Semiconductor Foundry Market Outlook:

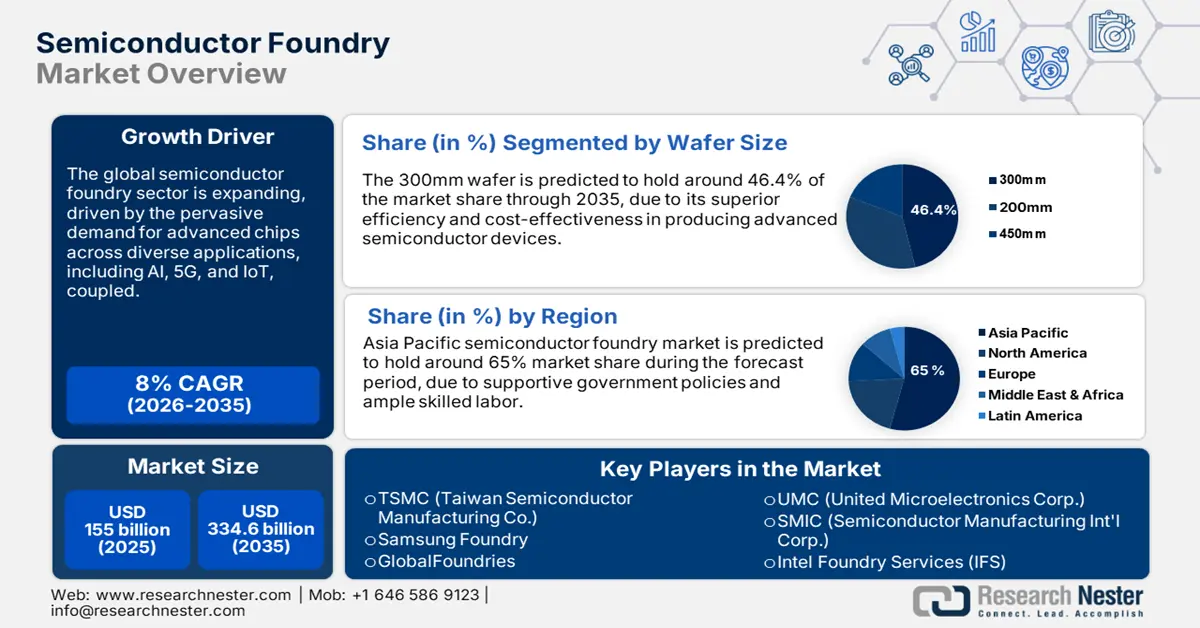

Semiconductor Foundry Market size is valued at USD 155 billion in 2025 and is projected to reach a valuation of USD 334.6 billion by the end of 2035, rising at a CAGR of 8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of semiconductor foundry is assessed at USD 167.4 billion.

The global semiconductor foundry sector is expanding rapidly, driven by a competition for technological sovereignty and robust global supply chains. The semiconductor industry is a critical national security and economic policy imperative for countries, moving beyond commercial rivalry. This is underscored by the launch of Intel Foundry in February 2024, marking the world's first systems foundry. The move quickly gained the approval of Microsoft's CEO, who announced that the company had selected Intel's 18A process for an upcoming custom chip product. This highlights a reality in which foundries are no longer factories but strategic allies of vital necessity to innovation.

The market expansion is being driven by massive government investments in re-shoring and diversifying chip production capacities. These programs are already yielding tangible dividends in the U.S., with the number of semiconductor industry plants rising at a significant rate. This is solely due to policy efforts like the CHIPS and Science Act, which, in April 2024, negotiated a first agreement with TSMC for as much as USD 6.6 billion in financing to enable its greater investment in Arizona, an outstanding collaboration between public policy and private industry that is reshaping the world's geography of semiconductor production.

Key Semiconductor Foundry Market Insights Summary:

Regional Highlights:

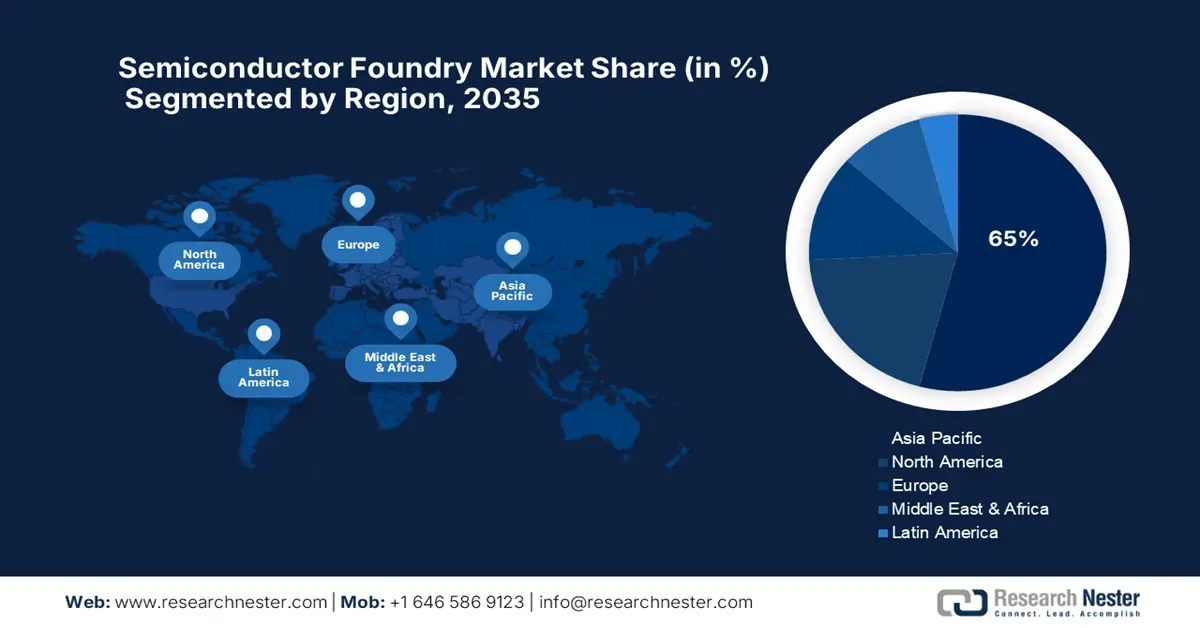

- By 2035, the Asia Pacific semiconductor foundry market is expected to retain nearly 65% share, underpinned by the extensive scale and efficiency of leading foundries in Taiwan and South Korea along with expanding Chinese manufacturing.

- North America is projected to post a 13% CAGR from 2026–2035, bolstered by unprecedented public–private investments expanding advanced semiconductor production capacity across the region.

Segment Insights:

- The 7nm segment is projected to command a dominant 62.5% share by 2035 in the semiconductor foundry market, propelled by its pivotal role in high-volume consumer, automotive, and data-center applications.

- The 300mm wafer segment is anticipated to hold about 46.4% share through 2035, supported by its higher surface-area efficiency and sustained global investments expanding 300mm fabrication capacity.

Key Growth Trends:

- Geopolitical reshoring and state subsidies

- Spike in AI and high-performance computing

Major Challenges:

- Enormous capital cost and execution risk

- Managing export controls and international trade

Key Players: TSMC (Taiwan Semiconductor Manufacturing Co.), Samsung Foundry, GlobalFoundries, UMC (United Microelectronics Corp.), SMIC (Semiconductor Manufacturing Int'l Corp.), Intel Foundry Services (IFS), STMicroelectronics, Tower Semiconductor, Tata Elxsi, ViTrox Corporation Berhad, Telstra, Infineon Technologies AG.

Global Semiconductor Foundry Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 155 billion

- 2026 Market Size: USD 167.4 billion

- Projected Market Size: USD 334.6 billion by 2035

- Growth Forecasts: 8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (65% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Taiwan, South Korea, Japan

- Emerging Countries :India, Vietnam, Singapore, Germany, Malaysia

Last updated on : 21 August, 2025

Semiconductor Foundry Market - Growth Drivers and Challenges

Growth Drivers

- Geopolitical reshoring and state subsidies: Among the principal drivers of expansion is the global push by governments to fortify regional semiconductor manufacturing, sparked by supply chain risk concerns and national security apprehensions. This has unleashed a tsunami of subsidies and strategic investment, spearheaded by the U.S. CHIPS and Science Act. In March 2024, the US administration announced a prospective agreement to provide Intel up to USD 8.5 billion in direct funding and $11 billion in lending to support its colossal growth plans in Arizona, Ohio, New Mexico, and Oregon, directly accelerating the construction of fresh, cutting-edge foundry capacity in American soil.

- Spike in AI and high-performance computing: The increasing demand for computer capacity driven by the AI explosion is forcing an increase in the production and manufacturing of the next-generation logic chips at a pace that is inducing foundries to invest in cutting-edge process nodes like 5nm, 3nm, and higher to produce the high-end GPUs, TPUs, and AI accelerators utilized for such purposes. Intel's official launch of Intel Foundry in February 2024 was geared to meet this demand, heralding itself as the globe's first systems foundry for the era of AI and emphasizing how AI has become a prominent aspect of industry-leading foundry technology.

- New centers for manufacturing: International efforts to de-risk supply chains are driving the unprecedented emergence of new semiconductor manufacturing clusters in geographies historically not known for advanced manufacturing. India is a particularly striking example, with government incentives attracting significant investment. For example, the Government of India sanctioned in February 2024 the establishment of three giant semiconductor facilities with a total investment of about $15.2 billion. This is India's first commercial semiconductor fab, a Tata Electronics and Powerchip Taiwan joint venture, which marks the entrance of a new significant player in the global foundry industry.

Challenges

- Enormous capital cost and execution risk: The semiconductor foundry industry is marked by huge capital cost and high execution risk, with one advanced fab costing tens of billions of dollars and years to construct. Such massive undertakings are prone to delays from the supply chain, build complexities, and sheer technical difficulty of ramping new process nodes to high-volume production. In August 2023, TSMC revealed a joint venture for the construction of a fab in Dresden, Germany, with total planned investment in excess of €10 billion, an amount that indicates the staggering capital outlay necessary to compete at the highest level.

- Managing export controls and international trade: The foundry industry operates in a complex and often hostile geopolitical environment, with access to markets and technology increasingly subject to national security-driven export regulation. Regulations pose massive compliance challenges and have the potential to dismantle established business relationships and supply chains, forcing businesses to operate in a challenging and unpredictable landscape.

Semiconductor Foundry Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8% |

|

Base Year Market Size (2025) |

USD 155 billion |

|

Forecast Year Market Size (2035) |

USD 334.6 billion |

|

Regional Scope |

|

Semiconductor Foundry Market Segmentation:

Technology Node Segment Analysis

The 7nm segment is anticipated to command a dominant 62.5% market share during the forecast period as it serves as the workhorse node for a broad spectrum of high-volume applications in consumer, automotive, and data center markets. While players are competing to get to 3nm and 2nm, foundries are committing to somewhat more mature nodes to enable a large customer volume. This strategy was followed up in January 2024 when UMC and Intel jointly announced the development of a 12-nanometer FinFET process platform. Through this partnership, UMC customers will be provided with a new, U.S.-based supply source for an advanced and cost-saving node, demonstrating the continued strategic importance of producing capacity below the absolute leading edge to meet the diverse needs of the market.

Wafer Size Segment Analysis

The 300mm wafer is predicted to hold around 46.4% of market share through 2035, considering it is the default standard for modern, high-volume semiconductor manufacturing. A higher surface area of the 300mm wafer compared to its 200mm version allows for more chips to be produced in each production run. Industry commitment to the 300mm standard is demonstrated by the tsunami of new fab projects being built globally. In February 2023, UMC commenced construction on its new Fab12i P3 fab in Singapore, a USD 5 billion investment to expand the company's 300mm wafer capacity for its 22/28nm processes. This project, whose manufacturing is due to commence in 2025, is a characteristic pointer that 300mm will remain the dominant wafer size for the foreseeable future, the foundation of the next generation of semiconductor manufacturing.

Our in-depth analysis of the semiconductor foundry market includes the following segments:

|

Segment |

Subsegments |

|

Technology Node |

|

|

Application |

|

|

Wafer Size |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Semiconductor Foundry Market - Regional Analysis

APAC Market Insights

Asia Pacific semiconductor foundry market is anticipated to maintain around 65% market share during the forecast period. The region's leadership is based on the record size and efficiency of foundries in Taiwan and South Korea, which produce the overwhelming majority of the world's most advanced logic chips. These are supplemented by a huge and highly integrated equipment and materials supply chain, and a strong and growing base of Chinese manufacturing.

China is aggressively pursuing technological independence in semiconductors, backed by a long-term national policy and massive state-guided investment. This aims to reduce foreign dependence on technology and develop an entirely indigenous supply chain for both mature and advanced nodes. In a firm demonstration of this, the government established its third and largest national integrated circuit industry investment fund in May 2024. With a registered capital of approximately USD 47.5 billion, its new Big Fund is dedicated to accelerating the country's push towards making its semiconductor dreams a reality.

India is emerging as a significant player in the semiconductor foundry market, driven by the government's ambitious plan to welcome investment and foster an indigenous manufacturing ecosystem. The Make in India program and the India Semiconductor Mission are making things favorable for new ventures. Furthermore, new state-of-the-art semiconductor design hubs, such as the cutting-edge 3-nanometer chip design, were set up in Noida and Bengaluru in May 2025. This is a milestone, as India had already achieved 7nm and 5nm designs. Moreover, this step strategically positions India to be a semiconductor innovation and manufacturing center.

North America Market Insights

North America is set to record a strong CAGR of 13% from 2026 to 2035, driven by a record wave of public and private investment that aims to rebalance the continent's semiconductor production on an equal footing with Asia. The U.S. CHIPS and Science Act has released hundreds of billions of dollars in capital, attracting massive investments from the world's leading foundry powers to build new, state-of-the-art fabs. This strategic push to enhance supply chain resilience and re-shore advanced manufacturing is making the region a top semiconductor manufacturing hotspot.

The U.S. is the epicenter of this manufacturing renaissance, and the CHIPS Act is driving a series of new fab announcements. In a landmark deal, the U.S. Department of Commerce reached a tentative accord in April 2024 to provide Samsung with as much as USD 6.4 billion in direct funding. This government support underpins Samsung's massive investment of over USD 40 billion to construct a new complex of state-of-the-art semiconductor facilities in Taylor, Texas, that will introduce state-of-the-art logic production, R&D, and packaging capability to America.

Canada is strategically positioning itself in the North America value chain of semiconductors by building on its strengths in the areas of compound semiconductors, advanced packaging, and R&D. The government is actively building its domestic industry through targeted investments from programs like the Strategic Innovation Fund. In March 2025, the government made a contribution of $8 million to Teledyne for the modernization of its semiconductor tools in its Bromont, Quebec, plant and to establish Canada's position on the global technology supply chain.

Europe Market Insights

Europe is likely to garner significant growth between 2026 and 2035 as a result of the European Chips Act, a multi-billion-euro initiative to double the continent's share in international semiconductor production. The ambitious plan is attracting top investments from world-foundry titans and fostering the growth of the local ecosystem with particular focus on serving the region's strong automobile and industrial sectors. The goal is to enhance Europe's technological autonomy and reduce its reliance on outside chip supplies, and strengthen the industrial base to become more solid and competitive.

Germany is emerging as the hub of Europe's semiconductor production plans with a series of massive investment projects unveiled by the world's leading chipmakers. For instance, Intel and the German Government signed a renewed letter of intent in June 2023 for Intel's planned wafer fabrication plant in Magdeburg. The renewed agreement will see Intel increase its investment to over €30 billion for the plant, which will be significantly subsidized by the government to accommodate Europe's most advanced semiconductor production complex.

The UK is pursuing a targeted strategy focused on leveraging its current strengths in the design of chips, compound semiconductors, and R&D to secure its position in the global supply chain. In May 2023, the UK Government launched its National Semiconductor Strategy, a ten-year plan that commits up to £1 billion over the period. This strategy will cultivate the domestic chip industry by stepping up investment in R&D, improving access to prototyping, and stimulating the development of the UK's leading chip design ecosystem.

Key Semiconductor Foundry Market Players:

- TSMC (Taiwan Semiconductor Manufacturing Co.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Samsung Foundry

- GlobalFoundries

- UMC (United Microelectronics Corp.)

- SMIC (Semiconductor Manufacturing Int'l Corp.)

- Intel Foundry Services (IFS)

- STMicroelectronics

- Tower Semiconductor

- Tata Elxsi

- ViTrox Corporation Berhad

- Telstra

- Infineon Technologies AG

The global semiconductor foundry industry is fiercely competitive, with a few dominant technology companies engaged in competing for process leadership. The industry is dominated by companies such as TSMC (Taiwan Semiconductor Manufacturing Co.), Samsung Foundry, GlobalFoundries, UMC (United Microelectronics Corp.), SMIC (Semiconductor Manufacturing Int'l Corp.), Intel Foundry Services (IFS), and STMicroelectronics. Backing these giants are other prominent players that deal in more advanced but equally crucial process technologies for a wide range of applications.

A significant indicator of the changing competitive landscape is the UK Government's acquisition in October 2024 of a gallium arsenide semiconductor factory specializing in manufacturing bespoke semiconductor components. The factory, now rebranded Octric Semiconductors UK, safeguards around 100 highly skilled jobs and provides a secure domestic supply chain for key components utilized in defense systems. The future outlook for the semiconductor foundry industry promise additional strategic nationalizations and an increased focus on indigenous resilience.

Here are some leading companies in the semiconductor foundry market:

Recent Developments

- In May 2025, Infineon announced that the German Government had issued its final funding approval for the company's new fab in Dresden. This approval includes approximately €1 billion in public funding for the project. Infineon is investing €5 billion of its capital, and the new facility is expected to create as many as 1,000 new high-value jobs. The company reported solid results for the third quarter of its 2025 fiscal year, highlighting opportunities in software-defined vehicles and power solutions for AI data centers.

- In January 2025, GlobalFoundries announced that it would establish a new advanced packaging and photonics center at its Malta campus. The company's existing Fab 8 in Malta produces 400,000 wafers each year, and GlobalFoundries has invested over $15 billion in the site to date.

- Report ID: 3417

- Published Date: Aug 21, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Semiconductor Foundry Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.