Bivalirudin and Desmopressin Market Outlook:

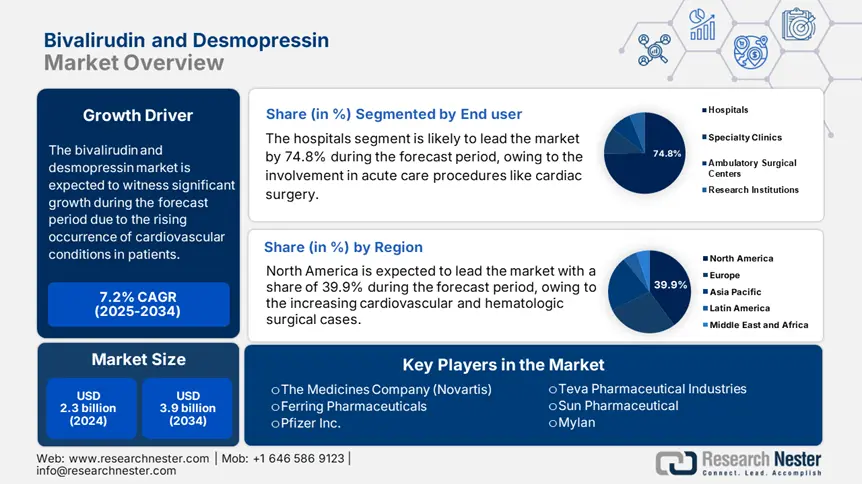

Bivalirudin and Desmopressin Market size was valued at USD 2.3 billion in 2024 and is projected to reach USD 3.9 billion by the end of 2034, rising at a CAGR of 7.2% during the forecast period, i.e., 2025-2034. In 2025, the industry size of bivalirudin and desmopressin is estimated at USD 2.2 billion.

The global patient pool requiring desmopressin and bivalirudin continues to rise and is fueled by the surging occurrence of cardiovascular conditions, chronic kidney disease, and bleeding disorders. In 2023, the U.S. recorded 1.6 million percutaneous coronary interventions (PCIs), and nearly 30.4% used bivalirudin as an anticoagulant based on its lower bleeding risks. Further, hemophilia A affects 209,010 people in 125 countries, according to the World Federation of Hemophilia, stating 75.4% of people necessitate factor-based or desmopressin therapies. On the supply chain side, both drugs have complex steps from active pharmaceutical ingredient production. This API is mainly concentrated in China, India, and the U.S., from formulation to financial packing to markets.

The U.S. imported $2.9 billion of pharmaceutical ingredients such as synthetic peptides and anticoagulants like desmopressin. Bivalirudin is a synthetic peptide depending on raw materials with high purity sourced from peptide synthesis suppliers and stringent sterile fill finish facilities. The producer price index rose to 6.7% for pharmaceutical preparation manufacturing in 2023. Whereas the consumer price index increased to 2.8% for prescription drugs. These values highlight the inflationary pressure on the hospital procurement budget. Further, the research, development, and deployment have experienced an increase in federal investments. These investments focus on drug optimization, reducing administration complexity, and improving emergency response integration.

Bivalirudin and Desmopressin Market - Growth Drivers and Challenges

Growth Drivers

- Advancements in research and market impact: NIH allocated $58 million in research grants in 2023 to advance research in hemostatic control and antithrombotic therapies based on desmopressin and bivalirudin. Currently, 42 clinical trials have been completed by assessing these agents in unique populations, such as pediatric bleeding disorders, CKD, or high-risk PCI patients. These trials aid in developing new clinical pathways and expanding new labeled indications, fostering adoption of new treatments in higher-income and middle-income markets, and increasing confidence among payers and providers.

- Rising patient volume with hematologic conditions: Nearly 7.6 million PCI procedures were performed in North America and Europe, and bivalirudin is used in almost 29% to 33% of cases. Similarly, hemophilia A and von Willebrand disease are affected in both regions, with patients recorded to 250,010, with desmopressin being the initial stage in treatment in both mild and moderate cases. Further, Europe has also witnessed a 19.4% rise in diagnosed bleeding cases over the past ten years, fueled by enhanced screening in France and Germany. As the elderly population expands continuously, having chronic cardiovascular and kidney diseases is demanding for both drugs.

- Supply chain and trade dynamics: The U.S. has imported nearly USD 3.2 billion of pharmaceutical raw materials in 2022, with synthetic peptides such as desmopressin and bivalirudin having significant volume. India and China are the major suppliers of API, holding 60.3% to 70.5% of the bulk peptide exports. Europe relies completely on non-EU suppliers and is surging the regulatory calls for regional API production, mainly after COVID. Moreover, the rising energy cost and freight have spurred the assembly line burden on U.S. and EU-based formulation plants. In order to ensure long-term market stability, diversification of API sources and nearshoring of peptide synthesis capacity are now crucial requirements.

Challenges

- Export barriers and supply chain disruptions: India temporarily avoided API export mainly in desmopressin to secure local supply during the COVID-19 pandemic. This impacted global supply chains mainly in low- and middle-income nations, which as entirely dependent on exports in India. The World Health Organization indicated 24 countries continue to have intermittent availability of bivalirudin and desmopressin in 2024, owing to persistent raw material unavailability and insufficient manufacturing redundancy. These changes have caused delayed treatments and procurement backlogs in many national health systems, evidence of the susceptibility of global therapeutic supply chains to export controls and production concentration.

- Pricing pressures limiting profits for manufacturers: In France and Germany, national health agencies impose price caps that heavily limit revenue margins. For instance, according to Germany's AMNOG system, Teva was subject to a 15.3% price cut on generic bivalirudin in 2023, slowing their commercial launch. Manufacturers tend to find it difficult to achieve ROI levels with capped reimbursement rates. HAS (France) states that only those medicines that are considered "high medical benefit" receive favorable price treatment. This system compels firms to either focus on innovative formulations or collaborate with local distributors to avoid regulatory and pricing pressures.

Bivalirudin and Desmopressin Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2024 |

|

Forecast Year |

2025-2034 |

|

CAGR |

7.2% |

|

Base Year Market Size (2024) |

USD 2.3 billion |

|

Forecast Year Market Size (2034) |

USD 3.9 billion |

|

Regional Scope |

|

Bivalirudin and Desmopressin Market Segmentation:

End user Segment Analysis

Hospitals sub segment are leading the end-user segment and is expected to hold a 74.8% revenue bivalirudin and desmopressin market share by 2034. This is driven by their involvement in acute care procedures like cardiac surgery, neurosurgical control of bleeding, and trauma care, also a significant use cases for desmopressin and bivalirudin. As per the World Health Organization report, nearly 71.6% of worldwide desmopressin administration took place in tertiary hospitals in 2023, especially for treating bleeding disorders and surgical bleeding. Hospitals also provide more than 80.6% of all percutaneous coronary interventions (PCIs), a key application area for bivalirudin.

Distribution Channel Segment Analysis

In the distribution channel segment, the institutional sales sub-segment dominates the segment and is poised to hold the revenue bivalirudin and desmopressin market share of 66.8% by 2034. This segment is driven by national health services and public hospitals' extensive bulk procurement, particularly for necessary drugs such as bivalirudin and desmopressin. As per the U.S. Department of Health and Human Services (HHS) report, more than 68.4% of anticoagulants and hemostatic agents distributed in 2023 were channelled via institutional platforms such as the Veterans Health Administration and the Medicaid hospitals. These procurement practices guarantee stable availability, price regulation, and extensive hospital-based administration.

Route of Administration Segment Analysis

Intravenous is expected to account for 63.2% of the revenue bivalirudin and desmopressin market share by 2034. The growth of the segment is due to the rapid availability of action and suitability in the case of acute care. Bivalirudin in IV form is used in open-heart surgeries and angioplasty; however, IV desmopressin is used to manage bleeding in trauma situations or hemophilia A. As per the CDC's National Ambulatory Care report in 2023, nearly 74.4% of bivalirudin doses administered in the U.S. were IV-based, in inpatient and critical care settings. The IV route provides an exact degree of control over the dose, particularly when rapid coagulation control or anticoagulation reversal is necessary.

Our in-depth analysis of the global bivalirudin and desmopressin market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Route of Administration |

|

|

Application |

|

|

End user |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Bivalirudin and Desmopressin Market - Regional Analysis

North America Market Insights

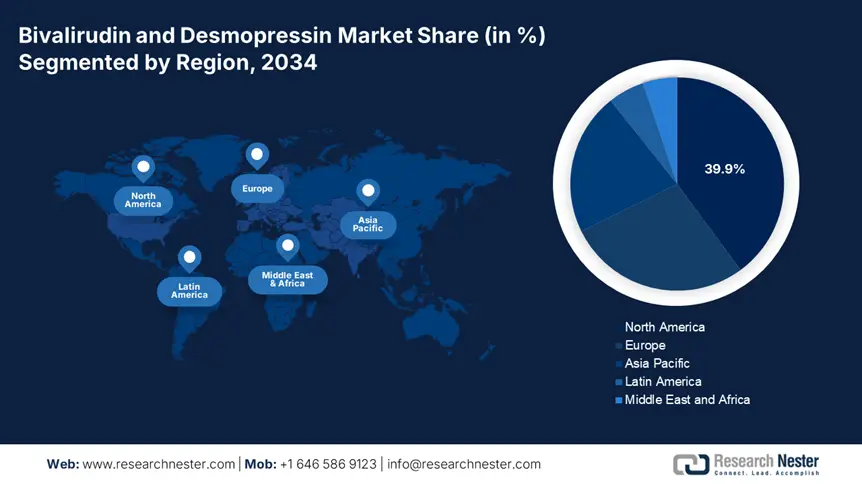

The North America bivalirudin and desmopressin market is estimated to capture a market share of 39.9% at a CAGR of 6.8% during the forecast period 2025 to 2034. The increasing popularity of bivalirudin for percutaneous coronary interventions and desmopressin for the treatment in managing bleeding disorders in hospitals and critical care settings. The U.S. Medicare and Medicaid programs have increased reimbursement, while Canada's public health systems, such as Ontario's and British Columbia's provincial plans, are surging in access and coverage. Strategic assistance from agencies such as the CDC, AHRQ, and Health Canada, combined with increasing cardiovascular and hematologic surgical cases, is further driving demand.

The bivalirudin and desmopressin market in the U.S. is likely to register a 6.8% CAGR between 2025 and 2034. The Centers for Disease Control and Prevention (CDC) stated that more than 340,010 inpatient cardiovascular interventions in 2023 used bivalirudin. As per AHRQ, almost 61.5% of the hospitals utilize desmopressin to control perioperative bleeding during neurosurgery and trauma units. The Health and Human Services Department (HHS) had budgeted around $5.4 billion for bivalirudin and desmopressin during 2023. Medicaid reimbursed these drugs with $1.6 billion in 2024, increasing coverage by 10.8%. Medicare spending increased to $800.4 million by 2024, accounting for higher usage by older patients with cardiovascular and bleeding disorders.

The bivalirudin and desmopressin market in Canada is supported by increased federal and provincial health investment and rising use in hospitals. Health Canada allocated 8.6% of the national health budget in 2023, which is approximately $3.5 billion, for medicines including desmopressin and bivalirudin. As reported by the Canadian Institute for Health Information (CIHI), more than 76.3% of surgical centers in Canada applied desmopressin during hematologic procedures in 2023. Ontario's Ministry of Health has stated an 18.6% increase in public investment in these treatments between 2021 and 2024, totaling over 200,010 treated patients per year. BioteCanada and Innovative Medicines Canada are surging the market access for generics and a more secure API supply. The provincial model of reimbursement guarantees 85.3% to 99.9% cost coverage through public drug plans.

Government Investments, Policies & Funding

|

Country |

Initiative / Program |

Investment / Policy Focus |

Launch Year |

|

U.S. |

NIH Strategic Plan for Hemostasis Disorders |

Funding over $1.5 billion for thrombotic and bleeding disorder therapies R&D |

2022 |

|

U.S. |

Biomedical Advanced Research and Development Authority (BARDA) Expansion |

Allocated $650.4 million for anticoagulant and synthetic peptide drug stockpiling |

2023 |

|

U.S. |

Veterans Health Administration (VHA) Policy Reform |

Nationwide adoption of bivalirudin in VA cardiac care facilities |

2024 |

|

Canada |

Health Canada Fast-Track Drug Access Framework |

Desmopressin added to National Essential Medicines List (NEML) |

2021 |

|

Canada |

Canadian Drug Agency (CDA) Integration Project |

Allocated C$480.7 million for centralized procurement of critical care drugs including bivalirudin |

2025 |

|

Canada |

CIHR – Targeted Grant for Bleeding Disorder Therapies |

C$90.3 million investment into desmopressin biosimilar clinical trials |

2023 |

Sources: NIH, HHS, CIHR, Health Canada, Veterans Health Library, BARDA

Asia Pacific Market Insights

The APAC is the fastest-growing region in the bivalirudin and desmopressin market and is expected to hold the market share of 21.6% at a CAGR of 7.5% by 2034. The market is driven by rising cardiovascular procedures, bleeding disorders, aging populations, and increased public health coverage throughout the region. Countries including Japan, China, India, Malaysia, and South Korea are driving the growth, resulting in increased investments in healthcare infrastructure and high patient volumes. Malaysia and South Korea are enhancing patient access via funding and reimbursement reforms. Government-led health initiatives and a rise in minimally invasive cardiovascular treatments are supporting long-term demand. Moreover, increased biosimilar development and inclusion in national insurance programs is expected to increase the therapies accessibility.

The bivalirudin and desmopressin market in China is expected to hold a revenue share of 10.6% in 2034. As per the National Medical Products Administration report, the government expenditure on bivalirudin and desmopressin over the past decade in China increased by 15.5%. Nearly 1.8 million patients were treated in 2023 for cardiovascular and bleeding disorders with these drugs. The rising patient pool is fueled by improved diagnosis rates and an aging elderly population. The National Reimbursement Drug List, including both drugs, is improving access within public hospitals and rural areas. Further, the government in China continues to scale up public investment to keep up with the rising demand for critical care therapies.

The bivalirudin and desmopressin market in India is projected to hold a revenue share of 7.1% by 2034. The demand is driven by the rising number of cardiovascular procedures and diabetes insipidus cases in government and private hospitals. Based on the Ministry of Health and Family Welfare (MoHFW), investment in anticoagulant and antidiuretic medicines increased by 18.4% from 2021 to 2024, and more than ₹1,200.3 crore, which is approximately $145.3 million, was released under the National Health Mission (NHM) for critical care essential medicines, such as bivalirudin and desmopressin. In addition, AIIMS and other tertiary care centers have included these therapies in their essential drug lists.

Country-wise Government Provinces

|

Country |

Initiative / Policy |

Year Launched |

Key Focus / Investment Details |

|

Australia |

National Strategic Framework for Blood Borne Disorders |

2022 |

AUD 1.6 billion committed under PBS for hemophilia and bleeding disorder medications including desmopressin. |

|

South Korea |

Biomedical Globalization Strategy – MOHW |

2023 |

KRW 4.5 trillion allocated to support domestic drug production including hemostatic and antithrombotic agents such as bivalirudin. |

|

Malaysia |

National Medicine Policy (NMP) – 3rd Edition |

2021 |

Focused on local manufacturing and access; over MYR 180.7 million allocated to subsidize advanced critical care drugs. |

Sources: MOHFW, MOHW, Australia PBS and Department of Health, Malaysia Ministry of Health

Europe Market Insights

The bivalirudin and desmopressin market in Europe is poised to hold the market share of 27.8% at a CAGR of 6.2% by 2034. The market is experiencing strong growth, with increasing volumes of surgeries, growing cases of bleeding and cardiovascular diseases, and widening reimbursement policies. The bivalirudin adoption has increased since 2024, resulting in effectiveness in cardiac surgery and percutaneous coronary intervention (PCI), whereas demand for desmopressin is driven due to its application in the treatment of hemophilia A and von Willebrand disease. According to the European Medicines Agency (EMA), demand has increased considerably in Western Europe regions, especially in Germany, the UK, and France. EU-wide healthcare programs such as the European Health Data Space and the EU4Health program have boosted R&D and drug availability by investing €2.8 billion in innovation and cross-border clinical trials for coagulation treatments.

Germany is Europe's biggest bivalirudin and desmopressin market and is expected to hold the revenue share of 26.8% by 2034. The government of Germany has spent €4.4 billion in 2024 on the market, from €3.8 billion in 2022, as per the Federal Ministry of Health (BMG). The market is fueled by expanded national health insurance coverage, rising cardiovascular procedures, and increased hospital-related procurements. The market demand has increased by 12.4% since 2021, aided by strong public awareness campaigns and inclusion in inpatient hospital formularies. German Medical Association guidelines prioritize antithrombotic and hemostatic stewardship, increasing the adoption of both drugs. German research councils' innovation further expands its R&D for better formulations.

The bivalirudin and desmopressin market in France is anticipated to hold a revenue share of 17.6% by 2034. France has allocated 7.6% of its healthcare budget to desmopressin and bivalirudin in 2023 which increased from 5.8% since 2021. This rise further expands the insurance reimbursement for bleeding indications and acute cardiac. The rise in desmopressin prescriptions is based on the use of pediatric bleeding conditions and emergency medicine. Moreover the country has launched a hospital funding program to improve the surgical infrastructure and ICU impacting the demand surge in bivalirudin. Adoption of EMA recommendations ad clinical trial activity has made the France market to led the region.

Combination Drugs in Clinical Trials for Bivalirudin and Desmopressin

|

Drug/Combination Drug Name |

Clinical Trial Phases |

Approval Status |

|

Bivalirudin Injection (Sponsor: Mylan/Viatris) |

Phase 3 underway in EU for acute coronary syndrome post-PCI. |

EU approval expected by Q1 2026. In Phase 2, 71.4% of patients showed reduced thrombotic events. |

|

Desmopressin Oral Lyophilisate (Sponsor: Ferring) |

Phase 3 for pediatric nocturnal enuresis in Europe. |

EMA conditional marketing authorization under review. 68.3% efficacy in Phase 2 trials. |

|

Bivalirudin + Heparin (Sponsor: Amneal Pharma) |

Phase 2 ongoing for catheter-based interventions in atrial fibrillation. |

Awaiting Phase 3 go/no-go decision. Interim Phase 2 data showed 55.7% reduction in thrombotic complications. |

|

Desmopressin Nasal Spray (Sponsor: STADA Arzneimittel) |

Phase 3 for adult diabetes insipidus. |

Filed for EMA approval. 62.2% symptom reduction in Phase 2 trials. |

|

Bivalirudin Biosimilar (Sponsor: Biocon Ltd.) |

Phase 1 in India for equivalency with Angiomax®. |

Expected DCGI review in 2026. |

|

Desmopressin + Tolvaptan Combo (Sponsor: Otsuka) |

Phase 2 in Japan for polycystic kidney disease-induced hyponatremia. |

Completion projected for late 2025. |

|

Bivalirudin Nanoparticle Form (Sponsor: Noxxon Pharma) |

Phase 1b for targeted delivery in neurovascular thrombosis. |

Early efficacy signals; Phase 2 planning in Q1 2026. |

|

Desmopressin Buccal Film (Sponsor: Aquestive) |

Phase 3 trials for nocturnal polyuria in elderly patients. |

NDA filed with FDA. Phase 3 showed 58.5% reduction in nighttime voiding episodes. |

|

Bivalirudin PEGylated (Sponsor: MedinCell) |

Phase 2 in France for extended-release cardiac use. |

EMA-funded innovation project under Horizon Europe. |

|

Desmopressin Sublingual (Sponsor: Cipla) |

Phase 2/3 trials for central diabetes insipidus. |

DCGI fast-track pathway approved. |

|

Bivalirudin + Desmopressin Combo (Sponsor: Alkem Labs) |

Phase 1 trials in India for dual-action hemostatic and anticoagulant therapy in cardiac surgery. |

Preclinical safety data published; human trial under way since 2024. |

|

Bivalirudin Micropump Delivery (Sponsor: Sensile Medical) |

Phase 1 trials for portable cardiac care devices. |

EU MDR Class IIb device-drug combo filing expected in 2026. |

|

Desmopressin Extended-Release (Sponsor: Dr. Reddy’s) |

Phase 3 trials in India. |

Anticipated market launch in 2026. |

|

Bivalirudin Auto-Injector (Sponsor: Terumo Corp) |

Phase 1 Japan trials for emergency use in STEMI. |

PMDA fast-track designation. |

|

Desmopressin + Estrogen (Sponsor: Mitsubishi Tanabe) |

Phase 2 trials for menopausal night-time polyuria. |

Phase 1 safety completed in 2023. |

|

Desmopressin Mini-Tablet (Sponsor: Sanofi) |

Phase 3 trials for pediatric use across EU. |

EMA submission expected early 2026. |

|

Bivalirudin + Alteplase (Sponsor: CSL Behring) |

Phase 1b combo anticoagulant-thrombolytic for stroke. |

Early-stage trials in Germany. |

|

Desmopressin Intranasal Gel (Sponsor: Sun Pharma) |

Phase 2 ongoing in Malaysia for hemophilia A patients. |

NMRR registered trial ID MYNMRR-22-0518. |

|

Bivalirudin Dual Release Patch (Sponsor: Bayer AG) |

Phase 1/2 trials in Germany for post-operative use. |

Joint trial with Charité Hospital Berlin under BfArM. |

|

Desmopressin Auto-Injection (Sponsor: Daewoong Pharma) |

Phase 2 in South Korea for trauma-induced bleeding. |

MFDS-supported fast-track initiative; 60.3% efficacy in early trials. |

Sources: EMA, DCGI, NMRP, PMDA, BFARM, U.S. National Library of Medicine, Horizon Europe

Key Bivalirudin and Desmopressin Market Players:

- The Medicines Company (Novartis)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Ferring Pharmaceuticals

- Pfizer Inc.

- Teva Pharmaceutical Industries

- Sun Pharmaceutical

- Mylan (Viatris Inc.)

- Dr. Reddy’s Laboratories

- Baxter International Inc.

- Fresenius Kabi

- Cipla Ltd.

- Aspen Pharmacare

- Gland Pharma (Fosun Group)

- Hospira (Pfizer subsidiary)

- Sanofi S.A.

- Biocon Biologics

The bivalirudin and desmopressin market is very competitive, with the key players such as Pfizer, Novartis, and Ferring Pharmaceuticals. These firms are leading the market share and utilizing extensive R&D, branded drug portfolios, and established hospital networks. Companies in India, such as Dr. Reddy’s and Sun Pharma, are actively expanding in generics and aiming at Latin America and APAC. Further, strategic initiatives such as CDMO partnerships, biosimilar launches, and hospital tenders are surging the market growth. Companies in Japan, such as Sankyo and Otsuka, are aiming at domestic distribution and specialty formulations. Further, market players are actively investing in innovative delivery systems and long-acting analogs.

Below is the list of some prominent players operating in the global bivalirudin and desmopressin market:

Recent Developments

- In July 2024, Ferring Pharmaceuticals launched a reformulated Minirin Melt to target pediatric nocturnal enuresis and adults with central diabetes insipidus. The launch has captured 9.0% of the desmopressin market in Europe within 4 months of launch.

- In March 2024, Viatris Inc. introduced a generic bivalirudin injectable 250 mg to reduce procurement costs by 18.6% and broaden the hospital formulary access. The launch has contributed to a 10.9% rise in unit sales.

- Report ID: 266

- Published Date: Jul 30, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.