Digital Health Market Outlook:

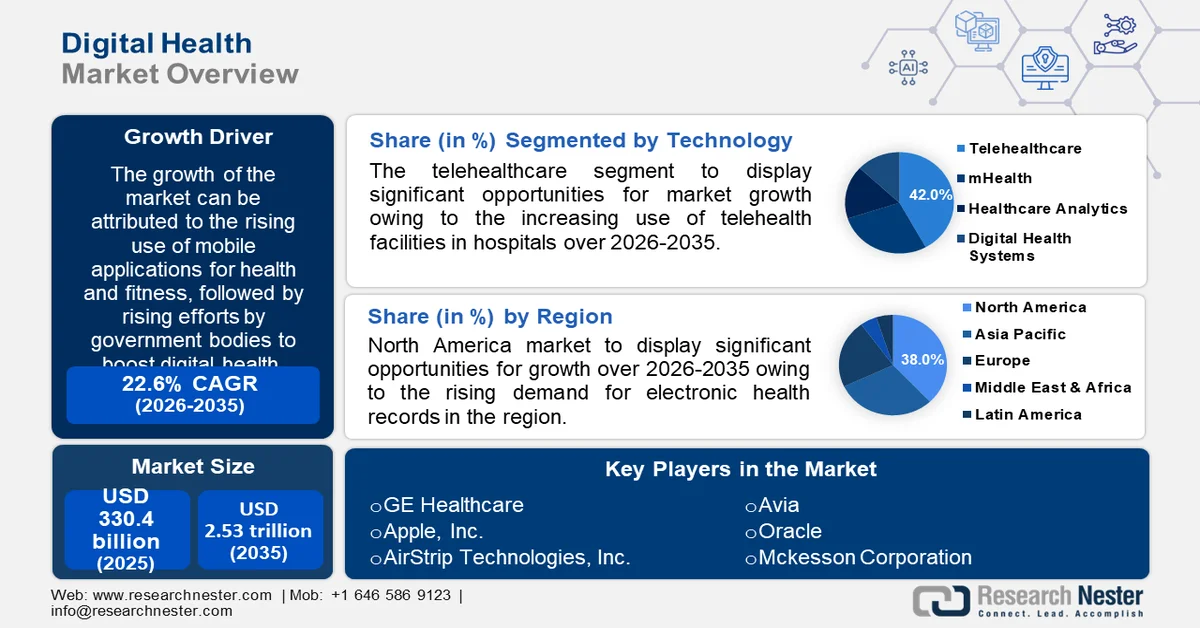

Digital Health Market size was valued at USD 330.4 billion in 2025 and is likely to cross USD 2.53 trillion by 2035, expanding at more than 22.6% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of digital health is assessed at USD 397.6 billion.

The market growth is driven by rising use of mobile applications for health and fitness, followed by rising efforts by government bodies to boost the digital health. For instance, more than 318,000 health apps were available for download in 2018 nearly twice as many as there were in the biggest app stores in 2015 across the globe. Also, United Nations and the World Health Organization introduced a General Plan of Work, 2019-2023, which involves accelerating the creation, expansion, and use of digital health solutions.

In addition, Growing adoption of telehealth services and the rising use of smartphones by experts will propel the market revenue. Numerous telemedicine solutions, including websites, robots, and chatbots, enable virtual doctor visits and primary care, e-prescriptions, remote patient monitoring, and screening in real-time, all of which is playing a crucial role in providing timely attention to the patient. Almost 25% of doctors use mobile devices to provide patient care, and 4 out of 5 doctors use them to help with their daily tasks. Furthermore, telemedicine has become 50% more popular in behavioral health for scheduling virtual consultation with counsellors, psychologists, and other behavioral health.

Key Digital Health Market Insights Summary:

Regional Highlights:

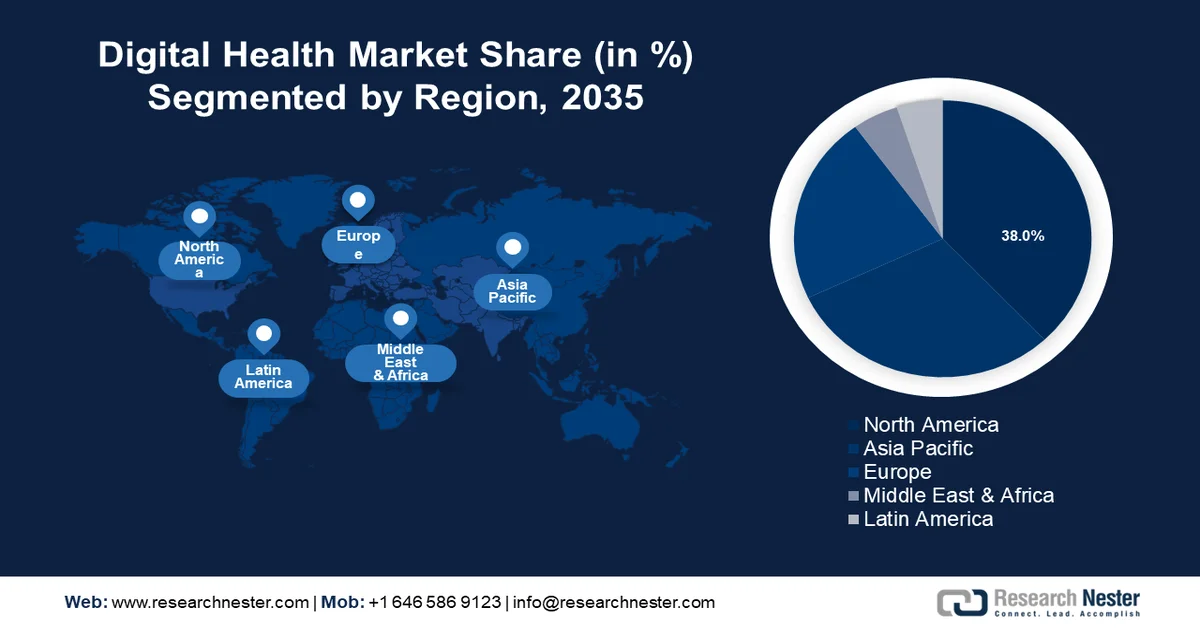

- The North America region is projected to hold a dominant 38% share of the digital health market by 2035, impelled by rising demand for electronic health records and expanding telehealth utilization.

- Asia Pacific is anticipated to witness lucrative CAGR growth in the market during 2026–2035, fueled by accelerating adoption of fitness applications and increasing digitization of healthcare infrastructure.

Segment Insights:

- The telehealthcare segment in the digital health market is projected to command the largest share by 2035, driven by expanding integration of telehealth facilities across hospitals.

- The software segment is expected to secure a significant share of the market by 2035, propelled by continuous introduction of advanced digital healthcare software platforms.

Key Growth Trends:

- Growing Use of Smartphones, Laptops, & Tablets

- Rise in the Number of People Using Fitness Wearable Devices

Major Challenges:

- Digital Health Implementation Requires High Investment

- Need for Frequent Maintenance of the Software and Hardware

Key Players: Bekaert S.A., IntraMicron, Inc., V. Bekaert S.A., PPG Industries Ohio Inc., Fiberguide Industries Limited, Fibrometals SRL, Green Steel Group, MBC Metal Limited, Nippon Seisen Co., Ltd, BinNova Metal Fiber Technology GmbH.

Global Digital Health Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 330.4 billion

- 2026 Market Size: USD 397.6 billion

- Projected Market Size: USD 2.53 trillion by 2035

- Growth Forecasts: 22.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: China, India, Japan, Germany, Brazil

Last updated on : 25 February, 2026

Digital Health Market - Growth Drivers and Challenges

Growth Drivers

- Growing Use of Smartphones, Laptops, & Tablets – The mobile health, or mHealth, the business has grown as mobile devices become more and more used in healthcare. In fact, 74% of hospitals are more effective than those that don't use mobile devices to gather patient data around the world. Moreover, around 84% of healthcare professionals utilize mobile devices to support patients after they leave the hospital.

- Rise in the Number of People Using Fitness Wearable Devices - Wearable medical gadgets are made to gather information about users' personal health and exercise. They can even transmit a patient's health data in real time to a physician or other healthcare expert. More than 445 million wearable fitness devices were supplied to consumers in 2020 worldwide, and the epidemic contributed to a more than 31% increase in fitness tracker revenue.

- Favorable Government Initiatives for Digital Healthcare – Higher government efforts is expected to boost the market growth. The National Digital Health Mission (NDHM) was launched by the Ministry of Health and Family Welfare of the Government of India in August 2020 with the goal of offering essential assistance for the integration of digital health infrastructure throughout the nation.

- Growing Use of Electronic Health Record (EHR)– Around 97% of doctors electronically recorded BDOH data in 2021, while 85% of doctors electronically recorded SDOH data. Compared to other medical professionals, primary care physicians electronically collected SDOH and BDOH data at a higher rate.

- Rising Benefits of Digital Healthcare Systems– By utilizing contemporary, digital information and communication technologies in healthcare, around 1 billion individuals around the world are anticipated to receive better healthcare services and better attention during emergencies.

Challenges

- Digital Health Implementation Requires High Investment

- Need for Frequent Maintenance of the Software and Hardware

- Rising danger of data theft- Data security is the top worry for healthcare firms. As medical services become more digital, the risk of security breaches, data thefts, and fraud has increased. Any kind of cyberattack can result in the loss of private and sensitive patient health data. Hence, growing anxiety over data theft is predicted to impede market expansion. Attacks on the healthcare system affected 45 million people in 2021, up from 34 million in 2020 in the United States

Digital Health Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

22.6% |

|

Base Year Market Size (2025) |

USD 330.4 billion |

|

Forecast Year Market Size (2035) |

USD 2.53 trillion |

|

Regional Scope |

|

Digital Health Market Segmentation:

Technology Segment Analysis

The telehealthcare segment is estimated to gain the largest digital health market share by 2035, propelled by increasing use of telehealth facilities in hospitals. The advantages of telehealth include less risk of contracting diseases, improved access to care, and patient convenience. During the pandemic, hospitals increased the use of telehealth, virtual visits, video conversations, patient portals, and remote monitoring equipment. Compared to around 8% in 2017, nearly 26% of providers surveyed indicated telehealth is their organization's main agenda for 2022. Furthermore, in a study of 254 patients at Massachusetts General Hospital concerning telemedicine consultations, around 80% gave them an excellent rating for effectiveness and communication, and nearly 82% said they would suggest them to relatives and friends.

Component Segment Analysis

The software segment is expected to garner a significant digital health market share by 2035. Digital healthcare software is seen as a practical and affordable way to quicken the pace of digital innovation, helping providers to promote productivity, increase revenue, enhance the experience of both the patient and employee, and improve care quality. The segment growth is also attributed to introduction of new software. For instance, in March 2022, GE Healthcare announced to launch Edison Digital Health Platform, which is advanced software that is created to provide holistic views of each patient and support integrated care pathway management by gathering information from numerous sources and vendors to enhance clinical applications.

Our in-depth analysis of the global market includes the following segments:

|

By Technology |

|

|

By Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Digital Health Market - Regional Analysis

North American Market Insights

The North American digital health market is estimated to account for majority revenue share of 38% by 2035. The market growth can be attributed to rising demand for electronic health records. Around 86% of non-Federal general acute care hospitals had adopted a 2015 Edition certified electronic health record, according to statistics from 2019 and 2021. (EHR). Comparatively, only 23% of specialty hospitals and 40% of rehab hospitals are using the HER. In addition to this, the growing use of telehealth services is also expected to augment the market growth in the region. In the United States, telehealth utilization increased from about 51% in February 2019 to over 62% in March 2021.

APAC Market Insights

The Asia Pacific digital health market is expected to grow at a lucrative CAGR during the forecast period, due to growing use of fitness apps. India saw the largest growth of 156% for health and fitness apps between Q1 and Q2 2020. Moreover, between 2020 and 2021, 76 million health applications were downloaded in India, a 38% rise over the previous year. In addition to this, the most well-liked medical app in China as of December 2021 was Ping An Good Doctor, which had about 12 million active monthly users. Besides this, the rising penetration of digitization in healthcare will boost the market expansiob. In India, over 80% of respondents are willing to increase their budget for digital healthcare and IT infrastructure in order to get better outcomes.

Europe Market Insights

Further, the market in the Europe is poised to hold significant share by the end of , propelled by increasing use of telehealth and telemedicine, owing to their benefits. In Germany, telemedicine interventions have reduced hospital admissions, decreased all-cause mortality for patients with heart failure, and increased quality of life. Furthermore, the regional market growth is also ascribed to rising use of the internet by people to solve health-related queries. According to the Eurostat ICT household survey, in the first quarter of 2020, 55% of EU citizens aged 16 to 74 conducted online searches for health-related information.

Key Digital Health Market Players:

-

GE Healthcare

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Avia

- Oracle

- Mckesson Corporation

- Epic Systems Corporation

- Samsung Electronics Co., Ltd.

- Apple, Inc.

- AirStrip Technologies, Inc.

- Qualcomm Technologies, Inc.

- CISCO Systems, Inc.

Recent Developments

-

AVIA announces the launch of AVIA Marketplace, the innovative platform for innovators at health systems to examine, verify and choose the best digital health solutions. The platform connects providers of digital health solutions with those who need their products and services, enabling providers to reach relevant clients.

-

GE Healthcare announce the collaboration with Tribun Health with the aim to integrate Tribun's Health Suite data with GE Healthcare's products to provide a data management solution.

- Report ID: 993

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.