Healthcare ERP Market Outlook:

Healthcare ERP Market size was valued at USD 9.1 billion in 2025 and is projected to reach USD 19.2 billion by the end of 2035, rising at a CAGR of 7.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of healthcare ERP is evaluated at USD 9.8 billion.

The global healthcare ERP adoption is closely aligned with the federal digitization mandates, reimbursement modernization, and the financial accountability requirements across the public and private health systems. According to the ASTP March 2022 data, 4 in 5 office-based physicians and nearly 96% of all non-federal acute care hospitals have adopted a certified EHR. This data indicates a near-universal digital infrastructure across care delivery organizations. This high penetration of core clinical systems increases the demand for the integrated financial management, supply chain, human resources, and asset tracking platforms that connect operational and clinical datasets. Moreover, the CMS December 2023 data shows that healthcare spending reached USD 4.5 trillion in 2022. This expenditure scale provider organization faces sustained pressure to manage labor costs, procurement efficiency, reimbursement compliance, and reporting accuracy.

Besides, the public sector digitization program further reinforces the structured enterprise platform investments. The Government of UK March 2024 report shows that the government has committed 2 billion euros to digitize the national health service, including the modernization of core infrastructure and data systems. Moreover, the need for integrated systems is also fueling the demand. The transition to the value-based care models requires providers to track the quality metrics and patient outcomes along with financial data. This requires a level of data integration that older systems cannot support. Further workforce shortages are a critical issue, making administrators use technology to optimize staff schedules and reduce the administrative burden on clinicians. These factors collectively drive health systems to adopt comprehensive software systems to meet regulatory requirements and maintain operational stability.

Key Healthcare ERP Market Insights Summary:

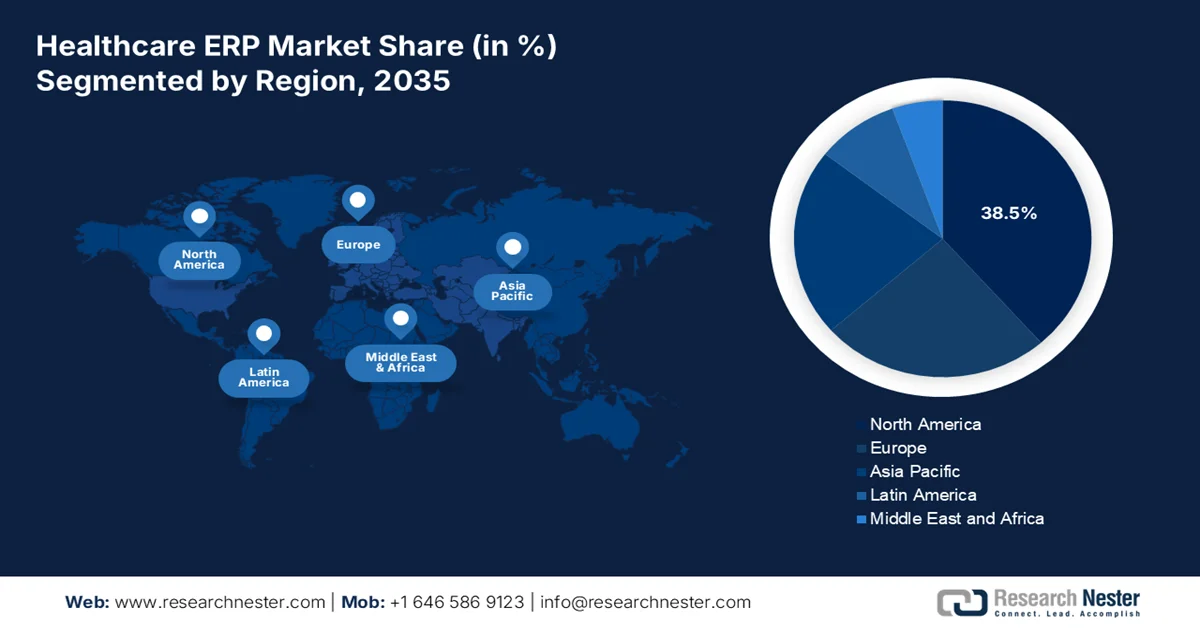

Regional Highlights:

- North America in the healthcare ERP market is projected to secure a 38.5% revenue share by 2035, attributed to mandatory value-based care reporting requirements and federal funding for health information technology modernization

- Asia Pacific is forecast to expand at a CAGR of 8.7% during 2026–2035, stimulated by massive government investments in healthcare infrastructure modernization and digitalization of paper-based systems

Segment Insights:

- The cloud sub-segment in the healthcare ERP market is projected to account for a 68.3% share by 2035, propelled by the sector’s urgent need for scalability and remote accessibility

- The large enterprises sub-segment is anticipated to command a significant share by 2035, fueled by the complexity and scale of operations within major hospital systems and multinational pharmaceutical corporations

Key Growth Trends:

- Workforce expansion and labor cost pressures

- Supply chain modernization and procurement transparency

Major Challenges:

- Rising cybersecurity threats

- Resistance to change from the professionals in the healthcare sector

Key Players: Oracle Corporation, SAP SE, Microsoft Corporation, Infor, Epic Systems Corporation, QAD Inc., Sage Group plc, Odoo, Unit4, Syspro, Constellation Software Inc.

Global Healthcare ERP Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 9.1 Billion

- 2026 Market Size: USD 9.8 Billion

- Projected Market Size: USD 19.2 Billion by 2035

- Growth Forecasts: 7.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, United Kingdom, Japan, China

- Emerging Countries: India, Indonesia, Vietnam, Brazil, Mexico

Last updated on : 23 February, 2026

Healthcare ERP Market - Growth Drivers and Challenges

Growth Drivers

- Workforce expansion and labor cost pressures: Healthcare remains one of the largest employment sectors globally, increasing the administrative complexity. According to the KFF February 2025 data, the U.S. hospitals employ over 6.7 million people. Labor represents the largest share of hospital operating costs, intensifying the demand for the centralized human capital management and workforce planning modules. Managing payroll, credentialing, scheduling, and compliance across such a large workforce requires scalable ERP systems. Additionally, the U.S. Bureau of Labor Statistics projects healthcare occupations to grow much faster than the average for all occupations, adding millions of new jobs and further increasing administrative and payroll management complexity across provider organizations, driving the healthcare ERP market.

- Supply chain modernization and procurement transparency: Pandemic-driven procurement disruptions exposed structural weakness in hospital supply chains. Moreover, the federal investments strengthen the supply chain resilience and stockpiling. Besides the public spending increases the expectations for transparent procurement and inventory accountability. ERP systems with the centralized supply chain modules support vendor performance tracking, demand forecasting, and contract compliance. The U.S. reported multi-billion-dollar federal investments to strengthen medical supply chains and expand the Strategic National Stockpile, reinforcing the need for real-time inventory visibility and standardized procurement controls across health systems.

- Growth in hospital infrastructure and capacity expansion: Government-backed hospital expansion programs increase the enterprise system requirements. According to the American Hospital Association, December 2025 data in the U.S., there were 6,093 hospitals in 2023, many operating within site systems requiring centralized procurement and financial consolidation. Moreover, the new facilities are commissioned institutions that require integrated ERP systems to standardize procurement, inventory, biomedical asset tracking, and vendor management. Further continuous federal capital funding will expand healthcare facility capacity and infrastructure, further increasing the need for standardized enterprise-wide financial and asset management systems across newly funded sites.

Challenges

- Rising cybersecurity threats: The healthcare ERP systems are the main targets for the cybercriminals, creating an immense challenge for the suppliers who must architect security from the ground up rather than as an afterthought. Moreover, the healthcare organization has experienced many data breaches affecting millions of patients' records, with ERP and financial systems representing the most common breach vector. The market manufacturers must invest heavily in AI-powered threat detection to remain competitive

- Resistance to change from the professionals in the healthcare sector: Cultural resistance represents a significant non-technical barrier in the healthcare ERP market, for manufacturers and administrative staff often resist workflow changes imposed by the new systems. This resistance stems from decades of familiarity with legacy interfaces and the critical nature of healthcare workflows, where changes could impact patient safety. Additionally, inadequate training and fear of increased administrative burden further intensify hesitation among healthcare professionals, slowing down ERP implementation and user adoption rates.

Healthcare ERP Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

7.7% |

|

Base Year Market Size (2025) |

USD 9.1 billion |

|

Forecast Year Market Size (2035) |

USD 19.2 billion |

|

Regional Scope |

|

Healthcare ERP Market Segmentation:

Delivery Model Segment Analysis

The cloud sub-segment is the dominant one and is poised to hold the share value of 68.3% by 2035. The dominance is due to the sector’s urgent need for scalability and remote accessibility. The healthcare providers are rapidly migrating from legacy on-premises systems to cloud-based solutions to facilitate real-time data sharing across multiple facilities and support the rise of telehealth services. This shift allows organizations to reduce the total cost of ownership while benefiting from the continuous software updates that ensure compliance with evolving healthcare regulations. According to the Commonwealth Fund data in August 2025, nearly 99% of community health centers are equipped with at least one electronic health record system, driving the cloud adoption in the healthcare sector. The flexibility of the cloud model ensures that healthcare systems can integrate operational data with clinical platforms, making it the leading choice for modernizing healthcare infrastructure.

Deployment Scale Segment Analysis

The large enterprises sub segment are driving the deployment scale segment in the market. The segment is driven by the complexity and scale of the operations within the major hospital systems and multinational pharmaceutical corporations. These entities require highly integrated ERP solutions capable of managing thousands of employees and a vast quantity of patient data across multiple facilities. The large enterprises possess the capital resources to invest in comprehensive, customizable systems that smaller organizations cannot afford. Additionally, large enterprises often operate across multiple geographies, requiring ERP platforms that support regulatory compliance, multi-currency transactions, and standardized reporting frameworks across regions. Their ongoing digital transformation initiatives and focus on data-driven decision making further accelerate the adoption of advanced, scalable ERP systems with analytics, AI integration, and interoperability capabilities.

Component Segment Analysis

The services sub-segment holds the largest revenue share in the healthcare ERP market. services including consulting, implementation, training, and managed support, are driving the market growth. Software alone cannot generate value without expert configuration to meet the stringent healthcare regulations and complex clinical workflows. The high cost and critical nature of these services are driven by the need for interoperability with existing electronic health records and compliance with the evolving standards. According to the JMIR publications in December 2025 data, over 75% of the hospitals reported that integrating new IT systems with the existing EHR required significant external consulting and customization services. Further, the support services ensure compliance with federal security and privacy mandates, solidifying the services segment as the primary long-term revenue driver in the Healthcare ERP ecosystem.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Application |

|

|

Business Function |

|

|

Delivery Model |

|

|

End user |

|

|

Deployment Scale |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Healthcare ERP Market - Regional Analysis

North America Market Insights

North America is expected to dominate and hold the regional revenue share of 38.5% by 2035. The market is driven by the mandatory value-based care reporting requirements and federal funding for health information technology modernization. The demand in this region is primarily driven by the need for large hospital systems and integrated delivery networks to manage complex financial operations, extensive supply chains, and vast distributed workforces across multiple facilities. The market is marked by a trend toward cloud-based deployments, as organizations seek to reduce the burden of maintaining on-premise infrastructure and gain access to advanced analytics and artificial intelligence capabilities. This advanced landscape demands ERP solutions to meet the unique operational workflows of leading healthcare institutions.

The scale of national healthcare spending, workforce expansion, and continued federal digital oversight requirements are shaping the healthcare ERP market in U.S. The rising healthcare expenditure is reflecting sustained financial complexity across the provider systems. According to the U.S. BLS December 2023 data, employment continued to trend up in healthcare services (+19,000) and hospitals (+15,000). This makes the latest employment sector in the country. On the other hand, the recent developments in the market, such as in August 2024, Pfizer has launched PfizerForAll, which is a digital platform that helps simplify access to healthcare. These data indicate the driving demand for integrated enterprise systems capable of managing financial consolidation, workforce administration, procurement transparency, and regulatory reporting across complex healthcare networks.

Recent Advancements in the Market

|

Company |

Date |

Advancement |

|

Pfizer Inc. |

August 2024 |

Launched PfizerForAll, a digital healthcare platform integrating care access, prescription services, vaccination support, and savings programs into a single interface to streamline patient engagement and backend coordination. |

|

BHM Healthcare Solutions |

March 2025 |

Introduced a newly redesigned website (bhmpc.com) featuring updated branding, educational resources, and enhanced user experience to support health plans and healthcare organizations. |

|

Simplify Healthcare |

November 18, 2024 |

Announced the launch of SimplifyX, a new subsidiary expanding SaaS-based enterprise software offerings beyond the health insurance sector to broader industries. |

Source: Pfizer Inc., BHM Healthcare Solutions, Simplify Healthcare

The provincial health system consolidation and federal digital health mandates requiring operational integration are propelling the market in Canada. According to the CMA February 2024 study, the total health spending reached USD 344 billion in 2023, underscoring the scale of administrative and financial management required across public health systems. Moreover, the NLM November 2024 study indicates that 100% of surveyed healthcare institutions had implemented an EHR system, with 66.6% fully digitized and 33.3% are partially digitized, highlighting the strong foundational digital penetration. Additionally, workforce administration and financial consolidation are becoming essential to support multi-provincial operational governance and cost control, indicating a rising market growth

APAC Market Insights

The Asia Pacific is the fastest growing market and is poised to grow at a CAGR of 8.7% during the forecast period 2026 to 2035. The market is driven by the massive government investments in the healthcare infrastructure modernization and the digitalization of paper-based systems across both public and private healthcare sectors. Countries such as China and India are undertaking ambitious national health information architecture projects with the government funding directed toward te creating integrated networks that connect thousands of public hospitals and clinics requiring standardized ERP capabilities for resource allocation and supply chain management. The diverse economic development levels across the region, from advanced economies like Japan and Australia to rapidly growing markets like Indonesia and Vietnam, create a tiered demand landscape requiring vendors to offer scalable solutions.

The rising public expenditure and digital health integration are creating increased demand for patient relationship management software and healthcare financial management systems, fueling the healthcare ERP market in India. According to the PIB January 2023 data, the public health expenditure increased to 2.1% of GDP, reflecting higher government allocation toward healthcare infrastructure and digital systems. Moreover, the healthcare expenditure reached 8,008,684 in 2023. Under the Ayushman Bharat – Pradhan Mantri Jan Arogya Yojana (PM-JAY), over 36.7 crore (340 million) Ayushman cards have been issued to beneficiaries, generating high volumes of eligibility verification claims processing and beneficiary engagement workflows. This widespread digital adoption is driving rapid market growth.

The healthcare ERP market in China is rapidly digitizing, fueling demand for healthcare ERP platforms that integrate patient management, financial operations, and administrative workflows. As per the NLM October 2024 study, the digital healthcare market reached CNY 195.4 billion in 2022, with an average annual growth rate of 30% over the previous five years. Moreover, the electronic medical record (EMR) coverage extended to 90% of tertiary hospitals, 60% of secondary hospitals, and 40% of primary hospitals, reflecting a strong foundational digital infrastructure. On the other hand, the Frontiers March 2025 data indicates that over 3,000 internet hospitals now provide telemedicine services covering city and county levels, supporting more than 25.9 million people, while 125 national and regional medical centers have been established in second- and third-tier cities. These trends indicate rising demand for cloud-based ERP systems and integrated patient relationship management, thereby driving the market growth.

China Online Consultation and Digital Health Statistics

|

Parameter |

Statistics |

|

Online Consultations Provided |

40,462,801 (Jan 2008 – Dec 2022) |

|

Doctor Titles (Online Consultations) |

Intermediate: 30.15%, Senior: 58.12% |

|

Hospital Level |

Tertiary hospitals: 88.18% |

|

Digital Healthcare Market Value |

195.4 billion CNY in 2022 |

|

EMR Coverage |

Tertiary hospitals: 90%, Secondary hospitals: 60%, Primary hospitals: 40% |

|

Internet Hospitals |

Over 3,000 established |

|

Telemedicine Coverage |

City and county levels, serving 25.9 million people |

Source: NLM October 2024

Europe Market Insights

The healhcare ERP market in Europe is defined by the diverse national health systems, each with its unique regulatory requirements and reimbursement models. Spending patterns across the region are heavily influenced by the national recovery and the resilience plans, with countries such as Germany and France dedicating billions from EU recovery funds specifically to hospital digitalization and supply chain modernization. A significant trend is the move toward cloud-based deployments driven not only by efficiency gains but also by strict data security requirements under GDPR, which are more readily managed via certified cloud providers than disparate on-premises systems. This combination of regulatory pressure, targeted public funding, and the need for the cross border data exchange makes Europe a mature market for Healthcare ERP solutions.

The structured digital transformation, creating measurable demand for cloud-based administrative and enterprise platforms, is shaping the healthcare ERP market in Germany. According to the EMHA November 2022 data, the Hospital Future Act allocates EUR 4.3 billion to support hospital digital infrastructure upgrades, including IT security and digital documentation systems. additionally the, Germany’s Digital Strategy emphasizes secure cloud adoption and interoperable health data frameworks across federal and Länder institutions. With over 1,800 hospitals nationwide, multi-site providers are increasingly evaluating cloud-based ERP environments to centralize financial management, procurement, and workforce coordination while complying with strict data protection regulations. The combination of high public expenditure on federally funded digitization programs and policy-backed cloud enablement is accelerating enterprise modernization across Germany’s healthcare administration landscape.

The administrative systems across the National Health Service are driving the market in the UK. The UK Government's June 2022 data announced a 2 billion euros investment to digitize the NHS, aimed at upgrading core IT systems, improving data integration, and strengthening digital service delivery across trusts. In addition, the King's Fund November 2025 data depicts that the workforce exceeded 1.5 million staff in 2025, creating significant administrative scale requiring integrated financial, procurement, and workforce management platforms. As NHS trusts consolidate digital estates and replace legacy systems, demand for Healthcare ERP implementation services, including system integration, data migration, compliance configuration, and long-term managed support, is increasing to ensure standardized governance, financial oversight, and multi-site operational coordination across publicly funded healthcare networks.

Key Healthcare ERP Market Players:

- Oracle Corporation (U.S.)

- SAP SE (Germany)

- Microsoft Corporation (U.S.)

- Infor (U.S.)

- Epic Systems Corporation (U.S.)

- QAD Inc. (U.S.)

- Sage Group plc (UK)

- Odoo (Belgium)

- Unit4 (Netherlands)

- Syspro (South Africa)

- Constellation Software Inc. (Canada)

- Ramco Systems (India)

- SYSPRO (Australia)

- Kirloskar Technologies (India)

- IFS AB (Sweden)

- Greythorn (Australia)

- eXtendRMS (Malaysia)

- Samsung SDS (South Korea)

- Fujitsu (Japan)

- Hitachi, Ltd. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Oracle Corporation is a dominant player in the healthcare ERP market, leveraging its robust cloud infrastructure and data management capabilities to transform healthcare operations. By integrating vast amounts of clinical, financial, and operational data into its comprehensive ERP suits oracle enables healthcare providers to achieve a unified view of their enterprise. According to the Q2 annual report, the company has made a revenue of USD 1.0 billion in cloud ERP services.

- SAP SE holds a significant position in the global market by offering industry-specific solutions that streamline complex business processes for hospitals and health systems. SAP’s technology is pivotal in integrating administrative and clinical data to create a seamless information flow supporting everything from supply chain logistics to financial accounting and human capital management. In 2024, the company made a free cash flow of 4.11 billion euros.

- Microsoft Corporation has carved out a substantial niche in the healthcare ERP market by combining its ubiquitous cloud platform, Azure, with powerful productivity and business intelligence tools. Their approach focuses on providing a flexible and secure foundation that integrates seamlessly with existing healthcare systems, including EHRs and specialized monitoring devices.

- Infor is a key specialist in the healthcare ERP market, renowned for providing deeply integrated industry-tailored solutions that address the unique challenges of modern healthcare providers. Infor’s cloud-based ERP suites are designed to improve operational efficiency by connecting the clinical supply chain and financial data into a single source.

- Epic Systems Corporation is an influential player in the broader healthcare ERP market by offering integrated administrative and financial tools that sit atop its extensive clinical platform. The strength lies in its ability to create a seamless digital ecosystem where operational data, such as billing, scheduling, and supply chain information, is directly linked to the patient’s electronic health record.

Here is a list of key players operating in the global market:

The competitive landscape of the market is highly fragmented and dynamic, defined by a mix of the leading global technology giants and specialized regional vendors. The key players are actively pursuing strategic initiatives, such as mergers and acquisitions, to enhance their product portfolios and expand their geographic reach. For example, in September 2024, ChrysCapital Group signed definitive agreements to sell a controlling beneficial interest in GeBBS Healthcare Solutions Private Limited. A significant trend is the heavy investment in cloud-based and AI-integrated solutions to offer real-time data analytics, improve interoperability, and ensure compliance with stringent healthcare regulations such as HIPAA. Further, companies are forming strategic partnerships with healthcare providers to develop customized, scalable solutions that address specific operational challenges, thereby strengthening their market position and driving innovation in digital health management.

Corporate Landscape of the Healthcare ERP Market:

Recent Developments

- In December 2025, Trivitron Healthcare announced the launch of Trivitron Digital.AI, a next-generation digital health venture created to accelerate the transition toward AI-enabled, interoperable, and patient-centric Smart Hospital ecosystems.

- In October 2025, BD (Becton, Dickinson and Company) introduces the BD Incada Connected Care Platform, a new scalable, AI-enabled, cloud-based platform that unifies BD device data into one intelligent ecosystem for the first time.

- In June 2024, Oracle NetSuite announced a new solution to help healthcare organizations improve business efficiency and support Health Insurance Portability and Accountability Act (HIPAA) compliance.

- Report ID: 4392

- Published Date: Feb 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.