Antibiotics Market Outlook:

Antibiotics Market size was valued at USD 55.4 billion in 2025 and is projected to reach USD 82.9 billion by the end of 2035, rising at a CAGR of 4.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of antibiotics is assessed at USD 57.7 billion.

The global market operates within a complex framework defined by the critical public health needs and significant economic challenges. The core demand driver is the rising burden of infectious diseases. According to the WHO November 2023 data, bacterial infectious is the leading cause of global mortality, and antimicrobial resistance is responsible for nearly 1.27 million global deaths directly attributable to drug-resistant infections. This clinical burden sustains baseline demand across hospital and community settings, particularly for injectable antibiotics used in sepsis, pneumonia, surgical prophylaxis, and intensive care. Moreover, the CDC December 2024 data indicates that the number of hospital visits for infectious disease account for 10.2 million. This data indicates that there is a need for continuous antibiotic supply across public and private healthcare systems.

Reported New Cases of Infectious Diseases

|

Disease |

Number of New Cases |

|

Tuberculosis |

8,916 |

|

Salmonella |

58,371 |

|

Lyme Disease |

34,945 |

|

Meningococcal Disease |

371 |

Source: CDC December 2024

Further, the weekly surveillance of influenza and the season’s disease burden leading to bacterial infections requires antibiotics. On the other hand, the study from the Frontiers September 2024 data highlights that urinary tract infections reported over 150 million cases, driving the usage of antibiotics. Additionally, in the U.S., the Biomedical Advanced Research and Development Authority and the National Institutes of Health collectively allocate hundreds of millions of dollars annually to antibacterial R&D and manufacturing preparedness. Similarly, the European Union and WHO-backed initiatives emphasize procurement guarantees and subscription-style payment models to stabilize supplier revenues while preserving stewardship goals. Overall, the market remains volume-driven, policy-regulated, and institutionally supported, with the long-term sustainability increasingly dependent on public sector funding, hospital purchasing contracts, and national AMR action plans rather than traditional commercial scaling.

Key Antibiotics Market Insights Summary:

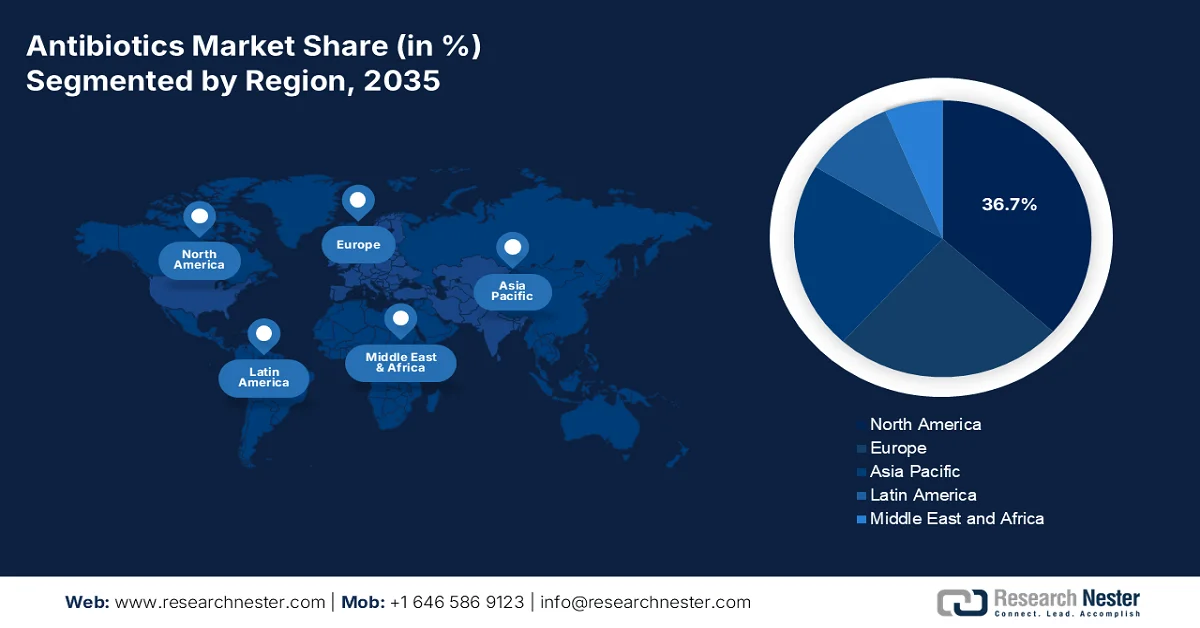

Regional Highlights:

- North America is anticipated to command 36.7% revenue share of the antibiotics market by 2035, attributed to advanced clinical practices, structured reimbursement reforms, and sustained federal support for antimicrobial resistance research and stewardship initiatives.

- Asia Pacific is projected to expand at a CAGR of 5.5% during 2026–2035, fueled by high infectious disease burden, expanding healthcare access, and government-led universal health coverage programs.

Segment Insights:

- In the antibiotics market, the broad spectrum segment is projected to account for 70.3% share by 2035, propelled by its widespread empirical first-line use in severe infections where pathogen identification remains uncertain.

- The oral segment is expected to maintain a leading position over the forecast period 2026–2035, driven by strong outpatient care adoption, IV-to-oral switch protocols, and broad generic availability enhancing affordability and adherence.

Key Growth Trends:

- Government funded hospital care

- Government investment in antibiotic R&D

Major Challenges:

- Prohibitive R&D costs and poor ROI

- Rapid development of antimicrobial resistance

Key Players: Pfizer Inc. (U.S.), GlaxoSmithKline plc (GSK) (UK), Merck & Co., Inc. (U.S.), Novartis AG (Switzerland), Sanofi (France), Roche Holding AG (Switzerland), AstraZeneca plc (UK), Abbott Laboratories (U.S.), Johnson & Johnson (U.S.), Bayer AG (Germany), Eli Lilly and Company (U.S.), Melinta Therapeutics (U.S.), Teva Pharmaceutical Industries Ltd. (Israel), Sun Pharmaceutical Industries Ltd. (India), Lupin Limited (India), Aurobindo Pharma Ltd. (India), Daiichi Sankyo Company, Limited (Japan), Yuhan Corporation (South Korea), CSL Limited (Australia), Pharmaniaga Berhad (Malaysia).

Global Antibiotics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 55.4 billion

- 2026 Market Size: USD 57.7 billion

- Projected Market Size: USD 82.9 billion by 2035

- Growth Forecasts: 4.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (36.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: Brazil, South Korea, Mexico, Indonesia, Saudi Arabia

Last updated on : 12 February, 2026

Antibiotics Market - Growth Drivers and Challenges

Growth Drivers

- Government funded hospital care: Public hospital spending directly influences the market demand, as antibiotics remain foundational in inpatient infection management. According to the KFF February 2025 data, hospital care accounts for over 31% of the total health expenditure across the member countries, with antibiotics embedded within the essential medicines lists. Moreover, Medicare and Medicaid in the U.S. finance a significant share of inpatient antibiotic use. As per the NLM April 2023 study, nearly 30% of hospitalized patients receive at least one antibiotic course. Similar trends are seen in Europe, where the national health system procures antibiotics centrally to ensure the uninterrupted supply for surgical prophylaxis, sepsis, and ICU care. Additionally, the hospital antibiotic use surveillance data indicate that inpatient antibiotic utilization remains highest in ICUs and surgical wards, reinforcing stable, non-discretionary demand tied to government-funded acute care capacity rather than elective prescribing patterns.

- Government investment in antibiotic R&D: Weak commercial returns have shifted the market innovation funding towards governments. In the U.S., the NIH and BADRA collectively have invested hundreds of millions of dollars annually in antibacterial research, clinical trials, and manufacturing preparedness. According to the WHO June 2024 data, fewer than 32 antibiotics are under development to target the BPPL infections, reinforcing the need for public funding. moreover the, Europe and the U.S. are also piloting subscription-style payment models to ensure predictable revenues while limiting overuse. Further, U.S. federal incentives such as the PASTEUR Act and BARDA procurement agreements are designed to de-risk antibiotic commercialization by guaranteeing minimum revenue floors for critical antibiotics, strengthening long-term supply continuity for public health systems.

- Increased surgical volumes in public health systems: Rising surgical volumes, mainly in the publicly funded system, drive the consistent demand for prophylactic market. Various government reports have shown a continuous growth in the elective and emergency surgeries as the population age with procedures such as orthopedic and cardiovascular surgeries heavily reliant on perioperative antibiotics. As per the CDC September 2025 data, nearly 50% of the inpatient antibiotic use is linked to the surgical prophylaxis and postoperative care. On the other hand, the publicly funded hospitals account for the majority of inpatient surgical procedures in aging economies, structurally anchoring antibiotic demand to government-financed operating room capacity rather than discretionary prescribing.

Challenges

- Prohibitive R&D costs and poor ROI: Developing a novel antibiotic can cost billions but offers minimal commercial return due to the pricing and stewardship limits. To overcome this, many companies have focused on public-private partnerships such as the AMR Action Fund to share risk. Though the antibiotics market is expected grow by volume in generic segments, not high-margin novel drugs, underscoring the ROI disconnect.

- Rapid development of antimicrobial resistance: AMR can erode a drug’s efficacy within years of launch, minimizing its commercial lifecycle. Many companies have faced reports of resistance emerging within years of clinical use. This scientific challenge necessitates a continuous R&D pipelines a cycle that is financially unsustainable under the current market conditions.

Antibiotics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.1% |

|

Base Year Market Size (2025) |

USD 55.4 billion |

|

Forecast Year Market Size (2035) |

USD 82.9 billion |

|

Regional Scope |

|

Antibiotics Market Segmentation:

Spectrum of Activity Segment Analysis

The broad spectrum is leading and is poised to hold the share value of 70.3% by 2035 in the market. These agents are designed to target a wide range of bacterial species, making them the empirical first-line choice for severe or rapidly progressing infections where the specific pathogen is unknown. This clinical necessity drives their high market volume despite stewardship guidelines advocating for the narrower-spectrum drugs when possible. The widespread use of broad-spectrum agents is a major contributor to antimicrobial resistance, making their utilization a key focus of public health policy. On 11 June 2024, the Global Antibiotic Research & Development Partnership (GARDP) and Bugworks Research Inc. announced the agreement to co-develop an innovative compound (BWC0977) with broad-spectrum antibiotic activity against multidrug-resistant bacteria that cause life-threatening infections.

Route of Administration Segment Analysis

The oral sub-segment is leading in the antibiotics market. The segment dominance is rooted in outpatient care models where oral antibiotics provide a convenient cost effective and non-invasive treatment option that drives high patient adherence. The segment is further strengthened by the formalization of IV to oral switch protocols in hospitals, which allow for earlier discharge and reduced costs by transitioning patients from intravenous to oral therapy. Further, the broad availability of oral generic antibiotics and fixed-dose combinations has improved the affordability and access across both developed and emerging markets. Moreover, the favorable reimbursement policies and strong physician preference for step-down oral therapy in mild to moderate infections further reinforce sustained demand for this segment.

Distribution Channel Segment Analysis

Hospital pharmacies constitute the leading distribution channel sub-segment by revenue in the market, acting as the vital hub for dispensing the most advanced, potent, and expensive antibiotics. This channel’s dominance is linked to the management of severe complex or multidrug-resistant infections that require intravenous administration, intensive monitoring, and stringent stewardship, all centralized within the hospital setting. According to the CDC, September 2025 data, 50% of the long term care facilities in the U.S. hospitals are prescribed antibiotics. Furthermore, hospital pharmacies play a critical role in antimicrobial stewardship programs, ensuring guideline-driven use of high-end antibiotics to limit resistance and optimize outcomes. On the other hand, the rising incidence of hospital-acquired infections and increased ICU admissions continues to concentrate the antibiotic utilization and revenue generation within hospital pharmacy channels.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Drug Class |

|

|

Spectrum of Activity |

|

|

Route of Administration |

|

|

Application |

|

|

Distribution Channel |

|

|

Drug Origin |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Antibiotics Market - Regional Analysis

North America Market Insights

The North America market is dominating and is poised to hold the regional revenue share of 36.7% by 2035. The market is defined by the advanced clinical practice and stringent economic controls. It is dominated by the U.S., which drives the regional dynamics via a complex interplay of high prices for the novel agents and aggressive cost containment for generics. The primary strategic trend is the shift toward alternative reimbursement models designed to secure a sustainable pipeline for critical new antibiotics. Moreover, the robust antimicrobial stewardship programs enforced by bodies such as the CDC and CMS further shape prescribing behavior by prioritizing targeted, evidence-based antibiotic use. Further, growing federal funding for antimicrobial resistance research and incentive programs for novel drug development continue to support long-term market stability and innovation.

The high outpatient utilization, particularly for oral formulations despite stewardship-driven controls is driving the market in the U.S. According to the CDC, the antibiotic prescribing surveillance using 2024 U.S. Census data, total oral antibiotic prescriptions reached 255.9 million in 2024, translating to approximately 760 prescriptions per 1,000 persons, highlighting sustained baseline demand across the population. Adults aged ≥20 years accounted for 200.0 million prescriptions, while pediatric use remained significant at 55.7 million prescriptions, reinforcing demand across age cohorts. Regionally, the Southern U.S. led utilization with 112.0 million prescriptions and a rate of 844 per 1,000 persons, indicating higher disease burden and prescribing intensity. From a product mix perspective, penicillins dominated with 58.3 million prescriptions, followed by cephalosporins and macrolides, while amoxicillin alone accounted for 55.2 million prescriptions, underscoring its central role in first-line therapy. These data demonstrate that the U.S. market is set to have a positive growth.

Oral Antibiotic Prescribing by Specialty

|

Specialty |

Number of Antibiotic Prescriptions (Millions) |

Antibiotic Prescriptions Per Provider, Rate |

|

Primary Care Physicians |

68.9 |

171 |

|

Physician Assistants & Nurse Practitioners |

103.1 |

176 |

|

Surgical Specialties |

16.3 |

112 |

|

Dentistry |

25.3 |

126 |

|

Emergency Medicine |

14.2 |

201 |

|

Dermatology |

5.1 |

271 |

|

Obstetrics/Gynecology |

4.1 |

74 |

|

Other |

18.9 |

27 |

|

All Healthcare Professionals |

255.9 |

118 |

Source: CDC 2024

The publicly funded healthcare utilization and national antimicrobial stewardship priorities are the primary drivers of the market in Canada. According to the NLM August 2021 study, 3.5 million individuals with a total of 51 ,367, 938 oral antibiotic prescriptions were dispensed nationwide, reflecting consistent community-level demand despite stewardship interventions. Moreover, the NLM research study in March 2022 indicates that approximately 37% to 40% of patients received at least one antibiotic during acute care admissions in recent reporting years, underscoring the role of publicly funded hospitals in sustaining inpatient demand. Overall, the market in Canada is volume-stable and policy-regulated, with demand closely tied to provincial healthcare budgets, centralized hospital procurement, and national AMR action plans rather than private market expansion.

APAC Market Insights

The Asia Pacific antibiotics market is growing rapidly and is expected to grow at a CAGR of 5.5% during the forecast period 2026 to 2035. The market is driven by the high population density, a significant burden of infectious disease, and expanding access to healthcare. Moreover, the growth is diversified with the high-growth markets in India and China. On the other hand, the rising healthcare utilization and high rates of over-the-counter access and self-medication drives the antimicrobial resistance. A key regional driver is government-led universal health coverage expansion, such as India's Ayushman Bharat, which increases formal healthcare access for hundreds of millions. Further, the AMR is directly responsible for rising death rates, underscoring the critical need driving both demand and regulatory response in the region.

Government-backed innovation and domestic drug development aimed at addressing antimicrobial resistance and reducing import dependence are propelling the growth of the market in India. As per the article published by PIB in December 2024, the Government of India announced the successful development and launch of Nafithromycin, the country’s first indigenously discovered macrolide antibiotic, which was developed by Wockhardt with funding support from the Department of Biotechnology (DBT) and BIRAC. The project received ₹8 crore in public funding for Phase III clinical trials and involved a total development investment of approximately ₹500 crore, underscoring strong public–private collaboration. This milestone positions India’s antibiotics market on a higher-value growth trajectory, shifting from high-volume generics toward innovation-led government-supported products while reinforcing long-term demand through public hospital adoption and national AMR initiatives.

Strong government regulation and large public hospital utilization are driving the market in China. According to the NLM February 2022 study, public hospitals accounted for 67.4% of the rise in the inpatient sector in the total medical expenditures and 57.2% of the rise in the outpatient sector, propelling the baseline antibiotic demand in government-funded healthcare settings. At the same time, China has reduced outpatient antibiotic prescribing rates in public hospitals, reflecting tighter controls rather than reduced clinical need. Collectively, these factors indicate that China’s market growth is volume-stable and policy-driven, supported by high hospital throughput and universal insurance coverage, while shifting toward regulated, essential-use–based demand rather than unrestricted prescribing.

Europe Market Insights

The Europe antibiotics market is expanding and is defined by strategic initiatives to stimulate novel antibiotic development and stringent cost containment, coordinated by antimicrobial stewardship. The key demand driver is the high burden of AMR reporting number of high mortality rate from resistant infections, necessitating for a continued demand for effective treatments. The dominant trend is the adoption of the subscription-style payment scheme. Further, aggressive generic competition and stringent pricing by national health technology assessment (HTA) bodies suppress overall market growth, shifting focus towards hospital-based, last-resort therapies and creating a stable environment for market entry and sustainable commercialization.

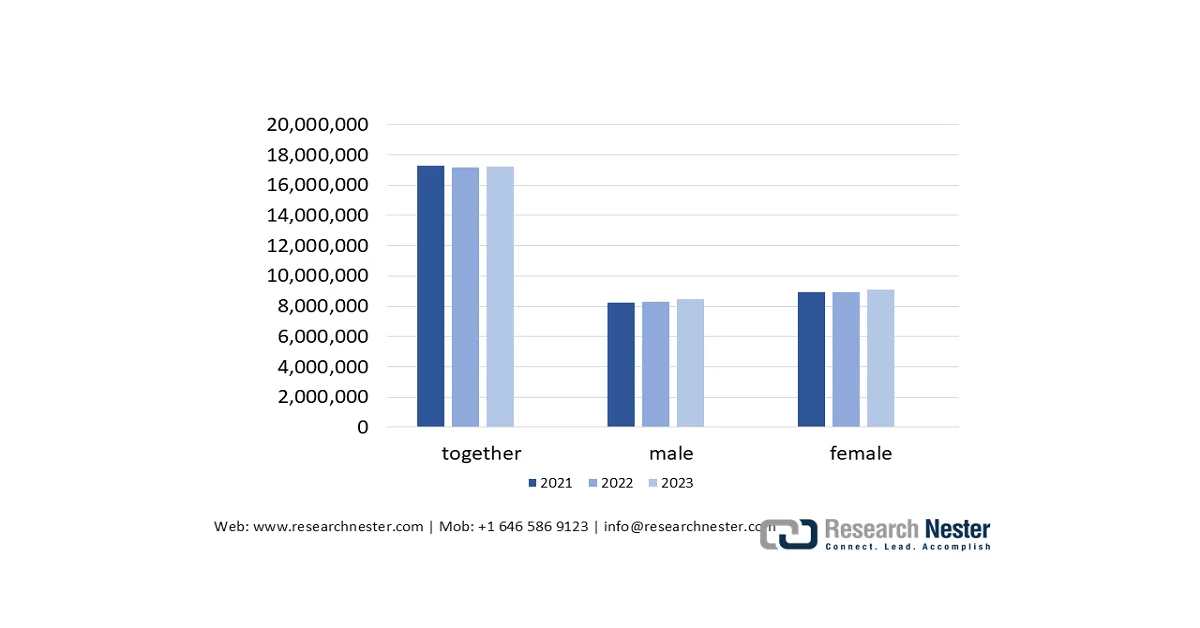

High and stable inpatient care volumes financed via statutory health insurance is driving the antibiotics market in Germany. According to Destatis, November 2024 data, total inpatient discharges increased from 17,157,549 in 2022 to 17,205,585 million in 2023, while treatments excluding foreign or unknown residence rose more sharply to 17,522,946 million cases in 2023, reflecting a 2.3% year-on-year increase. Demand is increasingly driven by older populations, with hospital cases among patients aged 65 years and older rising to 43,867 per 100,000 inhabitants in 2023, up 2.9% year-on-year, a demographic segment with higher antibiotic exposure due to comorbidities and surgical interventions. Short-term inpatient stays (1–3 days) also increased to 8,315,400 cases, supporting continued use of perioperative and empiric antibiotics despite a stable average length of stay of 7.2 days. Collectively, these trends indicate a positive uplift in the market growth.

Number of Patients Discharged from Hospitals

Source: Destatis November 2024

The direct government intervention to address antimicrobial resistance and to stabilize the economics of antibiotic development are actively shaping the market in UK. As per the GARDP article in February 2024, the UK Department of Health and Social Care committed an additional £2.5 million to the Global Antibiotic Research & Development Partnership via the Global AMR Innovation Fund, bringing total UK investment in GARDP programs to £23 million. This funding supports late-stage clinical development and access planning for new and reformulated antibiotics, including treatments for drug-resistant gonorrhoea and neonatal sepsis, conditions that directly impact NHS inpatient care. GARDP’s 2024–2028 strategy, which targets €220 million to advance up to six antibiotic treatments, aligns with the UK’s broader AMR strategy to ensure the future supply of clinically critical antibiotics.

Key Antibiotics Market Players:

- Pfizer Inc. (U.S.)

- GlaxoSmithKline plc (GSK) (UK)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- Roche Holding AG (Switzerland)

- AstraZeneca plc (UK)

- Abbott Laboratories (U.S.)

- Johnson & Johnson (U.S.)

- Bayer AG (Germany)

- Eli Lilly and Company (U.S.)

- Melinta Therapeutics (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Aurobindo Pharma Ltd. (India)

- Daiichi Sankyo Company, Limited (Japan)

- Yuhan Corporation (South Korea)

- CSL Limited (Australia)

- Pharmaniaga Berhad (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Pfizer Inc. is a dominating leader in the market and uses its vast scale and established portfolio. Pfizer focuses on ensuring supply chain resilience for critical antimicrobial and participates in public private partnerships such as the AMR Action Fund to combat antimicrobial resistance via investment in novel antibiotic R&D aiming to bridge the funding gap in this challenging sector.

- GlaxoSmithKline Plc maintains a significant presence in the antibiotics market via its established vaccines and medicines. Its key initiative involves a dual strategy, responsibly managing its legacy antibiotic products while directing R&D investment towards innovative mechanisms such as exploring bacteriophage therapies and new biological agents to address the most urgent threats of antimicrobial resistance.

- Merck & Co., holds a strong position in the antibiotics market with the key anti-infective agents. The company strategically emphasizes pioneering research in areas of high unmet need, including combinational therapies for resistant Gram-negative infections. The company actively engages in global antimicrobial stewardship programs and advocates for novel payment models to ensure sustainable innovation and access to new antibiotics. The company has made a net sale of USD 16.4 billion in Q4 2025.

- Novartis AG has historically been a major player in the antibiotics market. Its strategic initiative has involved a portfolio refinement, divesting certain mature assets to focus R&D resources on other therapeutic areas. Moreover, it continues to play a role via responsible lifecycle management of essential antibiotics and support for antimicrobial resistance initiatives. According to the 2024 annual report, the company has made a net sales of USD 21, 146 millions in the U.S.

- Sanofi is a key player in the antibiotics market, mainly via its broad vaccines portfolio, which includes crucial preventative solutions. Its strategic initiatives focus on ensuring reliable long term access to its established injectable antibiotics, while its R&D pipeline targets novel approaches to fight bacterial infections, often via collaborative ventures with biotech innovators.

Here is a list of key players operating in the global market:

The global antibiotics market is highly competitive and is dominated by the large multinational pharmaceutical companies, along with significant generic manufacturers mainly from India and China. The key strategies include vertical integration of API production, strategic partnerships for R&D in novel antibiotic classes, and portfolio diversification into complex generics to combat thin margins. For example, in December 2024, Delbert Pharma announced the acquisition of Azactam (aztreonam) from Bristol Myers Squibb. Besides the high cost and scientific difficulty of developing new drugs have also been an increase in public-private funding initiatives. Moreover, the pricing pressures, stringent regulations, and antimicrobial resistance challenges are reshaping the landscape, driving consolidation and a focus on specialty and reserve antibiotics.

Corporate Landscape of the Antibiotics Market:

Recent Developments

- In September 2025, Tabuk Pharmaceutical Manufacturing Company, a fully owned subsidiary of Astra Industrial Group and a leading pharmaceutical company in the Middle East and Cumberland Pharmaceuticals Inc., a specialty pharmaceutical company, announced the launch of Cumberland’s Vibativ (telavancin) injection in Saudi Arabia.

- In August 2025, Iterum Therapeutics plc, which is focused on delivering next-generation oral and IV antibiotics to treat infections caused by multidrug-resistant pathogens in both community and hospital settings, today announced the U.S. commercial launch of ORLYNVAH (sulopenem etzadroxil and probenecid) oral tablets.

- In June 2024, Orchid Pharma Limited has announced the launch of its new drug Cefepime-Enmetazobactam, which has been approved for the treatment of complicated Urinary Tract infections (cUTI), Hospital-Acquired Pneumonia (HAP) and Ventilator-Associated Pneumonia (VAP) indications.

- Report ID: 4465

- Published Date: Feb 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.