Airport Information Systems Market Outlook:

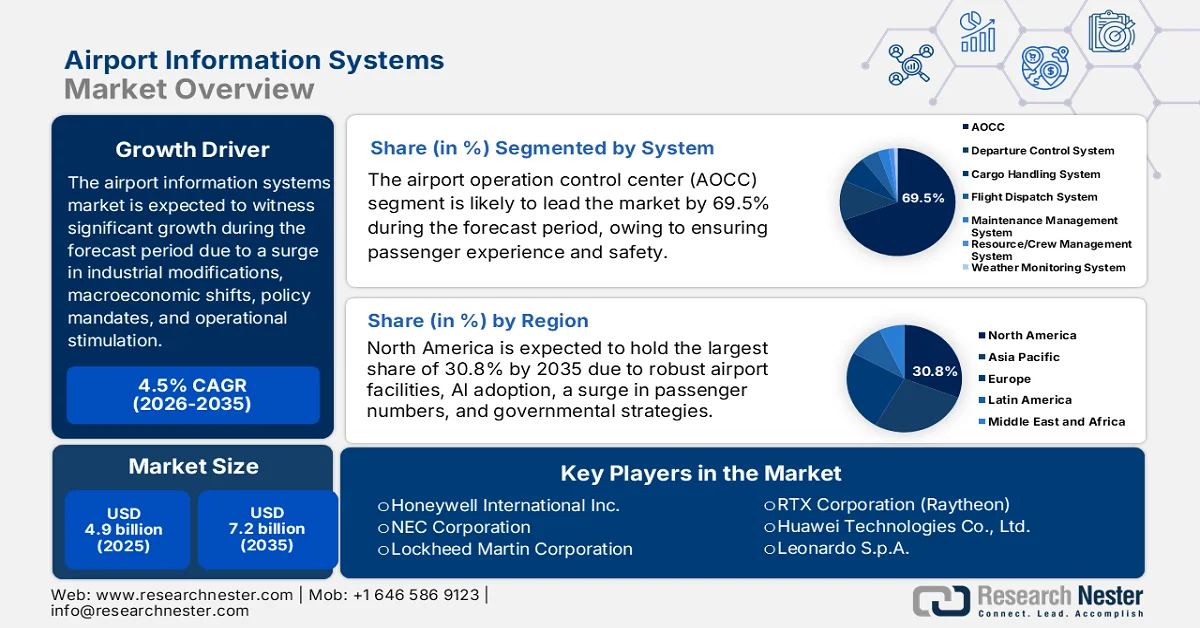

Airport Information Systems Market size was valued at over USD 4.9 billion in 2025 and is expected to reach USD 7.2 billion by the end of 2035, growing at a CAGR of 4.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of airport information systems is estimated at USD 5.1 billion.

The global airport information systems market is gradually evolving under the influence of distinct forces that represent the long-lasting and fundamental catalysts, such as structural industry modifications, policy mandates, and macroeconomic transitions, for creating the sustained demand. According to official statistics published by the IATA Organization in June 2025, the net profit from the aviation industry amounted to USD 6 billion, demonstrating an improvement from USD 32.4 billion as of 2024. Additionally, net profit margin catered to 3.7%, indicating an increase from 3.4% in the same year, as well as 3.6% in 2023. Moreover, the return on invested capital was at 6.7%, which further improved from the 6.6%, while operating profits amounted to USD 66 billion, and overall revenues catering to a record high of USD 979 billion, thus proliferating the market growth.

Furthermore, the digital twin adoption for operational simulation, the presence of touchless biometric corridors, the edge computing deployment, and outcome-based contracting models are a few trends suitable for boosting the airport information systems market globally. As per an article published by the ITF Global Organization in 2025, the lifting of travel restrictions as of 2022 is regarded as a turning point for the overall aviation industry, with an increase in passenger levels that reached 9.4 billion, exceeding 9.2 billion in previous years. Besides, commercial aviation significantly supports nearly 87.7 million employment opportunities worldwide. Moreover, 6 out of 10 airports indicated a shortage in staff across the overall industry, leading to only 50% as of 2023. Likewise, in Europe, 1 in 9 vacancies is projected to remain unfilled, but despite these challenges, with digitalization and advancements, the airport information systems market is continuing to grow across different regions.

Key Airport Information System Market Insights Summary:

Regional Highlights:

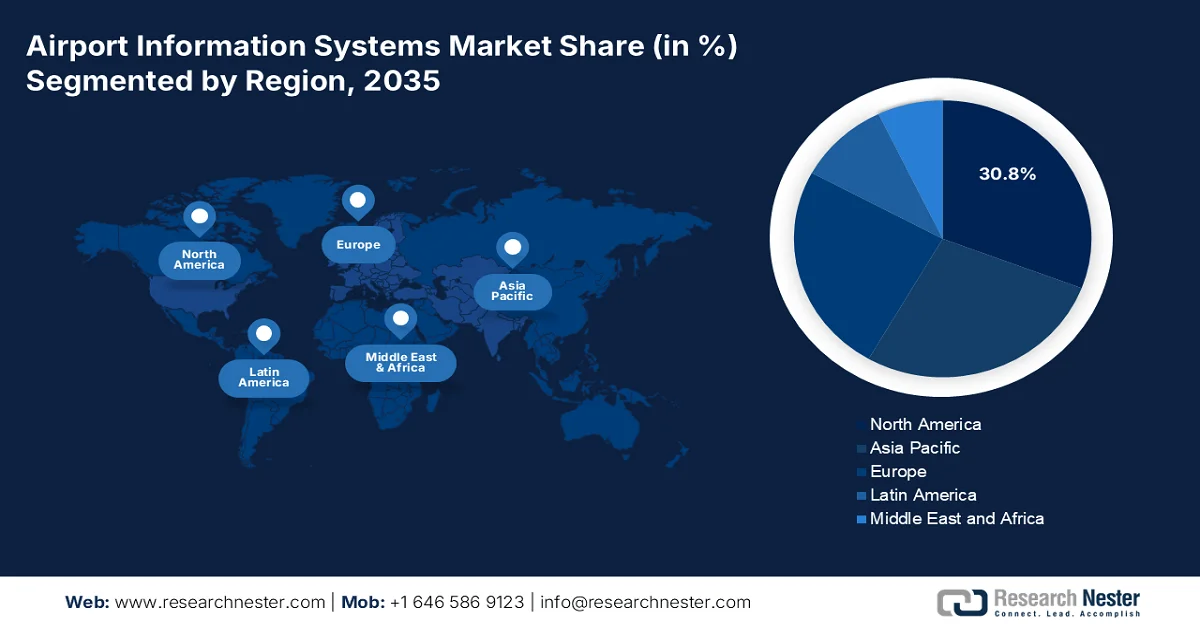

- North America airport information systems market is projected to hold a 30.8% share by 2035, bolstered by strong infrastructure investments and growing adoption of AI-driven airport operations

- Europe is anticipated to witness the fastest growth in the market during 2026–2035, impelled by regulatory-driven upgrades in biometric systems and increasing focus on sustainable airport operations

Segment Insights:

- The airport operation control center (AOCC) sub-segment in the airport information systems market is projected to account for a 69.5% share by 2035, fueled by its role as a centralized operational hub enhancing safety, efficiency, and passenger experience

- The terminal side segment is expected to secure a significant share during 2026–2035, propelled by rising global passenger traffic and increasing demand for seamless, contactless travel experiences

Key Growth Trends:

- Increase in urban air mobility integration

- Surge in climate resilience mandates

Major Challenges:

- High implementation and integration costs

- Legacy infrastructure and system interoperability constraints

Key Players: SITA NV (Belgium), Siemens AG (Germany), Amadeus IT Group, S.A. (Spain), Thales S.A. (France), International Business Machines Corporation (IBM) (U.S.), Northrop Grumman Corporation (U.S.), Honeywell International Inc. (U.S.), NEC Corporation (Japan), Lockheed Martin Corporation (U.S.), L3Harris Technologies, Inc. (U.S.), Indra Sistemas, S.A. (Spain), RTX Corporation (Raytheon) (U.S.), Huawei Technologies Co., Ltd. (China), Leonardo S.p.A. (Italy), Saab AB (Sweden), Inform GmbH (Germany), RESA Airport Data Systems (France/International), Intersystems Group (Australia), Tata Consultancy Services Limited (TCS) (India), ADB SAFEGATE (Belgium), Collins Aerospace (U.S.), Alstom (France), Assaia (Switzerland), SITA (Belgium).

Global Airport Information System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.9 billion

- 2026 Market Size: USD 5.1 billion

- Projected Market Size: USD 7.2 billion by 2035

- Growth Forecasts: 4.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (30.8% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, Brazil, United Arab Emirates, Indonesia, Vietnam

Last updated on : 27 March, 2026

Airport Information Systems Market - Growth Drivers and Challenges

Growth Drivers

- Increase in urban air mobility integration: The emergence of electric vehicle takeoff and landing aircraft, along with urban air mobility corridors, is creating the latest category of vertiport facility that demands purpose-built information systems. According to official statistics published by the PIB Government in January 2026, the fleet of airlines in India has been continuously expanding, with the placement of orders for over 1,500 airplanes. Moreover, there have been 70 airports in the country, and at present, numbers have increased to over 160, which is suitable for the increase in air mobility corridors. Besides, the government has deliberately activated more than 100 air drones in the nation, due to which 15 million passengers can travel in such routes based on the UDAN scheme, thus making it suitable for uplifting the airport information systems market.

- Surge in climate resilience mandates: The presence of coastal airports faces existential threats from sea-level rise, storm surges, and extreme weather incidents, prompting government-based infrastructure hardening programs in the airport information systems market. Besides, national aviation authorities in island nations, the Netherlands, and the U.S. Gulf Coast are demanding airports to implement climate adaptation plans that include redundant IT infrastructure, decentralized operational control centers, and predictive weather integration systems. This driver extends beyond sustainability into business continuity, forcing airports to allocate capital to solutions that enable resilient operations during climate-related disruptions.

- The labor shortage automation imperative: The structural shortage of skilled aviation personnel, such as security screeners, ground handlers, and air traffic controllers, is readily forcing airports to escalate automation not as a suitable measure, but as an operational necessity. As per a data report published by the IATA Organization in June 2023, the worldwide economy for the air transport industry grew by 3% in 2023, denoting a decrease from 3.4% as of 2022 and 6.3% in 2021. Besides, emerging economies have the capacity to reach 3.9% of the gross domestic product (GDP), through 56% of low-income developing nations are usually under debt distress. Therefore, all these challenges resulted in labor shortage, which in turn is suitable for the airport information systems market for increasingly implementing digitalized systems to carry out operational activities.

Challenges

- High implementation and integration costs: The aspect of deploying comprehensive airport information systems requires substantial capital expenditure that extends far beyond the initial software licensing or hardware procurement. Airports must invest heavily in infrastructure upgrades, including the installation of high-speed fiber networks, biometric scanners, digital displays, baggage handling automation, and centralized control centers, often while maintaining continuous 24/7 operations. For many airports, particularly mid-sized regional hubs and those in emerging economies, securing the necessary funding, whether from government budgets, private investors, or public-private partnerships, remains a formidable obstacle in the airport information systems market.

- Legacy infrastructure and system interoperability constraints: A substantial portion of the world's airport infrastructure is built upon legacy systems that were designed decades ago for standalone, siloed operations rather than the integrated, data-sharing environments demanded by modern smart airport concepts. These aging systems, ranging from flight information display systems and baggage handling controls to airfield lighting and ground radar, frequently depend on proprietary protocols, outdated hardware, and specialized maintenance knowledge that is becoming increasingly scarce. The technical debt accumulated over years of incremental upgrades creates significant barriers to implementing unified airport operation control centers (AOCC) that require real-time data fusion across airside, terminal, and landside domains, thus causing a hindrance in the airport information systems market growth.

Airport Information Systems Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.5% |

|

Base Year Market Size (2025) |

USD 4.9 billion |

|

Forecast Year Market Size (2035) |

USD 7.2 billion |

|

Regional Scope |

|

Airport Information Systems Market Segmentation:

System Segment Analysis

The airport operation control center (AOCC) sub-segment, which is part of the system segment, is anticipated to garner the largest share of 69.5% in the airport information systems market by the end of 2035. The sub-segment’s upliftment is highly attributed to its centralized and critical nerve center of an airport facility, which is crucial for enhancing passenger experience, efficiency, and safety. Besides, according to official statistics published by the International Civil Aviation Organization in August 2025, the global flights account for 37 million as of 2024, along with 4.5 billion passengers. Additionally, the accident rate accounts for 95%, with 10% fatal accidents, 296 fatalities, 134 critical injuries, as well as 2.5 accidents per million flight departures, and 65 fatalities per billion passengers. Therefore, to combat these incidents, there is a huge growing demand for the sub-segment globally.

Passengers and Flight Departure Worldwide Traffic Analysis (2019-2024)

|

Year |

Passenger (Billion) |

Flight Departure (Million) |

|

2019 |

4.5 |

38.7 |

|

2020 |

1.8 |

22.4 |

|

2021 |

2.3 |

24.9 |

|

2022 |

3.2 |

31.2 |

|

2023 |

4.1 |

35.2 |

|

2024 |

4.5 |

37 |

Source: International Civil Aviation Organization

Type Segment Analysis

Based on type, the terminal side segment in the airport information systems market is projected to account for the second-highest share during the forecast period. The segment’s growth is highly driven by the immediate priority airports place on enhancing passenger experience and streamlining front-end operations. Additionally, the primary drivers for the segment are the surging global air passenger traffic and the corresponding demand for frictionless, contactless travel. Key technologies include self-service kiosks, biometric boarding systems, automated bag-drop units, and real-time flight information displays, all designed to reduce queue times and improve passenger flow. Regulatory mandates, such as Europe’s Entry/Exit System (EES) and the TSA's biometric screening expansion in the U.S., are further accelerating investment, as airports must upgrade their terminal infrastructure to comply with enhanced security and identity management requirements.

Application Segment Analysis

By the end of the stipulated timeline, the passenger information systems sub-segment, part of the application segment, is expected to hold the third-largest share in the airport information systems market. The sub-segment’s development is highly fueled by its importance for its modernized transit, suitable for offering real-time data on delays, routes, and schedules to enhance the overall passenger experience. In addition, the sub-segment also serves as the primary communication interface between airport operators and travelers throughout their journey. These systems encompass a comprehensive suite of solutions, including Flight Information Display Systems (FIDS), public address systems, wayfinding kiosks, mobile applications, and digital signage networks that deliver real-time updates on flight statuses, gate assignments, boarding calls, baggage claim locations, and emergency notifications.

Our in-depth analysis of the airport information systems market includes the following segments:

|

Segment |

Subsegments |

|

System |

|

|

Type |

|

|

Application |

|

|

Component |

|

|

Deployment Mode |

|

|

Airport Class |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Airport Information Systems Market - Regional Analysis

North America Market Insights

North America in the airport information systems market is anticipated to garner the highest share of 30.8% by the end of 2035. The market’s upliftment in the region is primarily supported by the presence of strong airport infrastructure, an increase in passenger volumes, sustained government modernization strategies, the integration of AI and data analytics in airport operations, along with enabling predictive resource allocation and enhanced passenger flow management. According to official statistics published by the Department of Transportation in October 2024, the Bipartisan Infrastructure Law offers an unprecedented USD 20 billion in airport infrastructure funding that is essential for optimizing passenger experiences, enhancing competitiveness in the airline sector, and modernizing the region’s airports. Additionally, there has been further investment of USD 5 billion to ensure critical infrastructure improvements, thus proliferating the airport information systems market growth.

Bipartisan Infrastructure Law Airport Investments in North America (2024)

|

Components |

Numbers/Amount |

|

Flight Handing |

More than 16,400,000 across over 19,600 U.S.-based airports per year |

|

Passenger Screening |

3 million |

|

Flight Cancellation Rate |

1.2% within over 10 years |

|

Penalty Provision |

USD 225 million by the Biden-Harris Administration |

|

Flight Operations |

More than 45,000 regular flights with 2.9 million passengers |

|

Busy Airport Days |

10 |

|

Refunds and Reimbursement |

USD 4 billion |

|

Number of Airlines Guaranteeing Free Rebooking and Meals |

10 |

Source: Department of Transportation

The airport information systems market in the U.S. is growing significantly, owing to regulatory modernization mandates, a surge in passenger volumes, robust digitalized transformation strategies, the adoption of advanced data-sharing platforms, real-time operational databases, and digitalized towers. As per an article published by the Bureau of Transportation Statistics in November 2025, domestic airlines carried 86.8 million systemwide and scheduled service passengers as of August 2025. Besides, domestic enplanements accounted for 74.5 million, and international enplanements catered to 12.2 million passengers in the same year. Moreover, in terms of seasonal adjustments, systemwide enplanements account for 82 million, along with domestic enplanements catering to 71.1 million and international enplanements with 10.9 million, thus enhancing the market expansion.

The strong government support for infrastructure modernization, an increase in air passenger traffic, the rapid implementation of advanced passenger processing technologies, effectively prioritizing the modernization of airport infrastructure to enhance operational efficiency, security, and safety, are certain factors bolstering the airport information systems market in Canada. As stated in an article published by the Statistique Canada in August 2025, 5.8 million passengers have been recorded passing through pre-board security screening at different checkpoints. These are operated at the country’s 8 largest airports, denoting an upsurge by 3.6% in July 2024, as well as 7.8% increase from the pandemic level. Moreover, in July 2025, 1.6 million passengers were readily screened for global flights, demonstrating a surge by 9.4% year over year (YoY), thus positively impacting the market demand.

Europe Market Insights

Europe in the airport information systems market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the robust regulatory push for significant upgradation to terminal-side passenger processing and biometric systems, focus on sustainable airport operations, generous energy-efficient information systems, and reduced operational expenses. According to official statistics published by the Airports Council International Europe in January 2025, with every 10% increase in air connectivity yielding a 0.5% gain in GDP, along with a 1.6% rise in employment, airports in the region are permitted to expand to meet the future demand, which effectively fuels the comprehensive economic activity. Therefore, this denotes a huge growth opportunity for the airport information systems market in the overall region.

The airport information systems market in Germany is gaining increased traction, owing to strong digitalization strategies, substantial government support for aviation infrastructure modernization, baggage handling infrastructure, and generous funding for airport digitalization projects under the German government's aviation strategy. Based on government estimates published by the ITA in December 2024, the aerospace industry in the country significantly generated a revenue of USD 48.2 billion as of 2023, with the objective of emerging as the most notable location for climate-neutral aviation. Besides, mandatory sustainable aviation fuel has been applied to the country through regional legislation, which requires fuel for flights arriving in the whole of Europe, regardless of the facility to comprise a minimum SAF level of 2%, thus driving the market expansion.

The continuous surge in tourism traffic, the majority of airport infrastructure investments, the presence of leading domestic airport vendors, and generous fund allocation for airport sustainability and digitalization are responsible for enhancing the airport information systems market in Spain. Based on government estimates published by the Ministry of Industry and Tourism in March 2026, the Secretary of State for Tourism declared that 45% of Spain Tourism 2030 Strategy is currently underway, effectively suitable for tourist destinations, residents, workers, companies, and tourists. Besides, to achieve this strategy, the Secretary of State has effectively placed tourism at the service of the country, which includes residents as part of the domestic tourism ecosystem, along with their well-being as one of the central focuses of the Strategy, thus fueling the market development in the country.

APAC Market Insights

The Asia Pacific in the airport information systems market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by unprecedented investments in greenfield airport construction across Southeast Asia, India, and China, along with large-scale modernization of present aviation facilities in Singapore, Japan, and South Korea. According to official statistics published by the ACI Asia Pacific in July 2025, the region significantly serves as the ultimate voice of 127 airport members and operates over 600 airports across 44 countries. In addition, the region also accounts for 5 affiliate airport members, 9 associate members, and 104 business partners. Besides, in 2023, regional airports significantly handled 3.4 billion passengers, along with 51 million tons of cargo, thereby making it suitable for bolstering the market growth.

The airport information systems market in China is gaining increased exposure, owing to airport construction programs, robust centralized government backing for smart aviation infrastructure, approved plans for expanding the commercial network, and the existence of an airport development pipeline. As stated in an article published by the State Council in January 2025, the Civil Aviation Administration of China (CAAC) notified that the industry gained an overall transportation turnover of 148.5 billion ton-km as of 2024, denoting a 25% YoY increase as well as 14.8% higher than previous years. Moreover, passenger traffic in the country reached 730 million, indicating a 17.9% increase from 2023 and 10.6% from previous years. Besides, mail and cargo volume have hit 8.9 million tons, rising by 22.1% YoY and 19.3%, thus proliferating the market’s growth in the overall country.

The aspects of the massive airport infrastructure modernization program, rapidly growing middle-class air travel demand, robust government initiatives under the National Civil Aviation Policy 2026, and the design of digital-first smart airports are certain trends that are responsible for bolstering the airport information systems market in India. Based on government estimates published by the PIB Government in April 2025, aviation is one of the fastest-growing industries, and it is continuously growing, with 4 billion people and rapidly growing middle-class population. Besides, the country’s domestic air passenger traffic successfully reached a historic milestone, exceeding 500,000 passengers within a single day as of 2024. In addition, the UDAN scheme has significantly operationalized 619 routes and 88 airports, with further plans to extend to 120 additional destinations, thereby denoting an optimistic outlook for the market expansion.

Key Airport Information Systems Market Players:

- SITA NV (Belgium)

- Siemens AG (Germany)

- Amadeus IT Group, S.A. (Spain)

- Thales S.A. (France)

- International Business Machines Corporation (IBM) (U.S.)

- Northrop Grumman Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- NEC Corporation (Japan)

- Lockheed Martin Corporation (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Indra Sistemas, S.A. (Spain)

- RTX Corporation (Raytheon) (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Inform GmbH (Germany)

- RESA Airport Data Systems (France/International)

- Intersystems Group (Australia)

- Tata Consultancy Services Limited (TCS) (India)

- ADB SAFEGATE (Belgium)

- Collins Aerospace (U.S.)

- Alstom (France)

- Assaia (Switzerland)

- SITA (Belgium)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SITA NV serves as a cornerstone of the global aviation technology landscape, providing the majority of the world’s airlines and airports with mission-critical passenger processing, baggage tracking, and communication systems. The company focuses on delivering integrated, cloud-native platforms that unify airport operations across airside and terminal environments.

- Siemens AG leverages its deep expertise in industrial automation and digital twins to offer comprehensive baggage handling, building management, and operational control solutions for major international hubs. The company emphasizes energy-efficient and fully integrated infrastructure that aligns with broader smart airport and sustainability initiatives.

- Amadeus IT Group, S.A. specializes in passenger service systems, departure control, and advanced airport operational databases that enable seamless collaboration between airlines and airport operators. The company continues to expand its footprint by integrating biometric identity management and real-time resource optimization tools into its core portfolio.

- Thales S.A. combines its aerospace heritage with cutting-edge digital technologies to deliver high-assurance solutions spanning air traffic management, cybersecurity, biometric passenger flow, and airport command-and-control centers. The company is recognized for its strong focus on secure, interoperable systems that support both regulatory compliance and operational resilience.

- International Business Machines Corporation (IBM) brings enterprise-grade artificial intelligence, hybrid cloud, and predictive analytics to the airport information systems sector, enabling data-driven decision-making across complex operational environments. The company partners with airport authorities to deploy cognitive solutions that optimize turnaround times, maintenance schedules, and passenger experience at scale.

Here is a list of key players operating in the global airport information systems market:

The global airport information systems market is characterized by a blend of established aerospace and defense giants alongside specialized technology providers. Besides, North America and Europe remain the dominant regions due to high digital maturity and modernization budgets. Notable players are focusing on strategic acquisitions such as SITA's purchase of CCM, AI-driven analytics for predictive operations, and forming joint innovation labs with airport authorities to co-develop next-generation passenger processing and biometric solutions. Moreover, in May 2024, Collins Aerospace, which is an RTX business, introduced Collins’ Airport Surface Awareness System to ensure real-time monitoring, recording, and tracking of both ground support and aircraft equipment at airports, thereby making it suitable for bolstering the airport information systems industry worldwide.

Corporate Landscape of the Airport Information Systems Market:

Recent Developments

- In March 2026, Alstom effectively secured a USD 437 million contract for upgrading and refurbishing the Skyway automated people mover system at Houston Intercontinental Airport and expanding maintenance and operational services for the upcoming 15 years.

- In December 2025, Assaia successfully raised USD 26.6 million in an oversubscribed Series B funding round, which was led by Europe-based investment company, Armira Growth, along with existing investors.

- In April 2024, SITA unveiled its trailblazing airport management tool, which is known as the SITA Airport Operations Total Optimizer, particularly during the Passenger Terminal Expo 2024 in Germany.

- Report ID: 506

- Published Date: Mar 27, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Airport Information System Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.