Hemostats Market Outlook:

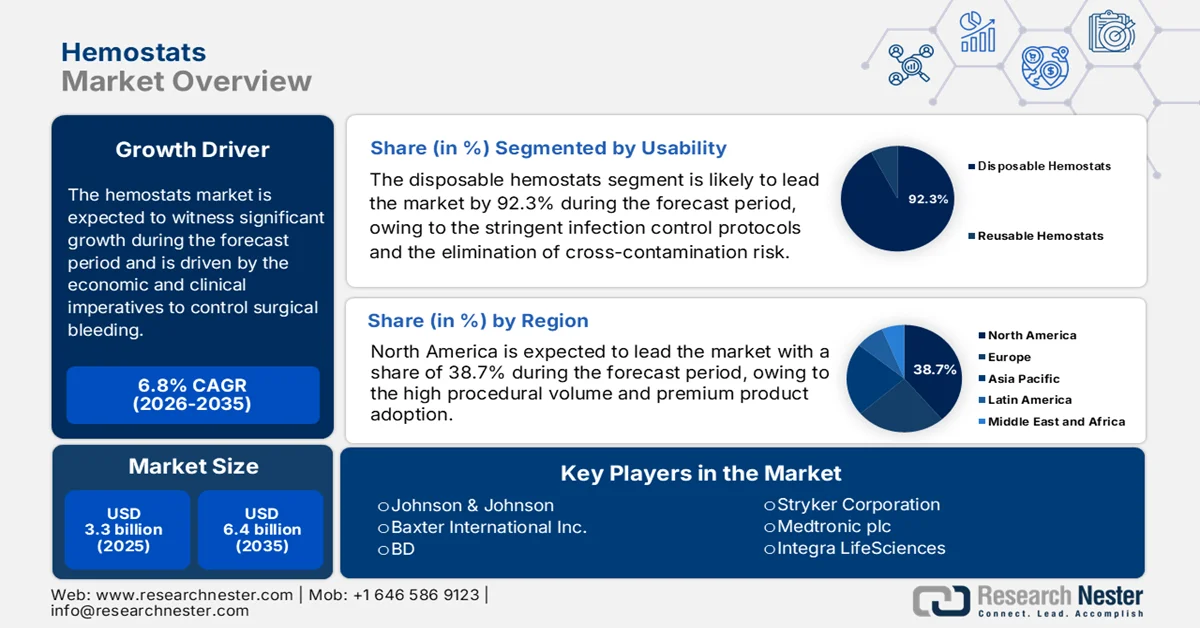

Hemostats Market size was valued at USD 3.3 billion in 2025 and is projected to reach USD 6.4 billion by the end of 2035, rising at a CAGR of 6.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of hemostats is estimated at USD 3.5 billion.

The global market is driven by economic and clinical imperatives to control surgical bleeding, which is a leading cause of preventable mortality. Moreover, the public health system utilization and surgical volume trends continue to underpin the demand for hemostatic agents across the acute and elective care settings. According to the NLM April 2024 study, the surgery rates in the U.S. range from 12.0 to 21.4 operations per 100,000 persons, with cardiovascular, orthopedic, gastrointestinal, and oncologic surgeries representing a substantial share of cases where the intraoperative bleeding control is mandatory. Further, the August 2024 CDC report shows that nearly 1,047.8 per 100,000 people visit hospitals due to injury-related hospitalization visits, reinforcing the routine procurement of hemostatic solutions by the hospital system. Moreover, the NLM September 2022 study indicates more than 310 million major surgical procedures are conducted globally, supporting a baseline demand for surgical bleeding management tools.

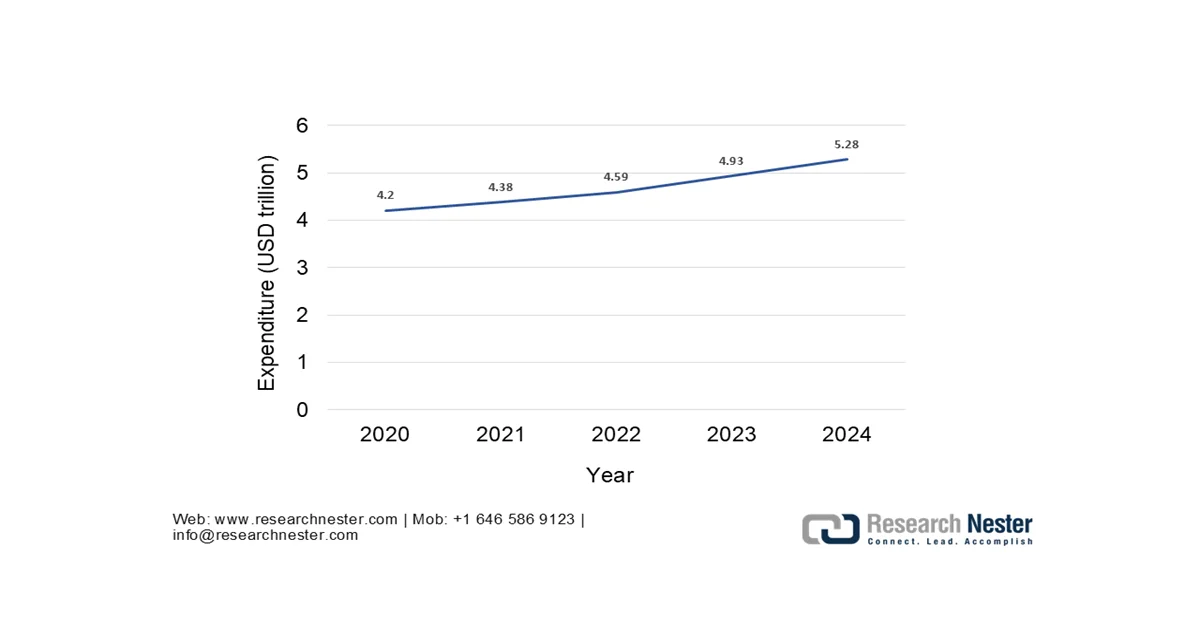

Besides, on the budget and policy point, government healthcare expenditure trends are directly supporting the procedural growth. As per the Health System Tracker January 2026 data, the healthcare spending reached USD 1.4 trillion in 2024, with surgical consumables embedded within the diagnosis-related group reimbursement. On the other hand, the European healthcare spending is also surging, with surgical capacity expansion prioritized under national resilience and recovery plans. Moreover, the trauma and emergency surgery funding remains stable, demanding rapid hemostatic intervention in the emergency and military healthcare system. Overall, the market experiences active growth and is supported by the government-funded surgical volumes, long-term investments in hospital infrastructure, and trauma burden.

Total Healthcare Expenditure

Source: Health System Tracker January 2026

Key Hemostats Market Insights Summary:

Regional Highlights:

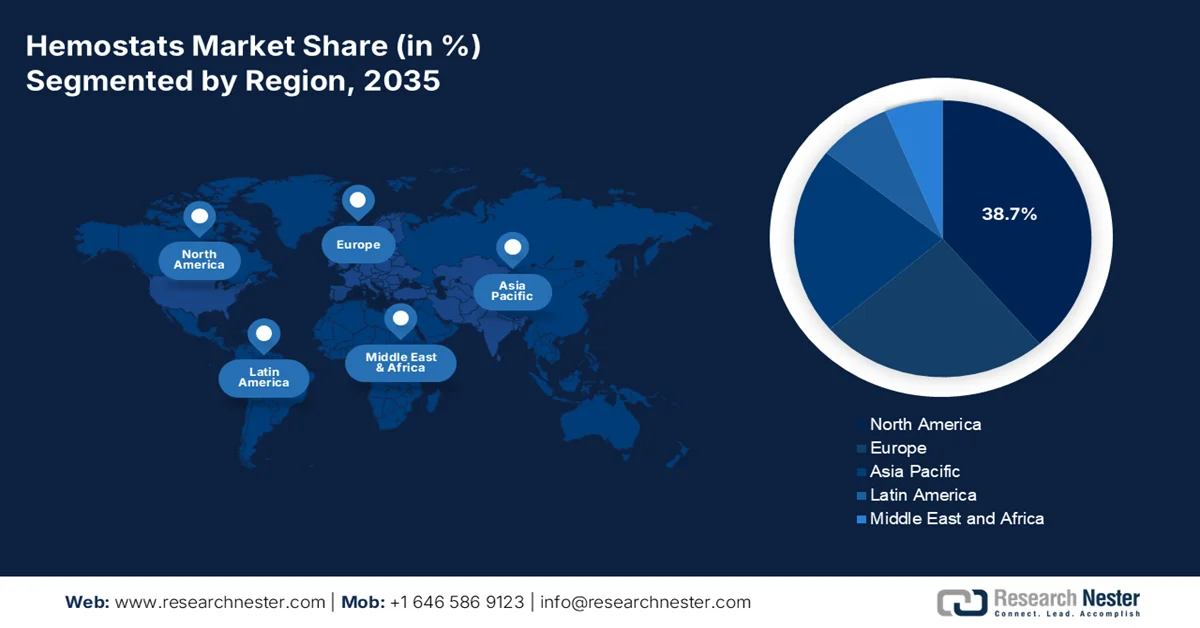

- North America in the hemostats market is projected to secure a 38.7% revenue share by 2035, owing to high procedural volumes, premium product adoption, and strong regulatory oversight supported by value-based care initiatives.

- Asia Pacific is forecast to expand at a CAGR of 8.1% during 2026–2035, fueled by expanding healthcare infrastructure, rising surgical volumes, and increasing healthcare expenditure.

Segment Insights:

- The disposable hemostats segment in the hemostats market is projected to command a 92.3% share by 2035, propelled by stringent infection control protocols and the elimination of cross-contamination risks through pre-sterilized single-use solutions.

- The hospitals and clinics segment is anticipated to hold the largest share by 2035, driven by high surgical volumes and bulk procurement supported by centralized purchasing and reimbursement-linked adoption of advanced hemostatic technologies.

Key Growth Trends:

- Growth in surgical volumes

- Expansion of public trauma and emergency care infrastructure

Major Challenges:

- Established brand loyalty and clinical preference

- Stringent and evolving material sourcing

Key Players: Johnson & Johnson, Baxter International Inc., BD, Stryker Corporation, Medtronic plc, Integra LifeSciences, Teleflex Incorporated, CryoLife Inc., Pfizer Inc., Braun Melsungen AG, CSL Behring, Grifols S.A., Hemostasis LLC, Takeda Pharmaceutical Company Limited, Equimedical, Samyang Biopharm, Anshul Life Sciences Pvt Ltd, Biomaterials Sdn. Bhd., Medical Illusions

Global Hemostats Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.3 billion

- 2026 Market Size: USD 3.5 billion

- Projected Market Size: USD 6.4 billion by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: - United States, Germany, Japan, China, United Kingdom

- Emerging Countries: - India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 12 February, 2026

Hemostats Market - Growth Drivers and Challenges

Growth Drivers

- Growth in surgical volumes: The rising surgical procedure volumes within the publicly funded healthcare systems are a primary demand driver for the market. According to the NLM May 2025 study, nearly 90% of surgical resources are performed by the privileged 10% of the world’s population, and 90% of trauma mortality is seen in low- and middle-income countries. This data indicates a significant need for surgical prompting governments and global health organizations to broaden the surgical capacity and emergency care infrastructure in the resource-constrained regions. As access to essential surgeries improves, the demand for cost-effective and easy-to-use hemostatic products is expected to rise sharply. Consequently, publicly funded programs and trauma care investments will play a critical role in stimulating the hemostat adoption worldwide.

- Expansion of public trauma and emergency care infrastructure: Government investment in trauma systems directly increases the demand for rapid bleeding control solutions. According to the CDC June 2025 report, the injuries result in over 43.5 million emergency department visits annually in the U.S., many requiring surgical and interventional bleeding management. Moreover, the WHO June 2024 report indicates that trauma accounts for nearly 8% of global mortality, driving the sustained funding for emergency surgical capacity, mainly in low and middle-income countries. Further, the scaling up of trauma centers, emergency surgical units, and pre-hospital care systems is reinforcing the consistent demand for the market, and they act as essential tools in acute bleeding control. National trauma network expansions in Asia, the Middle East, and Europe emphasize faster hemorrhage control to reduce mortality.

- Government investment in cancer and cardiovascular programs: The public cancer and cardiovascular care programs are expanding the surgical interventions. As per the WHO February 2024 data, in 2022, there were nearly 20 million new cancer cases registered in the U.S., with surgery remaining a core treatment modality. Further, the NLM December 2023 data indicates that a total of 123.2 per 100,000 population per year was performed with cardiac surgical volume in high-income countries. Moreover, the WHO identifies cardiovascular disease as the leading global cause of death, driving continued investment in cardiac surgery infrastructure. These procedures have high bleeding risk profiles, increasing the demand for market and the routine use of adjunct hemostatic agents.

Challenges

- Established brand loyalty and clinical preference: Surgeons exhibit a strong loyalty to familiar, trusted brands in the surgical protocols. Displacing these requires direct, costly surgeon education and proof of superior outcomes. The company in the market tackles this by deploying dedicated medical science liaisons to demonstrate the benefits of hemoblast in live surgeries, a high-touch strategy essential for market penetration but with a long ROI period.

- Stringent and evolving material sourcing: The top-tier hemostats rely on the high purity biological materials. Sourcing is constrained by limited suppliers, rigorous validation, and regulatory scrutiny for transmissible spongiform encephalopathy. Top players in the market use vertical integration as a leading fractionator to secure the supply for fibrin sealants, a key advantage smaller players lack, exposing them to supply chain volatility and cost fluctuations.

Hemostats Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 3.3 billion |

|

Forecast Year Market Size (2035) |

USD 6.4 billion |

|

Regional Scope |

|

Hemostats Market Segmentation:

Usability Segment Analysis

The disposable hemostats are leading and dominating the segment, poised to hold the share value of 92.3% by 2035 in the market. The segment is driven by the stringent infection control protocols, the elimination of cross-contamination risk, and the convenience of pre-sterilized, ready-to-use products that improve the operating room efficiency. The critical priority of preventing healthcare-associated infections makes disposable variants the standard of care. Moreover, the CDC January 2026 data shows that 1 in 31 patients in the hospitals have at least one healthcare related infections, which is a risk that reusable devices can provide without intensive reprocessing. The market’s trajectory firmly favors disposable solutions to reduce this persistent clinical and financial burden. Further, the favorable regulatory guidance and hospital procurement policies increasingly support single-use surgical instruments and ensure consistent device performance across high-volume surgical settings.

End user Segment Analysis

The hospitals and clinics are projected to hold the largest share value in the hemostats market. This segment’s leadership stems from its role as the primary site for the major surgical procedures, trauma centers, and complex interventions requiring advanced hemostatic agents. The concentration of the surgical volume, specialized staff, and high acuity care within hospitals creates a sustained high-volume demand. According to the AHA 2023 report, in the U.S., there are nearly 6,129 hospitals, and total admissions in all the hospitals are 34,011,386. This volume directly translates to the consistent bulk procurement of hemostats, securing hospitals' position as the indispensable end user. Moreover, hospitals benefit from centralized procurement and reimbursement-linked purchasing, enabling faster adoption of advanced hemostatic technologies to improve surgical outcomes and reduce the intraoperative blood loss and complications.

Distribution Channel Segment Analysis

The direct tenders are leading the distribution channel segment in the market, and are primarily facilitated via group purchasing organizations and direct hospital contracts commands the largest share. This channel’s dominance is due to its economic efficiency, allowing large healthcare systems to use their purchasing power for significant volume-based discounts and standardized product formularies. It ensures reliable supply chain logistics for mission-critical surgical supplies. A statistical insight is the healthcare spending directing the group purchasing in the hospital and clinics to reduce the cost of the medical supplies and equipment via negotiated contracts and federal supply schedules. This indicates a massive scale of centralized procurement that defines and drives the leading distribution channel.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Formulation |

|

|

Application |

|

|

End user |

|

|

Distribution Channel |

|

|

Usability |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Hemostats Market - Regional Analysis

North America Market Insights

North America is the largest and dominating market, and is expected to hold the regional revenue share of 38.7% by 2035. The market is defined by the high procedural volume, premium product adoption, and strong regulatory oversight. The key drivers include an aging population requiring complex surgeries, a robust shift to outpatient settings like ASCs, and a focus on value-based care that prioritizes technologies reducing complications and overall costs. Further, the primary trend is the integration of the hemostats into consolidated surgical suites and procedural bundles offered by major medical device companies, making standalone market entry challenging. Growth is further driven by the intense price negotiation from Group Purchasing Organizations and evolving Medicare reimbursement policies that reduce the cost-effectiveness of new technologies.

The rising trauma mortality risks and government-tracked surgical volumes in the U.S. are driving the market in U.S. According to the NLM May 2025 study, the hemorrhage is the leading cause of preventable death, accounting for nearly 43% of trauma-related deaths in civilian settings and up to 90% in combat environments, indicating a sustained federal investment in rapid bleeding control across emergency and hospital care systems. Moreover, the NLM April 2023 study has reported that over 2.8 million hip and knee arthroplasty procedures occurred in 2022, showing a 14% YoY increase, signaling high-volume orthopedic procedures where intraoperative bleeding control is routine. On the other hand, the recent advancements and clinical adoption are further supported by FDA-regulated innovation; for example, ETHIZIA Hemostatic Sealing Patch received U.S. regulatory clearance in November 2023, reflecting hospital demand for adjunct solutions that reduce operative bleeding and complications, and boosting the market growth.

Recent FDA Approvals and Clearances for Advanced Hemostatic Products

|

Product Name |

Company Name |

FDA Pathway |

Approval Date |

Intended Use |

Key Regulatory Notes |

|

PerClot Polysaccharide Hemostatic System |

Artivion, Inc. (formerly CryoLife, Inc.) |

PMA |

May 19, 2023 |

Surgical hemostasis for control of bleeding |

FDA-approved via PMA; supported by Summary of Safety and Effectiveness Data (SSED) and product labeling |

|

TRAUMAGEL |

Cresilon, Inc. |

510(k) Clearance |

August 15, 2024 |

Temporary external use for controlling moderate to severe bleeding |

Designed for emergency and trauma settings; rapid bleeding control |

|

LifeGel Absorbable Hemostatic Gel |

Medcura |

FDA Breakthrough Device Designation |

March 2024 |

Absorbable hemostatic agent for bleeding control |

First and only absorbable hemostatic gel to receive FDA breakthrough designation |

Source: Artivion, Inc, Cresilon, Inc, Medcura

The publicly funded surgical volumes, trauma care utilization, and sustained federal and provincial healthcare spending are the key drivers for the growth in the Hemostats market in Canada. According to the NLM May 2023 study Canada hospitals performed over 2 million inpatient surgical procedures, with the cost of USD 60 million, with orthopedic, cardiovascular, and general surgeries accounting for a significant share of cases requiring intraoperative bleeding control. Further, the rising health expenditure, with hospital care remaining the largest spending category under provincial budgets. Trauma-related demand also remains structurally relevant in the market. As stated in the article of the Government of Canada in June 2022, the injury-related hospitalization accounts for 225,208 cases, sustaining emergency surgical and hemorrhage management needs within publicly operated trauma centers, thereby denoting a positive market growth.

APAC Market Insights

The Asia Pacific hemostats market is growing rapidly and is expected to grow at a CAGR of 8.1% during the forecast period 2026 to 2035. The market is defined as having high growth potential driven by the expanding healthcare infrastructure, rising surgical volumes, and increasing healthcare expenditure. The key drivers include large populations with growing access to insurance, government-led healthcare modernization initiatives, and rising disease burden requiring surgical intervention. Further, the region presents a highly fragmented landscape with varying regulatory pathways price sensitive and technological adoption. Growth is propelled by the expansion of medical tourism hubs and the strategic focus of multinational corporations on customizing the products and pricing for specific APAC markets.

The expanding government-funded surgical access trauma burden and sustained public healthcare investment are driving the market in India. According to the NLM January 2024 study, India performs over 1385.28 and 355.94 per 100 000 surgical procedures annually, with a significant proportion occurring in public hospitals under national health programs. Moreover, the government schemes are increasing surgical throughput in secondary and tertiary care facilities. Further, the trauma-related demand reinforces baseline consumption, as the Petroleum and Natural Gas Regulatory Board in September 2024 reports over 460,000 road accidents and approximately 168,000 fatalities in 2022, many requiring emergency surgical intervention and hemorrhage control. Together, these data show there is a suitable upliftment of the country’s market growth.

The hemostats market in China is supported by large-scale, government-funded surgical volumes, expanding hospital infrastructure, and rapid population aging. As stated in the NLM February 2025 study, the annual day surgeries increased over 1.25 million, reflecting sustained procedural demand within public hospitals where bleeding control products are routinely utilized. Moreover, the World Bank's December 2025 data depicts that China reported that national healthcare expenditure exceeded 5.37% of the GDP in 2022, with public financing accounting for the majority of hospital service funding. On the other hand, the People’s Republic of China, October 2024 article reports that China’s population aged 60 and above reached 297 million in 2023, increasing the incidence of orthopedic, cardiovascular, and oncologic surgeries that require effective hemorrhage management, hence boosting the market growth.

Europe Market Insights

The hemostats market in Europe is expanding rapidly due to regulatory harmonization under the Medical Device Regulation, an aging population, and driving surgical volumes. Further, the growth is driven by the increasing prevalence of chronic disease requiring surgical intervention and the expansion of minimally invasive procedures, which require reliable topical hemostats. Moreover, the major trend is the increasing centralization of procurement via regional and national tenders, supporting the large suppliers with comprehensive portfolios. However, pricing pressure remains intense, with reimbursement decisions increasingly tied to health technology assessment (HTA) outcomes that demand robust clinical and economic evidence for new products.

High orthopedic surgical intensity and a rapidly aging population are the main drivers for the market growth in Germany. According to the NLM September 2023 study, Germany recorded 310.6 hip replacement procedures per 100,000 population, the highest rate among OECD countries and significantly above the OECD average of 191.5 per 100,000, indicating structurally elevated demand for intraoperative bleeding control in publicly reimbursed arthroplasty procedures. As per the Destatis data in December 2022, the Federal Statistical Office of Germany projects that the population aged 67 years and over will increase by approximately 4 million, reaching at least 20 million by the mid-2030s, driving a higher incidence of degenerative joint disease and elective joint replacement surgeries. As hip and knee arthroplasty procedures require adjunct hemostatic agents to manage blood loss and reduce transfusion risk, these trends indicate that hemostats market in Germany is set to experience an active growth opportunity.

The universal healthcare system and the rebound of publicly funded elective orthopedic procedures within the National Health Service are driving the market in UK. According to the British Orthopedic Association article in May 2022, over 42,000 orthopedic operations were performed in March 2022, the highest monthly volume since 2021, signaling renewed momentum in elective surgical activity despite winter capacity constraints. Moreover, the pre-pandemic baseline is approximately 48,500 orthopedic procedures per month. This recovery phase indicates sustained procurement of surgical consumables, including hemostatic agents, as hospitals address surgical backlogs. Orthopedic surgeries, particularly hip and knee replacements, are among the most bleeding-intensive elective procedures funded by the NHS.

Key Hemostats Market Players:

- Johnson & Johnson (U.S.)

- Baxter International Inc. (U.S.)

- BD (U.S.)

- Stryker Corporation (U.S.)

- Medtronic plc (U.S.)

- Integra LifeSciences (U.S.)

- Teleflex Incorporated (U.S.)

- CryoLife, Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Braun Melsungen AG (Germany)

- CSL Behring (Germany)

- Grifols, S.A. (Spain)

- Hemostasis, LLC (Sweden)

- Takeda Pharmaceutical Company Limited (Japan)

- Equimedical (Netherlands)

- Samyang Biopharm (South Korea)

- Anshul Life Sciences Pvt Ltd (India)

- Biomaterials Sdn. Bhd. (Malaysia)

- Medical Illusions (Australia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Johnson & Johnson is a dominant player in the hemostats market and uses its unparalleled surgical reach. Its strategic initiatives focus on integrating advanced hemostatic agents such as the Surgicel family of absorbable hemostats with its ecosystem's surgical tools and energy devices, creating comprehensive blood management solutions for operating rooms globally.

- Baxter International Inc holds a foundational position in the hemostats market via its biosurgery portfolio, including the FLOSEAL and TISSEEL lines. The company strategically emphasizes clinical education and real-world evidence to demonstrate cost effectiveness and improved patient outcomes while also exploring synergies between its homostats and its market-leading infusion and renal care platforms. The company has made a total revenue of USD 10.6 billion in 2024.

- BD engages with the hemostats market mainly via its interventional surgery segment. A key strategy is the combination of its hemostasis products, such as the HEMOPATCH sealant, with precision surgical instruments, aiming to standardize the care and control bleeding in complex laparoscopic and open surgeries, thereby reducing the complications.

- Stryker Corporation’s strategy in the hemostats market is deeply integrated with its dominant position in surgical navigation and orthopedics. Through its surgical technologies division, it advances products such as the HEMOBLAST line, focusing on biomimetic and chitosan-based technologies that offer precise application in high blood loss specialties such as cardiac trauma and orthopedic surgery. In 2024, the company has made a global sales of USD 22.6 billion.

- Medtronic plc competes powerfully in the hemostats market by directly embedding advanced hemostatic technologies, such as those from its EVARREST and TACHOSIL portfolio, into specific surgical procedure protocols. Its strategic initiative is to provide therapy beyond the device, combining hemostats with its market-leading surgical staplers and energy platforms to deliver data-driven, holistic solutions for surgical bleeding management.

Here is a list of key players operating in the global market:

The global hemostats market is defined by intense competition, with dominance held by large diversified medical device corporations from the U.S. and Europe. These key players use extensive R&D capabilities, robust clinical data, and broad international distribution networks to maintain their market position. Strategic initiatives are heavily focused on product innovation, including the development of combination and advanced sealant hemostats, as well as strategic acquisitions to expand the product portfolios and geographic reach. For example, in May 2022, Hemostasis closed the acquisition of Fiagon Medical Technologies. Companies are also pursuing targeted marketing and partnerships to penetrate the emerging markets and strengthen their presence in high-growth surgical segments such as minimally invasive procedures.

Corporate Landscape of the Hemostats Market:

Recent Developments

- In April 2025, Baxter International Inc. announced the introduction of Hemopatch Sealing Hemostat, which can be stored at room temperature, at a symposium in Austria. The product's evolution optimizes accessibility in the operating room, delivering an immediate solution for surgeons to control bleeding or prevent leakage.

- In August 2024, Toagosei Co., Ltd. has announced that it has launched a dental hemostatic agent for tooth extraction sockets called Aron cure Dental. Aron Cure Dental is a new concept dental hemostatic agent. It stops bleeding after tooth extraction with a hydrogel polymer sponge.

- In April 2024, LifeScience PLUS officially introduced its breakthrough product for the treatment of donor sites at the 56th Annual American Burn Association (ABA) Meeting in Chicago. DonorSeal is a 100% natural plant-based cellulose matrix that provides benefits in rapid hemorrhage control, blood loss reduction, and wound healing promotion.

- Report ID: 4484

- Published Date: Feb 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.