncology workflows |

|

TruSight Oncology Comprehensive |

Illumina, Inc. |

August 21, 2024 |

Comprehensive genomic profiling test used in oncology diagnosis and treatment planning |

Advanced diagnostics, oncology decision-support integrated with imaging |

Source: FDA

High MRI utilization capacity constraints and an aging installed base are driving the market in Canada. According to the NLM August 2024 study, Canada operates 432 MRI units across 11 jurisdictions, translating to 10.8 units per million people, placing the country in the bottom quartile of OECD nations for MRI availability. Despite limited unit density, demand remains strong, with 2.21 million publicly funded MRI examinations performed in FY 2022 to 2023, representing 55.6 exams per 1,000 population and a 4.3% increase. High operational intensity further underscores demand, as MRI systems run 15.3 hours per day on average, with 76% of sites operating on weekends. Moreover, the average equipment age of 8.4 years, with over 37% of systems older than 10 years, supports near- to mid-term replacement demand. Collectively, constrained capacity, rising exam volumes, and aging systems position MRI as a key growth segment within Canada’s market.

APAC Market Insights

The Asia Pacific market is growing rapidly and is poised to grow at a CAGR of 7.2% during the forecast period 2026 to 2035. The market is driven by the rising healthcare expenditure, expanding access to insurance, and significant government investments in public health infrastructure. The key demand drivers include a large and aging population, increasing prevalence of chronic diseases, and efforts to bridge the urban-rural healthcare divide through the establishment of tiered diagnostic networks. A major trend is the rapid adoption of mid-tier and value-based imaging systems tailored for high-volume use in emerging economies, alongside premium modality adoption in mature markets like Japan and South Korea. Local manufacturing initiatives, particularly in China and India, are increasing competition and influencing pricing.

Rising diagnostic demand and continued reliance on imported high-end imaging systems is driving the medical imaging market in India. According to the Medical Dialogue August 2025 data, India has spent over USD 25 billion between 2020 to 2021 and 2024 to 2025 on imports of electromedical equipment, including diagnostic imaging devices, with annual imports consistently exceeding USD 5 billion, underscoring sustained procurement demand. Moreover, the CCI August 2024 report depicts that the MRI market remains highly consolidated with Siemens holding the majority of the share of 34.22% reflecting strong incumbent dominance driven by installed base and service contracts. Further the high import dependence estimated by the government at over 85% of the medical devices market continues to shape pricing and supply dynamics. Overall, India’s market growth is driven by expanding diagnostic volumes, replacement demand, and infrastructure scale-up, rather than rapid domestic manufacturing expansion in the near term.

Market Share of MRI Manufacturers

|

Rank |

Manufacturer |

Market Share (% of Revenue) |

|

1 |

Siemens |

34.22% |

|

2 |

GE Healthcare |

24.14% |

|

3 |

Philips |

21.03% |

|

4 |

United Imaging Healthcare Co., Ltd. |

8.14% |

|

5 |

Hitachi / Fujifilm |

4.24% |

Source: CCI August 2024

The China medical imaging market is expanding rapidly, driven by a rising chronic disease burden and concentrated demand in tertiary hospitals, where advanced imaging is most heavily utilized. According to the NLM October 2023 study, over 60% of adults in the country live with at least one chronic disease, significantly increasing demand for CT and MRI across neurology, oncology, and infectious disease care, including meningitis, where imaging is essential for assessing complications and treatment response. Moreover, nearly 60% of patients seek care at tertiary hospitals, which represent less than 13% of total hospitals, indicating an imaging workload. At the same time, medical imaging data volumes are growing at approximately 30% annually, while the radiologist workforce is expanding at 4%, resulting in one radiologist per 70,000 people. Overall, China’s market growth is utilization- and capacity-stress driven, with strong momentum in hospital-based imaging to manage rising neurological and infectious disease caseloads.

Europe Market Insights

The medical imaging market in Europe is expanding rapidly and is defined by the mature, stable demand heavily influenced by the government healthcare budgets and stringent EU-wide regulatory frameworks. Growth is driven by the region's aging population and the consequent rise in the chronic diseases requiring advanced diagnostics. A key trend is the strategic modernization of the aging imaging infrastructure supported by EU funding initiatives like the EU4Health programme, which allocates substantial capital for health system resilience, including diagnostic equipment. Innovation is directed toward AI integration for workflow optimization and dose reduction, as well as the expansion of point-of-care ultrasound. Sustainability and lifecycle management are becoming critical purchasing criteria for public health systems.

The medical imaging market in Germany is expanding and is supported by the high diagnostic utilization, an aging population, and the strong hospital-based imaging capacity. According to the World Bank 2025, the share of the population aged 65 years and older increased from 23% in in 2024, driving sustained demand for imaging in oncology, neurology, and musculoskeletal care. Further, the Health System facts in February 2025 have depicted that 35 million have undergone MRI scans, supporting high procedure throughput rather than access expansion. Moreover, the hospital inpatient and outpatient case volumes rebounded post-pandemic, with diagnostic imaging remaining a core component of DRG-based hospital workflows. Together, high installed-base density, demographic-driven utilization, and strong hospital reliance on imaging position Germany’s market growth as utilization and replacement-led, favoring equipment upgrades, software integration, and service contracts over new site creation.

Medical Imaging Equipment Availability and Utilization

|

Imaging Modality |

Units per Million Population |

Exams per 1,000 Population |

|

CT Scanners |

36 |

160 |

|

MRI Systems |

35 |

158 |

|

PET Scanners |

2 |

2 |

Source: Health System Facts February 2025

The UK medical imaging market is expanding steadily and is driven by the rising diagnostic volumes, aging demographics, and sustained reliance on imaging to address care backlogs. The diagnostic imaging activity increased year over year, with millions of CT and MRI scans performed annually as part of the elective recovery and cancer pathways. Further, the Office for National Statistics April 2023 data shows that the population aged above 65 years exceeded 3.3 million, increasing demand for imaging in oncology, cardiovascular disease, and musculoskeletal care. Moreover, UK continues to operate with lower imaging equipment density than many peer countries, reinforcing high utilization per system rather than capacity surplus. This combination of elevated scan volumes, demographic pressure, and constrained installed base positions the UK market for growth driven by throughput optimization, equipment replacement, and extended operating hours rather than rapid site expansion.

Key Medical Imaging Market Players:

- GE HealthCare (U.S.)

- Siemens Healthineers (Germany)

- Philips (Netherlands)

- Canon Medical Systems (Japan)

- Fujifilm Healthcare (Japan)

- Hologic (U.S.)

- Agfa-Gevaert (Belgium)

- Samsung Medison (South Korea)

- Shimadzu (Japan)

- Mindray Medical (China)

- Carestream Health (U.S.)

- Esaote (Italy)

- Varex Imaging (U.S.)

- Konica Minolta (Japan)

- Planmeca (Finland)

- Bruker (U.S.)

- Canon Inc. (Japan)

- ContextVision (Sweden)

- MIM Software (U.S.)

- Siemens AG (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- GE HealthCare is a dominating leader in the market, using its vast portfolio across modalities such as CT, MRI, and ultrasound. The company is actively embedding AI across its platforms via its Edison ecosystem and forming partnerships to drive efficiency and precision in diagnosis. According to the 2024 annual report, the company's revenue grew by 2% YoY.

- Siemens Healthineers maintains a formidable position in the medical imaging market via technological excellence in high-end systems such as MRI and molecular imaging. Its key initiative involves deep integration of AI via its Teamplay platform, a strong focus on operational and clinical workflow solutions for healthcare providers, and acquisitions to boost its therapeutic and diagnostic capabilities.

- Philips competes in the medical imaging market with a distinctive strategy centered on connected care. It integrates its imaging system, such as ultrasound and CT, into broader enterprise-wide informatics and telehealth platforms. This approach aims to provide a longitudinal patient view supporting the diagnosis, treatment planning, and minimally invasive procedures within a value-based care model. In 2024, the company has made sales of EUR 18.0 billion in Q4 2024.

- Canon Medical Systems reinforces its role in the market by emphasizing Made for Life innovations that prioritize patient and clinician comfort. Its strategic initiatives include developing advanced lower-dose CT and MRI technologies incorporating AI for workflow and image enhancement, and offering cost-effective solutions to broaden access to high-quality imaging globally.

- Fujifilm Healthcare, historically strong in digital radiography and mammography, has strategically expanded its footprint in the broader medical imaging market. Following major acquisitions, it now offers a modality portfolio including CT and MRI. Fujifilm uses its deep expertise in image processing and AI to enhance diagnostic clarity and operational productivity across its system.

Here is a list of key players operating in the global market:

The global medical imaging market is defined by intense competition and consolidation, with dominant multinationals using extensive R&D, strategic acquisitions, and portfolio diversification to maintain leadership. The key initiatives include a strong pivot toward artificial intelligence and cloud-based solutions for enhanced diagnostics and workflow efficiency, expanding into emerging markets, and developing integrated low-cost systems for point-of-care use. Further Strategic partnerships with the tech firms and healthcare providers are also common to drive the innovation and the market penetration, while a growing emphasis on the value based care pushes the companies toward offering comprehensive solutions beyond the hardware. For example, GE HealthCare acquired Intelerad in November 2025 to advance the cloud-enabled enterprise imaging across care settings.

Corporate Landscape of the Medical Imaging Market:

Recent Developments

- In December 2025, GE HealthCare introduced advanced imaging solutions powered by NVIDIA technology to support timely diagnoses and streamlined clinical workflows. This collaboration underscores GE HealthCare’s ongoing commitment to integrating advanced technologies that aim to transform healthcare delivery and improve patient care.

- In November 2025, Siemens Healthineers launched artificial intelligence-enabled services to help healthcare providers address a range of challenges from hands-on image interpretation to complex scenario planning for entire healthcare environments.

- In February 2025, DeepHealth introduced new AI-powered radiology informatics and cancer screening solutions enabled by DeepHealth OS, its pioneering cloud-native operating system, to address clinical and operational challenges.

- Report ID: 4564

- Published Date: Feb 11, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.