Neonatal and Prenatal Devices Market Outlook:

Neonatal and Prenatal Devices Market size was valued at USD 8.8 billion in 2025 and is expected to reach USD 17.1 billion by the end of 2035, registering around 6.9% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of neonatal and prenatal devices is assessed at USD 9.4 billion.

The rising global incidence of preterm births, expanding maternal age, and increasing awareness surrounding early fetal and newborn screening are responsible factors for uplifting the neonatal and prenatal devices market. In addition, technological advancements are reshaping the landscape, wherein the manufacturers are prioritizing the integration of artificial intelligence, wireless remote monitoring, and portable, point-of-care diagnostic tools. According to an article published by the World Health Organization (WHO) in May 2023, around 13.4 million babies were born preterm in a year, which accounted for more than 1 in 10 births worldwide. Preterm birth complications caused about 900,000 deaths among children under 5, thereby making it the leading cause of mortality in this age group. Rates of preterm birth varied globally, ranging from 4% to16% of babies born, with survival inequalities stark between low- and high-income countries, thus elevating the growth potential of the market.

Historic Regional Preterm Birth Rates in 2020: Global Epidemiological Comparison

|

Region |

Preterm Birth Rate (%) |

|

Southern Asia |

13.2% |

|

Sub-Saharan Africa |

10.1% |

|

Eastern Asia |

<8% |

|

South-Eastern Asia |

<8% |

|

Northern America |

<8% |

|

Europe |

<8% |

|

Australia & New Zealand |

<8% |

Source: NIH

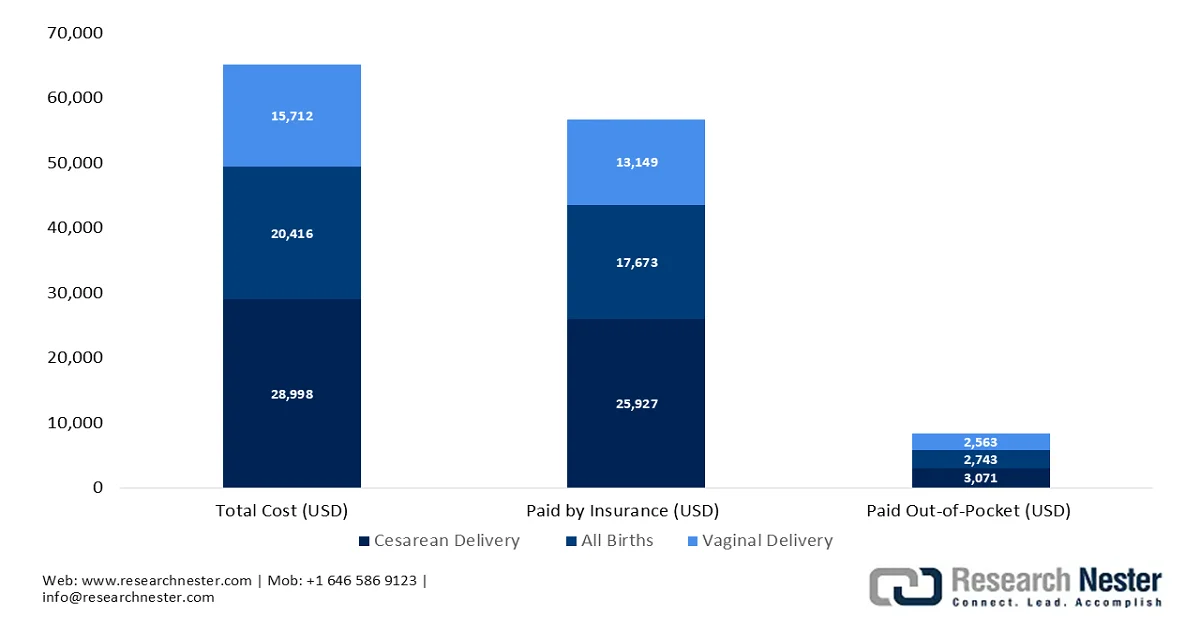

Furthermore, the coverage for neonatal as well as prenatal care by insurance providers readily increases access to healthcare services, which in turn drives greater utilization of prenatal and postnatal monitoring devices. Also, improved reimbursement support enables healthcare facilities to make investments in this equipment, thereby driving technology adoption. In September 2025, the article published by Health System Tracker revealed that pregnancy, childbirth, and postpartum care cost women with employer-sponsored insurance an average of USD 20,416, which includes USD 2,743 out-of-pocket, with vaginal deliveries being USD 15,712 and cesarean births reaching USD 28,998. In addition, the article also mentions infant healthcare with toddlers in their first two years, averaging USD 16,575 in medical costs. NICU admissions increase the spending, with infants admitted to the highest-level NICU incurring around USD 117,878 in total costs, thus underscoring the urgent need for affordable and cost-effective care devices in the market.

Pregnancy and Childbirth Costs by Delivery Type and Insurance Coverage 2021 - 2023

Source: HST

Key Neonatal and Prenatal Devices Market Insights Summary:

Regional Highlights:

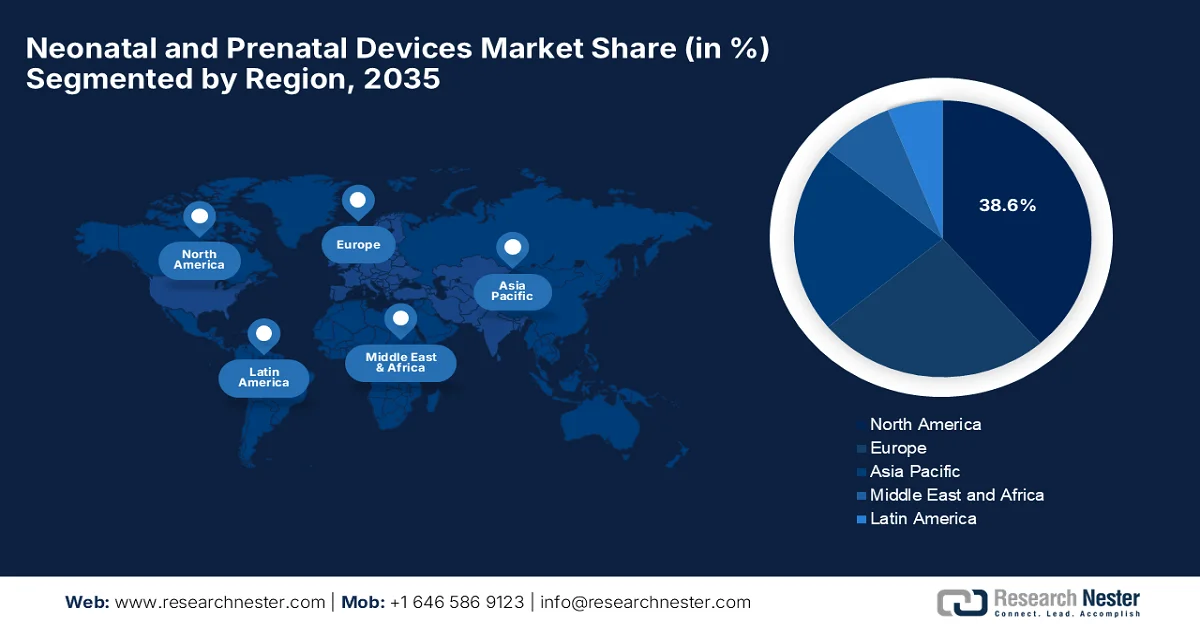

- The neonatal and prenatal devices market in North America is anticipated to account for a dominant 38.6% share by 2035, reinforced by the region's highly advanced healthcare infrastructure comprising well-established NICUs, tertiary care hospitals, and broad access to screening and monitoring technologies

- Asia Pacific is poised to witness the fastest expansion in the market during 2026-2035, spurred by surging investments in healthcare infrastructure across public and private sectors

Segment Insights:

- The non-invasive segment is anticipated to secure a considerable revenue share in the neonatal and prenatal devices market by 2035, stimulated by the increasing clinical preference for safer diagnostic approaches that reduce fetal exposure to invasive procedures and associated risks

- The hospital segment is projected to hold a noteworthy share by 2035, accelerated by the growing concentration of high-risk deliveries and preterm birth cases requiring specialized intensive care environments

Key Growth Trends:

- Technological evolution

- Expansion of NICUs

Major Challenges:

- Reimbursement and funding constraints

- Shortage of skilled healthcare professionals

Key Players: GE HealthCare, Koninklijke Philips N.V., Medtronic plc, Siemens Healthineers AG, Drägerwerk AG & Co. KGaA, Natus Medical Incorporated, Fisher & Paykel Healthcare Limited, Masimo Corporation, Atom Medical Corporation, Becton, Dickinson and Company, Getinge AB, NeoLight, Advanced Healthcare Technology Ltd, Canon Medical Systems Corporation, CooperSurgical, Inc.

Global Neonatal and Prenatal Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 8.8 billion

- 2026 Market Size: USD 9.4 billion

- Projected Market Size: USD 17.1 billion by 2035

- Growth Forecasts: 6.9 % CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.6% share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Thailand, Australia

Last updated on : 24 June, 2026

Neonatal and Prenatal Devices Market - Growth Drivers and Challenges

Growth Drivers

- Technological evolution: The continued product developments by leading pioneers drive extensive growth in the neonatal and prenatal devices market globally. The innovations in terms of non-invasive monitoring, portable incubators, and AI-enabled fetal tracking systems enhance diagnostic accuracy and patient outcomes. For instance, in February 2024, GE HealthCare announced that its Novii+ Wireless Maternal and fetal monitoring solution had received FDA clearance to monitor pregnant patients from 34 weeks onward, covering about 95% of eligible U.S. births. This belt-free, wireless patch tracks fetal heart rate, maternal heart rate, and uterine activity, thereby enabling mobility and comfort during labor while ensuring reliable, real-time monitoring, thus positively contributing to the market’s expansion.

- Expansion of NICUs: This, coupled with the expansion of hospital infrastructure worldwide, is a major boosting factor for the market. Rising investments in advanced medical facilities, especially in emerging economies, support the adoption of high-end prenatal and neonatal devices. As per an article published by the National Institute of Health (NIH) in May 2023, it identified 1,424 NICUs in the U.S., showing a highly expanded and stratified neonatal care infrastructure with Level II, III, and IV units distributed across regions. It found that higher-acuity NICUs and greater bed capacity were strongly associated with academic medical centers, children’s hospitals, and states with certificate of need regulations, reflecting structural healthcare investment patterns, thus suitable for bolstering the market’s growth.

Challenges

- Reimbursement and funding constraints: In most of the countries, inadequate reimbursements and limited healthcare funding hamper the growth of the neonatal and prenatal devices market. Hospitals and healthcare providers often analyze capital equipment purchases based on reimbursement potential and return on investment. Therefore, if the reimbursement rates fail to adequately cover the costs of equipment or procedures, healthcare institutions may postpone equipment upgrades or limit technology investments. This issue is particularly visible in emerging economies, in which healthcare budgets are constrained, and insurance coverage is limited. In this context, any type of variation in reimbursement frameworks across regions also creates uncertainty for manufacturers who are looking for market expansion.

- Shortage of skilled healthcare professionals: This is yet another aspect hampering the growth of the market. The effective use of neonatal and prenatal devices depends on the availability of trained healthcare professionals who are capable of operating this equipment and interpreting clinical data accurately. Most of the regions are still facing a shortage of neonatologists, obstetricians, fetal medicine specialists, neonatal nurses, and biomedical technicians. In addition, the complexity associated with modern monitoring systems, imaging technologies, and neonatal intensive care equipment increases the need for specialized training. Apart from this, inadequate knowledge can result in underutilization of advanced devices, diagnostic inaccuracies, delayed interventions, and reduced patient outcomes, causing severe hindrance to the market’s upliftment.

Neonatal and Prenatal Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.9% |

|

Base Year Market Size (2025) |

USD 8.8 billion |

|

Forecast Year Market Size (2035) |

USD 17.1 billion |

|

Regional Scope |

|

Neonatal and Prenatal Devices Market Segmentation:

Product Type Segment Analysis

Under the product type segment, prenatal and fetal equipment is forecasted to lead with a total share of 61.6% in the neonatal and prenatal devices market during the discussed timeframe. The segment’s dominance is effectively attributable to the increasing global emphasis on early diagnosis and continuous fetal monitoring, which has significantly improved pregnancy management outcomes. In November 2023, Philips secured a USD 60 million investment from the Bill & Melinda Gates Foundation in order to accelerate AI-powered ultrasound development on its Lumify Handheld Ultrasound. This innovation simplifies pregnancy diagnostics, reducing training time from weeks to hours, enabling midwives and frontline workers to detect abnormalities earlier.

Technology Segment Analysis

On the basis of technology, non-invasive is anticipated to grow with a considerable revenue share in the neonatal and prenatal devices market by the conclusion of 2035. The growth of the segment is mainly propelled by increasing clinical preference for safer diagnostic approaches that reduce fetal exposure to invasive procedures and associated risks. Healthcare providers across different nations are progressively shifting toward screening methods that enable proper assessment without disrupting maternal or fetal stability. For instance, in August 2025, the U.S. Food & Drug Administration (FDA) reported the clearance of Sentec AG’s LuMon™ System (K243765), a Class II ventilatory electrical impedance tomograph, for market distribution. This non-invasive device was deemed equivalent to legally marketed predicate devices, which allows commercialization under the general controls provisions of the Food, Drug, and Cosmetic Act.

End user Segment Analysis

By the end of the forecast period, the hospital segment is expected to hold a noteworthy share in the market. The increasing concentration of high-risk deliveries and preterm birth cases requiring specialized intensive care environments is the main factor responsible for the segment's leadership. Hospitals are the primary settings that are equipped with advanced NICUs, surgical backup, and multidisciplinary neonatal teams, which are essential for managing complex maternal-fetal conditions. In September 2025, Rainbow Children’s Medicare Limited (RCML) announced the launch of a new 100-bed greenfield hospital in Rajahmundry, Andhra Pradesh. The hospital will provide advanced pediatric and perinatal care, which includes NICU, PICU, high-risk obstetrics, and fertility services under BirthRight by Rainbow.

Our in-depth analysis of the neonatal and prenatal devices includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Technology |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Neonatal and Prenatal Devices Market - Regional Analysis

North America Market Insights

North America neonatal and prenatal devices market is anticipated to garner the highest share of 38.6% during the forecast period. The region’s leadership is mainly attributable to its highly advanced healthcare infrastructure, including a dense network of tertiary care hospitals, well-established NICUs, and enhanced access to screening and monitoring technologies. The existence of this strong clinical ecosystem supports early diagnosis and effective management of high-risk pregnancies and neonatal complications. In August 2024, the U.S. FDA reported that its pediatric and perinatal devices program conducts regulatory science research to make sure safe and effective medical devices for children and mothers during pregnancy and childbirth. This program develops certain testing methods, datasets, and computational models to close gaps such as limited device availability, lack of suitable designs, and high development costs, thereby ultimately supporting innovation and access in pediatric and maternal care.

The expanding clinical infrastructure, high rates of NICU admissions, and consistent demand are uplifting the U.S. neonatal and prenatal devices market. Market growth is primarily driven by government support and the rapid clinical integration of advanced technologies that offer automated thermoregulation. In May 2026, the U.S. Department of Health and Human Services announced the launch of Moms.gov as a first-of-its-kind platform to support new and expecting mothers. The site provides resources on pregnancy centers, Federally Qualified Health Centers, nutrition, mental health, breastfeeding, adoption, and more, also introducing tools such as Trump Accounts and Trump Rx. thus, strengthening maternal and infant health outcomes. With such support, the country is anticipated to witness exceptional growth in the next decade.

In Canada, the neonatal and prenatal devices market has gained immense exposure, mainly propelled by the country’s robust public healthcare framework and a strong institutional commitment to minimizing infant mortality rates. Market expansion is also driven by the modernization of provincial hospital networks and the integration of digital health infrastructure, which deliberately facilitates the adoption of wireless fetal telemetry and smart connected incubators. Based on the government data published in January 2026, the Community Action for Prenatal and Child Health Program funds nearly 495 projects on a yearly basis, thereby serving more than 230,000 pregnant people, young children aged 0 to 6, and caregivers across Canada. It unifies the Canada Prenatal Nutrition Program and the Community Action Program for Children by focusing on families facing poverty, isolation, systemic barriers, or challenges such as teen pregnancy and substance use.

APAC Market Insights

The Asia Pacific market is projected to grow at the fastest rate from 2026 to 2035. The region’s upliftment is mainly propelled by surging investments in healthcare infrastructure across both public and private sectors. Market growth is also being driven by rising disposable incomes, expanding medical insurance coverage, and proactive government health mandates, which are targeting early newborn screening. Based on the government data published in February 2026, a perinatal telemedicine project refined in Thailand and later adopted in Japan is saving lives by enabling real-time fetal monitoring at home through the iCTG device. This particular system uses two heart-shaped sensors to track fetal heartbeat and uterine contractions, transmitting data directly to hospitals for physician review, thus denoting a positive market outlook.

Government support with suitable subsidy programs and a focus on optimizing maternal and infant health outcomes are driving the growth of the neonatal and prenatal devices market in China. There is a rising trend in pregnancies among older demographics, which increases the clinical demand for advanced prenatal screening and continuous fetal monitoring systems. The country’s market is also benefiting from a strong domestic shift toward localized manufacturing of high-tech medical equipment, which accelerates the nationwide adoption of digital incubators and smart phototherapy devices. Based on the government data published in December 2025, China has announced plans to make childbirth essentially free under national medical insurance to reduce family financial burdens and foster a birth-friendly society. Seven provinces, including Shandong, already offer full coverage for standard hospital deliveries, with typical out-of-pocket costs dropping to USD 141.53 below, thus driving extensive usage of neonatal and prenatal devices.

Rising maternal age in urban areas and nationwide initiatives to reduce the neonatal mortality rate are accelerating the growth of the market in India. Market expansion is propelled by public healthcare programs along with a booming private healthcare sector expanding its premium neonatal intensive care unit footprints. As stated by Press Information Bureau (PIB) in May 2026, the country’s Union Health Ministry launched JANANI (Journey of Antenatal, Natal and Neonatal Integrated Care), which is a digital platform to strengthen maternal and child healthcare in India. The platform’s key features include QR-enabled MCH cards, automated alerts for high-risk pregnancies, and interoperability with platforms such as U-WIN and POSHAN. Hence, such instances drive demand for neonatal and prenatal devices by enabling integration, monitoring, and data-driven adoption.

India Ultrasound Machine Shipments by Country in 2023: Leading Suppliers, Import Value, and Trade Analysis

|

Exporting Country |

Import Value (USD Thousand) |

Quantity (Items) |

|

China |

89,845.50 |

1,160,950 |

|

Korea, Rep. |

65,186.82 |

87,783 |

|

U.S. |

25,776.01 |

12,971 |

|

Austria |

10,715.95 |

1,647 |

|

Italy |

8,802.52 |

858,845 |

|

Japan |

4,835.51 |

16,337 |

|

Norway |

3,062.43 |

326 |

|

Denmark |

1,988.64 |

642 |

|

France |

1,747.73 |

1,503 |

|

Germany |

1,425.49 |

20,848 |

Source: WITS

Europe Market Insights

The Europe market is progressing steadily owing to the presence of favorable universal reimbursement frameworks and clinical adoption of digital healthcare solutions. The region benefits from strict guidelines that mandate universal newborn screening for metabolic and congenital disorders, thereby ensuring consistent procurement of diagnostic devices across both public hospitals and private maternity clinics. In November 2023, at RSNA 2023, Philips introduced a suite of AI-enabled innovations that are especially designed to ease radiology workflows and improve patient care. Some of the highlights included next-generation ultrasound systems that boost diagnostic confidence, the world’s first mobile MRI with helium-free operations, and cloud-based PACS solutions integrating over 100 AI applications. Hence, such instances denote the industry’s shift towards integrated diagnostic ecosystems that improve workflow and maternal–fetal outcomes across healthcare systems.

A highly structured clinical guidelines and statutory health insurance framework that guarantees universal access to maternal-fetal care are fueling growth in the Germany neonatal and prenatal devices market. The country’s technological transition is being accelerated by substantial federal investments in hospital digitalization and the presence of prominent domestic medical engineering firms that prioritize the deployment of interconnected intensive care solutions. In May 2023, Siemens Healthineers announced a generous investment of USD 86 million to build a new semiconductor crystal factory in Forchheim, Germany, to expand capacity for photon-counting CT scanners such as the Naeotom Alpha. These cadmium telluride crystals enable sharper imaging with reduced radiation dose, addressing rising demand, thus contributing to the industry’s growth.

The UK neonatal and prenatal devices market has a strong opportunity to grow in the next decade, owing to the National Health Service (NHS) framework's strong focus on modernizing maternity services. Market growth is largely fueled by targeted government funding initiatives aimed at upgrading obstetric and pediatric units, which accelerate the procurement of next-generation fetal monitors, smart incubators, and advanced neonatal ventilators. Based on the government data published in April 2023, NHS England’s three-year delivery plan for maternity and neonatal services from 2023–2026 focuses on making care safer, more personalized, and equitable for women, babies, and families. In addition, its implementation relies on the dedication of maternity and neonatal teams across England, with a collective goal to improve outcomes and ensure consistent, high-quality care.

Key Neonatal and Prenatal Devices Market Players:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Medtronic plc (Ireland)

- Siemens Healthineers AG (Germany)

- Drägerwerk AG & Co. KGaA (Germany)

- Natus Medical Incorporated (U.S.)

- Fisher & Paykel Healthcare Limited (New Zealand)

- Masimo Corporation (U.S.)

- Atom Medical Corporation (Japan)

- Becton, Dickinson and Company (U.S.)

- Getinge AB (Sweden)

- NeoLight (U.S.)

- Advanced Healthcare Technology Ltd (UK)

- Canon Medical Systems Corporation (Japan)

- CooperSurgical, Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- GE HealthCare is one of the leading providers that offer fetal monitoring, neonatal incubators, warmers, phototherapy systems, resuscitation equipment, and perinatal digital solutions. In addition, the company has also expanded into digital health through CareIntellect™ for Perinatal, which is a cloud-based application that improves clinical workflows in maternal and fetal care.

- Koninklijke Philips N.V. is yet another foundational player in this sector, which leads with its integrated mother-and-child care solutions. Besides, the firm emphasizes support for mothers and infants before, during, and after birth, with fetal and maternal monitoring systems, developmental care solutions, neonatal positioning products, feeding solutions, and NICU support technologies.

- Siemens Healthineers AG has registered itself as a major participant in the prenatal diagnostics segment, primarily through its advanced ultrasound imaging portfolio. The company’s women’s health solutions are focused on delivering high-quality imaging for obstetric and gynecological applications.

- Drägerwerk AG & Co. KGaA has been recognized globally for its specialized neonatal intensive care solutions. The company is extensively focused on creating integrated NICU environments through incubators, radiant warmers, neonatal ventilators, monitoring systems, and jaundice management solutions.

- Fisher & Paykel Healthcare Limited is a leading specialist in neonatal respiratory care. The company deliberately develops and manufactures products for infant resuscitation, invasive ventilation, continuous positive airway pressure therapy, nasal high-flow therapy, and respiratory humidification.

Here is a list of key players operating in the global market:

The global neonatal and prenatal devices market is being led by pioneers such as GE HealthCare, Philips, Medtronic, Siemens Healthineers, and Dräger, who are intensely contending through innovations and strong distribution networks. Companies are also making investments in terms of AI-enabled fetal monitoring, connected neonatal intensive care systems, wireless monitoring solutions, and digital healthcare platforms with the main goal of improving clinical outcomes and workflow efficiency. Mergers and acquisitions, partnerships with healthcare providers, and expansion of manufacturing capabilities are certain strategies opted for by the market participants to secure their market positions. For instance, in February 2026, Natus Sensory entered a multi-year tactical partnership with Canadian Hospital Specialties in order to expand access to newborn care solutions across Canada. This collaboration is also focused on education, adoption, and long-term clinical support across hearing, vision, phototherapy, and NICU connectivity.

Corporate Landscape of the Market:

Recent Developments

- In January 2026, NeoLight entered into a partnership with Advanced Healthcare Technology Ltd to expand its neonatal ecosystem in the U.S., distributing innovative transport and thermal regulation devices to hospitals. This collaboration strengthens NeoLight’s portfolio with solutions such as the NeoPod, BP37 temperature maintenance kit, and ScanPod, enhancing safety and efficiency in newborn care.

- In June 2025, Getinge expanded its Servo-c ventilator with a neonatal option, making it a universal solution for respiratory care across all patient categories. The new feature supports premature babies as small as 500 grams, thereby offering advanced safety and flexibility without extra accessories.

- In April 2024, GE HealthCare received FDA clearance for its Portrait VSM vital signs monitor, which measures blood pressure, pulse, oxygen saturation, temperature, and respiratory rate, integrating seamlessly with EMRs and Portrait Mobile for continuous monitoring.

- Report ID: 1336

- Published Date: Jun 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.