Flexible Space Market Outlook:

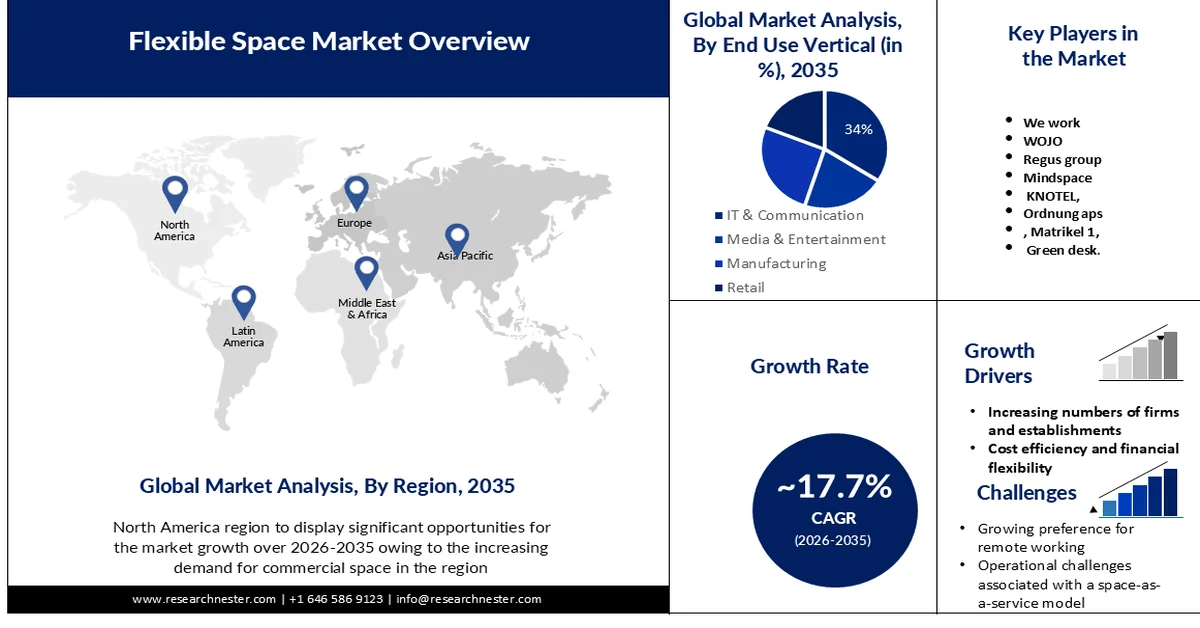

Flexible Space Market size was valued at USD 7.97 billion in 2025 and is expected to reach USD 40.67 billion by 2035, registering around 17.7% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of flexible space is assessed at USD 9.24 billion.

The market growth can be estimated by the rising trend among enterprises to outsource their operations to a third person rather than hiring a person to carry out the necessary jobs. Thus, resulting in improving the efficiency, and effectiveness of the business operations.

New players can enter the market more easily as a result of technological developments in the flexible space market. With the digital transformation companies are able to opt for flexible spaces easily, as all the data are saved on the cloud. Various growth and expansion strategies are used by companies for the adoption of flexible office spaces.

Key Flexible Space Market Insights Summary:

Regional Highlights:

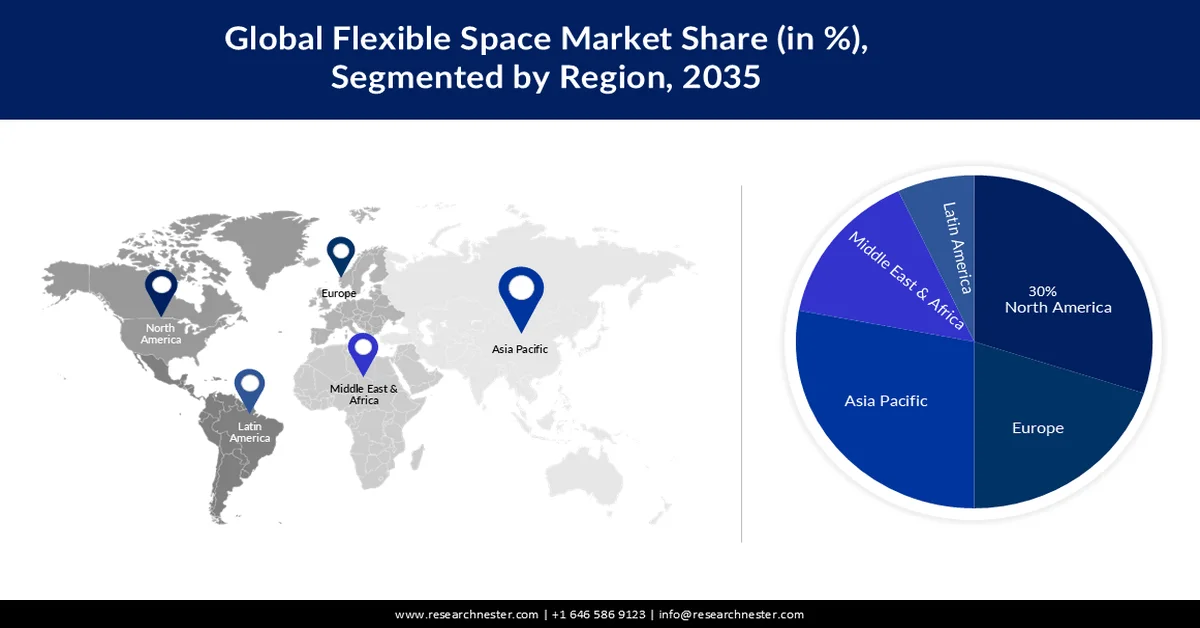

- The flexible space market in North America is projected to dominate with a 30% revenue share by 2035, driven by expanding commercial space demand in secondary and tertiary cities alongside rising adoption of flexible work models.

- Asia Pacific is expected to register growth rate 4% during 2026–2035, impelled by evolving corporate office strategies and sustained momentum in flexible office adoption.

Segment Insights:

- The co-working space segment of the flexible space market is projected to account for a 38% share by 2035, propelled by rising adoption among multinational companies seeking cost-efficient, collaborative, and skill-enhancing work environments.

- The IT & communication segment is anticipated to capture a 34% share by 2035, fueled by the growing need for flexible work patterns and disturbance-free environments for technical professionals.

Key Growth Trends:

- Increasing Numbers of Firms and Establishments

- Surge in the Number of Collaboration and Community

Major Challenges:

- Highly Competitive Industry

- Growing Preference for Remote Working

Key Players: IBM Corporation, Allscripts Healthcare Solutions Inc., Cerner Corporation, McKesson Corporation, Optum, Inc., CitiusTech Inc., Health Catalyst, Inc., Inovalon, Inc., MedeAnalytics, Inc., Oracle Corporation, SAS Institute Inc., SCIOInspire, Corp., Verscend Technologies, Inc., VitreosHealth, Inc.

Global Flexible Space Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 7.97 billion

- 2026 Market Size: USD 9.24 billion

- Projected Market Size: USD 40.67 billion by 2035

- Growth Forecasts: 17.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (30% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, United Kingdom, China, India, Germany

- Emerging Countries: India, China, Japan, Germany, United Kingdom

Last updated on : 25 February, 2026

Flexible Space Market - Growth Drivers and Challenges

Growth Drivers

- Increasing Numbers of Firms and Establishments; -Large corporations and firms are increasingly incorporating flexible space solutions into the firm’s establishments. By utilizing flexible spaces, these firms and corporations can provide project spaces or can create innovation hubs allowing alignment of workspaces with requirements. In addition, there are small firms that don’t want to invest a considerable amount in private office space, thus resulting in the increasing demand for flexible space. As per the data, there are more than 33 million small-scale businesses in the United States in 2022.

- Surge in the Number of Collaboration and Community; - Flexible spaces for fostering collaborations and community building through a shared work environment. These often facilitate networking opportunities, community events, and industry-specific programs that bring professionals from various backgrounds together.

- Increasing Requirement for Cost Efficiency and Financial Flexibility; - Traditional offices lease often come with high upfront costs and long-term commitments. In contrast, flexible spaces provide a cost-efficient alternative with flexible lease terms.

- Rising Trend of Freelancing – There are a large number of professionals that are not employed in one organization, and provide their services to more than one organization. Therefore, they require flexible space in order to provide service to a particular organization. According to a recent analysis, more than 1.5 Billion of the world’s workforce are working as freelancers.

Challenges

- Highly Competitive Industry-Flexible space market has become highly competitive with the entry of numerous providers. This saturation can make it challenging for individual providers to differentiate themselves and attract tenants. Standing out among the competition requires offerings unique value propositions, such as specialized industry-focused spaces, innovative amenities, or tailored services. Addressing these sorts of challenges requires strategic planning, continuous innovation, and a deep understanding of market dynamics. Providers that can effectively navigate these obstacles have the opportunity to thrive in a market and meet the evolving demands of businesses and professionals.

Growing Preference for Remote Working

Operational Challenges Associated with Space -As-A-Service Model.

Flexible Space Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

17.7% |

|

Base Year Market Size (2025) |

USD 7.97 billion |

|

Forecast Year Market Size (2035) |

USD 40.67 billion |

|

Regional Scope |

|

Flexible Space Market Segmentation:

Type Segment Analysis

The co-working space segment in the flexible space market is anticipated to hold the largest share of 38 % by the end of 2035. There has been growing concept of co-working space among the increasing multinational companies. Whereas, they require people for different operations for a particular period in order to reduce their expenditure. Moreover, from the other perspective, employees with different knowledge work in a common space that helps them to improve their skills, and gain more knowledge from each other.

End Use Vertical Segment Analysis

Flexible space market from the IT & communication segment is set to have a significant gain of 34 % in the upcoming years. There is a requirement for a large number of technical employees that needs flexible work pattern, in order to remain in their comfort zone.In addition, these areas have quiet areas, where employees can work without any disturbance.

Our In-depth Analysis of the global market includes the following segments:

|

Type |

|

|

End Use Vertical |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Flexible Space Market - Regional Analysis

North-America Market Insights

The flexible space market in the North America industry is predicted to account for largest revenue share of 30% by 2035. The growth of the market in the region can be attributed to the increased demand for commercial space from local enterprises in secondary and tertiary cities. For instance, the number of commercial buildings in the United States has increased by 5 % from 2012 to 2018. Businesses are deciding to expand into secondary and tertiary cities, a trend that is expected to boost the market significantly. Also, there has been a rise in the number of IT companies in the region that are open for flexible space. In addition, the rapid adoption of flexible work patterns by various organizations in the North America region is further poised to elevate the market’s growth in the region.

Asia Pacific Market Insights

The flexible space market for flexible offices in Asia Pacific is projected to grow at a compound annual growth rate of over 4% during the forecast period. The Asia Pacific Flexible Office Market has remained strongly active in the last 12 months, albeit against a backdrop of political instability and uncertainties caused by COVID-19. The sector is in good shape to benefit from the shift of office strategies by firms throughout the region, based on recent research.

Flexible Space Market Players:

- The office groups

- Business strategy

- Key product offerings

- Financial performance

- Risk analysis

- Recent development

- Regional presence

- SWOT Analysis

- We work

- WOJO

- Regus group

- Mindspace

- KNOTEL

- Ordnung aps

- Matrikel 1

- Green desk

- DBH business services

Recent Developments

- we work companies LLC announced that it has assigned an agreement with one leading real estate companies in Israel, Ampa group. The deal would allow WeWork to expand its operations in Israel.

- jones Lang LaSalle, IP, INC. announced that it has signed a vested agreement with bp to transform its workplaces globally. JLL has been associated with bp for over a decade, and the deal would allow JLL to meet the Net Zero Carbon ambitions of the latter.

- Report ID: 3104

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Flexible Space Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.