Cardiovascular Devices Market Outlook:

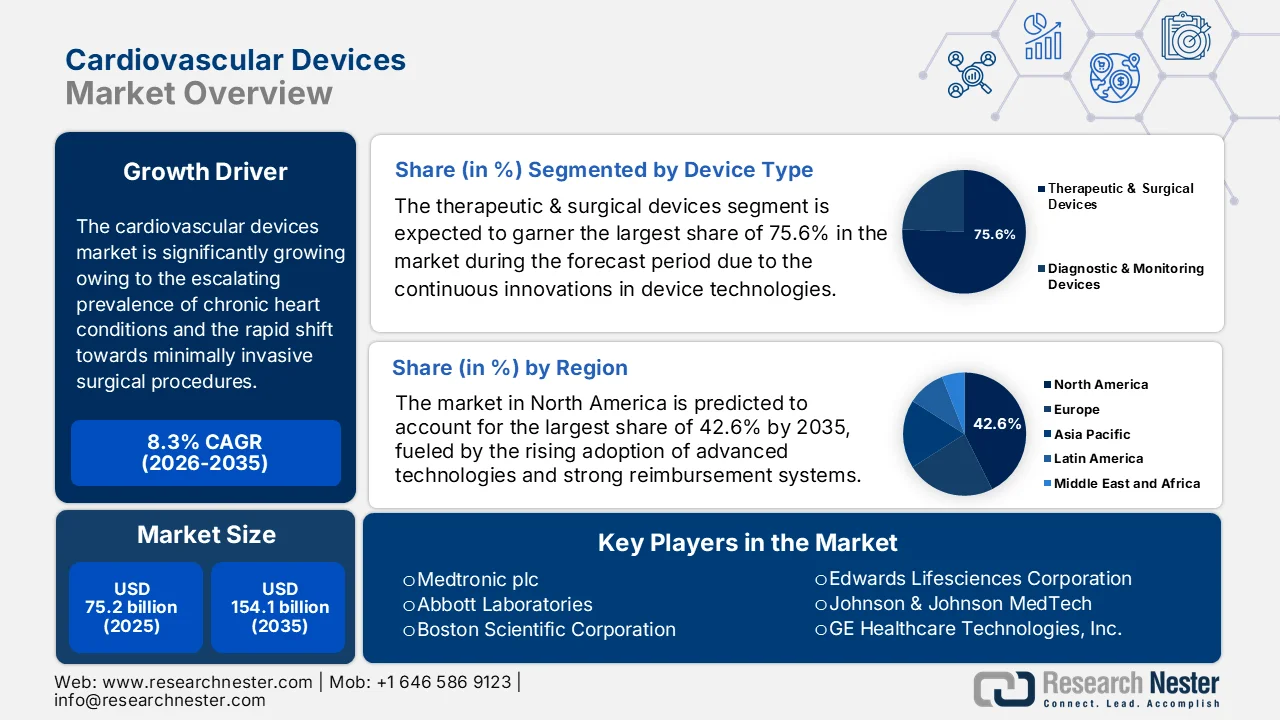

Cardiovascular Devices Market size was valued at USD 75.2 billion in 2025 and is expected to surpass a total of USD 154.1 billion by the end of 2035, registering a CAGR of 8.3% during the forecast period, i.e., from 2026 to 2035. In 2026, the industry size of cardiovascular devices is evaluated at USD 81.4 billion.

The global cardiovascular devices market is poised for tremendous growth owing to the escalating prevalence of chronic heart conditions and the rapid shift towards minimally invasive, rather than open-heart, surgical procedures. According to the official statistics published by the National Institute of Health (NIH) in August 2025, between 2025 and 2050, cardiovascular prevalence is projected to rise by 90%, crude mortality by 73.4%, and crude DALYs by 54.7%, wherein deaths are projected to increase from 20.5 million in 2025 to 35.6 million in 2050. It also mentioned that age‑standardized prevalence will remain relatively constant, which is -3.6%, whereas age‑standardized mortality and DALYs are expected to decline by 30.5% and 29.6%, respectively. Ischaemic heart disease will continue to dominate, causing 20 million deaths, and high systolic blood pressure will drive 18.9 million deaths globally, all of which will drive demand for advanced cardiovascular devices.

Furthermore, the proliferation of ambulatory surgical centers and emerging technologies in structural heart repair are also driving demand, transforming trade dynamics in the cardiovascular devices market. According to the reports published by the Observatory of Economic Complexity (OEC), the global trade in terms of pacemakers for stimulating heart muscles reached a total of USD 7.4 billion in 2024, growing 7.7% from 2023, with a five-year CAGR of 6.1%. It stated that Switzerland, Ireland, and the Netherlands led exports, whereas the U.S., Netherlands, and Belgium were the largest importers. In addition, the U.S. ran a significant trade deficit of USD 1.4 billion, highlighting reliance on imported devices. Product complexity ranks moderately at 1.2, indicating specialized manufacturing and assembly requirements, hence denoting a huge opportunity for the cardiovascular devices market to grow in the years ahead.

Global Trade Statistics of Pacemakers for Stimulating Heart Muscles (USD Billion) - 2024 Exporters, Importers, Surpluses & Deficits

|

Metric |

Value (2024) |

Notes |

|

Global Trade Value |

USD 7.4 billion |

Total trade of pacemakers |

|

World Trade Rank |

511 / 5380 |

0.033% of total world trade |

|

Product Complexity Index |

1.2 |

Rank 276 / 3119 |

|

Export Growth |

7.7% |

YoY increase from USD 6.9 billion in 2023 |

|

Top Exporters |

Switzerland USD 1.7 billion, Ireland USD 1.5 billion, Netherlands USD 0.7 billion |

Leading suppliers |

|

Top Importers |

U.S.- USD 1.8 billion, Netherlands USD 1.05 billion, Belgium USD 0.55 billion |

Largest consumers |

|

Countries with Trade Surplus |

Switzerland USD 1.7 billion, Ireland USD 1.2 billion, Malaysia USD 0.7 billion |

Exports > imports |

|

Countries with Trade Deficit |

U.S. -USD 1.47 billion, China -USD 0.53 billion, Japan -USD 0.33 billion |

Imports > exports |

|

Export Share in Country Portfolio |

Anguilla 1.09%, Ireland 0.62%, Switzerland 0.44% |

Pacemakers as % of total exports |

|

Five-Year CAGR |

6.13% |

Annualized growth over 2019–2024 |

Source: OEC

Key Cardiovascular Devices Market Insights Summary:

Regional Highlights:

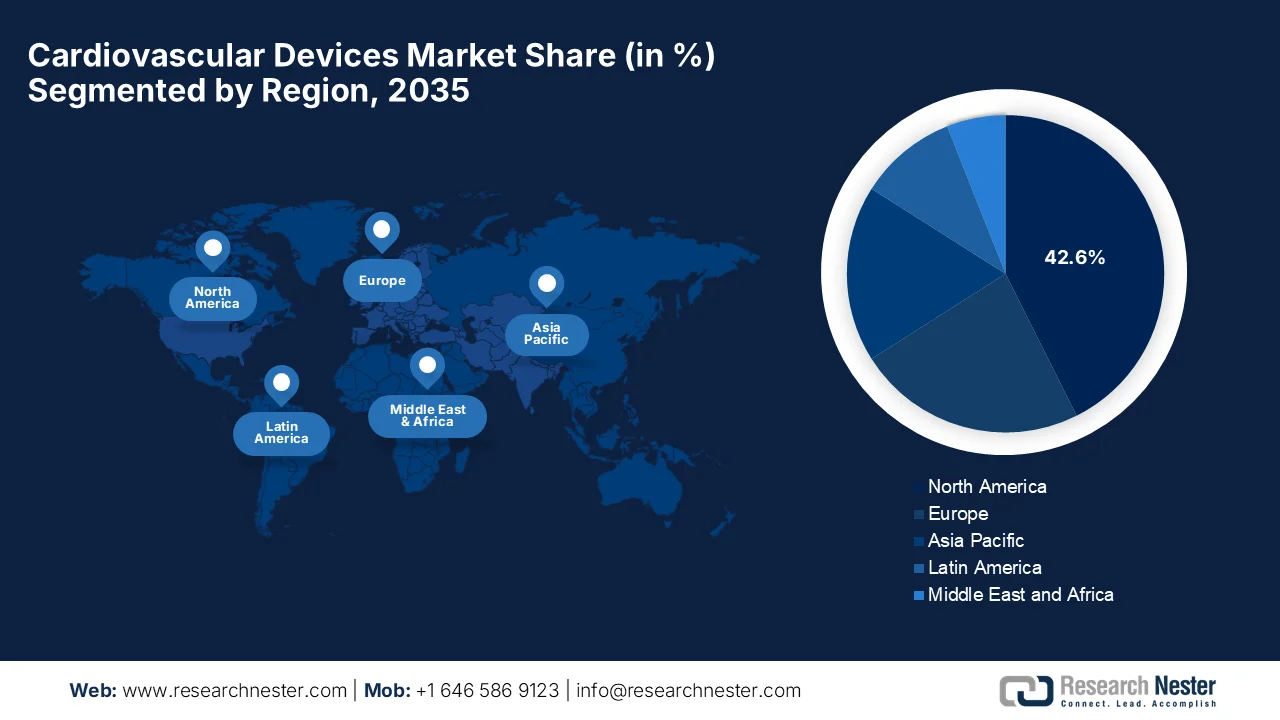

- North America cardiovascular devices market is projected to account for 42.6% share during the forecast period, driven by high adoption of advanced technologies, strong reimbursement systems, and rising prevalence of cardiovascular diseases

- Asia Pacific market is expected to expand at the fastest pace over 2026–2035, fueled by increasing government investments in healthcare infrastructure and a rapidly ageing population

Segment Insights:

- The therapeutic & surgical devices segment in the cardiovascular devices market is anticipated to dominate with a 75.6% share during the forecast period, propelled by rising global burden of cardiovascular diseases and increasing adoption of minimally invasive procedures

- The coronary artery disease segment is expected to witness considerable revenue share by 2035, impelled by growing prevalence of lifestyle-related risk factors and increasing emphasis on early diagnosis and screening

Key Growth Trends:

- Technological advancements and innovation

- Growth in minimally invasive procedures

Major Challenges:

- High cost of devices and procedures

- Stringent regulatory requirements

Key Players: Medtronic plc (Ireland), Abbott Laboratories (U.S.), Boston Scientific Corporation (U.S.), Edwards Lifesciences Corporation (U.S.), Johnson & Johnson MedTech (U.S.), GE Healthcare Technologies, Inc. (U.S.), Baxter International Inc. (U.S.), W. L. Gore & Associates, Inc. (U.S.), Terumo Corporation (Japan), Nihon Kohden Corporation (Japan), Japan Lifeline Co., Ltd. (Japan), Siemens Healthineers AG (Germany), Koninklijke Philips N.V. (Netherlands), B. Braun SE (Germany), BIOTRONIK SE & Co. KG (Germany), Getinge AB (Sweden), Impulse Dynamics (U.S.).

Global Cardiovascular Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 75.2 billion

- 2026 Market Size: USD 81.4 billion

- Projected Market Size: USD 154.1 billion by 2035

- Growth Forecasts: 8.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, France

- Emerging Countries: India, South Korea, Brazil, Mexico, Saudi Arabia

Last updated on : 13 April, 2026

Cardiovascular Devices Market - Growth Drivers and Challenges

Growth Drivers

- Technological advancements and innovation: The ongoing innovations in terms of device technologies, which include bioresorbable stents, remote monitoring systems, AI‑integrated diagnostics, and advanced imaging, readily expand clinical use cases. These innovations drive the cardiovascular devices market by reducing surgery times and enabling earlier detection of heart conditions. In March 2026, MicroPort NeuroScientific announced that its APOLLO Dream sirolimus target-eluting stent system had received Food & Drug Administration (FDA) breakthrough device designation, marking a major step forward in intracranial atherosclerotic disease treatment. It is especially designed to restore cerebral blood flow, and the stent uses a proprietary microgroove drug‑delivery system with sirolimus and bioabsorbable polymer placed on the vessel‑facing surface, hence suitable for bolstering the overall cardiovascular devices market’s growth.

- Growth in minimally invasive procedures: The cardiovascular devices market is facing an incremental demand for minimally invasive processes such as transcatheter valve replacements, catheter‑based diagnostics, which tend to reduce recovery times. In this context, NIH in April 2024 revealed that a study of 305 patients having varicose veins at Zhejiang Rongjun Hospital examined perceptions as well as preferences regarding minimally invasive therapies (MIT) by comparing them with traditional surgery. Besides, it mentioned that among patients who expressed a treatment preference, 76% preferred MIT, especially in terms of male patients, highlighting a growing inclination toward less invasive procedures due to faster recovery and better aesthetic outcomes. At the same time, the main influencing choices are vascular surgeon recommendations and the number of follow-up visits, which underscores the importance of provider-patient communication and education.

- Expansion of healthcare infrastructure: Improvements in terms of healthcare infrastructure, particularly in emerging economies, increase access to cardiovascular diagnostics as well as treatment services. In April 2026, Mount Sinai announced the launch of the Adams Valve Institute, which is a global center for advancing care and surgical innovation for valvular heart disease. It also stated that this particular institute will unite experts in imaging, surgery, and research to improve outcomes and expand access. At the same time, it will focus on complex procedures such as the Ross operation, establish Centers of Excellence for rare and underserved conditions, and drive policy reform to reduce barriers to care. Therefore, such instances denote that targeted expansion of specialized healthcare infrastructure is a key cardiovascular devices market growth driver, as it enhances access to advanced cardiovascular procedures and strengthens clinical capabilities.

Challenges

- High cost of devices and procedures: One of the major obstacles causing hinderance to cardiovascular devices market is the huge cost of advanced devices as well as related procedures. Technologies such as implantable cardioverter defibrillators, transcatheter valves, and ventricular assist devices require considerable investments in terms of manufacturing, R&D, and clinical validation, which drives up prices. Therefore, this factor limits accessibility, particularly in low- and middle-income countries where healthcare budgets and reimbursement frameworks are limited in scale. Even in the case of developed markets, huge out-of-pocket expenses can create hesitation among patients from opting for advanced treatments. In addition, hospitals also face financial pressures, creating a barrier for widespread market adoption.

- Stringent regulatory requirements: The cardiovascular devices market needs to go through a rigorous approval process for the product debut and commercialization. Regulatory bodies across different nations and regions require huge clinical trials, safety data, and a long time for approvals. These rigorous processes increase development expenses and ultimately cause a delay in time-to-market for these devices. At the same time, smaller companies especially find it difficult to meet these requirements due to limited resources. In addition, the aspect of evolving regulatory standards, including post-market surveillance and compliance requirements, adds to intense complexity. These regulations can slow innovation and limit the availability of new technologies, thereby negatively impacting the market’s expansion as well as exposure.

Cardiovascular Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.3% |

|

Base Year Market Size (2025) |

USD 75.2 billion |

|

Forecast Year Market Size (2035) |

USD 154.1 billion |

|

Regional Scope |

|

Cardiovascular Devices Market Segmentation:

Device Type Segment Analysis

The therapeutic & surgical devices segment is expected to garner the largest share of 75.6% in the cardiovascular devices market during the forecast period. The segment’s dominance is largely propelled by the rising global burden of cardiovascular diseases and increasing adoption of minimally invasive procedures. In April 2024, Abbott received U.S. FDA approval for TriClip, which is the first transcatheter device especially designed to repair tricuspid regurgitation by offering a safe, minimally invasive option for patients unable to undergo open-heart surgery. At the same time, results from the TRILUMINATE Pivotal trial showed 90% of patients experienced significant improvement in valve function and quality of life. Hence, this approval underscores the growing innovations in advanced therapeutic and surgical cardiovascular devices, driving the segment’s dominance.

Application Segment Analysis

In the application category, coronary artery disease is predicted to grow with a considerable revenue share in the cardiovascular devices market by the end of 2035. The segment’s growth is effectively propelled by lifestyle-related risk factors such as obesity and diabetes. At the same time, increasing screening and early diagnosis deliberately boosts device utilization across healthcare systems. Centers for Disease Control and Prevention (CDC) in October 2024 revealed that in the U.S., CAD is the most common type of heart disease, affecting about 5% of adults age 20 and older and causing 371,506 deaths in 2022. Also, cardiovascular disease is the leading cause of death across most racial and ethnic groups, with one person dying every 34 seconds, and 805,000 residents in the U.S. experiencing a heart attack annually. The significant prevalence, mortality, and risk factor burden continue to fuel early diagnosis, screening, and adoption of cardiovascular devices.

Product Category Segment Analysis

The interventional cardiology device, which is under the product category, is anticipated to capture a significant revenue share in the cardiovascular devices market during the stipulated timeframe. These interventional devices lead within product categories due to their prominent role in minimally invasive treatments such as angioplasty. In March 2024, Boston Scientific received the U.S. FDA approval for the AGENT Drug‑Coated Balloon, which is the first coronary drug‑coated balloon in the U.S. to treat in‑stent restenosis. ISR accounts for about 10% of percutaneous coronary interventions, and the AGENT DCB offers a safer alternative to repeat stenting or radiation. In the pivotal AGENT IDE trial of 600 patients across 40 sites, the device showed superior outcomes. Therefore, with consistent efforts from the leading pioneers and regulatory support, the segment is expected to witness immense growth in the years ahead.

Our in-depth analysis of the cardiovascular devices market includes the following segments:

|

Segment |

Subsegments |

|

Device Type |

|

|

Application |

|

|

Product Category |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cardiovascular Devices Market - Regional Analysis

North America Market Insights

The North America cardiovascular devices market is anticipated to garner the largest share of 42.6% during the forecast period. The region’s dominance is largely attributable to high adoption of advanced technologies, strong reimbursement systems, and rising prevalence of cardiovascular diseases. At the same time, rising healthcare expenditure and improved access to medical facilities have also fueled market growth. In June 2024, the article published by the American Heart Association stated that there will be a substantial rise in the economic burden of cardiovascular disease and stroke in the U.S. through 2050. It mentions that costs for cardiovascular conditions will reach USD 1.49 trillion by the end of 2050. At the same time, productivity losses are projected to rise 54% to USD 361 billion, with stroke accounting for the largest absolute increase, thus denoting a huge opportunity for cardiovascular devices.

A well-established healthcare system, coupled with ongoing advancements in medical infrastructure, supports the cardiovascular devices market expansion in the U.S. In addition to a strong research and development activity, the growing medical device manufacturing sector and government initiatives promoting device adoption collectively drive the country’s market growth. Centers for Medicare & Medicaid Services in November 2024 stated that the CY 2025 Medicare Physician Fee Schedule final rule sets the conversion factor at USD 32.35, which is an 83% decrease from USD 33.29 in 2024, and establishes new coding and reimbursement for atherosclerotic cardiovascular disease risk assessment and management. These services use standardized tools to estimate 10-year cardiovascular risk and guide interventions. Therefore, this policy reflects CMS’s effort to link Medicare payments with cardiovascular care quality, with the main goal of reducing heart attacks and strokes among beneficiaries.

Supported by an aging population and rising demand for cardiovascular treatments, the cardiovascular devices market in Canada is witnessing significant expansion. The strong government backing, along with a favorable healthcare system, contributes to the adoption of these devices and overall cardiovascular devices market expansion. In May 2022, the government of Canada generously invested a total of USD 5 million over five years to establish the Canada Heart Function Alliance, which is a pan‑Canada research network focused on heart failure. This particular alliance unites 100 researchers nationwide to improve prevention, diagnosis, treatment, and care for the people living with heart failure, with 90,000 to 100,000 new cases annually. Furthermore, it is supported by CIHR, Heart & Stroke, Mitacs, & NIH‑NHLBI, and the network aims to transform cardiac care and improve the market’s potential across the country.

APAC Market Insights

The Asia Pacific cardiovascular devices market is predicted to grow at the fastest rate from 2026 to 2035. The region’s prominence in this field is mainly propelled by government investments in advanced healthcare infrastructure. With a diverse and expanding population of chronic patients, digital health apps are strengthening the market for telemedicine as well as monitoring devices. In November 2024, the article published by the Organization for Economic Co-operation and Development stated that in this region, the population ageing is accelerating rapidly, with life expectancy rising by about 2 to 3 years over the last three decades. The share of people aged above 65 in lower‑middle and low‑income countries will double from 6% in 2023 to 13% in 2050, whereas it is expected to reach 31% in high‑income and 21% in upper‑middle‑income countries. Nations such as Japan, Korea, and Hong Kong will see over 35% of their populations aged 65+ by 2050, and the above-80 age group will triple, reaching 12% in high‑income countries.

Strong government backing for healthcare development, along with improved access to medical services, encourages the adoption of the cardiovascular devices market in China. The advancements in medical technology and an emphasis on local manufacturing of medical devices also bolster the overall cardiovascular devices market expansion. Based on the government data, the Healthy China Initiative (2023-2030) sets a nationwide strategy to prevent and control cardiovascular and cerebrovascular diseases with a main goal to reduce mortality to below 190.7 per 100,000 by 2030. Besides, it deliberately emphasizes early screening, risk factor management, and integration of traditional China and Western medicine at all healthcare levels. The plan strengthens community-based prevention, emergency response training, and Internet + healthcare services to improve access, quality, and standardized care across China, thus making it suitable for standard market growth.

Rising rates of obesity, high cholesterol, and diabetes contribute to the growth of the cardiovascular devices market in India. At the same time, strong government initiatives such as Ayushman Bharat and Make in India are actively promoting domestic production and innovation in cardiovascular devices. In January 2026, the Press Information Bureau (PIB) reported that the Government of India, through the Technology Development Board (DST), entered into a partnership with Drstore Healthcare Service India Pvt. Ltd. under the collaborative R&D Programme to develop a next‑generation continuous health monitoring device. This particular project integrates glucose monitoring with cardiovascular biomarkers such as BNP, Troponin‑I, and hs‑CRP for early detection of heart conditions alongside diabetes management. It is supported by collaboration with Canada’s Nanospeed Diagnostics Inc., and the initiative aims to enable real‑time, remote monitoring and preventive care for high‑risk patients.

Europe Market Insights

Europe cardiovascular devices market is forecasted for significant growth over the next decade. The supportive regulatory environment that facilitates the adoption of advanced cardiovascular devices is the main factor behind the regional market expansion. Moreover, a growing focus on preventive care and early diagnosis contributes to market upliftment. In April 2026, the Joint Research Center revealed that cardiovascular disease causes 1.7 million deaths annually in Europe and affects 62 million people, projected to exceed 100 million by 2050 due to an ageing population. It also mentioned that artificial intelligence is increasingly used in the regional hospitals for early detection and treatment, including coronary artery calcium scoring and CT-derived fractional flow reserve analysis. In addition, under the EU Safe Heart Plan, a USD 22 million initiative supports AI and data-driven cardiovascular tools with a main goal to improve clinical integration and equitable access across Member States.

In Germany, the cardiovascular devices market is poised for extensive growth owing to the continued technological innovation, specifically the integration of artificial intelligence in diagnostics. Meanwhile, the adoption of minimally invasive surgical systems and a nationwide push for remote patient telemonitoring are also prompting a profitable business environment for pioneers in this field. In November 2025, Fraunhofer IZM, in collaboration with Charité University Hospital and the Technical University of Berlin, developed a smart sensor vest that continuously monitors over 110 cardiovascular parameters by using AI to support diagnostics and risk assessment. The vest incorporates non-invasive methods such as ECG, bioimpedance, and seismocardiography, with data processed locally through mobile edge computing and transmitted wirelessly, thus positively impacting the market’s growth and exposure.

A primary emphasis on digital integration and minimally invasive therapies is responsible for driving the overall cardiovascular devices market in the UK. Technological adoption is concentrating on advanced systems such as pulsed-field ablation and transcatheter aortic valve implantation, which prioritize laboratory efficiency and reduced hospital stays. In addition, the procurement mandates are supporting environmental sustainability, which is leading to the rise of recycling initiatives for single-use catheters and devices. In May 2025, the article published by the National Health Service stated that it had rolled out AI-driven 3D heart scans, called HeartFlow Analysis, across 56 hospitals to accelerate the diagnosis and treatment of coronary heart disease. Since 2021, over 24,300 patients have benefited, saving the NHS almost USD 11.7 million and improving access to timely cardiac care, thus suitable for bolstering the cardiovascular devices market’s growth in the overall country.

Key Cardiovascular Devices Market Players:

- Medtronic plc (Ireland)

- Abbott Laboratories (U.S.)

- Boston Scientific Corporation (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- Johnson & Johnson MedTech (U.S.)

- GE Healthcare Technologies, Inc. (U.S.)

- Baxter International Inc. (U.S.)

- W. L. Gore & Associates, Inc. (U.S.)

- Terumo Corporation (Japan)

- Nihon Kohden Corporation (Japan)

- Japan Lifeline Co., Ltd. (Japan)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- B. Braun SE (Germany)

- BIOTRONIK SE & Co. KG (Germany)

- Getinge AB (Sweden)

- Impulse Dynamics (U.S.)

- CathWorks (Israel)

- LivaNova PLC (UK)

- Sahajanand Medical Technologies Limited (India)

- BPL Medical Technologies (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Medtronic plc maintains a dominant position that has a broader portfolio of products spanning cardiac rhythm management, structural heart, and coronary interventions. The company is highly concentrated on continuous innovation, including AI-enabled diagnostics and minimally invasive therapies.

- Abbott Laboratories is another key player that is well recognized for its leadership in interventional cardiology and structural heart devices, especially in terms of transcatheter valve therapies. The firm is mainly focused on advancing next-generation technologies and expanding indications for its existing products.

- Boston Scientific Corporation has established a strong presence through its diversified cardiovascular portfolio, which includes electrophysiology, coronary therapies, and peripheral interventions. The company has its main priority towards innovation in less invasive procedures and digital health integration.

- Edwards Lifesciences Corporation is a global leader in structural heart therapies, particularly in terms of transcatheter aortic valve replacement. Besides, the firm’s strategy centers on technological differentiation, strong physician engagement, and expanding access to advanced heart valve therapies across the globe.

- Terumo Corporation is a central player in this field, especially in interventional systems and vascular access solutions. The company benefits from a strong presence in Asia, along with growing penetration in Western markets.

Below is the list of some prominent players operating in the global cardiovascular devices market:

The cardiovascular devices market is being intensely dominated by multinational players, which have extensive product portfolios and strong R&D capabilities. Leading companies in this field are highly focused on innovation in minimally invasive technologies, such as transcatheter valves and pulsed-field ablation, with the main goal to improve patient outcomes. Mergers and acquisitions to expand product portfolios and geographic reach are certain expansion strategies adopted by companies in this sector. At the same time, firms are also proactively making investments in digital health, AI integration, and remote monitoring solutions. Partnerships with hospitals and expansion in emerging markets effectively strengthen market presence. In February 2026, Medtronic plc announced its intent to acquire CathWorks for up to USD 585 million to strengthen its cardiovascular portfolio through AI-based innovation. This particular deal builds on their 2022 partnership and focuses on expanding the adoption of the FFRangioSystem, which enables non-invasive, angiography-based coronary assessment.

Corporate Landscape of the Cardiovascular Devices Market:

Recent Developments

- In March 2026, BIOTRONIK announced the launch of its pivotal BIO‑LivIQ study to evaluate the LivIQ leadless pacemaker, which is a next‑generation device designed to deliver AV‑synchrony using advanced far‑field sensing. The trial will enroll 325 patients across 60 sites worldwide, assessing safety, pacing performance, and synchrony.

- In December 2025, Impulse Dynamics raised more than USD 158 million in funding to accelerate commercialization, clinical trials, and development of its heart failure technologies, including CCM therapy. The investment will significantly improve access to CCM therapy for patients and validate its clinical effectiveness.

- In December 2025, Philips announced the acquisition of SpectraWAVE Inc., bringing next‑generation AI‑powered coronary intravascular imaging and physiology assessment into its portfolio.

- In January 2025, CMS issued a National Coverage Determination approving implantable pulmonary artery pressure sensors for heart failure management under coverage with evidence development. This decision allows Medicare beneficiaries, including those previously denied under Medicare Advantage, to access the CardioMEMS HF System.

- Report ID: 3272

- Published Date: Apr 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.