Compression Therapy Market Outlook:

Compression Therapy Market size was valued at USD 4.8 billion in 2025 and is projected to reach USD 8.5 billion by the end of 2035, rising at a CAGR of 5.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of compression therapy is evaluated at USD 5.1 billion.

The global market demand is linked to the rising burden of chronic venous disorder, diabetes related complications, lymphedema, and post-surgical recovery needs. According to the NLM October 2021 study, the chronic venous insufficiency and varicose vein conditions affect an estimated 23% of adults in the U.S., with 11 million men and 22 million women aged 40 to 80 years. Besides, the NLM study in October 2025 shows lymphedema affects more than 140 to 250 million people globally, largely related to cancer treatment and aging, directly supporting the sustained institutional demand for compression-based interventions. On the other hand, the compression therapy is embedded within standard care pathways for venous leg ulcers. These ulcers are associated with high recurrence rates and long treatment durations, driving repeat utilization across hospitals, outpatient wound centers, and long-term care settings.

Further, the government expenditure trends reinforce the market stability. As per the NLM study in September 2022, chronic wounds, including venous leg ulcers, impose a financial burden on people. Moreover, the treatment is complicated, leading to the high utilization of resources and wound recurrence. As per the study, the U.S. for Medicare beneficiaries indicated the highest costs in hospital outpatient care, ranging from USD 9.9 to USD 35.8 billion, with compression therapy reimbursed as part of conservative and post-acute care bundles. Additionally, the public health guidelines from the organizations recommend compression as the first line management for venous leg ulcers and post thrombotic syndrome, ensuring continued procurement via centralized tenders. Collectively, these data highlight a long-term reliance on compression therapy within publicly funded care systems.

Chronic Wound Economic Burden Statistics

|

Region/Country |

Statistic/Details |

Estimated Cost |

|

Australia (Acute Hospitals) |

Annual costs for 47,300 VLU cases |

USD 785 million |

|

Australia (Residential Aged Care) |

Annual costs for 1,740 cases |

USD 18 million |

|

U.S. (Medicare) |

Expenditures for venous wounds and infections (2014) |

USD 1.5 billion (~1/5 of total) |

|

United Kingdom (NHS) |

Wound prevalence increases 2012-2018; management costs up 48% in real terms |

71% prevalence rise |

Source: NLM September 2022

Key Compression Therapy Market Insights Summary:

Regional Highlights:

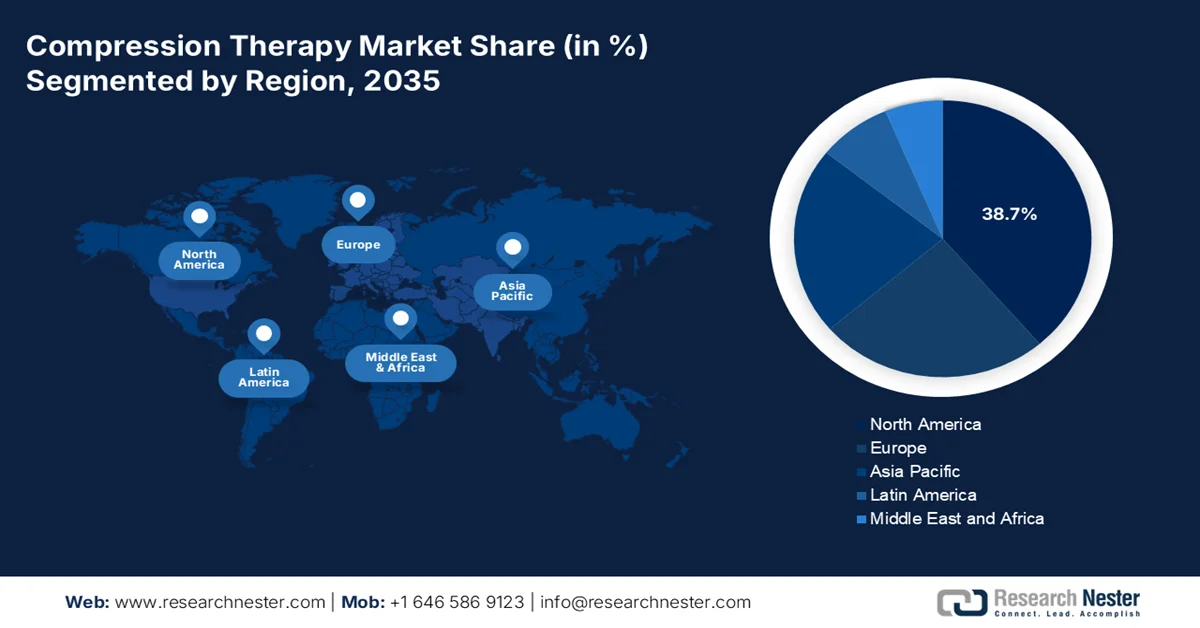

- North America in the compression therapy market is projected to command a 38.7% revenue share by 2035, impelled by an aging population, high prevalence of obesity and diabetes, and established reimbursement frameworks supporting home-based care adoption.

- Asia Pacific is anticipated to witness the fastest expansion through 2035, stimulated by rapid healthcare infrastructure modernization, rising healthcare expenditure, and increasing surgical volumes necessitating venous thromboembolism prophylaxis.

Segment Insights:

- In the compression therapy market, the synthetic materials segment is projected to account for a dominant 75.6% share by 2035, propelled by the rising prevalence of varicose veins and the superior durability, consistent compression gradients, and moisture-wicking performance of nylon, polyester, and spandex blends.

- The static compression therapy segment is expected to retain the largest revenue share by 2035, driven by its established position as the gold standard first-line treatment for venous leg ulcers and the substantial burden of chronic wounds requiring constant pressure management.

Key Growth Trends:

- Public healthcare spending on chronic disease

- Growing prevalence of chronic venous disorders and lymphedema

Major Challenges:

- Cost pressure and pricing constraints from healthcare systems

- High R&D and clinical evidence requirements

Key Players: 3M (U.S.), Essity Aktiebolag (publ) (Sweden), Cardinal Health (U.S.), Smith & Nephew plc (UK), Paul Hartmann AG (Germany), BSN medical (Germany), Medtronic plc (Ireland), ConvaTec Group PLC (UK), Arjo (Sweden), SIGVARIS GROUP (Switzerland), medi GmbH & Co. KG (Germany), Julius Zorn GmbH (Germany), DJO Global (U.S.), Lohmann & Rauscher (Germany), Becton, Dickinson and Company (U.S.), Tactile Medical (U.S.), Ofa Bamberg (Germany), Nitto Denko Corporation (Japan), Bio Compression Systems, Inc. (U.S.), CONTINENTAL S.r.l. (Italy)

Global Compression Therapy Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.8 billion

- 2026 Market Size: USD 5.1 billion

- Projected Market Size: USD 8.5 billion by 2035

- Growth Forecasts: 5.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, Brazil, South Korea, Mexico, Indonesia

Last updated on : 11 February, 2026

Compression Therapy Market - Growth Drivers and Challenges

Growth Drivers

- Public healthcare spending on chronic disease: The growth in the government healthcare expenditure is the key driver for the market demand. According to the OECD November 2025 report, the average health spending across member countries reached 9.3% of GDP, with a growing share allocated to chronic disease management and aging-related care. In the U.S., the MIT Science Policy Review August 2025 data shows the national health expenditure exceeded USD 4.9 trillion, with the post-acute and outpatient care growing faster than the inpatient services settings, where the compression therapy is routinely reimbursed. The Europe countries allocate an increasing portion of public budgets to long-term vascular and wound care under statutory insurance systems. This sustained fiscal commitment enables stable procurement of compression products by hospitals and community care providers.

- Growing prevalence of chronic venous disorders and lymphedema: The epidemiological trends directly support compression therapy market utilization. As per the NLM November 2022 study, it is estimated that less than 25 million people in the U.S have chronic venous insufficiency, and 57% men and 73% women reported the prevalence of varicose veins. On the other hand, the lymphedema patients in the U.S. are largely linked to cancer survivorship and aging. These conditions require long duration repeat compression use driving the volume demand rather than one time treatment. Moreover, the public health systems classify compression therapy as a standard conservative management, ensuring inclusion in treatment protocols and reimbursement schedules. Further, the lymphedema-related care demand is rising across Asia and Europe, increasing compression therapy adoption in oncology-linked care settings.

- Aging population and mobility related care: Demographic aging is a long-term demand accelerator in the market. According to the United Nations 2023 data, the global population aged 65 and above will increase from 761 million in 2021 to 1.6 billion by 2050, with Europe and East Asia aging faster. Further, the older populations exhibit a higher incidence of venous insufficiency, edema, and reduced mobility conditions routinely managed with compression therapy. Moreover, the public health systems are responding by expanding home healthcare and community-based services where the compression therapy is preferred due to its non-invasive nature. Additionally, the government expenditure also highlights that the public spending on long-term care and home-based services is rising steadily, with the OECD countries allocating an increasing share of health budgets to community and domiciliary care programs that incorporate compression therapy for elderly patients with circulatory and mobility limitations.

Challenges

- Cost pressure and pricing constraints from healthcare systems: The global healthcare cost containment is a major challenge in the compression therapy market. In markets such as the U.S., the reimbursement rates from Medicare and private insurers are often fixed, squeezing the margins. Moreover, in Europe, the national health systems negotiate aggressive bulk pricing. Companies must demonstrate superior cost-effectiveness to justify the premium pricing. Top players compete by highlighting the clinical outcomes and reduced nursing time to justify their cost versus traditional bandages, battling for favorable formulary placement under the NHS procurement budgets.

- High R&D and clinical evidence requirements: Developing innovative, effective products requires substantial R&D investment and robust clinical data to prove efficacy and safety for reimbursement. Startups face a significant burden in the market. Leading players consistently invest in clinical studies to validate their gradient compression technology, pushing research on outcomes for venous leg ulcer and lymphedema. Further, various trials are being performed related to compression therapy, highlighting the intensive evidence environment manufacturers must engage with.

Compression Therapy Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.8% |

|

Base Year Market Size (2025) |

USD 4.8 billion |

|

Forecast Year Market Size (2035) |

USD 8.5 billion |

|

Regional Scope |

|

Compression Therapy Market Segmentation:

Material Segment Analysis

The synthetic materials are leading and are poised to hold the largest market share of 75.6% by 2035. The material, mainly nylon, polyester, and spandex blends, constitutes the leading sub-segment by material type, dominating the market due to their high durability, consistent compression gradients, moisture-wicking properties, and aesthetic appeal over natural fibers such as rubber and cotton. These advanced textiles enable the production of effective, comfortable, and patient-compliant garments for long-term use. Further, the data from the International Journal for Multidisciplinary Research in February 2025 shows that the prevalence of diagnosed varicose veins in adults was 9.8%, indicating a vast ongoing patient pool requiring synthetic compression garments for daily management.

Technology Segment Analysis

The static compression therapy is holding the largest market share value within the technology segment. The market is characterized by the use of constant pressure devices such as compression garments and inelastic bandages. Its leadership is attributed to its role as the first-line gold standard treatment for conditions such as venous leg ulcers, offering cost-effectiveness, ease of use, and proven clinical efficacy. The high prevalence of chronic wounds solidifies its market position. Besides, the NLM study in February 2022 indicates that in the U.S., nearly 6.5 million patients were affected by chronic wounds, a significant portion of which require static compression as a core component of management, fueling consistent demand for these technologies.

Product Type Segment Analysis

The compression garments are holding the largest share value in the compression therapy market. The compression garments include gradient compression stocking sleeves and socks. This dominance is due to the widespread application of both preventive care and chronic condition management, alongside high patient adoption due to improved comfort and aesthetics. The demand is sustained by the aging population and rising awareness of venous diseases. According to the NLM study in March 2024, the study indicates that compression garments reduce the muscle strength decline over a duration of 1-24 hr for trained individuals and over 72 hr for both trained and untrained individuals. Moreover, continuous innovation in the material further strengthens the long term adherence and repeat purchase decisions.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Technology |

|

|

Application |

|

|

Distribution Channel |

|

|

End user |

|

|

Material |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Compression Therapy Market - Regional Analysis

North America Market Insights

North America market is dominating and is expected to hold the regional revenue share of 38.7% by 2035. The market is defined by high technological adoption, stringent regulatory oversight, and a well-established reimbursement framework. The dominant drivers include an aging demographic, a high prevalence of obesity and diabetes conditions that significantly increase the risk of venous disease, and robust clinical guidelines mandating compression for postoperative venous thromboembolism prophylaxis in surgical settings. The key trend is the shift of care from inpatient to home settings, supported by the reimbursement policies. This drives the demand for advanced patient-applied devices and retail-grade compression wear. Overall, the market is consolidated, with major players competing on portfolio breadth, clinical evidence, and direct integration into value-based care pathways.

In the U.S. compression therapy market, the demand is supported by the regulatory clearances, high chronic disease prevalence, and growing surgical volumes. In April 2023, the U.S. FDA granted the 510 (k) clearance to AIROS Medical for its AIROS 8P sequential compression system, including the expanded garment indication for truncal and abdominal swelling, indicating a continued regulatory support for advanced compression solutions in lymphedema and venous care. Besides, the disease prevalence remains the major utilization driver. As per the NLM October 2025 study, 1 in 100,000 individuals in the U.S. are affected by lymphedema, while millions more suffer from chronic venous insufficiency conditions routinely managed with compression therapy. Additionally, the CDC November 2024 data indicates that the total diabetes prevalence at 15.8%, increasing the risk of venous edema, venous complication and post surgical swelling that require compression-based management. Overall, the prevention of these diseases is strengthening sustained institutional procurement across hospitals and outpatient centers.

Relevance of Regulatory and Clinical Announcements to the U.S.

|

Date |

Company Name |

Announcement Type |

Therapy Area |

|

April 4, 2023 |

AIROS Medical |

FDA 510(k) clearance for AIROS 8P Sequential Compression Therapy device |

Lymphedema, Venous complications |

|

March 2025 |

Jiale Health Technology Shenzhen Co., Ltd. |

510(k) substantial equivalence determination |

Medical compression leg massager device |

|

May 26, 2021 |

Koya Medical |

FDA 510(k) clearance for Dayspring active compression therapy system |

Lymphedema, Venous disease |

|

October 2023 |

Jiangsu MaxF Electric Appliance Co., Ltd |

510(k) clearance letter (device equivalence confirmation) |

Compression-related medical device |

|

December 19, 2025 |

Cytokinetics |

FDA approval of MYQORZO (aficamten) |

Obstructive hypertrophic cardiomyopathy |

Source: AIROS Medical, Jiale Health Technology Shenzhen Co., Ltd., Koya Medical, Jiangsu MaxF Electric Appliance Co., Ltd, Cytokinetics

The market in Canada is supported by the publicly funded healthcare delivery, aging demographics, and the rising utilization of community-based care for chronic conditions. According to Statistics Canada's September 2025 data, adults aged 65 years and older accounted for 19.5% of the population in 2025, expanding the patient base for venous lymphatic and mobility-related care routinely managed with compression therapy. The World Bank December 2025 data shows that the current healthcare expenditure is 11.31% GDP in Canada. Besides the Health Canada maintains the medical device licensing pathways aligned with the international regulatory standards, supporting the consistent market access for compression therapy devices across provinces. These trends indicate a stable market demand in Canada.

APAC Market Insights

The Asia Pacific compression therapy market is growing rapidly and is defined by the high growth potential driven by diverse but converging factors. The primary driver is the rapid expansion and modernization of healthcare infrastructure, increasing access to medical devices. This is complemented by rising healthcare expenditure from both public and private sector growing awareness of chronic venous diseases, and a surging burden of aging populations, diabetes, and obesity. The surgical volume is also rising significantly, increasing the need for VTE prophylaxis. Moreover, the key trends include the local manufacturing and regulatory harmonization efforts, such as those by the ASEAN Medical Device Directive, to lower costs and improve access. The market is seeing a shift from basic elastic bandages to more advanced gradient compression garments and pneumatic devices, mainly in urban hospital settings.

India’s market is emerging steadily and is supported by a growing burden of chronic vascular conditions, rising surgical volumes, and expanding public investment in hospital and community healthcare infrastructure. According to the NLM March 2024 study, the non-communicable diseases account for over 60% of the total deaths in India, with diabetes, cardiovascular disease, and obesity increasing the incidence of venous insufficiency, edema, and chronic wounds that require compression-based management. Moreover, the Ayushman Bharat PM JAY scheme is publicly funded inpatient and post acute care, including the surgical procedures, where compression therapy is routinely used for edema control and thrombosis prevention. Besides, the UNFPA 2023 data shows that the people aged above 60 represent 1.1 billion of the total population, driving the demand for non-invasive therapies in home and outpatient settings. Together, expanding public coverage, demographic aging, and rising chronic disease prevalence are strengthening the long-term demand outlook for compression therapy across Indian hospitals, ambulatory centers, and home healthcare providers.

The high and growing burden of varicose vein disease and the rapid adoption of minimally invasive treatments, such as radiofrequency ablation and endovenous laser ablation, are driving the market in China. Moreover, the compression therapy has replaced the traditional high ligation and stripping due to faster recovery and lower complication rates. As per the NLM study in October 2023, compression therapy is a standard adjuvant after thermal ablation to support the vein occlusion, reduce postoperative pain, and limit bruising. With varicose veins affecting an estimated 10–30% of the adult population and prevalence increasing with age, the expanding elderly demographic is driving a large procedural volume across tertiary and regional hospitals. Moreover, the study depicts that the short-term compression for about 24 hrs to 48 hrs reflects a broader shift toward simplified patient-centric care pathways aimed at improving compliance. These findings highlight a sustained growth in China’s compression therapy market within hospital, ambulatory, and home-care settings.

Europe Market Insights

The compression therapy market in Europe is growing significantly and is defined by a mature healthcare infrastructure rapidly aging population, and universal health coverage models. These factors create a stable and expanding patient base for the lymphatic and chronic venous conditions. Moreover, the growth is fundamentally driven by the demographic pressures and high prevalence of obesity and diabetes as key factors. Further, the demand is propelled by the stringent national clinical guidelines promoting compression as the first-line treatment for venous leg ulcer and post surgical VTW prophylaxis. Moreover, the market is shifting towards the patient friendly products to support home-based care models, reducing the hospital burden via active outpatient management and digital health integration.

Strong clinical evidence, high outpatient surgical activity, and statutory reimbursement under the public health insurance system are driving the market in Germany. According to the NLM study in March 2024, clinical evidence based on 12 randomized controlled trials demonstrates that compression therapy, when added to the pharmacological treatment during the acute phase of lower limb deep venous thrombosis, results in significantly faster pain reduction and reduced limb swelling. Further multiple randomized controls show that the medical compression stockings reduce the incidence and severity of post-thrombotic syndrome by 16% to 27%, confirming a relative risk reduction of 34%. These findings align with Germany’s guideline-driven healthcare system, where therapies supported by strong clinical evidence are routinely reimbursed under the statutory health insurance (GKV). Further Germany’s high burden of venous disease and emphasis on outpatient vascular care, this level of validated efficacy supports sustained demand for compression therapy across hospitals, vascular clinics, and ambulatory care settings.

The compression therapy market in UK is positioned for steady growth supported by the regulatory approvals, rising venous disease burden, and NHS-led adoption of advanced wound and thrombosis prevention solutions. The EU and UK regulatory approval of ConvoMatrix in September 2025 strengthens the UK market by expanding the treatment options for venous leg ulcers and diabetic foot ulcers, conditions where compression therapy is routinely used along with advanced wound dressing. Besides the recent development in October 2025 by the international launch of Cardinal Health’s Kendall SCD SmartFlow compression system, which reinforces the demand for intermittent pneumatic compression in UK hospitals, mainly for deep vein thrombosis and pulmonary embolism prevention. These developments align with NHS England’s focus on reducing VTE-related complications, improving outpatient and community wound care outcomes, and supporting continued growth of compression therapy utilization across UK hospitals, outpatient clinics, long-term care facilities, and home care settings.

Key Compression Therapy Market Players:

- 3M (U.S.)

- Essity Aktiebolag (publ) (Sweden)

- Cardinal Health (U.S.)

- Smith & Nephew plc (UK)

- Paul Hartmann AG (Germany)

- BSN medical (Germany)

- Medtronic plc (Ireland)

- ConvaTec Group PLC (UK)

- Arjo (Sweden)

- SIGVARIS GROUP (Switzerland)

- medi GmbH & Co. KG (Germany)

- Julius Zorn GmbH (Germany)

- DJO Global (U.S.)

- Lohmann & Rauscher (Germany)

- Becton, Dickinson and Company (U.S.)

- Tactile Medical (U.S.)

- Ofa Bamberg (Germany)

- Nitto Denko Corporation (Japan)

- Bio Compression Systems, Inc. (U.S.)

- CONTINENTAL S.r.l. (Italy)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- 3M uses its advanced material science and global commercial footprint. The company’s strategic initiatives focus on integrating its diverse wound care and surgical portfolios to offer comprehensive solutions from cohesive bandages to advanced layered systems. According to the 2024 annual report, the company has made a net sale of USD 11.08 billion.

- As a global hygiene and health leader, Essity holds a commanding position in the compression therapy market via brands such as JOBST and Leukoplast. The company’s strategy emphasizes a holistic approach to compression, combining premium medical compression garments with consumer-centric self-care products. Nearly 20% of the total net sales are from the health and medicine sector in 2024.

- Cardinal Health competes in the compression therapy market primarily via its vast distribution network and portfolio of its own brand medical products. Its strategic initiatives are centered on providing cost-effective, reliable compression solutions to a broad base of healthcare facilities and providers.

- Within the compression therapy market, Smith & Nephew’s strategic focus is on advanced wound management, where compression is a significant component. The company integrates its compression technologies, such as the ACTIVA line, with its advanced wound dressings and negative pressure wound therapy systems.

- Paul Hartmann AG is a key leader in Europe in the compression therapy market, renowned for systems such as the Tensopress and Setopress. The company’s strategy is built on a foundation of high-quality, innovative textile design and a strong commitment to clinical education. Strategic initiatives include developing multi-layer compression kits that simplify correct application for clinicians.

Here is a list of key players operating in the global market:

The global compression therapy market is fragmented, with the dominant multinational med tech corporations competing alongside specialized players. The key strategic initiatives include extensive investment in R&D to develop advanced materials and hybrid pneumatic devices. The market leaders are actively expanding via acquisitions of smaller niche companies and forging distribution partnerships to strengthen the geographic reach, mainly in high-growth emerging markets. For example, in November 2025, Solventum announces an agreement to acquire Acera Surgical. Moreover, a strong focus is on the direct-to-consumer marketing and educational initiatives for both patients and clinicians, which is also prevalent, aiming to drive the adoption of conditions such as lymphedema and chronic venous insufficiency.

Corporate Landscape of the Compression Therapy Market:

Recent Developments

- In September 2025, PurelyIV introduced Therabody RecoveryAir JetBoots compression therapy. Therabody RecoveryAir JetBoots are an advanced pneumatic compression system that uses dynamic air technology to provide a wave-like massage to the legs.

- In September 2025, AIROS Medical, Inc., a designer specializing in compression therapy devices that treat lymphedema and venous complications, announced the launch of expanded sizing for its truncal garments.

- In November 2024, Cardinal Health announced the U.S. launch of its Kendall SCD SmartFlow Compression System, the next generation of the Kendall Compression Series, offering an enhanced clinician and patient experience.

- Report ID: 4858

- Published Date: Feb 11, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.